Uniswap Fee Switch: Are we finally ready?

The latest proposal (Feb 23, 2024) on Uniswap’s governance forum has reignited discussions on the pivotal “fee switch” mechanism, which could significantly alter Uniswap’s status quo. So, to activate or not activate the fee switch, are we finally ready?

One of the foremost challenges within DeFi is the task of channelling a protocol’s success through its token. The term “useless governance token,” though a meme, highlights a genuine problem within the space.

Uniswap has been one of the most impactful protocols within the DeFi landscape, arguably the most successful and influential decentralised exchange (DEX) to date. However, the token of Uniswap, $UNI, struggles to appreciate. This presents a challenge for both shareholders and governance.

The Growth of Decentralised Exchanges

DEXs are one of the cornerstones of DeFi. They allow different actors to trade and conduct their permissionless operations on-chain without the need to trust 3rd parties, as seen in centralised exchanges (CEXs). Such autonomy cannot be attained without the involvement of key market actors who play a big part in ensuring decentralised exchanges remain well-oiled machines. Their contributions are valuable and essential. So much so that DEXs compete to offer the best reward structure in the form of fees.

For traders, liquidity providers (LPs), and market makers, DEX fees are a subject of debate, preference, and even strategic value. Each DEX offers different incentives for market participants in the form of trading fees and liquidity provider fees. There are also regular gas fees paid to miners in the underlying network, which are not decided by the DEX.

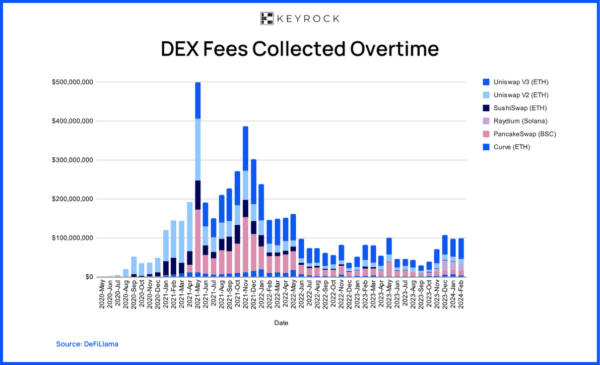

Evidently, trading on DEXs is appealing, which is why they’ve increased in popularity, year-on-year, capturing CEXs market share since DeFi Summer in 2020. The comparison of spot transaction volumes between CEXs and DEXs highlights the escalating appeal of decentralised exchanges, which accounted for 10% of the total volume by 2023.

This increase in DEX usage directly impacts LPs, whose monthly earnings on selected DEXs range between $30 million at the bottom of the bear market and $500 million at the peak of the bull market.

These fees, theoretically, are sufficient to compensate for the opportunity costs, market risks, and smart contract risks faced by LPs.

Uniswap’s Fee Structure

While there are different kinds of fees associated with trading on-chain, such as gas fees, trading fees, or front-end fees, we’re going to focus on trading fees that are fully accrued by LPs.

Uniswap’s fees comprise LP Fees or Swap Fees, paid by traders and accrued by LPs. Uniswap Labs charges a front-end fee for those trading directly through its interface. Finally, Protocol Fees, or the fee switch, divert a portion of LP Fees back to Uniswap itself.

Note that Uniswap Labs is a commercial company, and Uniswap Foundation is a non-profit that focuses on governance and community.

LP Fees or Swap Fee

Every trade on Uniswap incurs a fee. Fees are distributed pro-rata among LPs in a pool.

V1: An LP fee of 0.30% was taken out on each trade and added to the pool’s reserves.

V2: The protocol still applied a 0.30% fee to trades.

V3: Uniswap v3 introduced multiple pools for each token pair, each with different fee tiers. Liquidity providers can create pools at three fee levels: 0.05%, 0.30%, and 1%.

V4: Fee tiers no longer need to be limited thanks to the new hook functionality and the creation of a singleton architecture. Pool creators can set them to the rate they deem the most competitive or personalise them with a dynamic fee hook.

Protocol Fees

Introduced in V2, the “fee switch” mechanism allows a portion of LP fees to be redirected. Fees could be diverted to the protocol’s treasury controlled or potentially to $UNI holders.

In Uniswap V2, the protocol fee rate was fixed at 0.05%, which would be subtracted from the 0.30% LP swap fee, leaving liquidity providers with a 0.25% fee they can redeem.

This feature is deactivated by default and requires consensus from $UNI governance to activate the fee switch. This consensus has not been reached yet.

Uniswap V3 offers more flexibility, allowing governance to set the fee. The protocol fee can be set as 0 or between one-fourth and one-tenth. This value is set at a pool level, so each pool can have an independent protocol fee.

There have been various proposals regarding its activation and rate for Uniswap V3, but a consensus has yet to be reached.

Front-end Fee

On October 18, 2023, Uniswap Labs implemented a 0.15% swap fee on specific tokens to swaps conducted through its main interface. This move aimed to generate revenue to support operations, including research, development, and the expansion of Uniswap’s platform and ecosystem.

Since implementing the fee, Uniswap Labs has gained $3.5 million in revenue over 100 days, projecting an annual revenue of $13.02 million, despite only 1% of Uniswap’s volume incurring these fees. The minimal impact on trading volumes makes it challenging to assess the overall impact of this fee. For more detailed insights into the front-end fee, see Dune Dashboard.

DEX Competitor Playbook

Each DEX has unique fee structures, often designed to cater to specific market dynamics and user incentives. Here are three notable examples:

SushiSwap

Similar to Uniswap, SushiSwap typically charges a 0.3% fee on trades. The DEX also has a feature where 0.25% goes to active liquidity providers, and 0.05% gets converted back to $SUSHI (the platform’s native token) and distributed to $SUSHI token holders.

Curve Finance

Curve specialises in stablecoin and pegged-asset swaps. Its fee structure is flexible, and values between 0% and 1% can be used. Typically, a 0.04% fee is used. 50% of all trading fees are distributed to $veCRV holders.

PancakeSwap

Operating on the Binance Smart Chain (BSC), PancakeSwap charges a 0.2% trading fee for most of its transactions. Out of this, 0.17% is returned to liquidity providers, and the remaining 0.03% is sent to the PancakeSwap Treasury.

Despite the three of them offering value accrual mechanisms to their token holders, Uniswap stands still as the most liquid and where the most volume is traded on-chain venue in 2024.

The Fee Switch Dilemma

On the 23rd of February, 2024, the [RFC] – Activate Uniswap Protocol Governance was published. Far from being the first proposal regarding the fee switch, this one focuses on introducing a value accrual mechanism for $UNI aimed at incentivising holders in two main ways: aligning economic incentives and encouraging governance participation. It ensures that a portion of the fees earned by LPs is distributed to $UNI token holders who have delegated and staked their tokens.

The proposal outlines that the protocol fee should be switched on without discussing any specific parameter. In Uniswap V3, this parameter can be set between one-fourth and one-tenth. It is set at the pool level rather than globally; therefore, each pool’s level corresponds to a fee tier. Additionally, the fees are earned in the two tokens comprising the pool.

A threshold for claiming fees has been established, tentatively at 10 wETH. Claimants would have to exchange 10 wETH for the tokens held from accrued fees. This mechanism incentivises actors to claim—and thus swap—the fees into wETH as soon as possible to maximise profit and avoid being front-run by others.

Fees would be distributed daily to $UNI stakers on a pro-rata basis over a 30-day period. When new rewards are claimed and are set to be distributed, the reward distribution period resets back again to 30 days.

Impact of Proposal on Traders & LP’s

But what about the traders and LPs in the pools, who are crucial for the health of any DEX? LPs on Uniswap may hesitate to activate the fee switch as they are concerned about the impact on their returns.

Recent work on LP profitability has highlighted problems that LPs face impacting their profitability. Including toxic order flow, which can be measured through loss-versus-rebalancing (LVR), MEV bots providing just-in-time (JIT) liquidity, or just the overall competitiveness of LP’ing in Uniswap.

The fee switch, when activated, would divert a portion of trading fees to $UNI stakers or the Uniswap treasury, as recent and past proposals have outlined. This represents a reduction in the direct financial incentives for LPs.

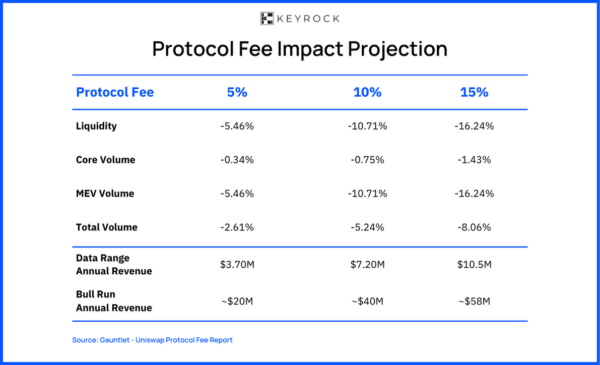

In response to this ongoing debate, the Uniswap Foundation has commissioned Gauntlet to assess the impact of introducing a specified fee on revenue, liquidity, and trading volumes. The report, which includes the details of its methodology, is available here.

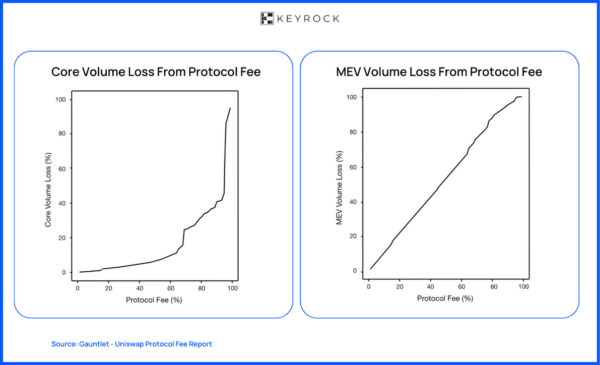

Gauntlet’s findings suggest that implementing a 10% protocol fee, diverting one-tenth of the fees from LPs to $UNI holders or Uniswap itself, would result in a 10.71% decrease in liquidity and MEV volume, alongside a 0.75% reduction in core trading volume.

Source: Gauntlet – Uniswap Protocol Fee Report

As highlighted not only by Gauntlet but by a broader set of the community, the introduction of this revenue reduction for LPs could make Uniswap less appealing, prompting LPs to explore alternative protocols and re-evaluate the opportunity costs.

So, Are we really Ready?

The introduction of a fee switch mechanism could set new industry benchmarks in revenue sharing, inspiring others, such as dYdX—who have previously hinted at a fee-sharing mechanism—to follow suit.

The Uniswap Foundation’s proposal sheds light on a significant issue: governance apathy, with less than 10% of circulating $UNI participants on a given proposal. While introducing a fee-sharing mechanism via staking and delegation might increase participation, it is unlikely to ignite a broader interest in governance.

However, this initiative could complicate liquidity provisioning on Uniswap, making it far more suited for sophisticated participants. As highlighted in Gauntlet’s report, the introduction of a one-tenth fee could lead to a reduction in liquidity and trading volumes.

The imposition of a front-end fee without engaging the community, alongside a perceived decline in their involvement in decision-making, with less than 10% of $UNI being used to vote, raises questions about Uniswap’s dedication to decentralised governance.

The primary aim of activating the fee switch, as highlighted in the Uniswap Foundation proposal, is to enhance governance participation, an ambition Keyrock has always vocally supported.

This is why our firm commitment to healthy governance practices hasn’t gone unnoticed, leading us to be one of the seven delegates to receive increased UNI delegation. Therefore, we can only be supportive of such a proposal.

However, we advocate for a phased, iterative approach, initially targeting a few select pools rather than implementing a drastic, global change. Drawing on insights from analyses like Gauntlet’s, we aim to make informed decisions that serve the best interests of Uniswap as a protocol, LPs in the pools, and traders—acknowledging each as a crucial actor of the ecosystem.

To have an overview of our voting and governance participation, check out our 0xkeyrock.eth wallet’s activity.

Read more: Airdrops in the Barren Desert: Surveying the traits behind 2024’s 11% success rate

- Looking for a liquidity partner? Get in touch

- For our announcements and everyday alpha: Follow us on Twitter

- To know our business more: Follow us on Linkedin

- To see our trade shows and off-site events: Subscribe to our Youtube