28 July 2025

Key Insights, Trading The Shift

Passing the Torch

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

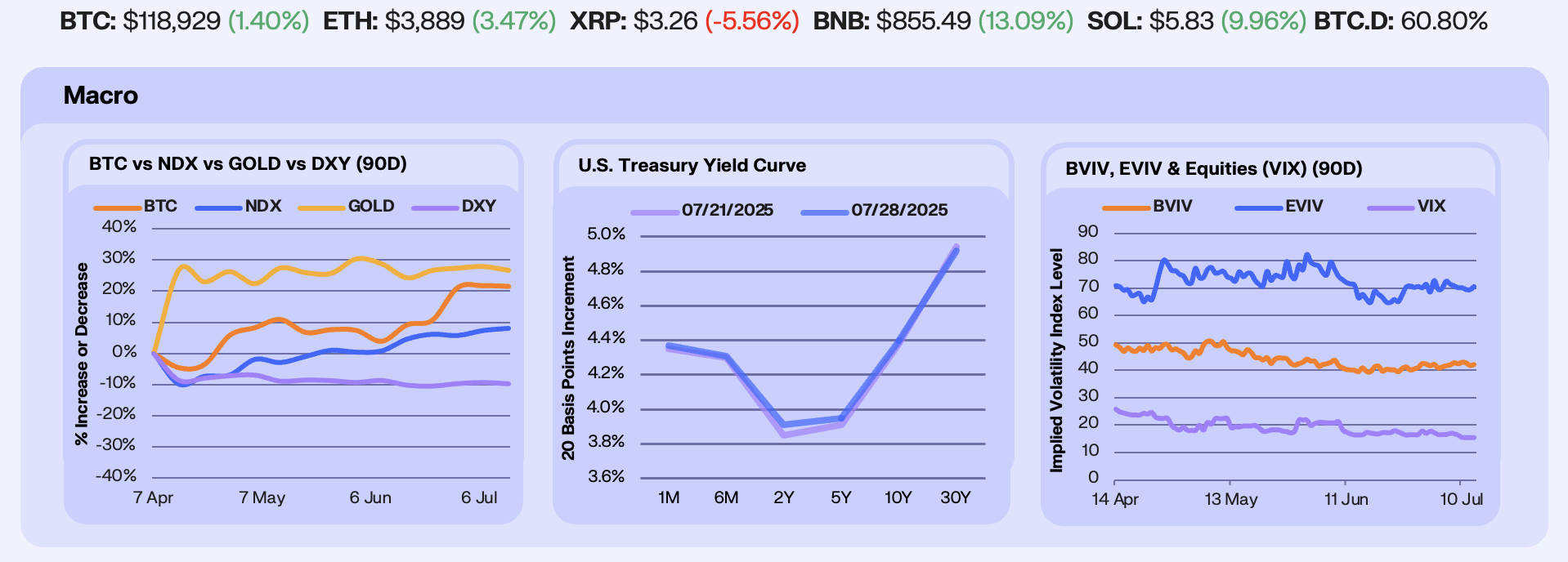

Last week, markets focused on tariff deadlines and the Fed’s policy stance ahead of this week’s rate decision. BTC (-0.2%) and Gold (-1.0%) held near highs amid persistent fiscal concerns, while the USD (-0.5%) continued to weaken. The Nasdaq (+0.6%) hovered near record highs and the S&P 500 broke above 6,350 for the first time, buoyed by resilient earnings and growing optimism around a soft landing. While we expect no rate cuts next week, inflation expectations are lowering and prediction market odds for a 25 bps rate cut in September increased 14%, from 42% to 56%.

Despite softer inflation expectations and rising odds of a September rate cut, long-end yields remain elevated, with the 30Y nearing 5%. This suggests that markets are pricing in more than just disinflation. Strong growth momentum, elevated debt servicing costs, and heavy Treasury issuance are likely contributing to a higher term premium. Even as the front end of the curve reflects an easing outlook, the persistence of high yields at the long end points to structural concerns around supply and fiscal sustainability.

Bitcoin’s implied volatility edged up from 41.9 to 42.1 but remains subdued, anchored by steady ETF flows and active hedging that suppress large moves. Bitcoin options continue to show little urgency for upside, with subdued IV and steady call selling suggesting traders expect the range to hold. **Ethereum, by contrast, remains more momentum driven, with IV still elevated at 70.8, reflecting its higher sensitivity to speculative positioning.

Our Take: With long-end yields still elevated, debt servicing costs rising, and uncertainty around tariffs and Fed timing, BTC appears to be entering a more passive phase. It’s being treated less as a trade and more as a macro hedge. In contrast, Ethereum is drawing speculative flow, with short-dated call demand surging during the move to $3,800. Positioning near $4,000 signals growing appetite for a breakout, one that could accelerate rotation into alts and mark a broader shift away from Bitcoin dominance.

ETH’s The Meta Now

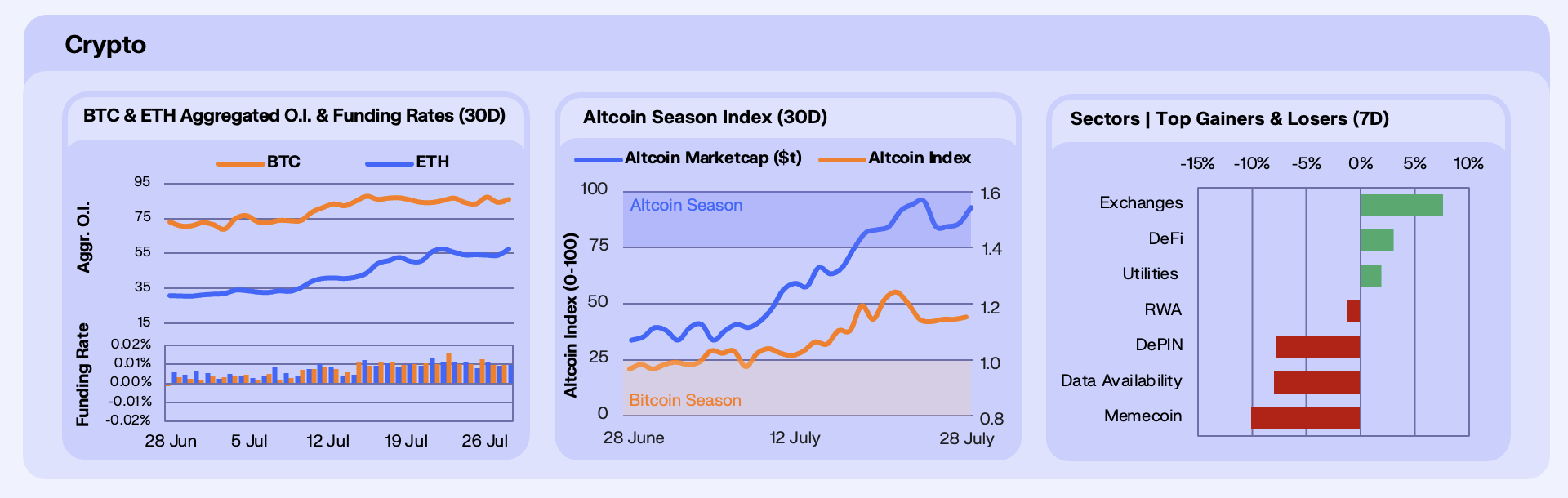

Despite consolidation in crypto markets this week, open interest remained largely unchanged. BTC OI rose slightly from $84.3b to $86b (+2%), while Ethereum’s neared its high of $57.7b. Funding rates climbed across both assets, but particularly in ETH, where positioning remains more aggressive. CME Ethereum futures open interest hit a record $5b, with volume surging to $105b even before month-end. On the broader market, ETH also overtook BTC in futures volume this week, hitting $96.8b versus BTC’s $55.4b (7DMA). The shift in relative activity underscores ETH’s growing appeal as an institutional vehicle.

Beyond Bitcoin and Ethereum, altcoins (+0.6%) paused after last week’s $180b rally in market cap. While memecoins remain prone to sharp weekly swings, DeFi tokens held firm, supported by strong protocol fundamentals and growing institutional interest around stablecoins and tokenization.

Our Take: Even as BTC holds strong, Bitcoin dominance is beginning to roll over and altcoins are showing early signs of life. The market appears to be entering a new phase of the rotation, where ETH strength typically precedes broader alt outperformance. Under the surface, capital is coiling in key sectors: DeFi blue chips are rebounding on renewed onchain activity, while applications and chains powering tokenization and stablecoin settlement are attracting fresh interest. If the rotation holds, these categories could lead the next leg higher.

stETH Shakeout

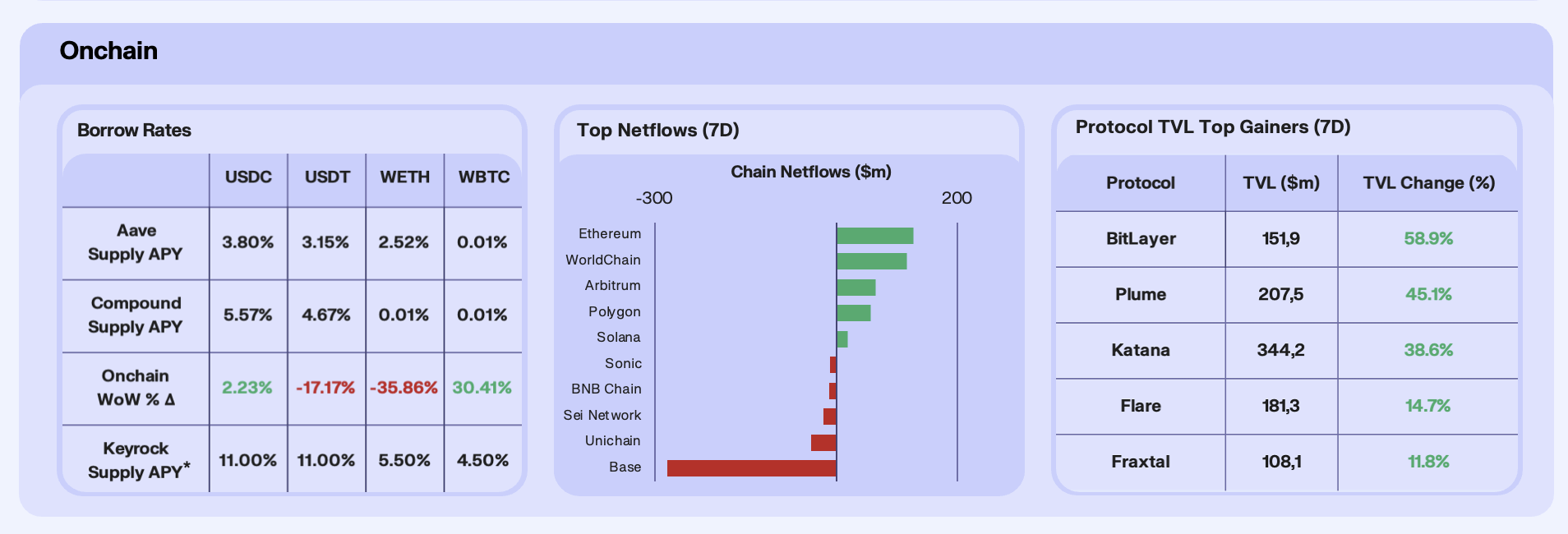

Onchain rates were mixed this week, with WETH posting the largest change in supply APY. ETH borrow rates continued their slide to 2.52% (–35.86% WoW), despite persistent interest in DeFi exposure. This decline in rates is attributed to an increase in supply WoW. The dynamic behind this slide is interesting, with pool dynamics and stETH looping acting as a driver.

Large Whale moves in the Aave WETH pool sent ETH borrow rates through the roof, and thus stETH looping, a popular DeFi strategy, costs to unattainable levels. The rush to unwind positions, coupled with an 18-day ETH validator exit queue, led to stETH sell pressure, resulting in a 30bps de-peg for the dominant ETH LST. Rates then suppressed to end the week, as supply reentered the pool, primarily from users fleeing stETH but still chasing ETH yield. USDC ticked up slightly to 3.80% (+2.23% WoW), while USDT fell sharply to 3.15% (–17.17% WoW).

Chain-level netflows cooled from last week’s highs. Ethereum and WorldChain led with strong inflows, combining for over $300m across the week. Polygon and Arbitrum also saw solid traction, while Base flipped sharply negative, posting the largest outflows by a wide margin.

Protocol-level liquidity gains were modest this week, with no clear unifying narrative. BitLayer led with a 59% TVL jump, driven by growing ecosystem attention around Bitcoin-native DeFi. Plume and Katana followed, up 45% and 39% respectively, though both remain early-stage and influenced by incentive programs. Fraxtal and Flare saw double-digit growth but contributed little to overall market direction.

Our Take: ETH DeFi is evolving, but we see this stETH rotation and subsequent ETH validator exit queue lengthening, as temporary, and driven by one-off events. The important take here is that capital remained in ETH, despite the issues.

The JPEGs Are Moving

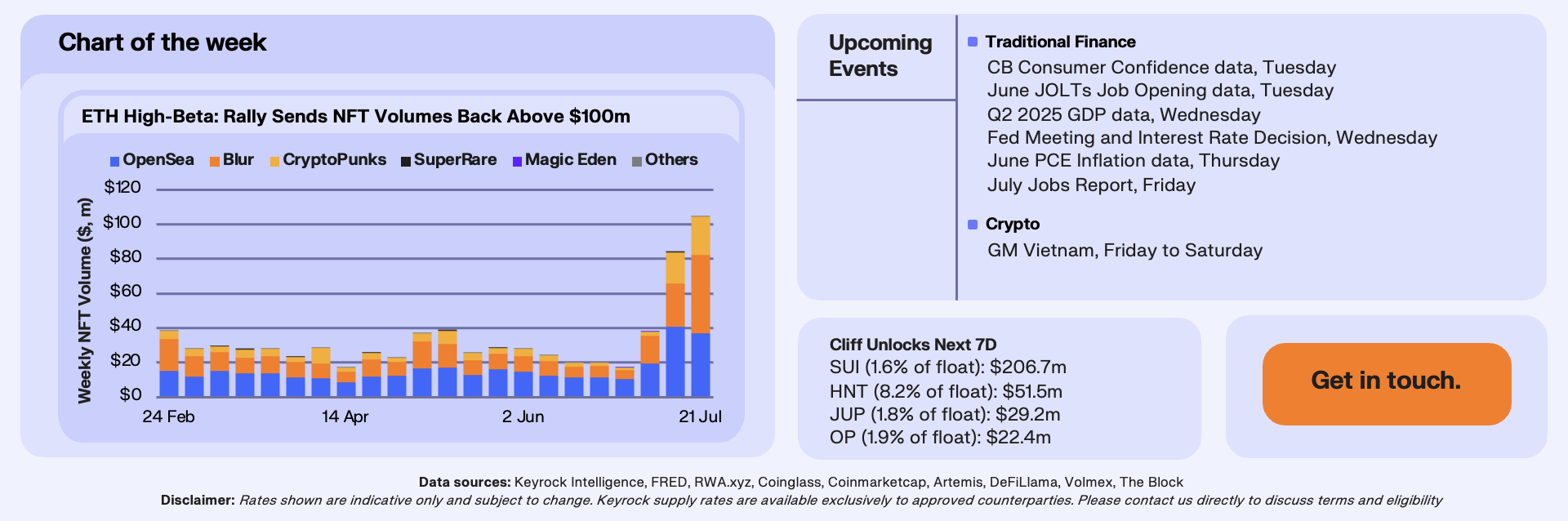

NFT volumes posted their strongest week of 2025, jumping nearly 5x since early July to hit $104.9m. The surge came off the back of ETH’s rally toward $3,800, reigniting risk appetite across the board. NFTs, which act as high-beta ETH exposure, were natural beneficiaries. Bitcoin Ordinals and Solana also saw rising activity, but this was very much an ETH-led move.

Blue-chip collections led the charge. One whale swept 50+ CryptoPunks in minutes, triggering the highest daily Punks volume since November 2024 and pushing the floor above $175k. Fidenzas saw more sales in one week than the prior four months combined, and Ringers ripped on low liquidity and renewed collector interest. The rotation extended into profile picture (PFP) projects too: Pudgy Penguins rose 45%, BAYC climbed back above 11 ETH, and Azuki jumped to 2 ETH, driven by a mix of memecoin catalysts, brand narratives, and growing buyer participation.

The rally wasn’t just whales, buyer counts rose ~80% across the board, and seller numbers followed. Blur and OpenSea volumes spiked, helped by retail FOMO. The return of auction wars, sweep threads, and cultural attention signals NFTs are regaining their place in the risk rotation. With ETH holding strong and liquidity looking for leverage, NFTs are becoming relevant again. Not just as collectibles, but as speculative vehicles with cultural upside.

Our Take: We flagged last week that the early signs of a risk-on shift were forming. This week’s NFT surge adds conviction here. ETH strength is bleeding into longer-duration, higher-beta assets. If the macro backdrop stays stable and ETH remains above $3,500, we think volumes can grind higher into August. But it’s still fragile, narratives are carrying markets, and without real momentum, this rally could cool fast.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.