17 November 2025

Key Insights: Waiting For The Drop

Waiting on the Prints

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

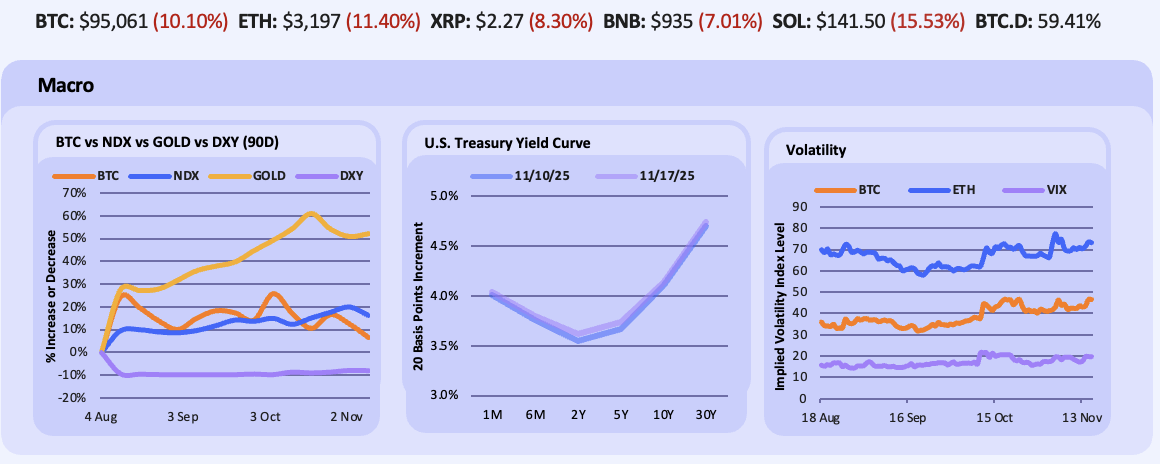

Markets spent last week positioning ahead of the delayed US data that will finally hit after the 43 day government shutdown ended, which was funded by roughly $619b in new borrowing. With no fresh releases yet, traders reacted instead to a coordinated hawkish push from Fed officials like Collins and Kashkari, which pulled December cut odds lower and pressured risk assets. NDX slipped -0.2%, BTC fell -10.1%, while gold jumped above $4,150 per ounce (+1.7%) before setting slightly lower as uncertainty around both the incoming data and the Fed’s reaction function sent flows toward safe havens. The absence of data made ADP’s earlier signal of the second largest private payroll drop since 2020 and the NFIB Small Business reading at 98.2, a six month low, more consequential as markets brace for job print data.

The Treasury curve moved slightly higher across most maturities last week, with the adjustment driven by the front end and belly. Week over week, 1M and 6M yields rose about 4 bps, the 2Y-5Y added 7 bps, while both the 10Y and 30Y rose 3-4 bps. The curve remains deeply bowed but now sits marginally above last week’s levels, reflecting positioning around the same uncertainty that weighed on risk assets: a data backlog, a hawkish Fed tone, and reduced conviction in a December cut.

Volatility swung sharply intraday throughout the week. BTC IV jumped 9.8% to 47, ETH IV climbed 3% to 73, and VIX moved 7% to 20. Demand for short-dated hedges has pushed BTC skew further toward puts, reinforcing a shift that now looks less like caution and more like fear. With the mix of the economic-data backlog and ongoing Fed policy uncertainty, markets may not be fully pricing how much realized volatility, in either direction, could move once those prints start to land.

Our Take: The market is caught between a data vacuum and a Fed that continues to lean hawkish, and that combination is creating a wider range of potential outcomes than current pricing reflects. The next batch of delayed releases over the next two weeks will finally give investors something concrete to anchor to, but until then the setup favors choppier price action.

Caution Across the Board

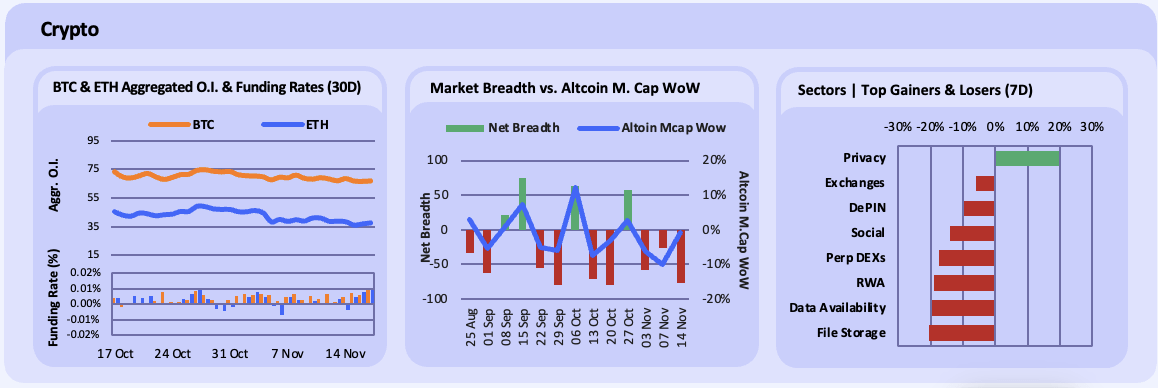

Open interest was broadly stable through the week, with BTC OI holding around $66-68b (-1.9%) and ETH OI drifting lower toward $37b (-8.7%). Perpetual funding stayed muted but positive for BTC while ETH funding softened and briefly dipped negative. This follows over $1.5b in liquidations last week, which flushed out leveraged longs and left positioning cleaner but still cautious. The market is neither aggressively short nor meaningfully risk-on, with derivatives activity reflecting a preference for short-dated protection rather than levered upside.

Altcoin breadth deteriorated again this week, with net breadth falling to -76 as decliners continued to dominate the tape. What makes this week’s weakness notable is the divergence between breadth and price action. Altcoin market cap slipped only -0.7% WoW, a far smaller drawdown than prior weeks where similarly uniform breadth coincided with much steeper losses. That gap suggests selling pressure is becoming more constrained and that the broader altcoin complex may be working its way into a buy zone as capitulation begins to slow. One standout was TEL, which rallied more than 60% after Telcoin Digital Asset Bank secured final regulatory approval from the Nebraska Department of Banking and Finance. Outside of isolated moves, participation remains thin, but the breadth-price divergence is an early sign that downside momentum may be losing steam.

Across sectors, dispersion remained elevated as capital continued rotating into isolated pockets of strength rather than broad beta. Privacy led with a +19.8% gain, one of the only areas attracting consistent bid in an otherwise heavy tape. In contrast, exchange-tokens under-performed (-6.1%) amid flat trading volumes and Perp DEXs (-17.5%) extended their declines as suppressed leverage demand continues to dampen token-linked fee narratives.

Our Take: The backdrop for crypto is still one of caution rather than conviction. Breadth is showing early signs of exhaustion, but for that to matter, the majors need to stabilize and lead first. BTC and ETH remain tightly linked to equity risk, so the next two weeks, with long-delayed macro data finally hitting, should give better visibility on whether that correlation will act as a tailwind or another headwind.

Defensive Onchain Capital

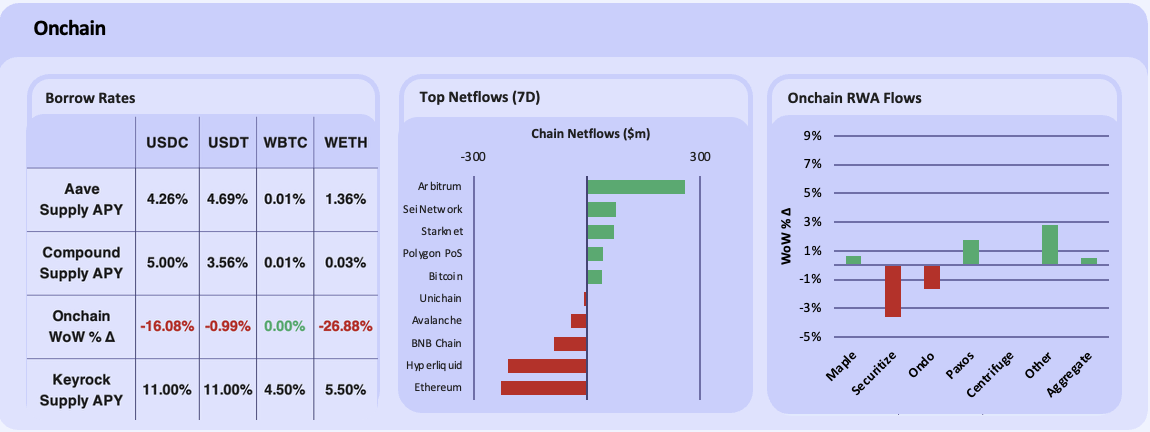

Lending rates across DeFi markets softened this week, struggling to sustain a trend as capital retreated further from risk assets following the ongoing correction. USDC and USDT yields declined 16% and 1% WoW respectively, driven primarily by supply balances compressing after last week’s surge. ETH supply APY rose 35% WoW, reflecting a tentative return to digital asset collateralised lending after October’s deleveraging. We’re seeing defensive positioning bleed into onchain markets, with stablecoins being parked for yield, rather than leveraged into directional trades.

Chail netflows painted a clear picture of consolidation amid market dynamics. Arbitrum dominated with $289m in inflows, as capital migrated from higher-risk venues like Hyperliquid, down $248m, and from L1s such as Ethereum, down $142m, and BNB Chain, down $85m. Hyperliquid’s POPCAT manipulation event on November 13th triggered $63m in liquidations and forced a temporary bridge pause, driving outflows towards Arbitrum, a dynamic we consistently see in large liquidation events. Ethereum’s exits were driven by ETF redemptions, of which we saw $259m on November 13th alone, and staking outflows, while BNB’s drawdown reflected retail cooldown and reduced onchain volumes.

In RWAs, aggregate AUM rose 0.47% WoW, highlighting sector resilience amid broader risk aversion. Paxos, up 1.7% eked out gains on gold-linked and tokenised credit products, expected to do well in this market. Meanwhile Securitize, down 3.6%, and Ondo, down 1.7%, saw moderate AUM pullbacks tied to ETF-linked redemptions and October’s market correction. Securitize’s SPAC-related volatility and Ondo’s token price drawdown contributed to transient outflows.

Our Take: Onchain liquidity continues to rebalance in market volatility, with this repeating dynamic reflecting the sensitivity of onchain market participants to changing conditions. We believe this reflects the growth in vault deposits, which inherently reflect changing market conditions. The data suggests we’re in a quieter, more selective phase of onchain growth, less about leverage, more about infrastructure.

Dormancy Divergence

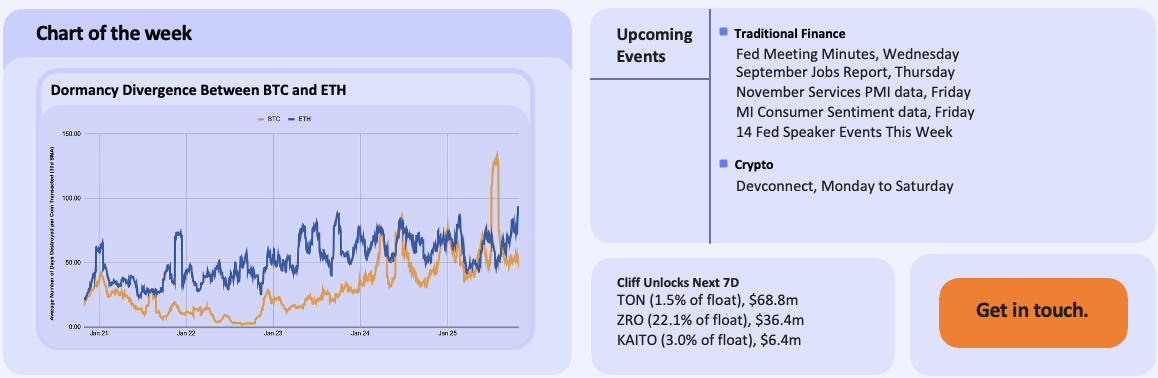

The market has been quick to note that for BTC, Long-Term Holders (LTHs) have been offloading supply since mid-July this year. Despite this, 61% of BTC has not moved in over a year. We believe that dormancy, which measures the average number of stationary days destroyed per coin moved, offers a far clearer behavioural fingerprint. Comparing BTC and ETH, we can see that BTC’s profile shows a steady, structural uptrend over the past five years, punctuated by occasional spikes when very old UTXOs move. ETH’s picture is more dynamic, with dormancy accelerating sharply through mid-2025 as older coins were mobilised through staking rotations, LST redemptions, and collateral shifts in DeFi. While BTC owners continue to sit largely untouched on long-held supply, ETH holders engage with the asset more frequently as part of its role in powering onchain activity.

Interpreting the divergence reveals a maturing two-asset system with distinct economic roles. Rising BTC dormancy underscores its position as the market’s dominant savings vehicle, an asset treated like long-term digital collateral. ETH’s mobilisation is not a sign of weaker conviction, but of utility, in that older ETH naturally ‘breaks dormancy’ when used in productive functions across staking, restaking, and DeFi. The volatility in ETH dormancy reflects usage intensity rather than speculative churn, aligning with its evolution into digital blockspace oil. Keyrock released a report earlier this week alongside Glassnode, which dives far deeper into assessing the monetary-style of BTC and ETH from the perspective of their onchain behaviour.

Our Take: BTC behaves like pure digital savings, while ETH behaves like scarce, productive fuel. The more these patterns diverge, the clearer the bifurcation becomes in how capital allocators, treasuries, and institutions treat the two assets.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.