1 September 2025

Key Insights: Waiting On The Cut

Markets Split Ahead Of Fed

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

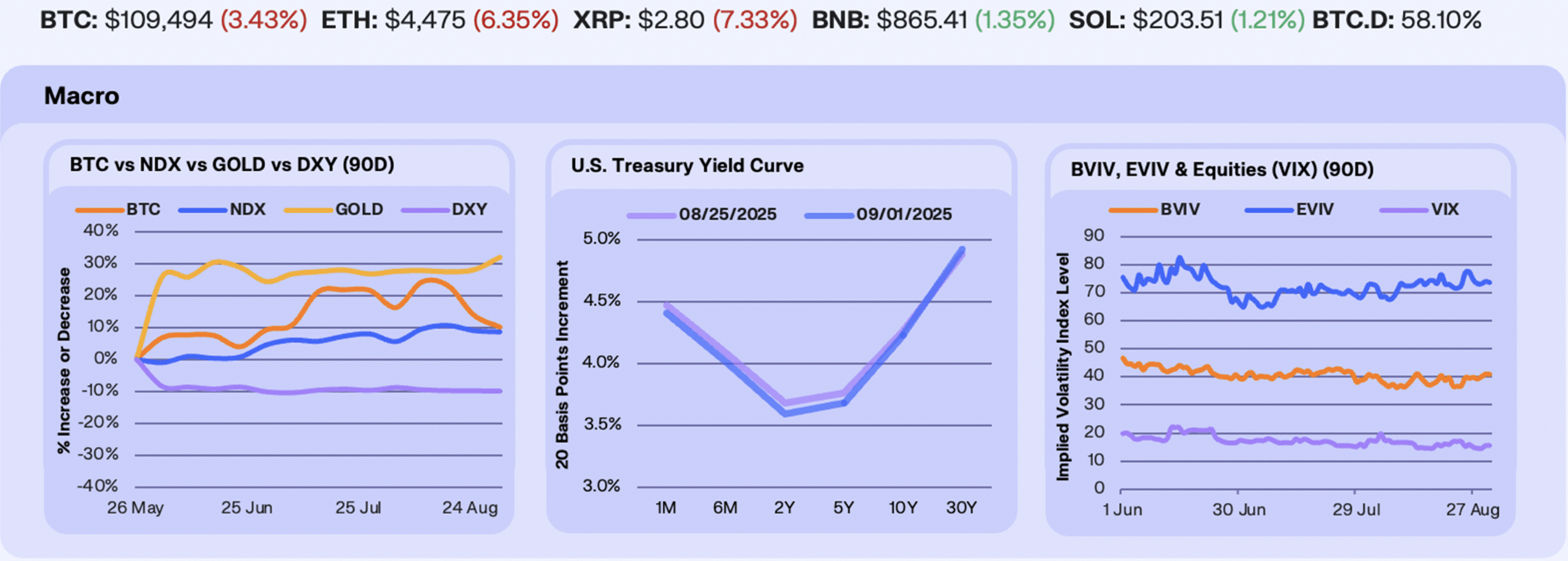

Last week brought a mixed performance across markets, with Bitcoin dropping 3.3% and erasing its post–Jackson Hole bounce as investors turn their focus to upcoming catalysts, the August jobs report on Friday, CPI data on September 11, and the Fed’s rate decision on September 17. Gold surged 3.1% as rate-cut expectations grew firmer, while the Nasdaq hovered near record highs (-0.4%) and the S&P climbed above 6,500 for the first time in history.

As a response to a likely 25 bps rate cut later this month, the yield curve bull-steepened considerably in a classic sign of inflation expectations rising. Short-end yields fell 6 to 9 bps as markets priced in easier policy, while the the 30Y pushed higher and up 4 bps on the week. The result is a more pronounced curve, with the 2s30s spread widening, highlighting the market’s pivot toward growth and inflation risk further out the curve.

Volatility chopped throughout the week. Bitcoin IV drifted higher from 39.8 to 41.0 (+3.0%), while Ethereum’s IV eased from 77.1 to 73.6 (-3.5%), retracing part of its recent spike. The VIX inched up from 15.1 to 15.4 (+2.1%), still close to multi-year troughs. The split underscores rotation in vol dynamics with BTC catching a bid amid downside risks while ETH cooled as momentum faded. Yet option markets continue to signal contained risk despite shifting macro expectations.

Our Take: The Fed’s dovish shift and signs of labor market softness strengthen the case for a September cut, giving risk assets a more supportive backdrop. The persistence of call premiums in long-dated BTC options signals that the market views this as a correction within a medium-term bull trend. Still, history shows markets tend to price in rate cuts well before they materialise, and with equities already at all-time highs, the environment may call for more defensive positioning rather than chasing outperformance.

Leverage Reset, Majors Poised

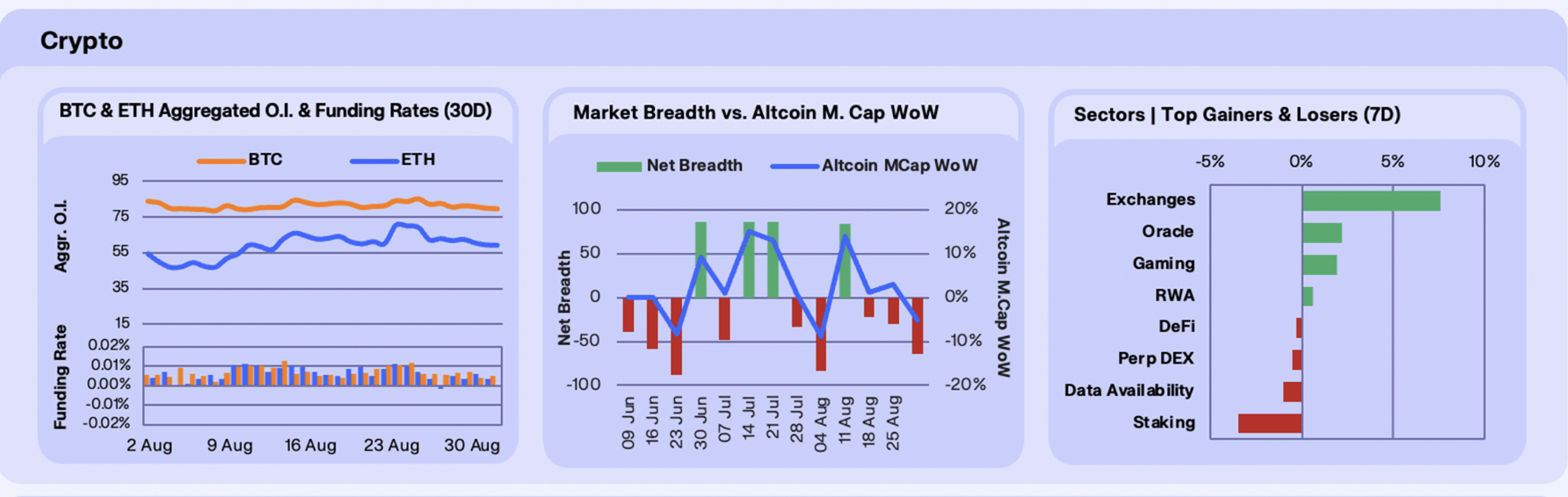

Majors slipped this week as macro headwinds and ETF flows drove mixed sentiment. BTC fell 3.9% WoW, dipping below $109k as $150m in long liquidations triggered the sharpest liquidation flush since December last year. ETH dropped 6.6%, despite $1.08b in ETF inflows this month, which pushed August to its strongest month on record. Crucially, ETH managed to sustained above the key price support level of $4,260, maintaining a higher low for this ETH rally. SOL outperformed, down only 2.8% WoW, supported by a flurry of DAT announcements totalling $2.5b in prospective buys, including Sharps Technology’s $400m raise and institutional interest from Galaxy, Jump, and Multicoin. Across majors, ETF rotation into ETH and Solana treasuries offset weaker BTC flows, keeping sentiment constructive despite hotter PCE data tempering broader risk appetite.

Derivatives positioning was muted this week, with BTC OI slipping 2.96% WoW to $79.5b while ETH edged below by $60b for the first time in weeks, falling by 4.85%. Funding rates held in a narrow band, with BTC averaging 0.006% and ETH oscillating between mildly negative and positive, ending the week flat at 0%. The divergence highlights a cooling in BTC leverage appetite after recent ATHs, while ETH positioning remains more balanced, with traders unwilling to push funding higher despite continued price action.

Altcoins slid 5.3% WoW, with breadth deteriorating sharply as just 18 tokens gained against 82 decliners for a -64 net breadth. The weakness follows two weeks of narrowing altcoin participation, underscoring how gains remain concentrated in majors while the broader market struggles. Despite headline narratives around ETF inflows and altseason, breadth volatility highlights how rotations are uneven and fragile. Until participation broadens meaningfully beyond majors, altcoin rallies risk fizzling out into lower liquidity drawdowns. We’re yet to see the sustained altcoin inflows required to call on a full-blown altseason.

Exchanges led sector gains this week, up 7.6%, powered almost entirely by CRO’s 76.7% surge. Crypto.com’s token rallied to highs near $0.38 on the back of a $6.4b joint venture with Trump Media, including an initial $105m CRO treasury buy and integration into Truth Social for rewards and payments. ETF speculation further fuelled demand, with filings for CRO-inclusive products sparking institutional inflows. Outside of exchanges, oracles, up 2.2%, and gaming, up 1.9%, posted modest gains, while staking, down 3.5%, lagged as investors rotated back to majors.

Our Take: The leverage reset sets the stage for majors to lead the next leg higher. If ETH ETF inflows sustain, and it manages to hold support at the $4,260 level, a breakout above $5k looks imminent, while Solana’s $2.5b treasury pipeline could carry it toward $220, and potentially up to $250 should broader market sentiment shift bullish. BTC may lag near-term, but ETF rotation and rate-cut tailwinds still anchor $120k+ retests into Q4.

Centrifuge Breakout Week

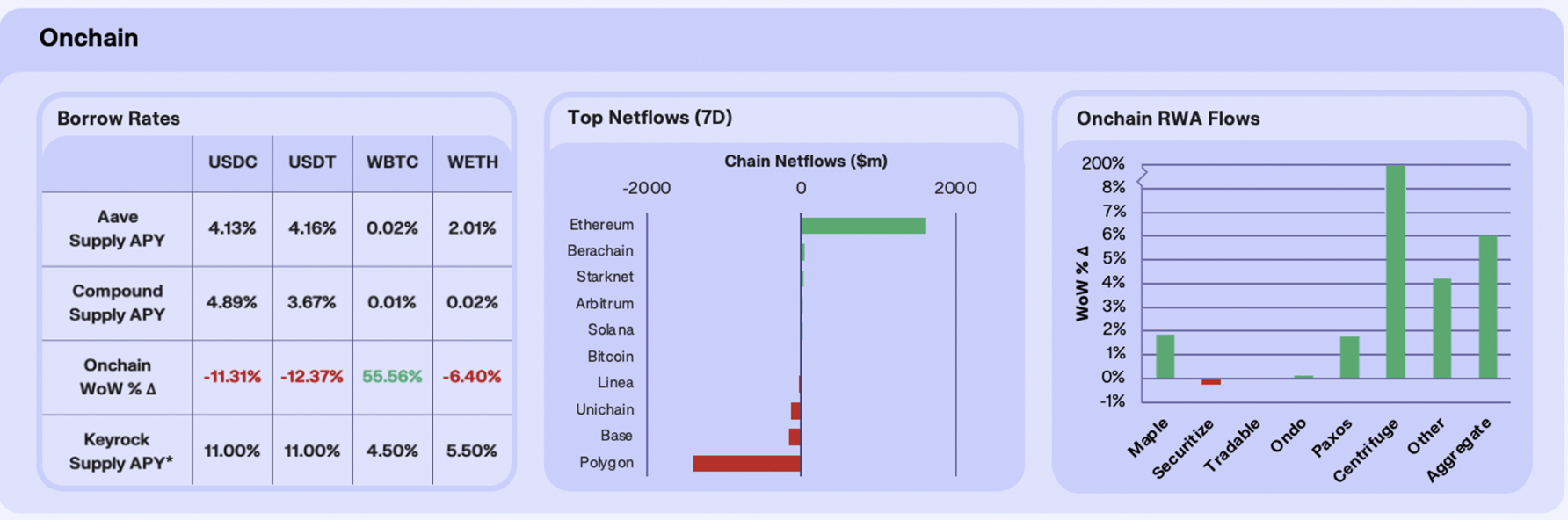

Stablecoin rates fell this week as supply inflows outweighed borrow demand. USDC APY dropped 11.3% WoW to 4.13%, as Aave deposits climbed 23.1% to $1.26b, a clear sign of oversupply pressure, as a result of capital rotating into safer assets amid the $150m BTC long liquidations shaking traders. USDT rates slid 12.4% WoW to 4.16%, with supply rising modestly at 3.4% to $1.28b on Aave’s Ethereum implementation, extending recent volatility after prior weeks of sharp swings. WETH rates fell 6.5% WoW to 2.01% despite a supply contraction of 16.1%, suggesting softer borrow demand despite ETH’s broader price action. This coincided with ETH OI falling below $60b, reflecting less leverage appetite directly on ETH. WBTC APY jumped 55.6% WoW on slightly reduced supply, though absolute yields remain negligible at ~0.02%.

Ethereum continued to dominate net inflows, adding over $1b this week as ETF demand and institutional rotation drove capital back to mainnet, as well as rotations away from waning L2s. Polygon PoS saw the steepest outflows at over $1b, hit by market-wide weakness and negative sentiment from the zkEVM deprecation.

RWAs were the standout this week, with sector AUM up 6.0% WoW, powered almost entirely by Centrifuge’s 206% surge. The protocol drew a $1b allocation into its tokenized AAA-rated CLO fund (JAAA) from Grove, alongside key integrations like Coinbase DEX listings, Aave Horizon collateral support, and the rollout of V3 across Ethereum, Arbitrum, and Base. Smaller gains came from Maple, up 1.8%, buoyed by syrupUSDC expansion, and Paxos, up 1.7%, on regulatory tailwinds, while Securitize saw minor outflows amid rotation to higher-yielding products. The move cements Centrifuge as the sector’s breakout protocol, positioning RWAs firmly at the TradFi–DeFi intersection.

Our Take: Stablecoin rates look set to stay compressed for the foreseeable unless leverage appetite rebounds. The real story this week however, was RWAs. Centrifuge’s $1b inflow marks an inflection point, if institutional allocation continues at recent pace, RWAs could overtake onchain yield platforms as DeFi’s core growth driver into Q4.

Institutions Pile Into ETH

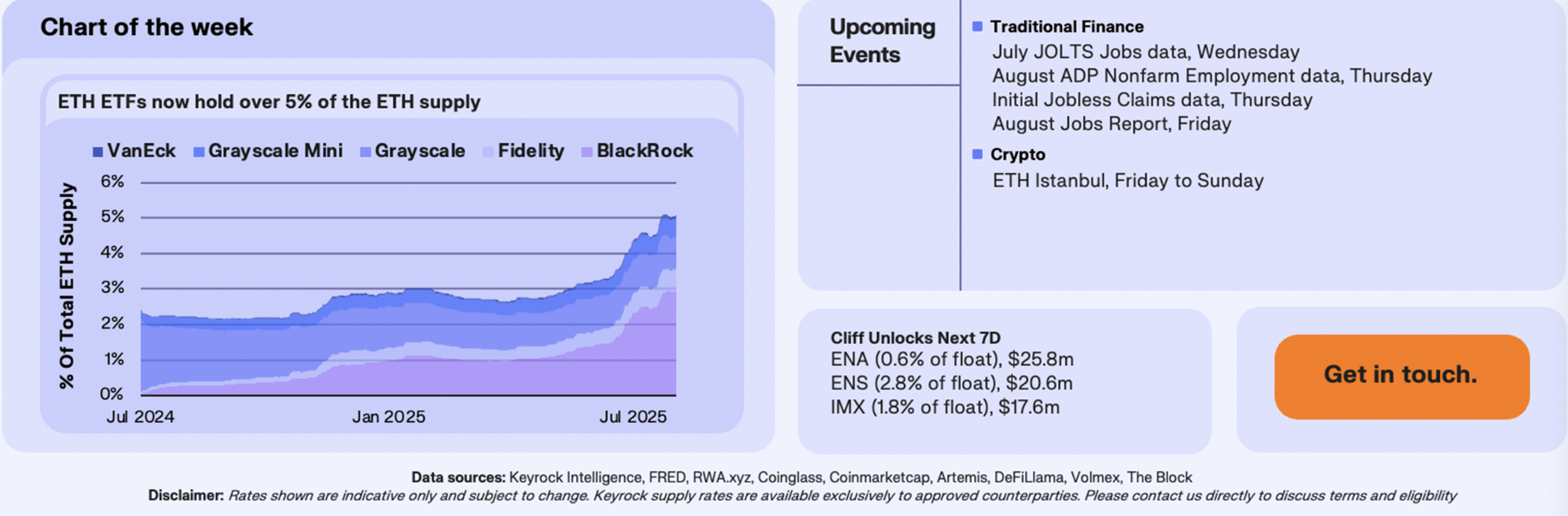

thereum ETFs have accumulated 6.74m Ether, which currently stands at 5.6% of the Ether supply. BlackRock holds the largest share with ~56.9%, followed by Grayscale at 17.3%, Fidelity at 11.9%, and Grayscale Mini at 10.3%, while smaller issuers like Bitwise, VanEck, and others make up the remainder.

Additionally, 70 DAT and Strategic ETH Reserve companies have accumulated 4.44m ETH, which is 3.7% of the supply. The largest holders include Bitmine Immersion Tech with 1.8m ETH (1.48% of supply), SharpLink Gaming with ~798k ETH (0.66%), The Ether Machine with ~345k ETH (0.29%), and the Ethereum Foundation with ~232k ETH (0.19%). These two different groups now control over 11.2m ETH (~$43.9b), equal to more than 9% of the total Ether supply.

Since the week of July 21, ETH ETFs have gained more than $6bn, while BTC ETFs have bled just over $500m, underscoring the strong institutional rotation into Ethereum. This activity was also further seen with some Bitcoin whales, such as a long-dormant holder of 56,816 BTC (~$6b), who recently moved 10,000 BTC ($1.08b) to a new wallet and sent 1,000 BTC ($108m) to Hyperliquid to rotate into ETH. Within last week, the whale deposited another 3,000 BTC ($325.5m), bringing total sales to 4,000 BTC ($434m), and accumulated ~99,059 ETH ($436m).

Our Take: In the short term, Ethereum has captured momentum while Bitcoin lags. Flows and whale activity have pushed ETHBTC higher, but the ratio now looks less compelling after a sharp rebound to 0.4. The cross is nearing the upper bounds of what cyclical rotation alone can deliver as sustained leadership would require structural catalysts. Meanwhile, we expect institutions to treat weakness in Bitcoin as an opportunity to re-accumulate rather than a shift in its long-term positioning.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.