22 June 2026

Key Insights: The Narrow Bid

The Narrow Bid

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

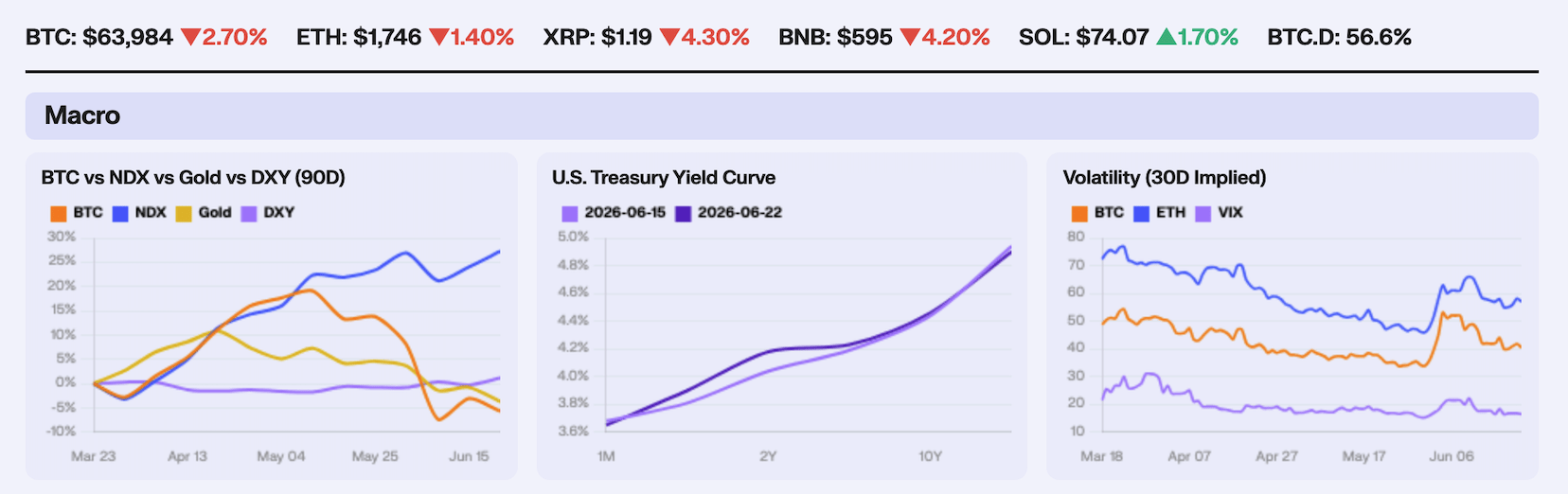

A hawkish Federal Reserve split the cross-asset tape, with the Nasdaq up 2.60% on resilient growth data while Bitcoin fell 2.70%, gold dropped 3.00%, and the dollar gained 1.42% on the DXY. The divergence is the story here, as risk equities powered through a higher-for-longer Fed while the macro hedges, gold and Bitcoin, took the hit from a firmer dollar and rising real yields. The risk-on tone had a poster child in SpaceX, whose record $75b listing on 12 June, the largest IPO in history, debuted at a roughly $1.77t valuation, popped ~19% on day one and has since pushed to a market cap above $2.3t. That is selective appetite for AI and tech, not a broad risk bid, and it ran in parallel with crypto bleeding out. Falling oil did much of the rest, with Brent down roughly -8% on the week toward $80 as the US-Iran ceasefire reopened the Strait of Hormuz, unwinding the geopolitical premium that had carried crude near $98-109 earlier in 2026, though the relief proved fragile as Iran moved to halt Strait traffic again over the weekend and Brent bounced back above $78 on Monday. Strong May retail sales at +0.9% against a +0.5% consensus underwrote the equity bid even as rate cut hopes evaporated.

The week’s decisive event was the FOMC on 17 Jun, where the Fed held at 3.50-3.75% on a 12-0 vote but let the dot plot leapfrog consensus. The median 2026 projection rose to 3.8% from 3.4% in March, now implying at least one hike this year, with 9 of 18 officials pencilling one in and the 2026 PCE forecast lifted to 3.6% headline and 3.3% core. It was Kevin Warsh’s first meeting as Chair, and he stripped the statement to roughly 130 words, dropped forward guidance and declined to submit a dot. The front end repriced hard, with the 2Y yield jumping +14bp while the 30Y slipped -4bp, a textbook bear flattening as the market priced higher-for-longer into the short end. CPI at +4.2% YoY the prior week gave the turn its cover.

Volatility told the opposite story, with the VIX jumping to 18.44 on FOMC day, around 12% higher, before fading to the mid-16s by Friday as the Fed decision passed and the Iran ceasefire briefly held. Crypto vol was crushed harder, with Bitcoin 30-day implied (DVOL) down to 41.8 by 21 June and Ether 30-day at 58.2, a rich 1.4x premium to Bitcoin. Treasury vol echoed it, the MOVE index in the high 60s near a one-year low despite the hawkish dots. The tension sits in the 26 Jun quarterly expiry, roughly $10.6b of Bitcoin notional, around 80% out-of-the-money, with max pain at $74k well above spot and a put/call near 0.87.

Our Take: The market is pricing calm into the exact moment the Fed flipped to a hike bias. Implied vol across equities, rates and crypto compressed to the lows just as the 2Y repriced +14bp and the market penned in a 2026 hike, and one of those two signals is wrong. We lean toward vol being too cheap. The pivot is next week’s May core PCE, the Fed’s marquee input, currently projected at 3.3%. An in line or hot print validates the hawkish dots, should push the front end higher again, and unwind the vol compression straight into a lopsided $10.6b Bitcoin expiry on 26 Jun that sits 80% OTM.

Controlled Deleverage

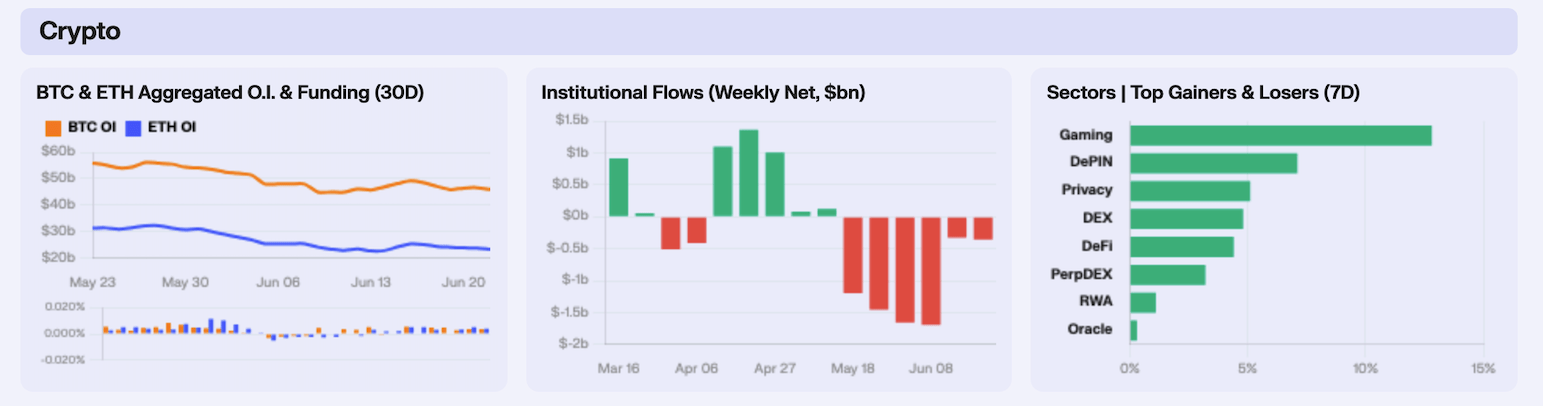

Crypto deleveraged in orderly fashion through the FOMC, with Bitcoin open interest peaking at $49.2B on 16 Jun, the day after the SpaceX-led risk-on, then bleeding lower for three sessions to a $45.9B trough on 19 Jun before a partial rebuild left it near $46B by Monday, down -6.5% on the week. Ether open interest ran the same path, topping out at $25.5B on 16 Jun and sliding -7.8% to roughly $23.5B. The unwind was a position cut rather than a liquidation cascade, and funding confirmed it, holding modestly positive on both assets through the week with only synchronised negative flushes around 15 Jun, before reverting within a session. Ether funding sat consistently richer than Bitcoin’s throughout. Longs kept control without ever running hot, the tell of a market trimming risk into the 26 Jun expiry.

Spot Bitcoin ETFs bled -$340m on the week, the damage back-loaded into a -$113m outflow on 19 Jun, the largest single day, while spot Ether ETFs shed -$35m despite a +$22.5m Monday inflow. Against that, the altcoin wrappers took money in, with spot Solana ETFs adding +$7.1m and spot XRP ETFs +$10.7m, the latter led by a +$5.3m print on 16 Jun. The direction is unambiguous, capital leaving Bitcoin and Ether and trickling into Solana and XRP, but the magnitude is not. The +$18m into the two altcoin products is barely a twentieth of the -$375m that left Bitcoin and Ether. This is rotation in sign, not in size, and it lands on the same conclusion as the spot tape, that the institutional bid stays Bitcoin-first even when Bitcoin is the asset being sold.

The sector board flattered the week, its green across every basket sitting at odds with a tape that saw Bitcoin fall -2.7% and the large-cap alts drop harder, with XRP -4.3%, BNB -4.2% and Dogecoin -6.5%, so the real moves were narrow and narrative-driven rather than broad. The cleanest was DePIN, where a 12 Jun US export-control order forcing Anthropic to cut foreign access to its frontier models reframed decentralised compute as censorship-resistant and sent Bittensor’s TAO up 30% intraday before it settled +16% on the week, dragging Render, Akash and io.net with it. Privacy was the other genuine mover, led by Zcash recovering +9.5% after its Orchard shielded-pool flaw was patched with no sign of exploitation. Elsewhere the strength was single-name rather than sectoral, with Aerodrome up 30% on its Dromos “Predictive Allocation” launch and buyback, and Ethena up 26% on a plan to route $250m into Securitize’s tokenised CLO fund.

Our Take: This week’s green pockets share a tell, each running on its own idiosyncratic catalyst, none on broad inflows. That is a market where the only alpha is narrative-specific and the beta is negative.The nearer pivot is the 26 Jun expiry, $10.6b of Bitcoin notional and 80% out-of-the-money with max pain at $74k far above a ~$64k spot, so the magnet is unlikely to bite. The open-interest rebuild and funding in the days after settlement, not this week’s heatmap, is where the next directional signal shows up.

The Cap Unlock

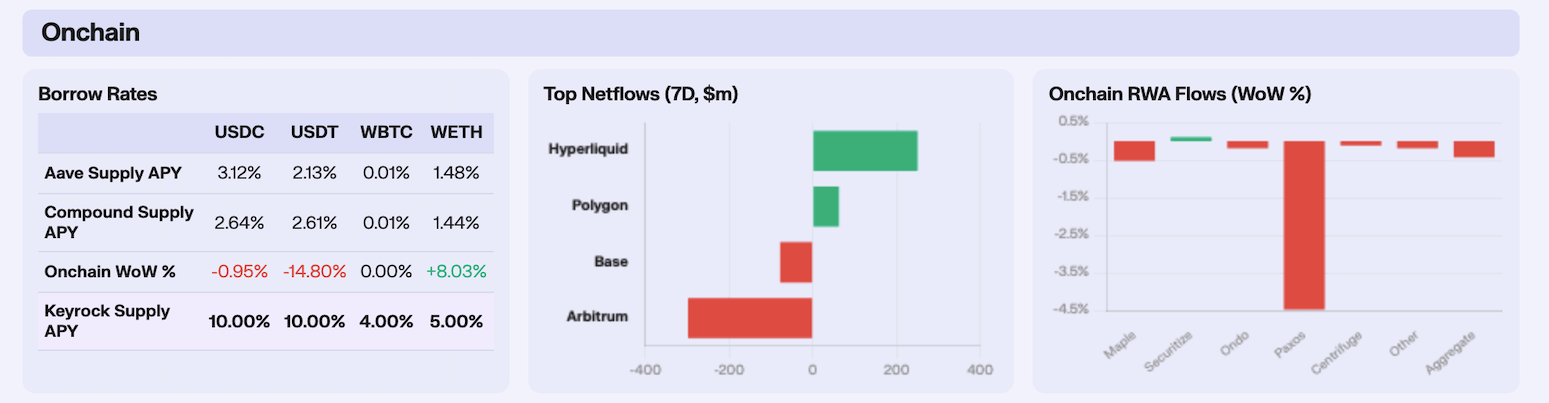

Onchain lending mirrored the deleveraging seen across the rest of the market, though the biggest move came with a mechanical asterisk. USDT supply on Aave jumped +46.47% over the week, while its supply rate fell -14.80%. The driver was not a sudden flight to safety but a supply-cap unlock, with USDT pinned at 97% utilisation against its ceiling, Aave’s Risk Stewards raised the V3 cap on 16 Jun, releasing queued spot deposits that promptly compressed the rate. USDC told a milder version of the same story, supply up +5.37% and its rate easing -0.95%. WETH ran the other way, with deposits down -14.13% and the supply rate rising +8.03%, the signature of ETH being pulled from the pool as the hawkish FOMC unwound leveraged longs.

Chain-level flows captured the same rotation, with capital draining out of general-purpose L2s and into Hyperliquid, with Hyperliquid pulling in +$250m on the week. The mirror image showed up on Arbitrum, which shed -$297.9m, the largest outflow of any chain, with Base losing -$77.8m and Polygon the lone large gainer at +$62.1m. The Arbitrum move is mechanically tied to Hyperliquid rather than coincidental, since Hyperliquid’s deposit bridge lives on Arbitrum One and consumes native Arbitrum USDC, so every dollar bridged into the venue leaves Arbitrum first. Beyond that link none of the L2 outflows carried a discrete catalyst, marking them as rotation rather than distress.

Tokenised real-world assets held roughly flat, the only notable decliner the commodities bucket, down -4.47%, as Paxos Gold tracked the week’s softer gold price. The growth, as it has all year, sat in tokenised credit. Securitize extended its STAC structured-credit fund to Solana with a $250m allocation from Ethena, while Janus Henderson’s tokenised AAA CLO strategy kept building on Centrifuge. Destructive risk stayed mercifully quiet, the week’s two exploits, a $2.15m drain on a deprecated Aztec bridge and a $4.67m infinite-mint on the Axelar-to-Secret bridge, both hitting legacy code and neither moving markets.

Our Take: Onchain said the same thing three ways, that capital is concentrating, not expanding. The only growing pockets were the ones with a specific draw. That is the deleveraging tape rendered in plumbing, and it rhymes with the Bitcoin-first ETF flows and the narrative-only sector bid from earlier in the letter.

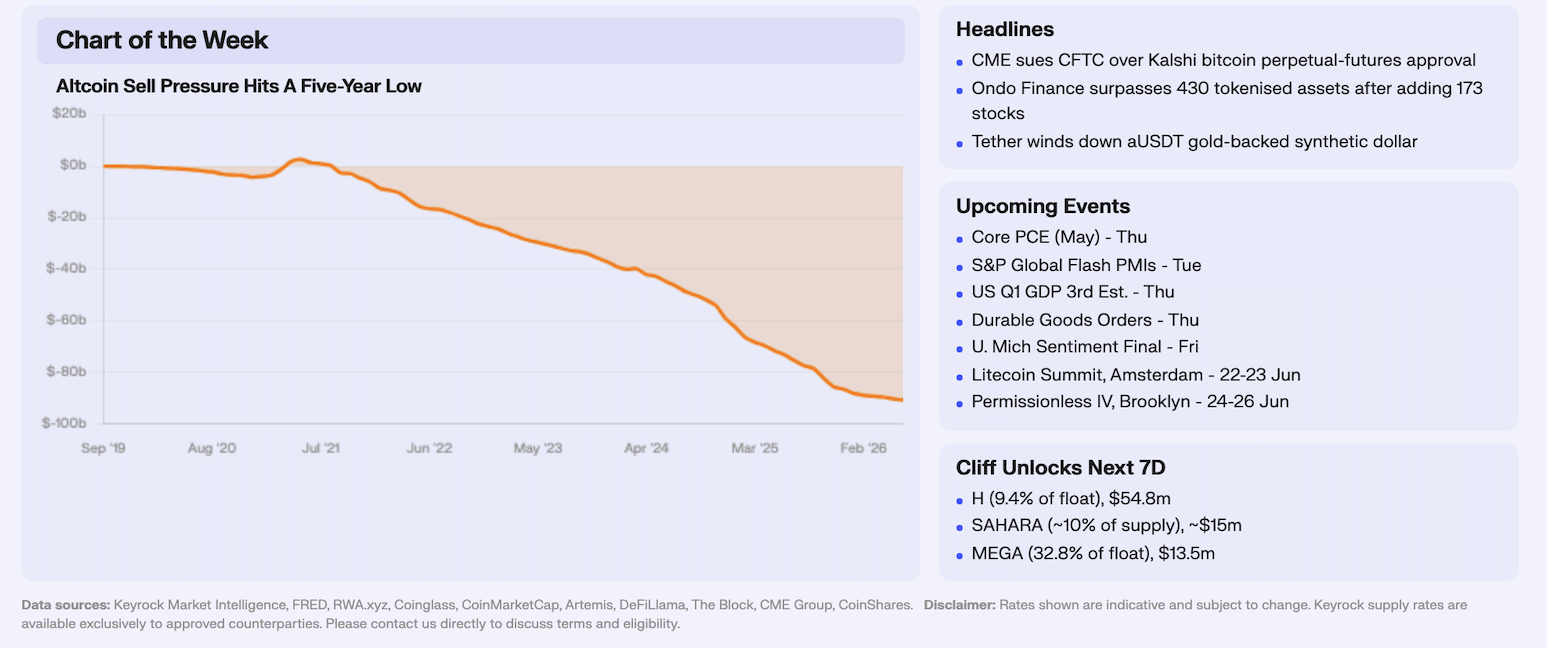

Altcoin Sell Pressure

The week’s chart measures whether altcoins are being net bought or net sold on Binance, tallied across the whole market every day since 2019. When the line falls, sellers are hitting the bid harder than buyers are lifting the offer, and the deeper it goes the longer that net selling has run. It is now at its most negative in five years. We took every one of the 437 live Binance USDT altcoin pairs, stripped out Bitcoin, Ether, stablecoins and the wrapped, staked and leveraged tokens, and summed the running gap between aggressive buying and aggressive selling. It is Binance-only, so treat the dollar level as indicative and read the direction and the turning points. The line printed -$90.66B on 18 June, down a further -$142M WoW and -$18.04B over the year from -$72.62B last June. The only stretch it spent above zero was the +$3.3B peak in May 2021, the blow-off top of the last altseason, every print since has been lower. As one analyst put it this week, “this is not a dip. It’s 15 months of continuous net selling on spot exchanges.”

This is a rotation trade, in which we see the spot altcoin bid dying while speculation moves to derivatives. On 16 Jun, altcoins were 51% of Binance futures volume against 28.85% for Bitcoin and 20.20% for Ether, so the appetite to trade alts is alive, however the appetite to accumulate them on spot is gone. The clearest tell is the divergence through 2023 to 2025, where we see across the whole Bitcoin advance from cycle lows to six figures, this line never turned, instead it accelerated downward. Alts never caught the institutional bid that carried Bitcoin to roughly $105k, because the ETF wrapper, the treasury-company bid and the regulated futures complex are all Bitcoin-first, now Ether-first. Note, the Binance spot lens is narrowing as flow leaves it, with DEX spot share up to ~13.6%, Binance’s own altcoin share roughly halved to under 40%, perp DEXs clearing $1T+ a month, and real off-exchange demand the chart cannot see, like altcoin treasury companies such as Hyperliquid Strategies now holding 27.8M HYPE. Some of the drop is migration, but spot accumulation has dropped materially.

Bitcoin dominance sits at ~56.6%, structurally elevated and as high as 60.66% in May, the ETH/BTC ratio is at a 10-month low below its 200-week moving average, and the Altcoin Season Index reads 52, which it labels “No Altcoin Season”. As Ben Cowen put it in May, “capital is not rotating into higher-risk assets, but instead consolidating into Bitcoin or moving to the sidelines.” Our desk states that almost as important as this is what has not happened. Bitcoin’s slide from ~$104,887 a year ago to ~$64,196 now has produced no mean reversion here at all, the signal that the selling is secular rather than tactical de-risking. Back in 2021 the line went positive only at the euphoric top, then spent three years handing it all back. There is no euphoria left to give back this time. A market this one-sided is also the setup for a violent short-covering snap if a real catalyst lands, because positioning and the natural bid are already washed out.

Our Take: This is the cleanest single read on whether altseason is real, and the signal lives in the slope, not the level. The live test is the ETF wrappers, and so far the data leans our way. Bitcoin and Ether ETFs bled ~$2.7B over two weeks while the spot Solana (~$1.1B AUM) and XRP (~$1.0B AUM) funds drew inflows, but combined that is barely 2% of Bitcoin ETF AUM. This is narrow intra-crypto rotation, not a broad bid, however much the optimists want an “Alt ETF Summer.” So watch the first derivative and ignore the headline rallies until the flow confirms them. The first up-week off this low, ideally one the Solana and XRP ETFs actually drive, is the only data point that matters.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.