24 November 2025

Key Insights: The Trend Isn't Your Friend

Risk-Off Momentum Builds

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

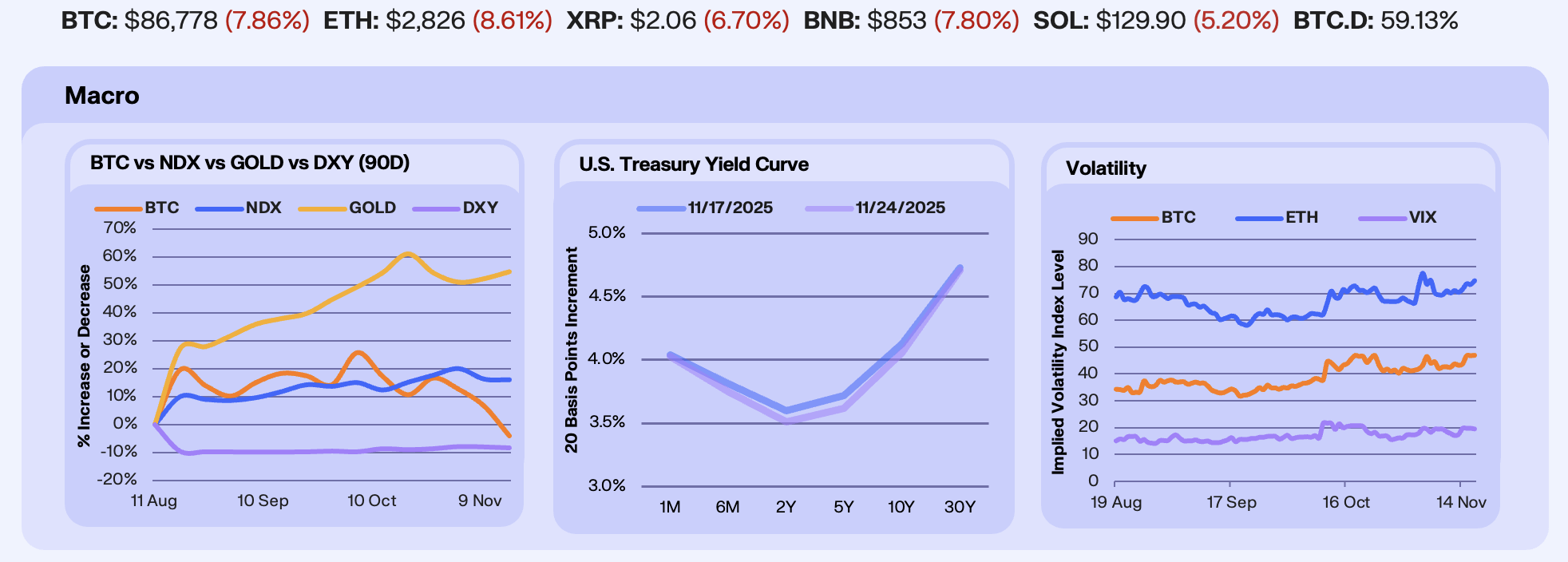

Last week brought the first clean read on labor conditions with the release of the government’s monthly payrolls, which beat expectations on the headline but revealed softening beneath the surface. Unemployment continued to drift higher, reinforcing concerns about weakening economic momentum as December Fed cut odds inched up to ~68%. Investors stayed cautious as BTC fell -7.8%, NDX dropped -3.1%, and the U.S. Dollar rose +1.0% amid a renewed flight to safety. Global equities logged their worst weekly performance since April’s tariff volatility, while NDX still leads BTC by 24% YTD despite the recent pullback.

Treasuries followed the macro tone with a bull steepening. Week over week, the 2Y-5Y eased 9-10 bps, while the 10Y eased 7 bps to 4.06%. The curve remains bowed but nudged lower across the belly as traders balanced softer labor signals against a Fed still unwilling to signal a turn. Abroad, Japan’s consideration of $110b in new stimulus drove a sharp jump in 40Y yields and weakened the yen, an illustration of how quickly long-end rates can reprice when fiscal pressure accelerates, and a reminder of the fragility embedded in the U.S.’s own deficit path.

Volatility picked up meaningfully across asset classes. Implied vol in BTC and ETH options stayed elevated, with BTC IV up 17.6% to 55 and ETH IV rising 2.6% to 76.7. The move was led by short-dated maturities as investors rushed to add downside protection, while the VIX jumped 32.6% to 25.3, its highest close since April. Option smiles stayed firmly skewed toward protection, and markets now assign a ~42% probability that BTC finishes 2025 above $100K. The move reflects mounting concern over an equity pullback and a broader repricing of global liquidity as the dollar strengthens. With positioning still asymmetric, the volatility regime is shifting decisively more defensive.

Our Take: The dollar remains the macro fulcrum for risk assets. Its strength is pulling global capital toward safety and away from speculative exposures, leaving Bitcoin trading more like a high-beta liquidity proxy than a macro hedge. Sentiment has washed out accordingly as Bitcoin’s Fear & Greed Index just hit its lowest level since 2022, historically a constructive entry point. But until the Fed softens or growth data stabilizes, volatility risks remain skewed to the downside.

Confidence Collapse

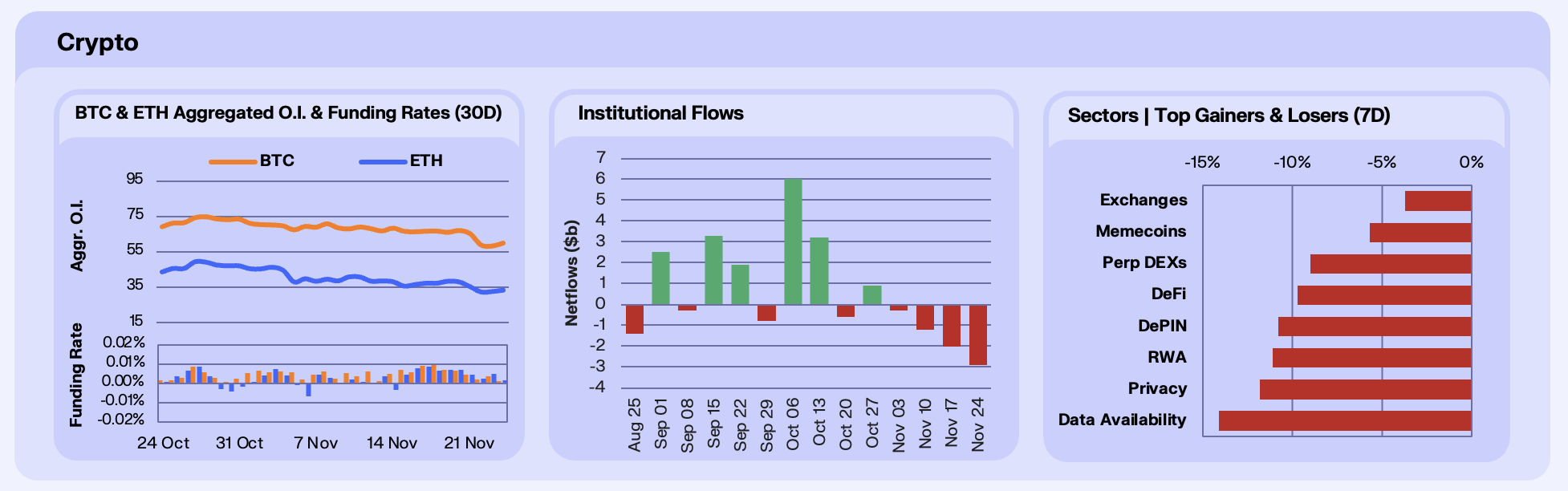

Sentiment across crypto markets turned sour last week, as the market suffered another heavy week of selling, with BTC, ETH and SOL down 8.4%, 11.1%, and 7.2% respectively. The selloff was driven primarily by macro pressure and ETF outflows haunting investors. Majors came under pressure from more than $2b in forced liquidations, while US demand remained soft, with the Coinbase Premium deeply negative for a third consecutive week, one of the longest stretches this cycle. SOL was the lone exception from an institutional perspective, with continued ETF inflows providing a modest cushion, though still not enough to offset the broader market stress.

OI unwound sharply, with BTC OI falling 10.2% WoW and ETH OI down 10.4%, effectively retracing almost all of early November’s build-up. Funding rates hovered just above neutral across majors, indicating a lack of speculative appetite and a broader shift toward risk minimisation. This week futures basis tightened, options skew flipped defensively, and trading volumes concentrated on major venues, with traders reducing directional exposure.

Institutional flows deteriorated meaningfully this week, for their fourth consecutive, and incrementally increasing, decline. Crypto ETPs saw -$2.9b in net outflows, the worst weekly print of the year. BTC institutional funds led the bleed with over $1.2b exiting, marking the third-largest weekly withdrawal since spot ETF launch day. As mentioned, SOL was a bright spot, with inflows across multiple days, sustaining a multi-week streak and reaching nearly $500m cumulative since launch. But at the aggregate level, November has now seen the heaviest month of ETF redemptions, reinforcing the risk-off tone across the asset class.

Our Take: This week saw one of the most intense confidence recessions we’ve seen this year, with October 10th sentiment looming and worsening in the face of macro stress tightening financial conditions. ETFs amplified outflows, and derivatives markets cleared leverage cleanly. With OI washed out, funding near neutral, and institutional flows capitulating, the market is now running lighter and cleaner into December. If macro stabilises, the setup favours a more constructive Q4 close, but for now, crypto remains firmly in defensive mode.

Onchain Rotation Continues

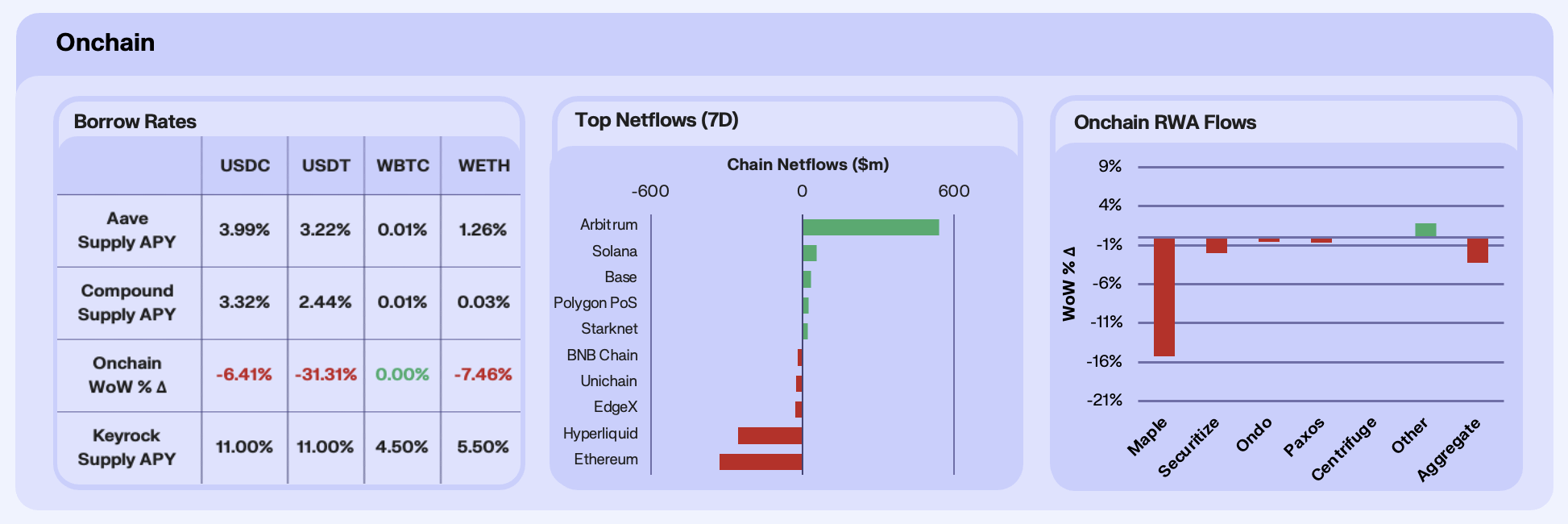

Onchain lending markets continue to soften as risk-off sentiment deepens within crypto markets. Stablecoin yields drifted lower as liquidity rotated out of risk and into defensive positioning. USDC and USDT supply APYs on Aave fell 6.4% and 31.3% respectively WoW, reflecting supply expansions accelerating borrow demand. WETH also cooled, with supply APY down 7.5% WoW. ETH was the lone outlier on Aave, where rising utilisation pushed APY up 4.9% WoW, a modest reversal after October’s deleveraging. Broadly, the rate environment continues to signal caution, with lenders parking stablecoins for passive yield.

Arbitrum led all networks in chain netflows this week, with over half a yard of inflows for the week alone, accelerating a multi-week rotation. Hyperliquid saw over $250m in outflows following the POPCAT manipulation event and a temporary withdrawal freeze that compounded already-heavy perp liquidations. Ethereum posted $337m in outflows as ETF redemptions drove capital away from the chain. Overall, flows this week mirror broader market dynamics of derisking from perps-specific networks and institutional outflows from L1s.

RWA markets proved more resilient, though still faced significant pressure. Aggregate AUM fell 3.24% WoW, pulled down almost entirely by Maple’s 15.24% decline following its high-profile legal dispute with Core Foundation, which froze ~$150m in assets and triggered institutional redemptions. Securitize, down 2%, and Ondo, down 0.6%, saw measured outflows tied to ETF-driven derisking and October’s market unwind, while Centrifuge was flat. The dispersion reflects a split market where credit-heavy RWAs faced the brunt of risk-off flows, while tokenised treasuries and diversified structures weathered the downturn more comfortably.

Our Take: The onchain data is behaving exactly how a mature market should during a correction. Rates are resetting, while capital consolidates into higher-quality venues, and RWAs are holding their ground aside from protocol-specific shocks. With leverage largely flushed and capital sitting defensively, the setup going into December is cleaner than headline price action suggests.

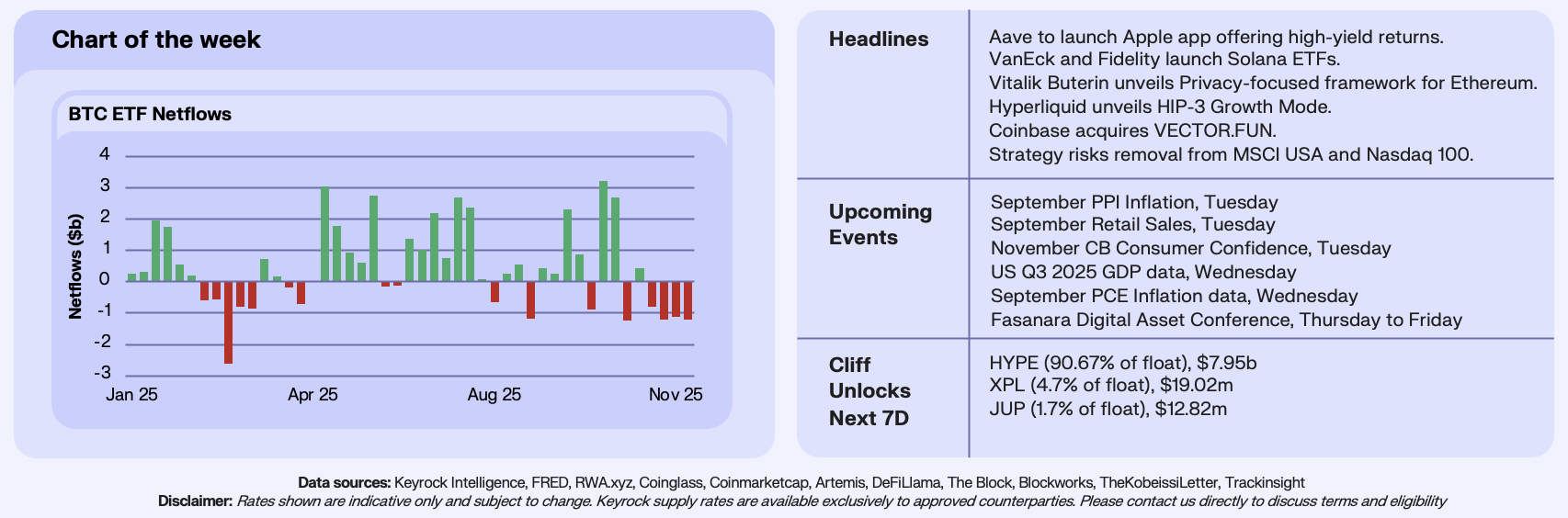

BTC ETF Pressure Mounts

BTC ETFs saw their heaviest week of redemptions since March, with roughly -$1.2 billion in netflows. Nov 20 marked the largest single-day outflow on record at approximately -$903 million, driven primarily by withdrawals from the largest issuers. BlackRock’s IBIT recorded -1.08 billion in net outflows for the week while Fidelity’s FBTC saw -120 million in outflows. These two products alone accounted for the majority of the pressure, reflecting a decisive pullback in institutional BTC exposure as macro uncertainty intensified.

The outflows occurred as investors rotated toward safety. The U.S. dollar continued to attract inflows, while the BTC-gold correlation has broken down sharply, turning negative and reaching approximately -0.30 in Q4. That shift indicates that Bitcoin has further decoupled from its defensive-asset narrative and is instead trading as a high-beta risk proxy. With ETF redemptions accelerating precisely as liquidity tightens and rate-cut expectations wobble, institutional positioning is adjusting to a more cautious macro regime.

Our Take: Bitcoin’s ETF flows are no longer functioning as a stabilizing force; if anything, they are amplifying weakness during periods of macro stress. Institutions aren’t abandoning Bitcoin, but they are increasingly treating it as a variable-beta exposure rather than a strategic core holding. As that shift accelerates, Bitcoin becomes far more sensitive to liquidity conditions, interest-rate expectations, and broader risk sentiment than to any idiosyncratic fundamentals.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.