6 October 2025

Key Insights: The Uptober Show

Shutdown Fuels Uptober Rally

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

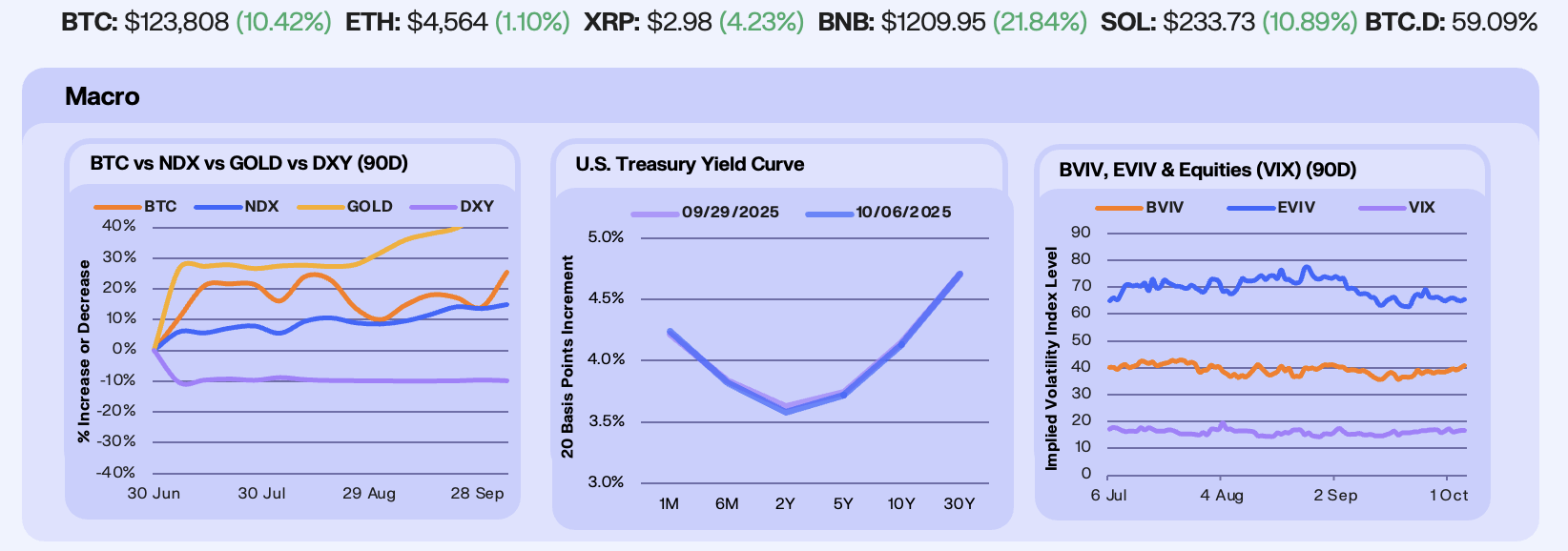

Last week, the US entered its first government shutdown since 2018, forcing the BLS to delay the September jobs report, a key input for the Fed’s rate-cut path. Markets remain uneasy about stagflation, with cuts unfolding as inflation risks linger and job openings hover near their lowest since January 2021. Against this backdrop, BTC rebounded to all-time highs (+10.1%), Gold (+3.1%) marked its 40th all-time high of 2025, the NDX (+1.2%) grinded higher, while the US Dollar (-0.3%) is tracking its worst year since 1973, down 9.8% YTD.

The yield curve edged lower this week as the U.S. government shutdown left investors to lean on the ADP National Employment Report, which showed private employers cut 32,000 jobs, the biggest drop since March 2023. The 2Y–5Y led the move, down 2–5 bps, while the 10Y slipped 2 bps. Meanwhile, Polymarket now prices a 90% chance of a 25 bps cut on October 29, up from ~80% earlier in the week. There’s growing expectations for additional easing as growth indicators soften, even as inflation tail risks persist.

Implied vols held steady this week as markets rallied, with BVIV hovering near 41 and EVIV flat in the mid-60s. The VIX edged +5.1% to 16.7, yet stays near multi-month lows. The recent rally has flattened option skews, with short-dated BTC and ETH smiles moving back toward balance as the put premium fades. Strong spot ETF inflows have reinforced that shift, easing pressure on downside hedges. The next test is whether vols can remain muted as macro data and Fed expectations dominate the October calendar.

Our Take: As we noted in last week’s update, the Uptober playbook is holding. The Fed’s path is being shaped by a weakening labor backdrop, but ETF inflows and seasonality are giving Bitcoin room to rally alongside gold. With option skews normalizing and vols still cheap to tail risk, traders have shifted from defensive puts to balanced positioning. The test now is whether macro softness can sustain the bid, or if inflation surprises cap the upside into Q4.

Risk Appetite Reignites

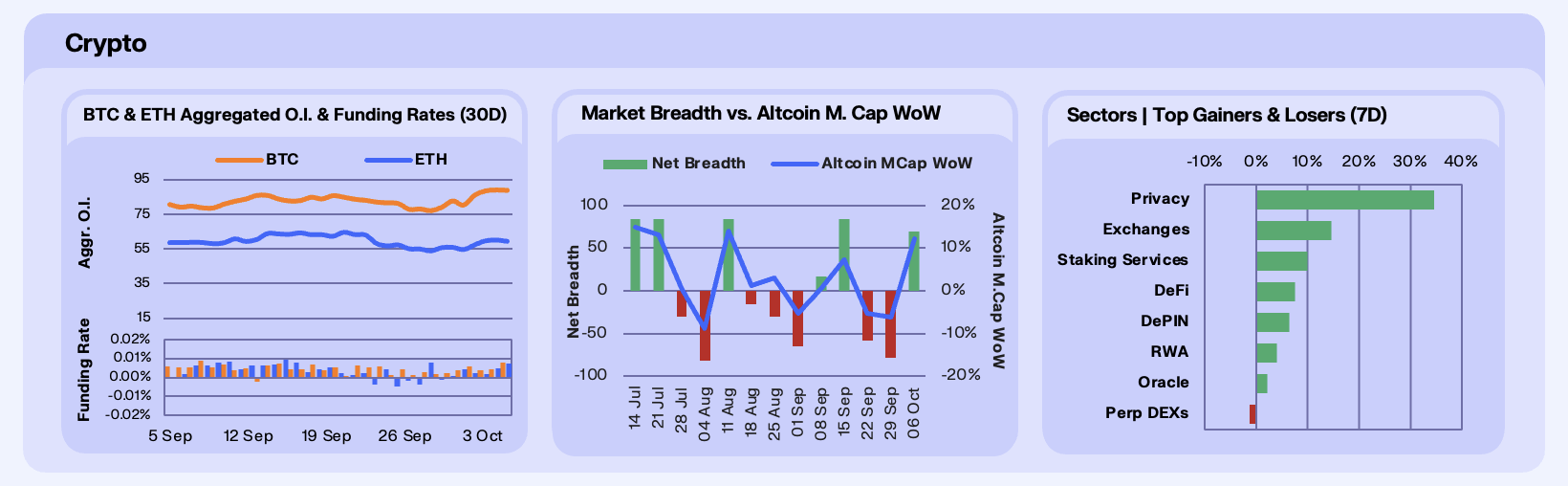

BTC OI climbed to $88.5b from $79.2b at the start of the week (+11.8%), while ETH OI rose more modestly to $59.7b from $55.7b (+7.1%). Binance and Bybit long/short ratios spiked to 53.8% and 50.7%, the highest since mid-July. There’s renewed speculative optimism after weeks of ETF-driven selling and liquidations as traders lean into longs on expectations of stabilizing outflows, supportive Q4 seasonality, and rising odds of Fed easing into year-end.

Funding rates stayed positive across BTC and ETH, showing continued willingness to pay for long exposure, though Ether’s rate remains close to neutral after last week’s sharp negative spike. Elevated leverage highlights bullish conviction but is also raising the risk of crowding, where a failure in spot follow-through could quickly flip into liquidation cascades.

Altcoins staged a strong rebound this week, with market cap rising +12.3% and breadth flipping back positive at +70 (84 advancers, 16 decliners). The recovery follows last week’s steep -6.1% drawdown and shows risk appetite rotating back into alts as ETF flows stabilize and Q4 seasonality kicks in. Participation was broad across majors and mid-caps, suggesting healthier momentum, though sustainability will hinge on macro conditions and whether BTC can extend its rally

The privacy sector (+34.6%) was the best performer in the market last week. The surge was driven by Zcash due to a renewed focus on financial privacy amid growing concerns over surveillance and data tracking. Prominent voices like Naval Ravikant describe ZEC as “insurance against Bitcoin” and a hedge against surveillance.

Our Take: In crypto markets, robust breadth is often interpreted as confirmation that strength is broadening beyond just a few leaders. While it doesn’t guarantee continuation, many traders view it as a more durable form of momentum. This week’s rebound in altcoins comes during October’s seasonal tailwinds for crypto and potential ETF-related inflows as supportive drivers. Given the breadth recovery, we lean toward sustained participation into October, acknowledging, however, that a breakdown in breadth would raise red flags.

Uptober Liquidity Flows

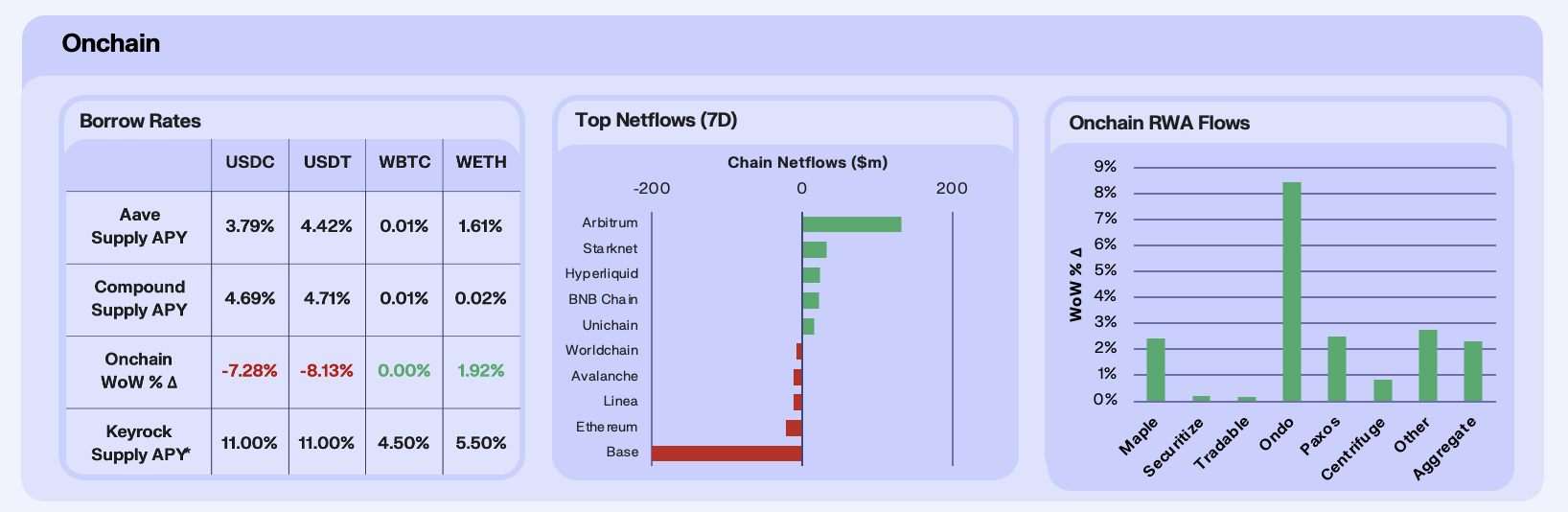

Stablecoin lending softened this week as deposits outpaced borrow demand across major pools. USDC and USDT APYs fell 7.3% and 8.1% WoW respectively, as Aave supply balances surged, up 19.8% for USDC and 43% for USDT. ETH yields edged slightly higher, up 1.9% WoW, on lighter supply, while WBTC rates remained negligible. Overall, the rate compression reflects a capital-heavy onchain environment, with abundant liquidity but low looping-centric leverage.

Chain netflows again highlighted Arbitrum’s dominance in the L2 rotation theme, recording $180 million in inflows driven by DeFi incentives and perps-led volume growth. The ongoing DRIP rewards program lifted yield-bearing USD assets to a record $497 million AUM, up 16% WoW, while lending TVL reached $1.8 billion, with Morpho, Euler, and Silo all hitting ATHs. In contrast, Base saw $208 million in outflows, its worst since May, amid operational strains. Rumours of a native BASE token have yet to offset damage from recent scams and ecosystem exits, with sequencer losses and declining incentive efficiency weighing on sentiment.

RWAs extended their rally, with aggregate AUM up 6.1% WoW. Maple led with 13.5% WoW growth, as syrupUSDT on Plasma filled a $200 million vault in under a minute, while syrupUSDC liquidity reached $4.18 billion and partnerships with Chainlink, Kamino, and Drift fueled 265% YTD revenue growth. Securitize gained 9.7%, propelled by BlackRock’s BUIDL fund crossing $1 billion AUM and new integrations with Ripple and RedStone. RWAs now exceed $33 billion sector-wide, underscoring tokenisation’s role as DeFi’s most consistent growth engine.

Our Take: Capital rotation continues to define onchain activity. Liquidity is abundant but selective. Arbitrum’s structured inflows show incentive-driven growth can transition into sustainable liquidity if reinforced by product and tech depth. With October historically strong for DeFi TVL and tokenised yields, ‘Uptober’ could extend beyond price action into fundamentals.

Venture Capital Floods Crypto

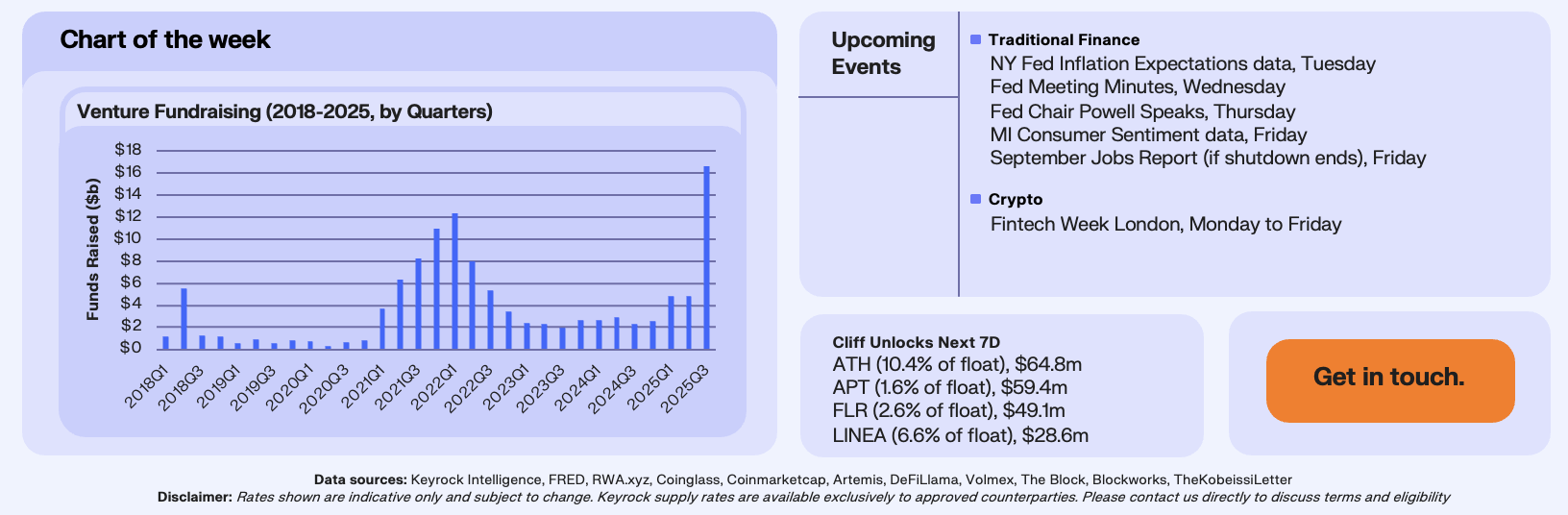

Crypto venture funding closed Q3 2025 at an all time high of $16.6 billion, the largest quarterly venture injection into the industry on record. At $3 billion higher than the second largest funding quarter back in Q4 2021, this is a clear signal that institutional capital is rotating back into digital assets at scale. The period was defined by major raises across both infrastructure and DAT companies. Ether Machine’s $645 million private financing ahead of its Nasdaq listing epitomised this trend, with several other DATs and infrastructure players raising in the nine-figures in single rounds. The result is a funding landscape less dependent on speculative consumer activity and increasingly dominated by stickier capital with longer-term alignment.

We view this as institutional allocators positioning ahead of adoption catalysts such as (i) further ETF approvals, with assets down the risk continuum as well as more complex flavours of existing assets such as staking ETFs, (ii) onchain credit markets, and the rise of tokenised real-world assets, (iii) potential macro and monetary headwinds that may favour digital assets, amongst other catalysts. The data shows this isn’t a retail-driven revival, with 82% of projects funded this year being tokenless, highlighting a shift away from the decentralised ethos of crypto protocols towards a more traditional structuring, reflecting the type of capital flowing into the space.

Our Take: The venture flywheel is turning again, and this time it’s being powered by institutions. With over $16 billion in fresh capital targeting the intersection of treasury management and onchain infrastructure. If DATs continue to attract and deploy capital at this pace, the second order effects felt in Q4 2025 and into 2026 could dramatically shift crypto’s capital base, with implications flooding onchain.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.