29 September 2025

Key Insights: The Silence of the Doves

Powell Pushback Rattles Markets

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

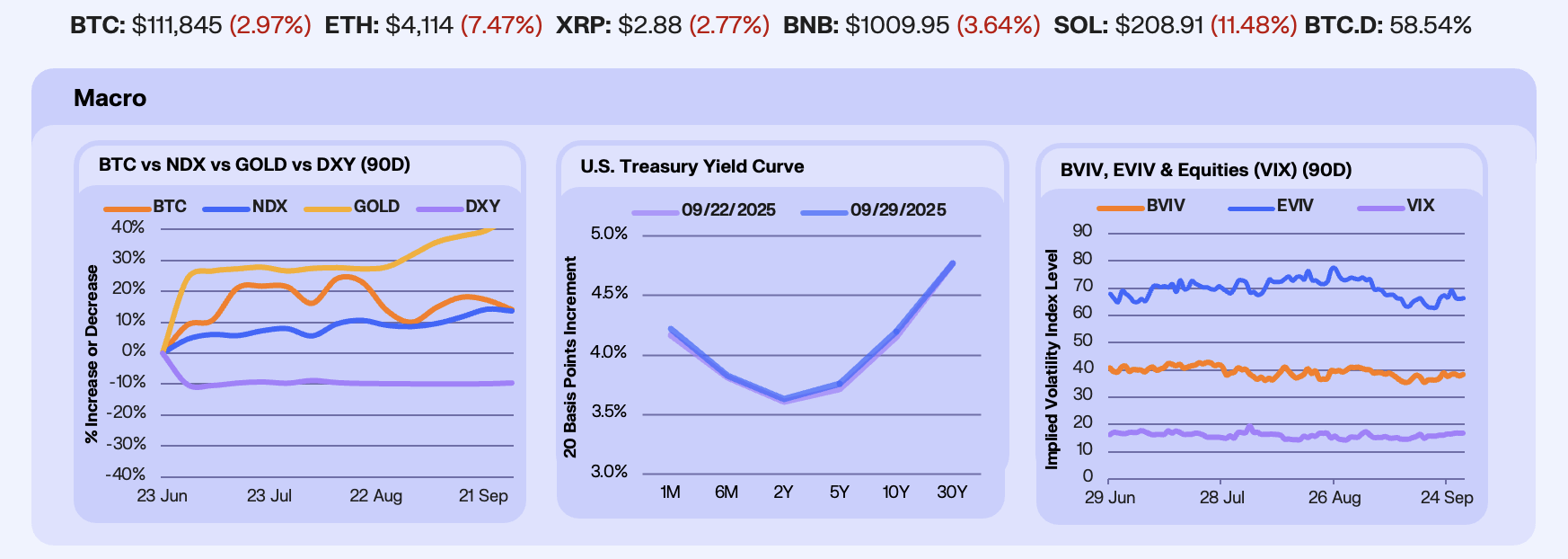

Last week Fed Chair Powell pushed back on rate cut hopes even as Q2 GDP was revised higher to +3.8%, the strongest reading in nearly two years, supported by resilient consumer spending, rising incomes and lower imports. He warned that easing too aggressively in today’s ‘low-hire, low-fire’ economy could leave inflation unresolved. Markets slipped with BTC down -2.7%, the Nasdaq lower by -0.5%, while Gold gained +1.4% to new highs on record global ETF inflows and the DXY rebounded +0.5% on Powell’s hawkish remarks.

The yield curve shifted higher across most maturities this week, with the 1M, 5Y, and 10Y each rising 5 bps, and the 6M and 2Y up 2 bps after Powell framed last week’s cut as a “risk-management” move rather than the start of an aggressive easing cycle. The 30Y was unchanged, as strategists continue to flag sticky services inflation and heavy Treasury issuance as structural pressures on duration. Without softer inflation or a shift in supply dynamics, the long end is unlikely to see meaningful relief.

Implied vols climbed last week as crypto markets absorbed over $2.5b in liquidations. Bitcoin IV gained +3.7% and Ethereum IV edged +0.2% while the VIX rose +4.7%. The spike in BVIV sent traders rushing for protection into forced unwinds and suggests optionality is finally being repriced after weeks of calm. The next test is whether spot stabilizes on upcoming macro data or if another wave of liquidations drives hedging demand higher.

Our Take: Powell’s caution now centers on the labor market, where payroll growth has slowed to around 30k a month and unemployment has ticked up toward 4.3%. That fragility makes the Fed wary of cutting too fast or too slow, a balance that leaves risk assets on edge. For Bitcoin, October’s strong seasonality and the prospect of rate cuts into a softening jobs backdrop argue for closer correlation with gold. After a wipe in liquidations, positioning looks cleaner but the market still needs to see where BTC can find its footing into Q4.

Risk Reset in Crypto

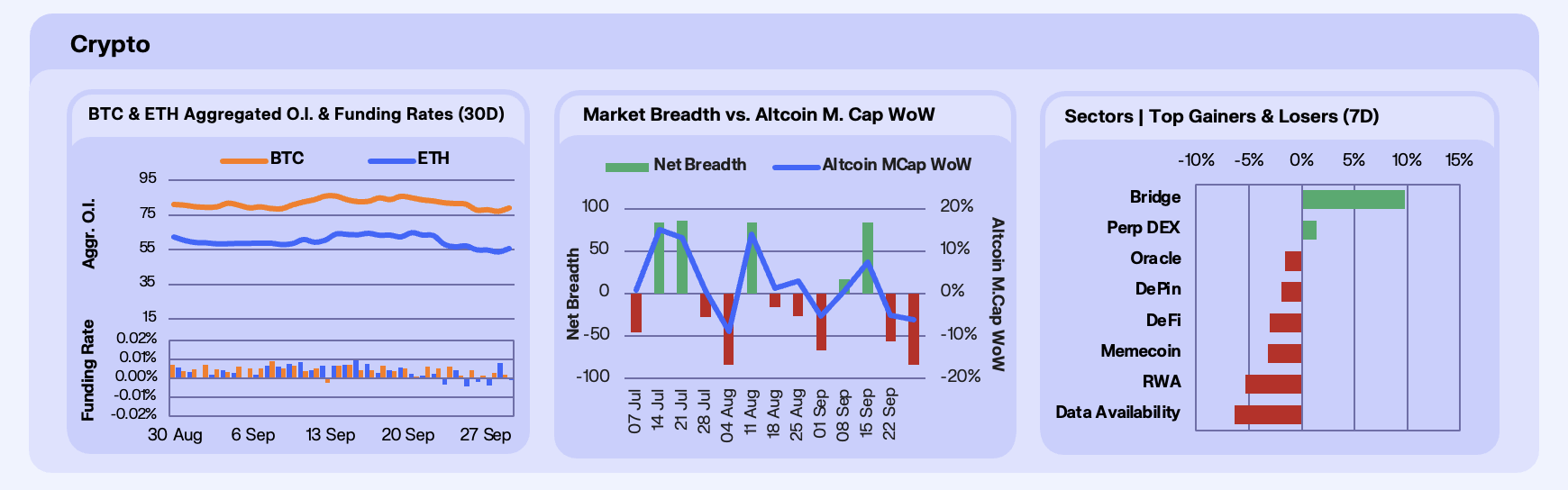

Majors ended the week lower, with BTC down 2.3%, ETH down 4.3%, and SOL down 8.4%. The decline was fueled by ETF redemption waves, including $363m worth of outflows from BTC products and a record $795.6m from ETH ETFs. This occurred alongside cascading liquidations of approximately $1.7b market-wide, including $45m in SOL longs, and supply overhang from token unlocks in SOL. Macro headwinds like rising bond yields added pressure, though steady accumulation from digital asset treasury companies provided a partial offset.

Derivative positioning reinforced this reset. BTC OI fell 3.6% WoW to $79.2b, while ETH dropped 4.2% to $55.7b. Funding rates stayed muted, with BTC positive and ETH flipping negative mid-week, reflecting a cautious long bias in BTC versus fading conviction in ETH. The divergence suggests institutions are de-risking from ETH while keeping measured exposure to BTC.

Market breadth weakened sharply, with altcoins posting net -84 breadth and a 6.1% WoW market cap decline. Just 8 tokens advanced versus 92 decliners, marking the weakest participation since early August and underscoring how liquidations and ETF flows weighed broadly across non-majors, and capital rotated up the risk continuum in this sentiment shift.

The broad base nature of this risk off shift is evident by the majority of sectors printing losses this week. Only bridge protocols (+9.8%) and Perp DEXs (+1.4%) gained. Notably, perp DEX momentum was underscored by ASTER, which surged 38% on Binance listings, strong fundamentals, and CZ backing.

Our Take: The synchronised ETF outflows mark an institutional reset, but the persistence of DAT accumulation suggests capital is not leaving crypto altogether. Instead, risk is being repriced. If ETH’s ETF bleed stabilises, breadth could recover quickly. Watch October ETF review timelines as the inflection point in the coming weeks, where fresh approvals or slowed redemptions could flip sentiment back to risk-on faster than expected.

RWA Growth Persists

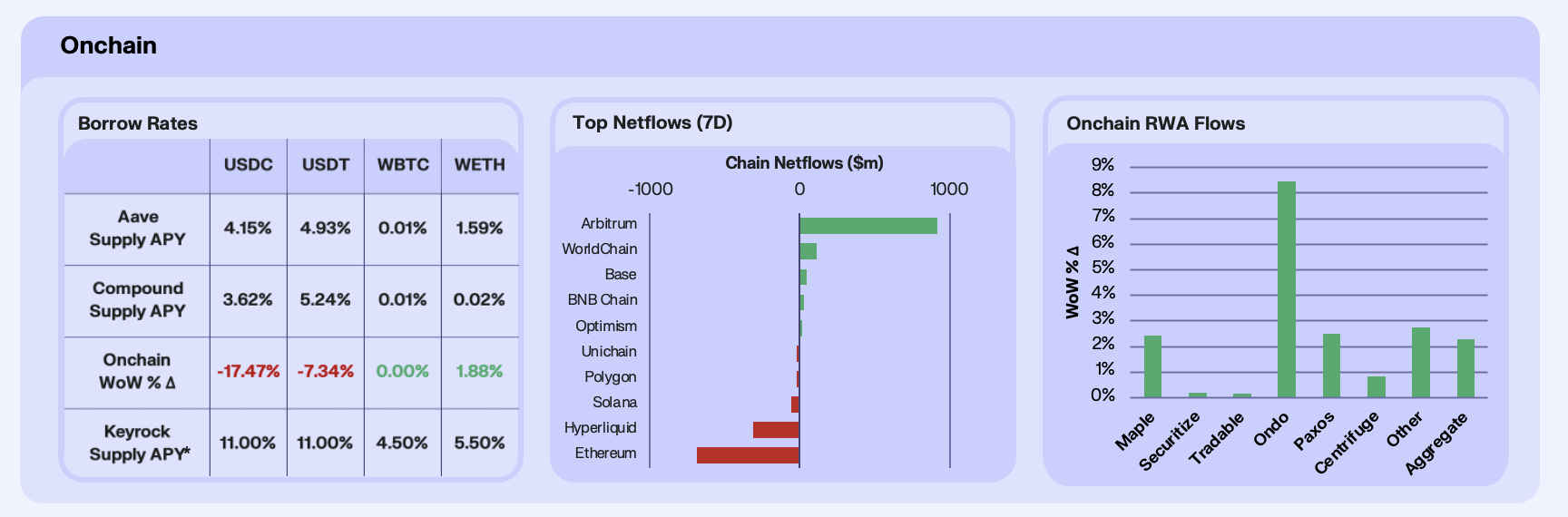

Onchain borrow rates softened this week, with stablecoins leading the move lower as fresh deposits outpaced borrow demand. USDC APY fell 17.5% WoW and USDT slid 7.3%, driven by Aave supply balances jumping ~39% across both assets. The dynamic reflects a familiar pattern of subdued demand to lever stables in risk-off market conditions. ETH rates were marginally higher, up 1.9% WoW, aided by an 11% supply contraction, while WBTC yields remained negligible.

Chain netflows highlighted a decisive rotation into Arbitrum, which posted $920m in inflows, far outpacing all peers. Liquidity migrated from Ethereum, which saw $687m in outflows, while Hyperliquid also shed $313m amid unlock concerns and a protocol exploit to Hyperdrive, a lending protocol in the HyperEVM. Smaller ecosystems like Solana, Polygon, and Linea saw muted outflows, while Base and WorldChain flows were broadly flat. Arbitrum’s ability to absorb capital at scale reflects the compounding effect of RWA activity, DeFi incentives, and sticky liquidity directed from Hyperliquid.

RWAs extended their run of steady growth, with aggregate AUM up 1.96% WoW. Maple led with an 8.6% surge, building on the momentum of its syrupUSDC product. Ondo rose 3.4%, pushing TVL toward $1.6b as tokenised Treasuries and equities drew flows, while Centrifuge added 2.5%, supported by institutional allocations. Paxos gained 1.8% on stablecoin integrations, offsetting a mild 1.5% dip in Securitize. With multiple protocols rolling out composable yield products, RWAs remain one of the few categories consistently growing despite broader DeFi volatility.

Our Take: This week’s flows reinforce market sentiment. DeFi remains heavily reflexive to broader market moves, particularly onchain rates. RWAs continue to prove themselves as the most reliable structural growth engine. We believe onchain flows and rates will remain reflexive throughout the rest of the year.

Onchain Management Powerhouses

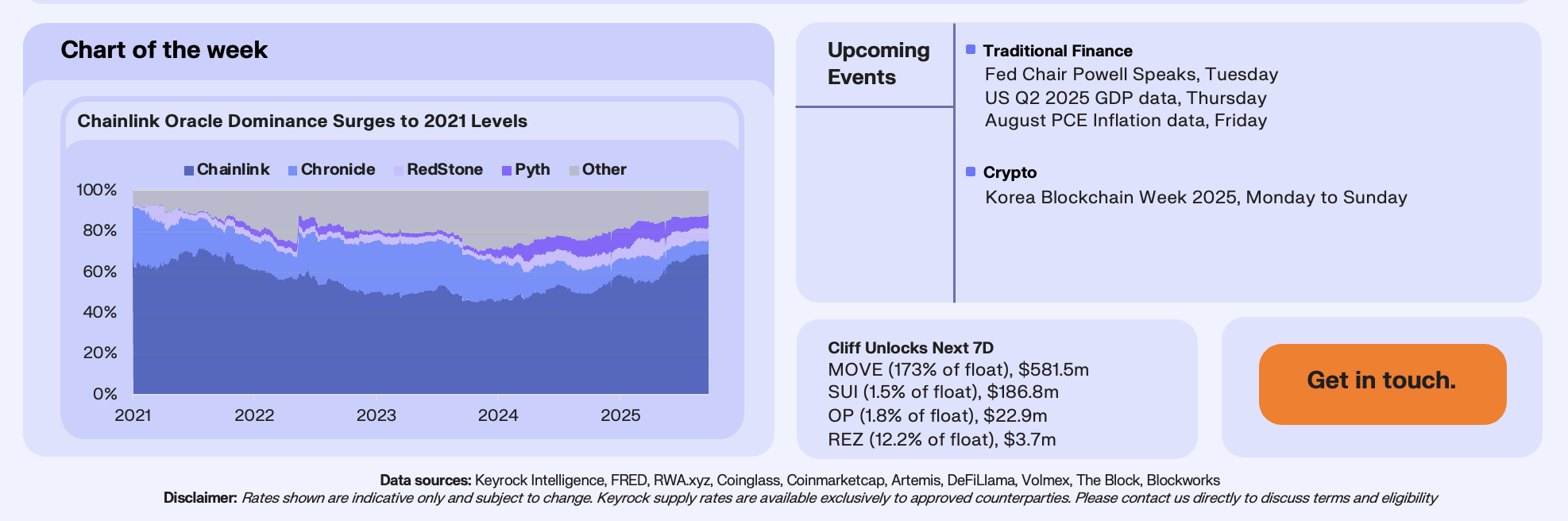

Morpho, Pendle and Maple now account for 62% of total onchain asset management AUM , underscoring how quickly specialist protocols are consolidating share in a market that only recently was led by general vaults. Morpho has climbed to $9.6b AUM, pushing to new highs as it cements itself as the largest onchain vault infrastructure. Pendle dominates the structured products vertical with $8.7b AUM, anchored by Ethena’s sUSDe which alone accounts for 70% of Pendle’s flows. Maple has established itself as the leading protocol in onchain credit with more than $3.3b AUM.

The rise of these three protocols reflects a broader shift in allocator behavior as our latest report highlights. Flows are increasingly moving into protocols offering specialization and institutional alignment. Morpho’s dual role as lending and vault infrastructure has made it a core building block across DeFi. Pendle has created liquid forward yield markets that attract DeFi natives seeking interest rate exposure. Maple has built a credit vertical that channels capital directly into institutional pools, a segment that scarcely existed onchain just three years ago.

Our Take: Nearly two third of industry AUM is now concentrated in Morpho, Pendle and Maple. These protocols have established themselves as leaders in vault aggregation, structured yield and credit, and their collective share highlights the direction of onchain asset management. With the industry projected to reach $64 billion AUM by end-2026 in the base case and as much as $85 billion in the bull case , we expect their share to expand further as allocators channel more liquidity into these verticals. Our latest report, ‘Onchain Asset Management: Designing the Future of Investment Strategies,’ explores this transformation in depth.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.