11 May 2026

Key Insights: The Pivot Week

Powell's Swan Song

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

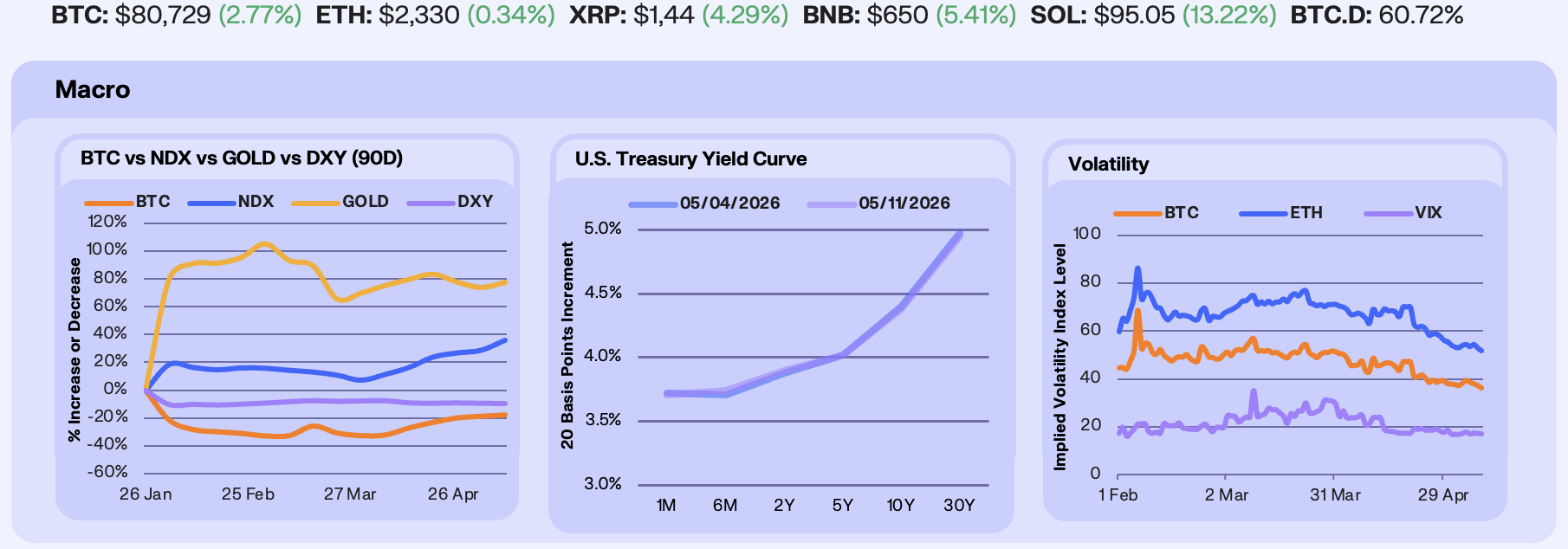

Risk assets rallied across the board into a record close. NDX added +5.50% to 29,234 on the 6th straight weekly gain for US equities, the longest streak since 2024, with strong mega-cap earnings led by AMD layered onto Thursday’s Court of International Trade ruling that struck down the Section 122 10% tariff surcharge Trump imposed in February. Gold added +2.07% to $4,679 as Iran and Hormuz stayed unresolved, with Tehran’s counter-proposal called “totally unacceptable” by Trump on Sunday after both sides exchanged fire Friday and a South Korean cargo ship was struck in the Strait. BTC caught the bid late and closed +1.21% at $80,791, with DXY -0.14% at $98.05, the dollar caught between softer wages and a hawkish committee.

Treasury yields rallied across the belly and long end. 2Y rose +2bp to 3.90%, 10Y -2bp to 4.38%, 30Y -3bp to 4.95%. April NFP printed +115K against +55-65K consensus Friday, but AHE landed at +0.2% MoM and +3.6% YoY, both below estimate, with the labour force shrinking and revisions roughly neutral. The low-hire low-fire read kept the cut trade alive at the back without forcing it into the front. Treasury’s Wednesday refunding statement kept coupon sizes flat at $125B and guided the same profile for the next several quarters, with the higher Q2 deficit funded through bills, removing the long-end supply pressure markets had positioned for. Productivity growth is sustained and tech-driven, a dovish supply-side framing into the chair handover.

Volatility compressed across the board. VIX closed -1.09% at 17.19, BTC 30-day ATM IV -5.39% at 36.18, ETH 30-day IV -4.20% at 51.83. While correlation between BTC and ETH remains elevated near 0.9, BTC continues to outperform ETH. BTC has broken out of its trading channel, whereas ETH is still struggling to do so. BTC dealer gamma remains relatively balanced, with sizeable positive call gamma above the 85-90k zone likely to dampen realized volatility. In contrast, ETH positioning shows signs of overwriting around the 2.3k area. As we expect this trend to continue, investors can express the view as a long BTC / short ETH premium-flat options structure, buying BTC upside exposure via calls and selling ETH calls against it.

Our Take: The biggest unpriced macro catalyst on the calendar lands this week. The Senate convenes Monday for the Warsh cloture vote ahead of Powell’s chair expiry on Friday May 15, with April CPI between them on Tuesday and the $125B in 3Y/10Y/30Y coupon auctions running Monday through Wednesday. Warsh has publicly argued for shrinking the Fed balance sheet faster than the current QT taper, and the reserves regime running at that pace is what has supplied the floor under risk since 2022. Faster QT pulls dollar liquidity down before it pulls rates anywhere, and a more politicized Fed running tighter reserves is the path that reprices the long end and the dollar before any cut narrative returns. Friday is a regime change the market is treating as a name change.

Spike, Unwind, Repeat

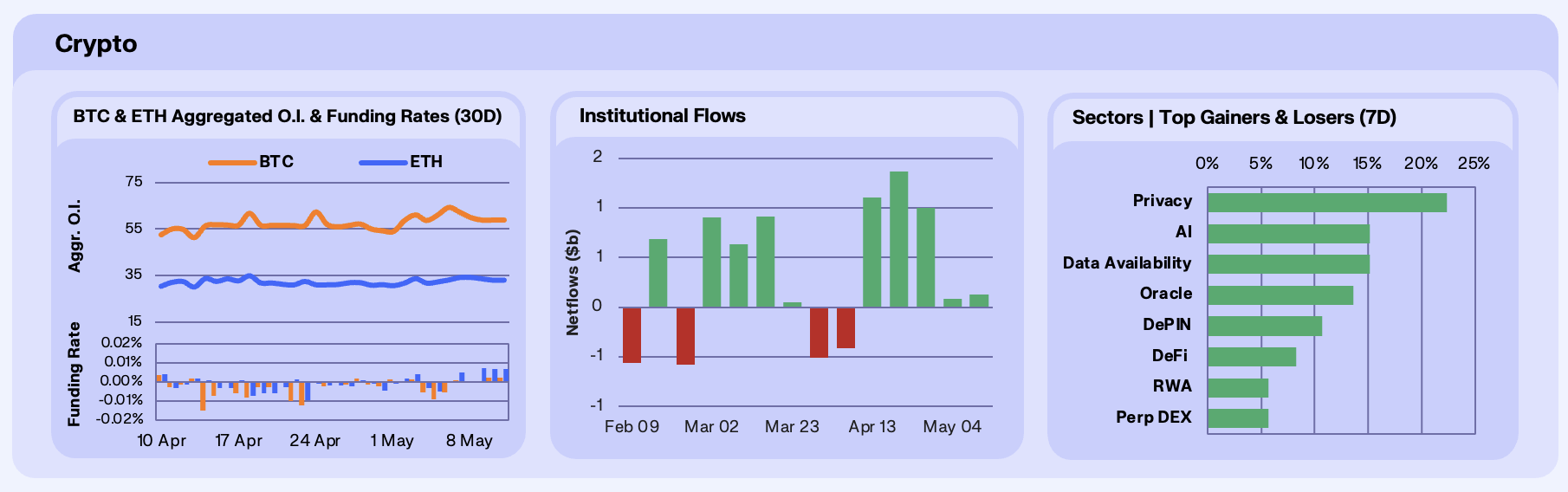

Crypto-related open interest closed effectively flat on the week but the print disguises a third consecutive spike-and-unwind cycle. BTC OI gained +0.34% WoW to $58.83B while ETH showed more sustained conviction at +4.01% to $32.96B. The intra-week shape repeated the now-familiar pattern whereby BTC OI built +$5.54B over Monday and Tuesday to peak at $64.17B as price cleared $82k on the back of the CLARITY Act compromise, then bled -$5.37B through Friday to settle within $200M of where it started. This is the third $5B+ OI spike in five weeks that has fully unwound, and the resting level of $58-59B has held as a floor since mid-April. ETH deviated from the BTC playbook, continuing to build through Thursday’s $34.13B peak before giving back only $1.17B into the weekend, suggesting stickier positioning. BTC funding posted -0.0089% on Monday, the most negative print in two weeks, before flipping positive on Wednesday and holding through Sunday. ETH funding firmed more decisively, reaching +0.0075% on Friday and sustaining through the weekend. After weeks of negative-leaning prints that each of our market commentary flagged as building squeeze potential, this is the first sustained multi-day positive regime on both assets since mid-April.

Institutional flows decelerated for a second consecutive week. Bitcoin ETFs recorded +$192.1M, Ethereum -$81.6M, Solana +$11.1M, and Ripple +$3.0M, for a combined +$124.6M. The three-week surge from mid-April that totalled $3.46B at a $1.15B weekly run rate has given way to two weeks combining for $205.6M, a 91% run-rate decline. ETH’s outflow breaks the positive streak that held across the prior four weeks. The total is the third-weakest positive week in 2026, sitting just above last week’s $81M and the $53M from late March. The divergence from the positioning signal is the week’s key tension, in which funding has flipped structurally positive and the OI floor continues to hold, but institutional capital is not following. The Senate Banking Committee’s CLARITY Act markup on May 14th, which follows the stablecoin yield compromise that removed the bill’s final legislative deadlock, is the nearest catalyst that could re-engage the institutional bid.

Sector performance was uniformly positive with privacy again dominant. Privacy led for the third consecutive week and fourth time in the last five at +22.4%, driven by ZEC surging to $600 on Grayscale’s spot ZEC ETF filing and shielded supply holding at 30% of circulating, while XMR rallied on the May 6th FCMP++ beta stressnet launch with the Trail of Bits audit commencing May 11th. AI printed +15.2%, extending the momentum from the late-April TAO and Bitwise spot ETF filings, matched identically by Data Availability at +15.2%.

Our Take: The funding flip is the signal that our prior commentaries spent weeks watching for. But the repricing is arriving in a form we did not anticipate, with the leverage complex normalising while institutional flows have downshifted to their weakest two-week stretch since late March. The two-legged support of leverage plus allocator capital that characterised the mid-April $3.46B institutional surge is currently running on one leg. The CLARITY Act markup on May 14 is the proximate test. If the Senate Banking Committee advances the bill, it would be the first major crypto market structure legislation to clear committee, the kind of regulatory event that historically re-engages the institutional bid. Combined with a funding regime that has structurally shifted, that setup would be the cleanest forward-looking case for sustained positioning we have seen this year. Our bias is the funding normalisation is durable, but the institutional leg needs the May 14th catalyst to confirm.

Hyperliquid Pulls In Flows

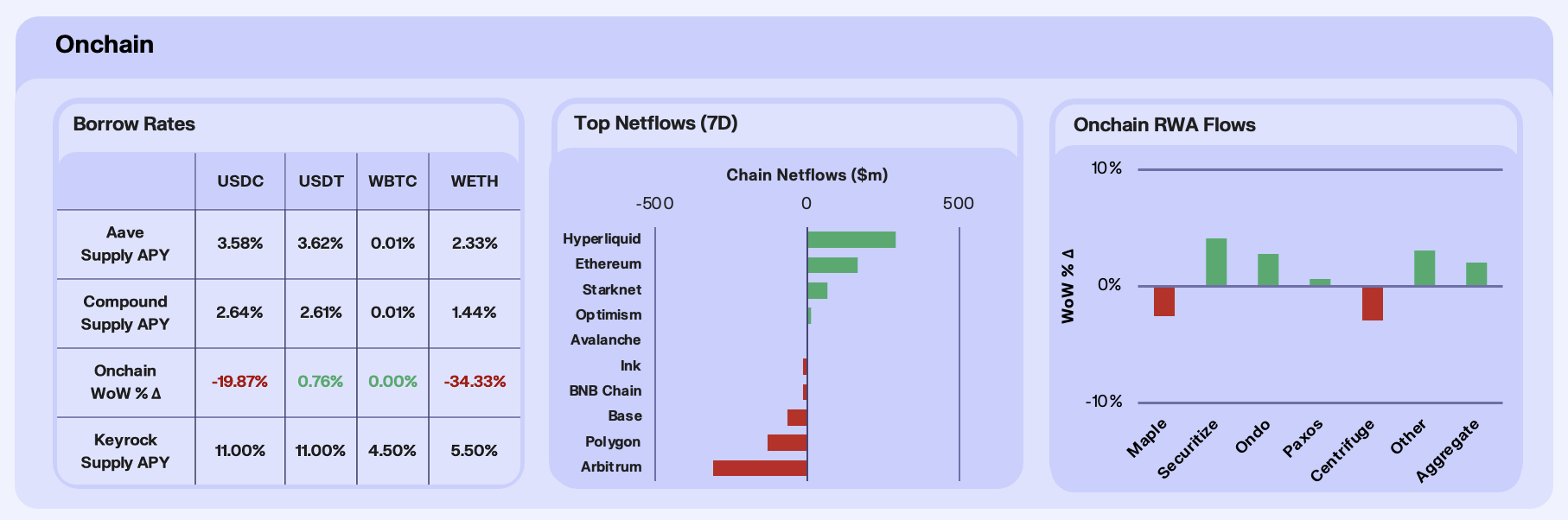

Stablecoin lending rates on Aave pulled back from last week’s post-exploit highs as deposits returned. USDT supply APY eased to 3.62% and USDC to 3.58%, while Compound held steady, confirming the 2% floor remains intact. The rate decline was supply-driven, where we saw Aave deposits rise +17.06% for USDC and +9.85% for USDT as confidence rebuilt post-KelpDAO.

Hyperliquid reasserted dominance at +$293.9M in net inflows, nearly tripling last week’s +$115.2M as HIP-4 prediction markets gained traction after launch. The zero-fee event contract platform hit a record $6.2M notional volume on opening day, accumulated $59M by May 9th, and pulled over 5,300 unique traders, outpacing Polymarket equivalents in several segments. Ethereum posted +$168.3M, driven by the Pectra hard fork boosting L1 staking activity and sustained spot ETH ETF inflows through the week. On the outflow side, Arbitrum recorded -$309.4M, the week’s largest, as KelpDAO exploit fallout escalated and the DAO voted on May 8th to approve release of 30K+ frozen ETH to Aave against an active US court restraining order and competing claims from North Korea-linked creditors, creating a governance-versus-legal uncertainty that triggered risk-off capital rotation. Polygon PoS shed -$101M despite a technical upgrade lifting TPS by 14%, insufficient to counter the liquidity shift toward Hyperliquid and post-Pectra Ethereum.

RWA AUM rose +2.02% WoW in aggregate, a second consecutive week of growth following the post-exploit dip. Securitize led at +4.13% on back-to-back milestones of FINRA approval to custody tokenised securities and enable atomic stablecoin settlement, the first broker-dealer cleared for the full stack. This was followed by the launch of regulated onchain secondary trading for tokenised equities with Jump Trading and Jupiter on Solana, with BlackRock’s BUIDL posting +7.05% on the week as a direct beneficiary. Ondo gained +2.80% after executing the first near-real-time cross-border redemption of OUSG in partnership with JPMorgan’s Kinexys, Mastercard, and Ripple on the XRP Ledger, with settlement completing in under 5 seconds. On the downside, Centrifuge fell -2.90% as a Coinbase partnership naming it the preferred tokenisation infrastructure for Base couldn’t offset a -8.00% drop in its flagship JTRSY product, while Maple declined -2.56% with product-level divergence suggesting reallocation across credit pools.

Our Take: Last week we asked whether prediction market volumes would cannibalise perp activity or expand the total addressable market. The first week of data answers clearly, suggesting additive demand, and the capital rotation numbers confirm the market is pricing this as a TAM expansion. The WETH recovery is another signal worth watching. Our bias remains that capital is concentrating around specificity, Hyperliquid for derivatives and prediction markets, Ethereum for post-Pectra staking infrastructure, Securitize and Ondo for institutional RWA rails, and the generalised L2 playbook continues to lose.

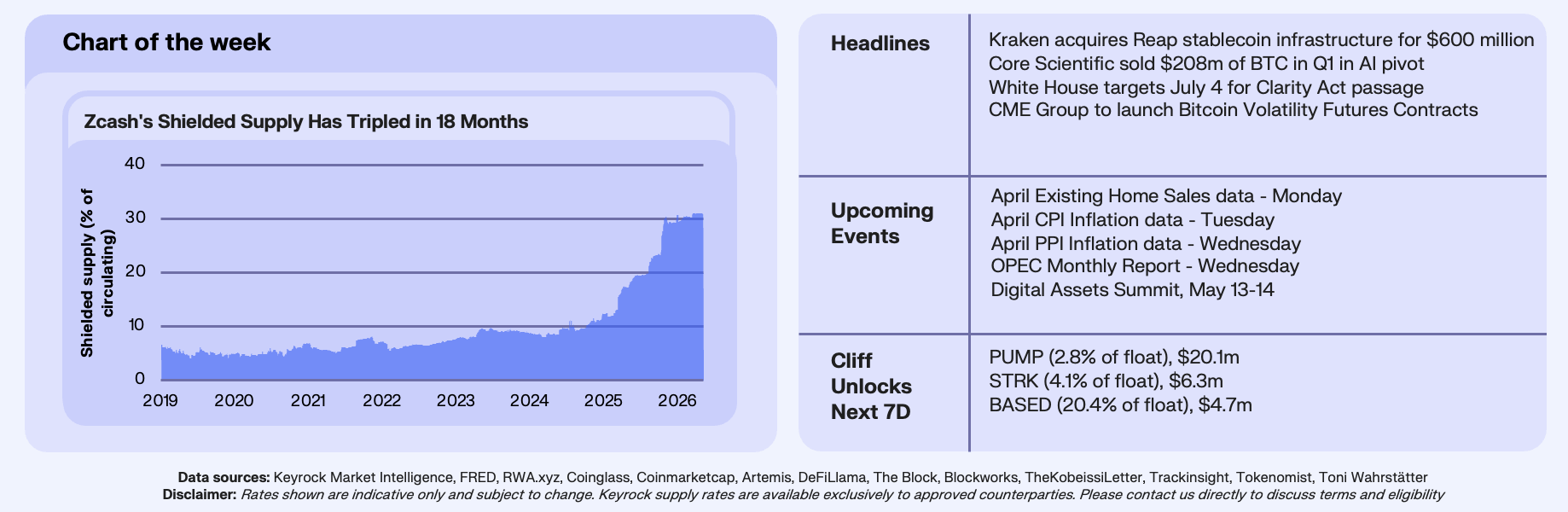

Privacy Capital Is Growing

This week’s chart tracks the percentage of Zcash’s circulating supply held in shielded pools. Shielded supply now sits at 30.83% as of 7 May 2026, up from ~11% in November 2024 and the 5-10% range that held for most of 2019 through 2023. About 5.15 million of the 16.7 million ZEC in circulation is currently locked in shielded form. The metric has nearly tripled in 18 months.

Privacy was the original cypherpunk thesis in crypto, and the period from August 2022 forward was its suppressed era. The Tornado Cash sanctions made the entire mixer category off-limits to compliant capital, chain-analytics firms turned de-anonymisation of Bitcoin and Ethereum into a category-defining business, and “privacy coin” became a label institutional investors avoided. The chart is the cleanest sign that the consensus quietly reversed. Roughly $2.9 billion of ZEC at current prices has migrated to shielded form, alongside Monero’s FCMP++ stressnet beta on 6 May that tested expanding the anonymity set from a ring of 16 to the full chain. Privacy primitives at the protocol layer have followed, with Railgun and Privacy Pools building usage on Ethereum and Aztec rolling out a privacy-first L2. The category has reframed from regulatory liability to portfolio insurance, with named disclosures from Multicoin Capital and endorsements from Naval Ravikant validating the trade for allocators who previously could not touch it.

The macro backdrop is what gave the reframe its weight. Travel Rule enforcement on crypto-asset service providers has tightened the surveillance perimeter on transparent ledgers, CBDC pilots in the EU and Asia have moved from theoretical to staged rollout, and chain-analytics has progressed to the point that any transparent transaction is treated as public information. Bitcoin’s institutional adoption arc, with sovereign buyers and ETF wrappers absorbing supply, has paradoxically eroded its privacy attribute. The thesis emerging from this configuration is that Bitcoin protects against fiat debasement and the privacy-asset complex protects against the transparency BTC has assumed in becoming a strategic reserve. ZEC’s selective-disclosure design makes it the cleanest privacy asset for a regulated balance sheet, since the same chain accommodates both audit-on-demand and full opacity at the holder’s choice.

Our Take: The privacy bid is early in its institutional cycle. ZEC’s compliance optionality is the gateway, with viewing keys allowing audit-on-demand without forced disclosure. Monero retains the cleaner technical purity but is harder to access through KYC’d venues. We’d own ZEC as the institutional expression of the privacy thesis through the EU AMLR effective date of 1 July 2027, with the wider privacy stack at the protocol layer (Aztec, Privacy Pools, Railgun) as the second derivative if mainstream privacy infrastructure scales beyond pure-asset venues.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.