Stablecoin Payments, The Trillion Dollar Opportunity

Written by Amir Hajian

Read the Full Report

Preface

The most comprehensive report on stablecoin payments.

From legacy payment systems to the stablecoin infrastructure transforming the global payments stack, we break down the architecture powering payments, the real-world use cases driving adoption, and the trends set to unlock $1 trillion across key verticals.

A 90+ page report written with Bitso, featuring 45+ expert insights from Circle, Ripple, Sphere, Ondo Finance, First Digital, BVNK, Conduit, Gnosis Pay, MANSA, and Lumx.

Access the full report to explore how stablecoin rails could power trillions in payments volume by decade’s end.

Introduction

Stablecoins’ real potential lies in emerging markets, home to 85% of the global population, yet underserved by traditional financial infrastructure. Stablecoin payments will unlock trillions in value by enabling faster, cheaper access to payments in regions long overlooked.

Stablecoins are starting to bridge the gap by collapsing the payment stack into a single layer. They’ve already grown from just 0.04% of the U.S. M2 in 2020 to over 1% today, marking the emergence of a parallel monetary layer.

Projected stablecoin share of U.S. M2 supply by 2030:

- Bull Case (10.4%) – Stablecoin adoption accelerates, unlocking trillions in value through faster, cheaper payments and deep integration into global financial infrastructure

- Base Case (5.2%) – Continued steady growth as stablecoins bridge the payment stack, expand use in B2B, P2P, and point-of-sale payments

- Bear Case (2.6%) – Conservative expansion driven by slower adoption

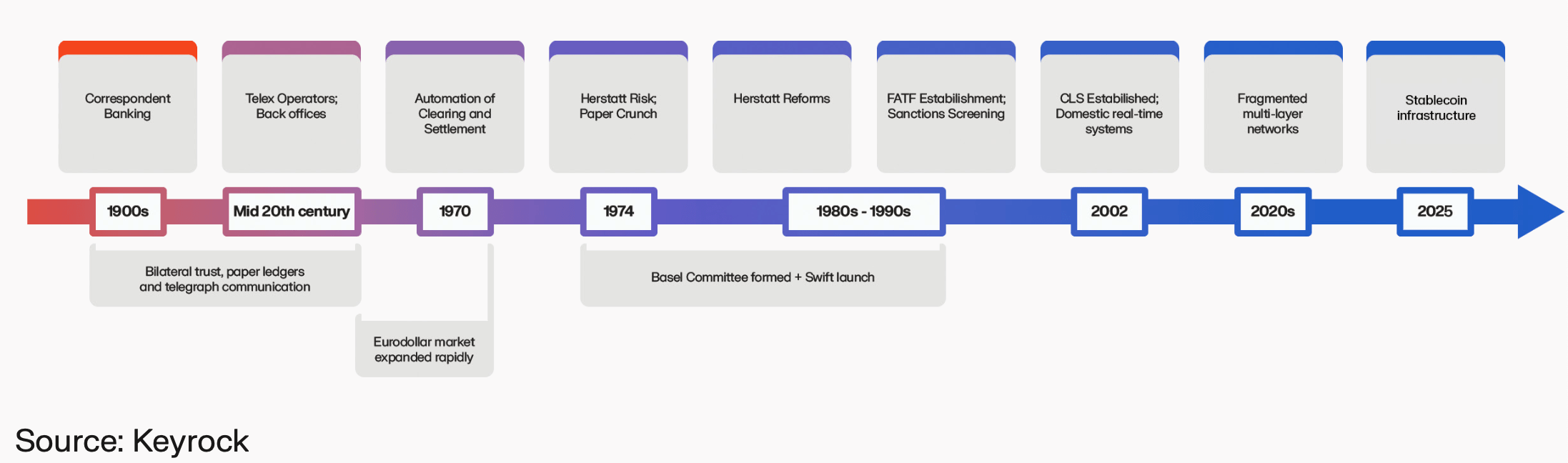

A Legacy of Layers

Today’s cross-border payment system wasn’t designed, it accumulated. Over decades, layers of intermediaries and compliance rules were bolted on to solve narrow problems, leaving behind a maze of inefficiencies.

One international payment can pass through five or more intermediaries: banks, FX desks, compliance checks, local clearing, global messaging. Each layer was added to solve a problem, but none replaced the one before it. This wasn’t accidental. The system was designed to manage risk, in a world that lacked real-time computation, trusted code, or transparency.

But those constraints no longer exist. Stablecoins are the next evolution in payment infrastructure.

Stablecoins 101

What are stablecoins? How do they maintain their peg, generate revenue, and move value onchain? This section breaks down the fundamentals, from minting mechanics and reserve strategies to the growing macro role of stablecoins in global finance.

As their supply nears $2 trillion, stablecoins could hold close to 25% of the Treasury bill market, directly impacting Fed policy and front-end yields. Every $3.5b increase in supply lowers three-month T-bill yields by 2.5 to 5 basis points, signaling the rise of a new monetary transmission mechanism.

Major issuers now hold more U.S. Treasuries than countries like South Korea, Germany, and Saudi Arabia. Their presence is already shaping demand at the short end of the curve and embedding liquidity into the heart of U.S. monetary policy.

Building The Stablecoin Payment Stack

Stablecoins aren’t just instruments, they’re infrastructure. We unpack how stablecoin rails are powering a new financial stack, starting with virtual USD accounts and the “stablecoin sandwich” model.

As stablecoin platforms evolve, they are beginning to own the full stack, from issuance and FX to wallets, compliance, and settlement. By collapsing the payment flow into a single layer, they streamline operations, lower costs, and unlock global reach. This vertical integration allows them to monetize every layer of the stack, including treasury deposits, transaction fees, DeFi yield, and consumer-facing applications, while returning more value to users.

Bridging the Legacy Stack

Stablecoins are emerging as orchestration layers for global payments, coordinating value across fragmented domestic rails. Acting as connective tissue between local banking systems, they treat fiat like packets of data and embed multi-step workflows and compliance directly into the transaction itself.

As credit flows move onchain, stablecoin rails also unlock capital efficiency. By replacing idle, prefunded accounts with short-term credit lines, platforms like MANSA and Arf are transforming liquidity management into a dynamic just-in-time model and turning every dollar into high-velocity working capital.

Proof in the Payments

We focus on the three largest sectors driving real-world stablecoin payment adoption: business-to-business (B2B), peer-to-peer (P2P), and card-based transactions. These categories offer the clearest view into how stablecoins are migrating from crypto-native flows to more mainstream payment activity.

We close with Onchain FX. While it remains the least developed in terms of adoption, it holds the potential to fundamentally rewire how money moves across currencies and borders. If current growth trends hold, annual stablecoin payment volume across key payment verticals will approach $1 trillion by 2030.

The Treasury Turnaround, B2B

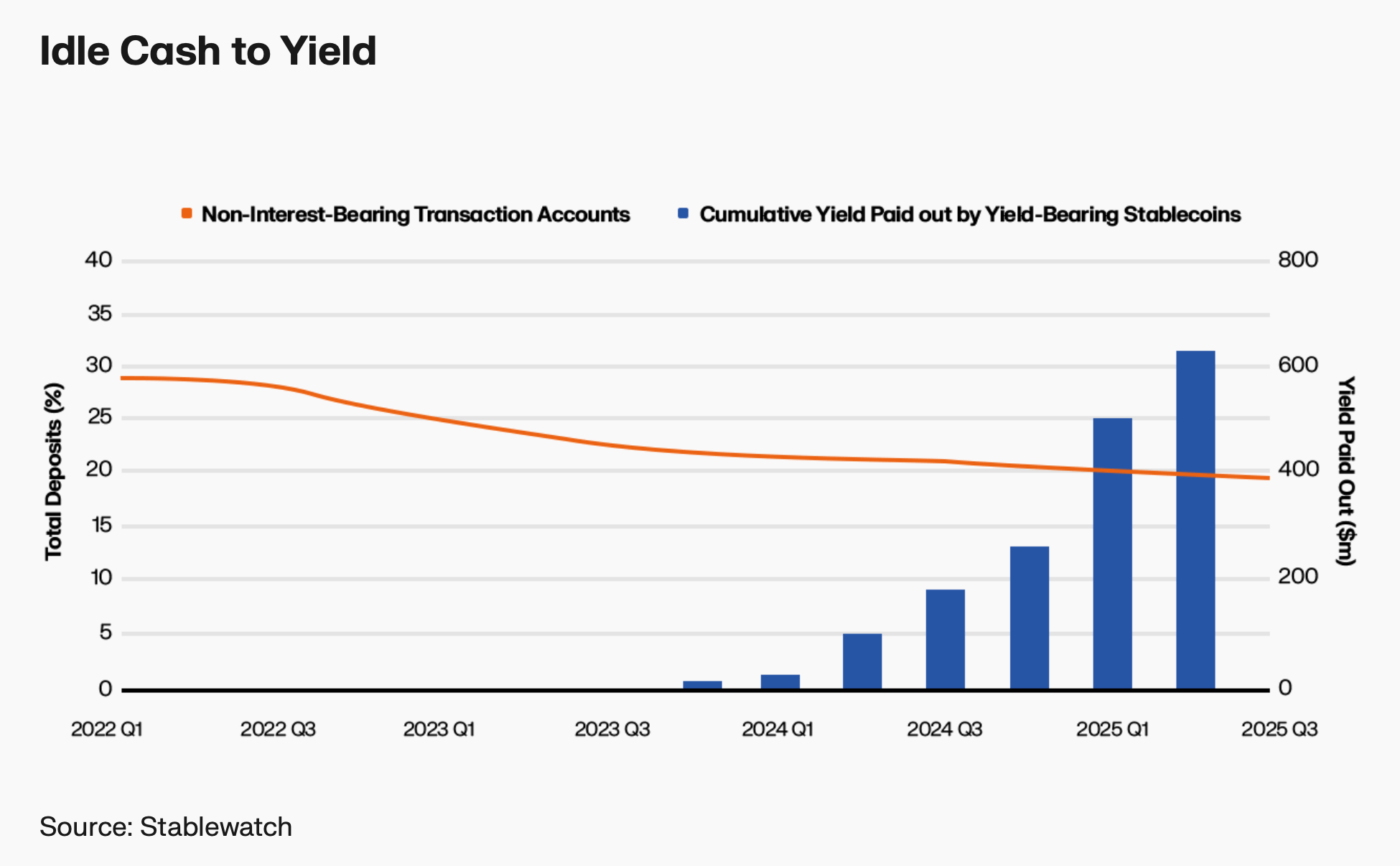

For many businesses, stablecoins are first making an impact in the back office. Treasury functions long constrained by fragmented balances, liquidity shortfalls, and opaque yield structures are being rebuilt.

Legacy B2B payments remain costly and slow, with most operations still manual and 21% of U.S. commercial deposits earning zero interest, a free spread worth $154 billion annually for banks. The stablecoin model flips this. Businesses can hold reserves in yield-bearing stablecoins, collect yield automatically, and use the same tokens for payroll, supplier settlement, or disbursements without batch cycles or cutoff windows.

Money That Finds A Way, P2P

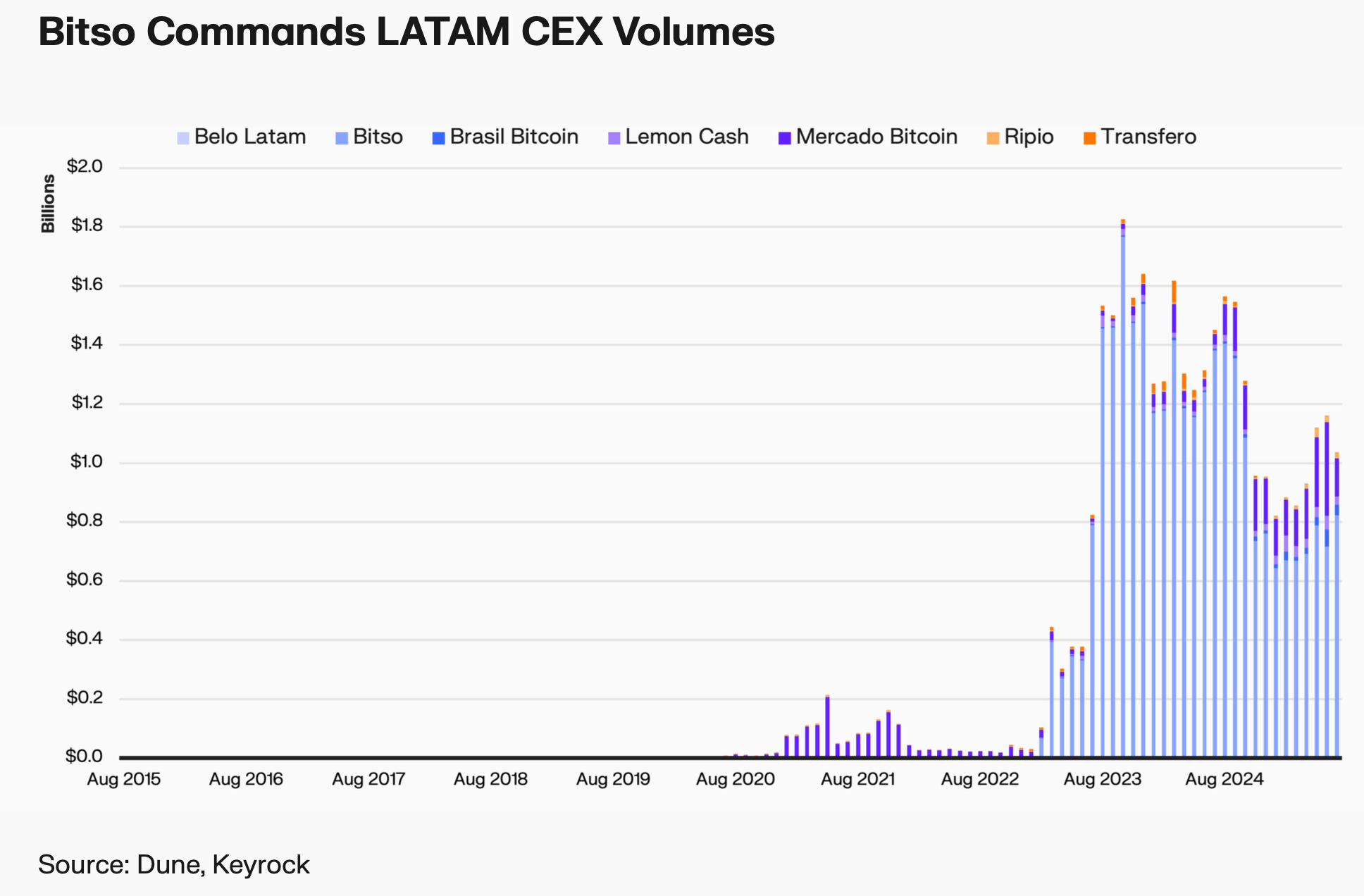

Stablecoins are reshaping person-to-person transfers, from cross-border remittances to everyday local payments. High remittance costs, with banks charging ~13% to send $200, continue to drive adoption of both dollar-pegged and local-currency stablecoins, which bridge the gap between cross-border inflows and day-to-day spending.

Stablecoins can deliver the same transfers in seconds for under 1%, making them up to 13× cheaper. Bitso, which now handles over 10% of the U.S.–Mexico remittance flows, processed $850m in July, 6.5× its nearest rival, while expanding into local stablecoins like MXNB and BRL1 that keep users onchain as both the payment medium and destination.

Stablecoin-Linked Cards

Stablecoin-linked credit and debit cards are emerging as one of the most compelling real-world use cases. By combining the global reach of Visa and Mastercard with blockchain’s programmability and transparency, fintechs now enable consumers to pay tens of millions of merchants directly from their stablecoin balances. This market is scaling quickly, with monthly volumes rising from ~$250 million in early 2023 to over $1 billion by early 2025.

On the backend, tokenized receivables are transforming card settlement and capital efficiency. Platforms like Rain tokenize Visa credit receivables and settle onchain per transaction, instantly releasing working capital and removing fiat repayment risk for lenders.

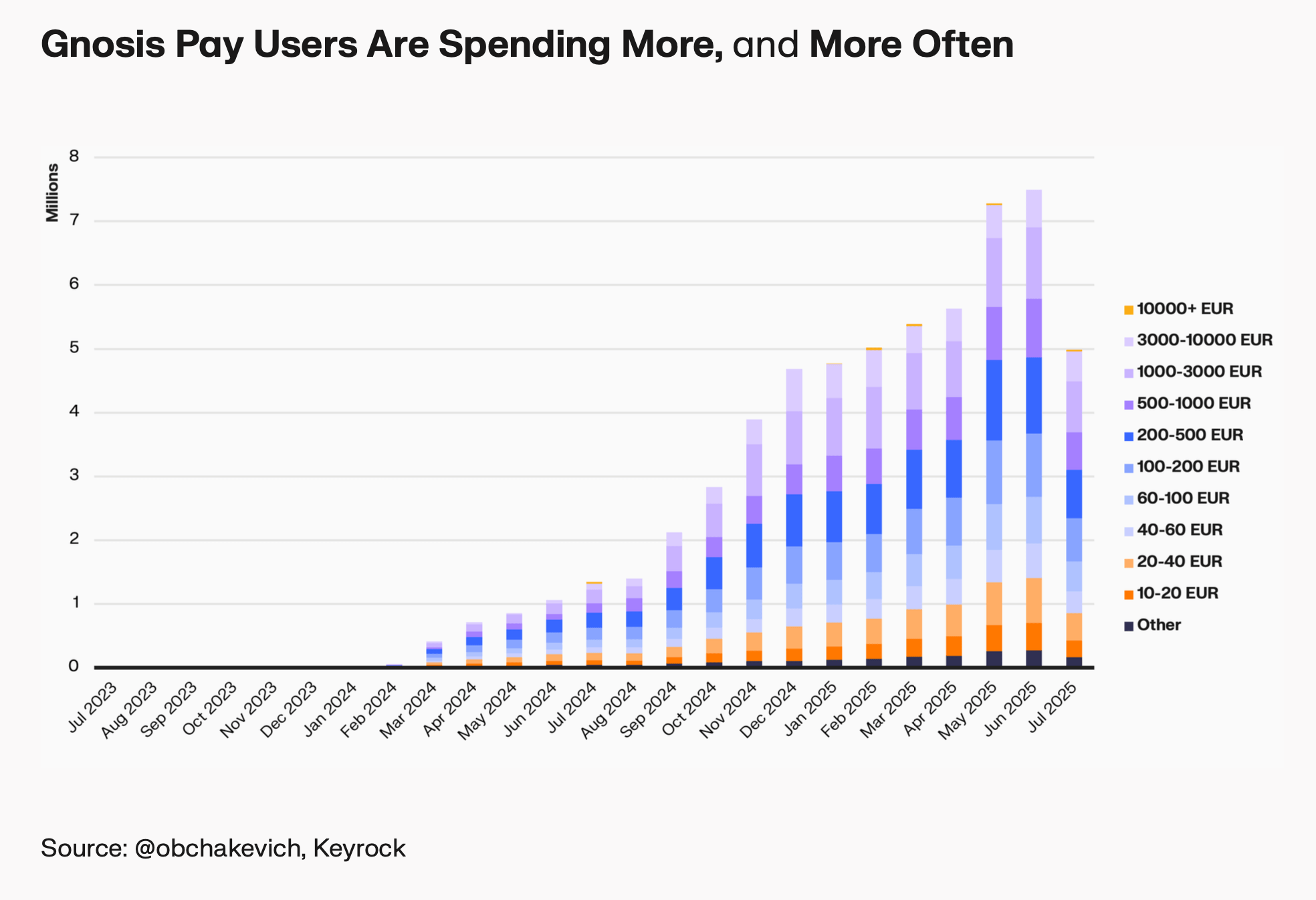

On the frontend, platforms like Gnosis Pay link self-custodial wallets directly to Visa debit cards, letting users spend USDC or EURe without intermediaries. With a 57% increase in monthly volume year-to-date, users are transacting more frequently and at higher values, with €1,000–€3,000 payments dominating power user activity.

Rewiring FX

Onchain FX offers a fundamental alternative to the legacy currency swap stack. It enables atomic Payment versus Payment (PvP) transactions, ensuring both legs of a trade settle simultaneously or not at all. By combining messaging and settlement into a single layer, it removes operational complexity and reduces errors.

Companies that once needed to liquidate money market funds, short-term treasuries, or other fixed-income holdings, often subject to cutoffs and multi-day delays, can now instantly convert tokenized equivalents into stablecoins and settle payments onchain. In traditional securities transactions, brokers execute while custodians settle over T+2 days.

With tokenization, cash, custody, and assets exist on one layer, which enables atomic settlement and automated actions via smart contracts. This unified architecture compresses payments, custody, and settlement into a single composable system, streamlines reconciliation, reduces friction, and unlocks new product designs.

Emerging Opportunities

The next phase of stablecoin adoption will be shaped by four enablers now moving from barriers to catalysts. Regulatory clarity, interoperability, liquidity, and programmability. Together, they form the foundation of the stablecoin ecosystem, from issuers and networks to wallets, middleware, compliance tools, and liquidity providers.

Regulatory clarity unlocks institutional adoption by removing legal uncertainty, while interoperability ensures stablecoins can move seamlessly across rails and applications. Liquidity depth allows stablecoins to scale without slippage or fragmentation, and programmability turns static value into dynamic infrastructure, enabling automated compliance, conditional payments, and new product design.

As these layers mature in concert, the stablecoin stack will evolve into a unified, interoperable settlement layer capable of bridging fiat and crypto at global scale.

Conclusion

Stablecoins have moved beyond their origins in trading to become a credible, programmable payment rail with the potential to move over $1 trillion annually within the decade. As regulation, liquidity, and interoperability mature, they are positioned to capture a meaningful share of cross-border flows.

Their trajectory is toward systemic relevance, reshaping how liquidity is managed, how policy is transmitted, and how money itself is experienced.

Read our full report on stablecoin payments to explore the architecture, use cases, and market forces driving this transformation.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.