2 February 2026

Key Insights: Winter for Doves

Hawkish Shift Reprices Markets

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

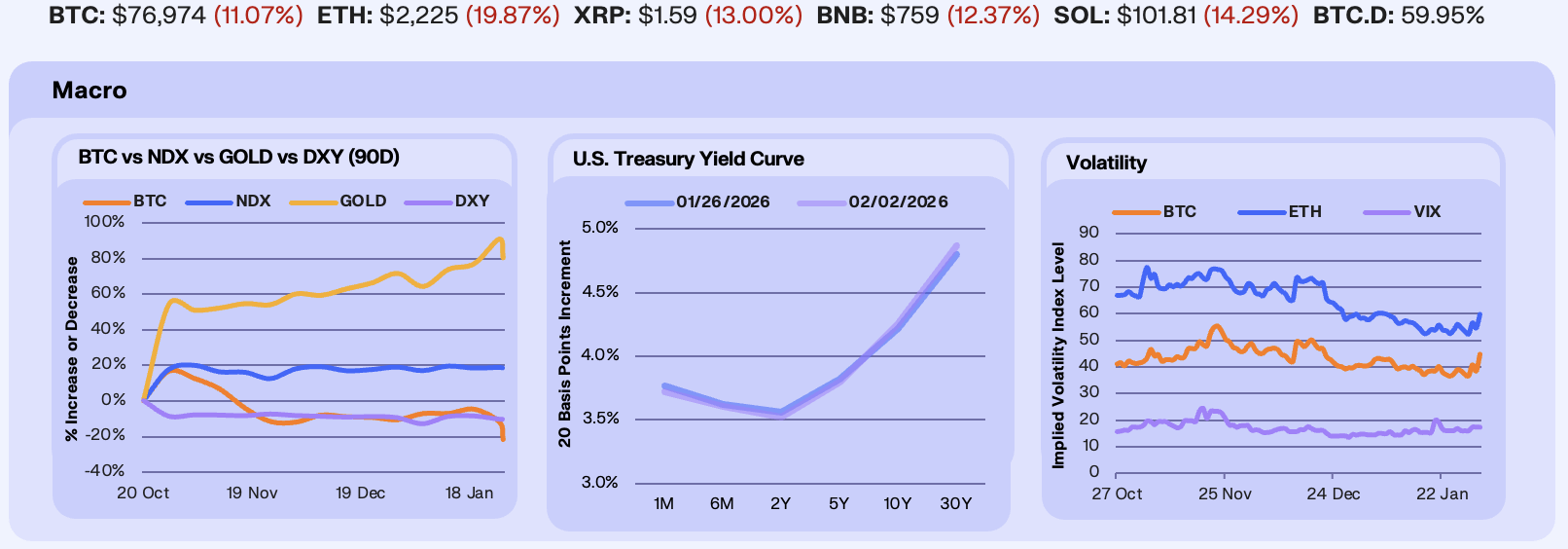

Last week was again defined by commodities and shifting Federal Reserve expectations, as markets reacted sharply to speculation around Kevin Warsh emerging as the next Fed Chair. Gold and silver surged to fresh all-time highs above $5,500 per ounce and $120 per ounce, respectively, before reversing late in the week after Warsh was confirmed as the next chair. His historically hawkish stance on inflation triggered a rapid repricing across assets, pushing yields and the dollar higher while pressuring equities and other risk-sensitive markets. Bitcoin fell −11%, continuing to trade as a higher-beta expression of Nasdaq weakness, while gold still finished the week down −5.6%. The Nasdaq slipped −0.2%, and the dollar ended the week marginally lower at −0.03% after briefly touching a four-year low.

Rates markets reflected this recalibration. The Fed held rates unchanged for the first time since July 2025, noting inflation remains “somewhat elevated,” the labor market has shown “some signs of stabilization,” and uncertainty around the economic outlook remains high. Treasury yields moved modestly across the curve, with the long end rising, leaving the curve slightly steeper. Markets now price a 90% probability of no rate change at the March meeting and continue to expect only two rate cuts this year, signaling skepticism that a leadership change would deliver the aggressive easing stance advocated by the administration.

Volatility reaccelerated late in the week amid heightened macro uncertainty and shifting Federal Reserve expectations. BTC ATM 30-day implied volatility jumped +14.9% WoW to 45, with ETH IV rising +6.6% to 60, as Bitcoin traded below $80,000 and ETH slipped under $2,500. Equity volatility also firmed, with the VIX up +3.2%. Short-dated options continue to price elevated tail risk. Even so, implied volatility across crypto remains low relative to history, underscoring a market that is cautious but increasingly sensitive to macro shocks and regime shifts.

Our Take: A key theme to monitor is Bitcoin’s evolving relationship with the dollar. While gold has long been viewed as the primary hedge against currency debasement, Bitcoin’s response to recent dollar weakness has hinted at a potential shift in perception. If BTC begins reacting more consistently to dollar moves and gains broader recognition as a macro hedge rather than purely a speculative tech asset, that relationship could become increasingly important in the months ahead.

Deleveraging Hits Majors

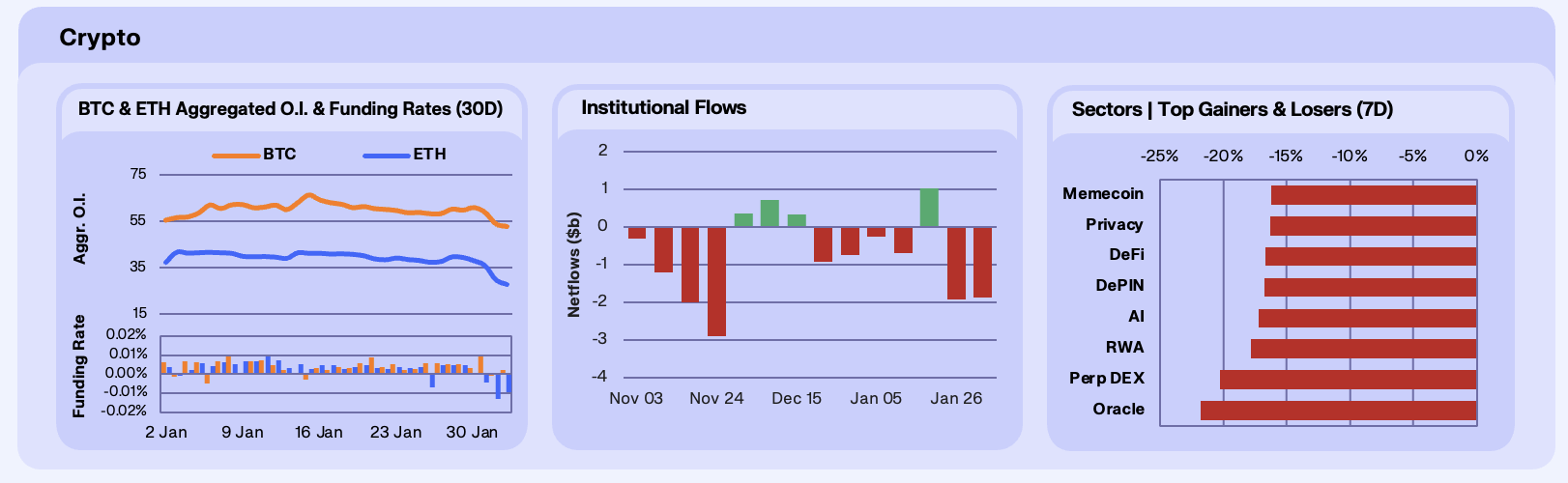

Across digital assets majors sold off sharply this week, with BTC -11%, ETH -22.8%, and SOL -17.2%, as risk appetite deteriorated and deleveraging did the rest. The macro backdrop turned less supportive after the Federal Reserve reiterated a ‘higher-for-longer’ posture at its late-January decision, keeping the market cautious on near-term easing. At the same time, rising geopolitical stress fed a flight-to-safety impulse, which tends to pressure high beta assets. Open interest collapsed as the move accelerated, with BTC OI falling roughly 12% WoW while ETH OI dropped 30% WoW, consistent with forced long unwind rather than a slow grind lower. ETH funding also flipped materially negative into month-end, while BTC funding stayed closer to flat-to-slightly-positive, another signal that ETH was the more crowded expression of risk this week.

Institutional flows matched price action, with digital asset investment products printing -$1.86b of net outflows, driven overwhelmingly by BTC (-$1.49bn) and ETH (-$337m), with SOL (-$3.1m) and XRP (-$31.2m) also negative. This wasn’t a rotation out of digital assets so much as a macro de-risking across the board, which fits with the scale of the derivatives flush and the speed of the drawdown.

Sector performance was uniformly red, but dispersion still tells you where positioning was most fragile. Oracles (-21.8%) and Perp DEX (-20.3%) underperformed, consistent with de-grossing in infrastructure beta and anything directly tied to leverage assumptions. Memecoins (-16.2%) and Privacy (-16.3%) were the best of a bad bunch, which we read as lower incremental leverage relative to the most crowded, institutionalised expressions.

Our take: This looked like a classic positioning reset, especially with the magnitude of OI compression suggesting the market forced itself back to a cleaner baseline. The upside signal we’re watching for is not price first, it’s OI turning up without funding going euphoric, which would imply risk is returning in a healthier shape.

Cautious Onchain Flows

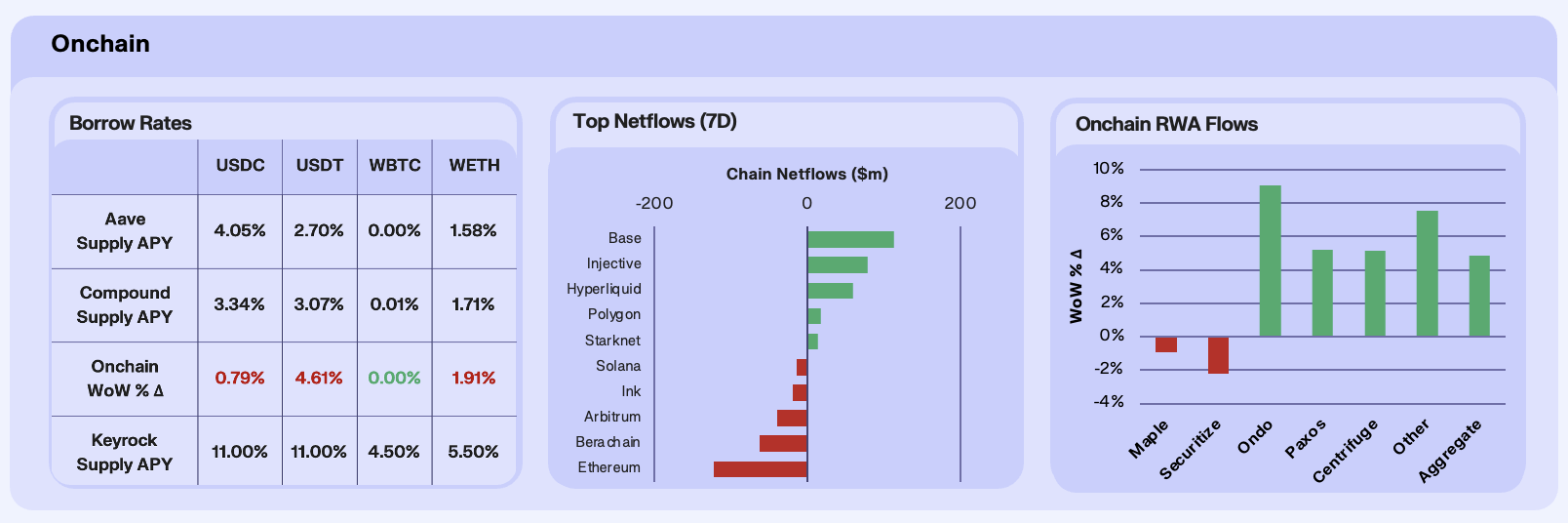

Supply yields were broadly up this week, with USDC and USDT rates firming while WETH softened. Aggregate onchain supply yields were mixed this week, with the stablecoin complex firming while beta assets softened. Aggregate onchain supply APYs moved up 0.79% for USDC WoW and 4.61% for USDT WoW, while WETH gained 1.91% WoW. The large swing in USDT rates appears, as ever, driven by a supply shock in which 15% of liquidity was pulled from the Aave lending pool. We read the sensitivity to liquidity, and thus insensitivity to demand, as a lack of onchain looping demand.

In terms of chain flows, we saw Base and Injective dominate this week, pulling in $113m and $79m respectively. This is consistent with capital leaning into new products, with Coinbase’s expansion into commodities futures for Copper and Platinum, and Injective’s cross-chain integration with Solana’s Jupiter. Losers included Ethereum (-$125m) and Berachain ($63m) as the latter was consistent with derisking behaviour ahead of known supply events, namely an upcoming unlock.

RWAs were strong at the headline level, with aggregate AUM up 4.85% WoW, but AUM flows were concentrated. Ondo (+9.05%) and Paxos (+5.21%) led gains, while Centrifuge (+5.17%) also contributed meaningfully. Meanwhile Maple (-0.95%) and Securitize (-2.22%) were modestly negative, which fits the pattern we highlighted last week, visible when risk appetite wobbles, in that credit and structured sleeves see faster churn than the core beta RWA exposures.

Our take: This week reads as an uncertain onchain economy, in which capital is backing off, unwilling to flow into speculative venues, or fully to retreat, given heightened uncertainty. There remains a growing correlation between onchain flows and macro sentiment, so we will need to see a material shift on the macro front before onchain activity heats up again.

Macro Perps Take Off

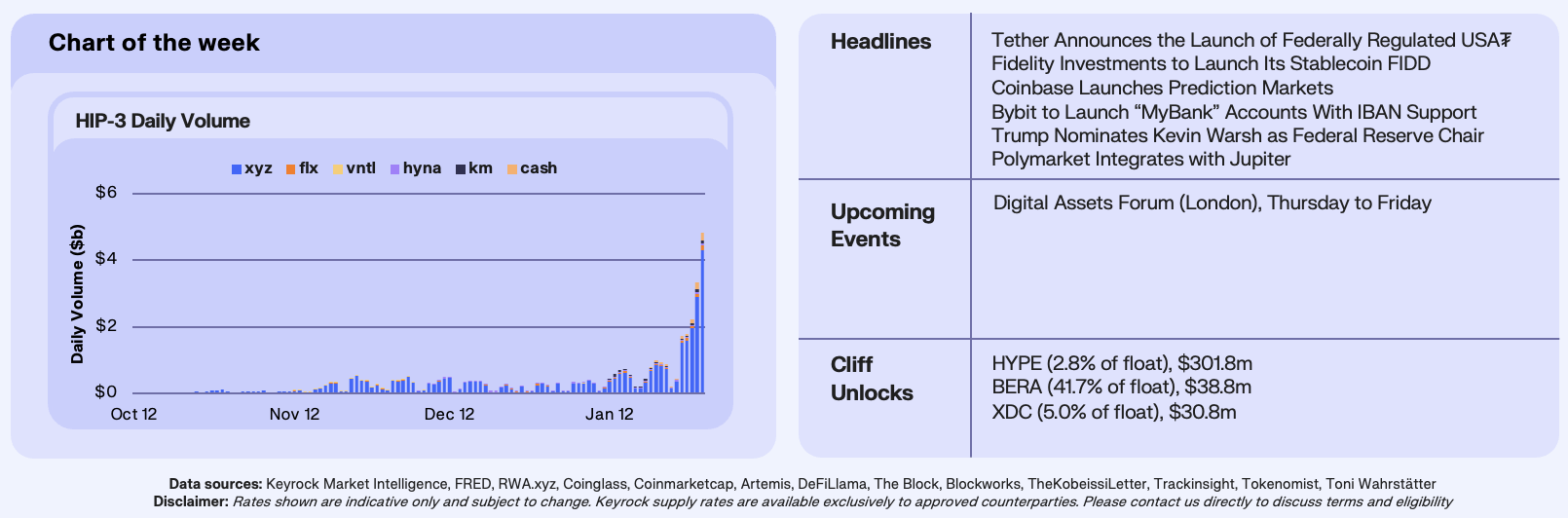

HIP-3 is Hyperliquid’s framework for listing third-party perpetual markets, allowing external providers to deploy new markets while tapping into Hyperliquid’s execution layer. Over the past several months, HIP-3 has quietly become one of the fastest-growing sources of volume in crypto, driven primarily by traders expressing leveraged exposure to macro assets. Recent activity has been dominated by Silver, Gold, Copper, Nasdaq, and S&P contracts, with traditional large-cap US equities contributing marginally by comparison.

The growth has been rapid and nonlinear. From October 12 to January 30, daily HIP-3 volume expanded from roughly $24m to $4.8b, representing an approximate 200x increase in just three and a half months. Momentum accelerated in January, with average daily volume rising from around $250m in December to roughly $2.27b between January 26 and 30, a near 9x jump in a single month. The period also saw four consecutive daily all-time highs, culminating on January 30, which coincided with Hyperliquid’s highest single-day revenue since November at $4.8m.

While xyz remains the dominant provider, its share has gradually diluted as new participants entered the ecosystem. Provider count has grown from a single venue in October to seven by January, and xyz’s share slipped from roughly 90–92% in mid-December to 87.2% by January 30, even as its absolute volume continues to grow. HIP-3 products now account for over 32% of total Hyperliquid volume at peak, with open interest climbing from approximately $160m in early December to around $1b today. Notably, Silver alone printed $2.93b in single-day perp volume on January 30, underscoring the extent to which macro-linked leverage is driving activity.

Our Take: HIP-3 is shaping up to be one of crypto’s most compelling growth vectors heading into 2026. As commodities and equity perpetual trading continues to attract both retail and institutional participation, Hyperliquid offers a streamlined venue to express leverage across these markets. With ongoing engagement with the CFTC around a legal framework for continuous perps, current volumes may ultimately look modest if US brokers are eventually able to offer continuous perps. For now, HIP-3’s expansion suggests Hyperliquid’s growth curve is still in its early innings.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.