4 May 2026

Key Insights: The Last Dance

The Long Goodbye

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

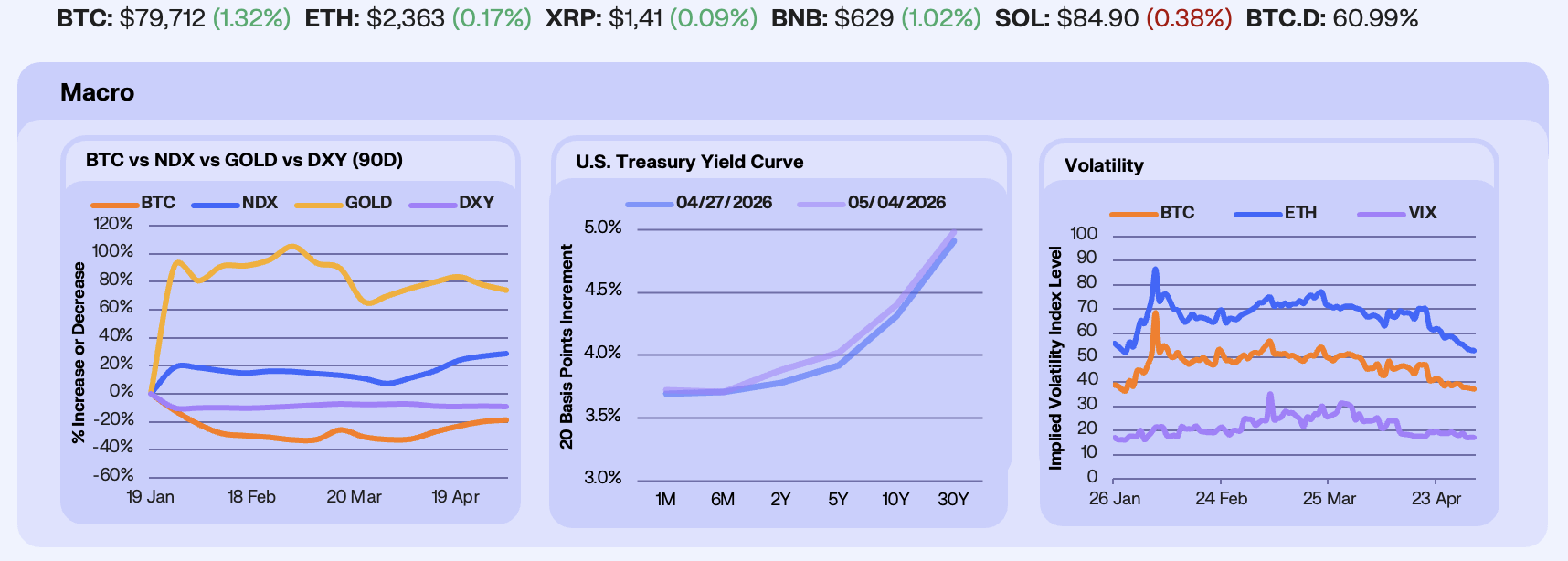

A dense data and earnings calendar resolved with risk holding while hard-money assets sold. The Fed held Wednesday at 3.50-3.75% on an 8-4 vote, the most dissents since 1992, in Powell’s last meeting before his May 15 chair expiry. After the close, Alphabet, Amazon, Meta, and Microsoft delivered prints that confirmed a multi-year AI capex cycle, with Google Cloud’s contracted backlog doubling to $460B, AWS at +28% YoY, and Meta raising 2026 capex to $125-145B. NDX added +1.5% to 27,710 and BTC rose +1.5% to $79,820 as the capex confirmation boosted risk assets. Gold dropped -2.2% to $4,584 as Thursday’s hot March PCE pushed the rate-cut path further out. DXY slipped -0.3% to 98.2, with the political backdrop offsetting the hawkish committee.

Treasury yields sold off across the belly and long end with the front anchored as Thursday’s data did the repricing. March PCE printed +0.7% MoM and 3.5% YoY headline, with energy goods and services up +11.6% as Iran war pass-through worked through, while core landed at +0.3% MoM and 3.2% YoY. Q1 GDP advance came in at +2.0% annualized, below the 2.2% consensus but firmly off the recession line. With Treasury borrowing estimates Monday and refunding statement Wednesday already pricing into long-end supply, and the effective tariff rate at 11%, the highest since 1943, the market has stopped expecting Fed cuts or hikes to move rates, and is pricing the long end higher on supply and inflation reasons instead.

Volatility compressed across the board with the bleed extending through the weekend. VIX fell -9.19% to 16.99, BTC 30-day ATM IV declined -5.78% to 37.20, and ETH IV dropped -9.83% to 53.10. The BTC term structure sits in normal contango, with the very front (2MAY-8MAY expiries) at 23-29 IV reflecting the post-FOMC drain, then 15MAY at 36, 29MAY at 37, and 26JUN at 38. OI is heavily concentrated at the 26JUN expiry with 111,707 BTC versus only 9,479 at 15MAY, leaving the June 16-17 FOMC as the dominant macro tail in options pricing rather than the May 15 chair transition.

Our Take: The cleanest read of the week sits in the divergence between the long bond and hard-money assets. The 30Y selling to 4.98% with PCE at 3.5% headline and the effective tariff rate at 11%, the highest since 1943, says inflation is sticky and term premium is rebuilding. That tension resolves the other way in our view. Hyperscaler capex aggregating to $725B across MSFT, GOOGL, AMZN, and META in 2026 (with ~$450B AI-specific) is the new stimulus channel, working through corporate cash flows rather than the federal budget, and it pulls forward demand on energy, chips, and grid build-out. That keeps the long end pinned higher and the dollar under political pressure into the chair transition. Gold giving back on the rate-cut repricing reads as a calendar move rather than a regime shift, and we’d be looking for the bid to firm into Wednesday’s refunding and the next round of inflation prints.

The Reload

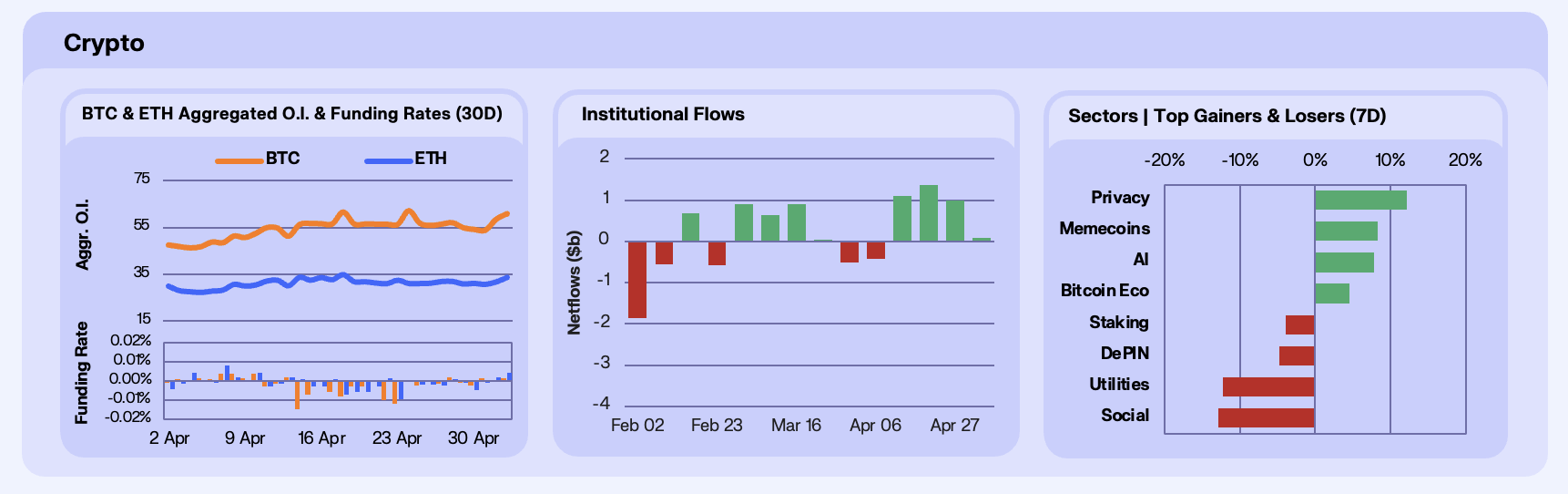

Open interest unwound through the FOMC and rebuilt across the weekend. The intra-week shape was textbook event-driven, with BTC OI peaking at $57.13B Tuesday, falling -$2.13B in a single session on Wednesday’s FOMC outcome, and bleeding through Thursday’s PCE to a $53.96B Friday low. Then Saturday saw a +$4.67B single-day rebuild and Sunday added another +$2.36B, closing the week at $60.99B for a +7.87% WoW gain that fully reversed the FOMC drain. ETH followed the same shape, $30.60B Friday low to $33.62B Sunday close for a +5.52% WoW build. Funding flipped clearly positive into the weekend, the cleanest positive ETH funding print of the week, breaking the negative-leaning regime that has held since mid-March.

The Friday print did the heavy lifting on flows. Bitcoin ETFs absorbed +$629.8M on May 1 alone, the largest single-day inflow of 2026, reversing -$467M of Mon-Thu outflows to leave BTC at +$162.8M weekly net. Ethereum recorded -$82.5M and Solana -$1.2M for a combined +$79M aggregate week, the fourth consecutive week of net BTC inflows but the first below the $700M threshold that the prior three streak weeks each cleared. BTC ETF AUM sits at $87.3B, ETH at $11.5B, and SOL at $132M. The pattern matches the OI rebuild beat for beat, with allocators pausing into the FOMC and PCE prints, then committing harder than they had in any single session this year once the calendar cleared.

Sector dispersion widened with privacy outpacing everything else through the weekend. Privacy led at +7.28% on ZEC +16.5%, with Grayscale’s Zcash Trust volume doubling into April and shielded supply hitting an all-time high of 30% extending the EU AMLR narrative that drove April’s earlier rally. TAO +15.5%, sustained through the weekend after the April 28 spot ETF filings from Grayscale and Bitwise, with AI also flipping to +7.8% on the same TAO and SN0 prints. Memecoins finished +8.3% on DOGE +10.1%, driven by the 21Shares physically-backed DOGE ETP listing on Xetra, the Grayscale DOGE flow flip after nine days of outflows.

Our Take: The OI rebuild and Friday ETF print together are the cleanest reload signal we have had in months. Allocators who paused into the macro calendar came back with the year’s biggest single-day BTC ETF inflow, BTC perp leverage rebuilt $7B in two sessions, and ETH funding flipped positive on Sunday for the first time this week. The market we have now is one that absorbed an 8-4 hawkish dissent, hot PCE, and a 30Y blowout, and still drove every measure of crypto positioning back to the upside by Sunday close. Our bias is the next leg is already underway.

Utilisation Snapback

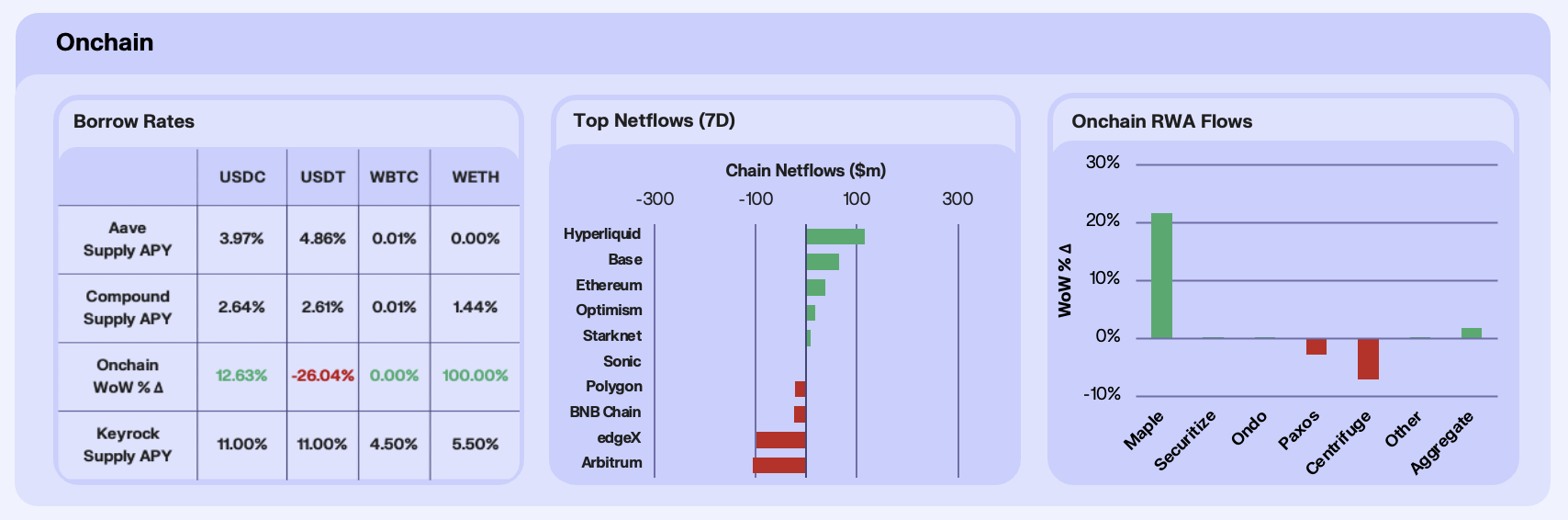

Stablecoin lending rates on Aave continued to rise in the aftermath of the KelpDAO exploit, with USDT supply APY surging to 4.86% and USDC rising to 3.97%. Utilisation nearly doubled for USDT, expanding from 0.095 to 0.166, while USDC climbed from 0.117 to 0.138, confirming that the utilisation snapback we flagged last week is materialising. Compound provided a cleaner read of baseline demand, printing 2.64% on USDC and 2.61% on USDT, both above the 2% floor we’ve tracked since early April. We see a pattern of borrowing demand returning, but selectively, with USDT absorbing the bulk of incremental activity.

Chain-level flows saw Hyperliquid reassert dominance at +$115.2m in net inflows, driven by the mainnet launch of HIP-4 prediction markets on May 2nd. The feature allows anyone to create binary outcome contracts by staking 1M HYPE tokens, with zero open fees, sub-second execution, and native integration into the existing perps platform. Early markets on short-term BTC price targets hit millions in daily volume within hours, outpacing Polymarket and Kalshi equivalents in several segments and representing a material expansion of Hyperliquid’s product beyond perpetuals. Base posted +$64.8m as bridged TVL crossed the $13B milestone, driven by sustained activity in payments, social, and DeFi pools rather than any single catalyst. On the outflow side, Arbitrum continued to bleed at -$106m as KelpDAO exploit fallout persisted, with active governance debate over the fate of the 30,766 frozen ETH now centring on the ‘DeFi United’ recovery effort backed by Aave Labs, LayerZero, Ether.fi, and Compound.

RWA AUM rose +1.78% WoW in aggregate, pulled almost entirely by Maple’s +21.75% surge. The catalyst was SYRUP’s listing on Revolut on April 30th, which exposed Maple’s institutional credit yield products to 70M+ users across the UK and EU and drove fresh inflows into syrupUSDC and syrupUSDT vaults. This week marked a sharp reversal from last week’s -11.19% drawdown when Maple withdrew all liquidity from Aave Mantle in the immediate aftermath of the exploit. Ondo edged up +0.29% after partnering with Broadridge Financial Solutions on April 28th. Centrifuge declined -7.13% on pool-specific redemptions in larger treasury and credit vaults despite expanding its RWA ecosystem onto Monad, while Paxos fell -2.76% as a dip in gold spot prices directly pressured PAXG AUM.

Our Take: Last week we asked whether the utilisation snapback would reprice lending rates higher or simply confirm structural decoupling from onchain credit risk. It seems it’s doing both, but asymmetrically, with USDT utilisation nearly doubling on Aave while USDC and WETH lagged, suggesting the recovery is demand-selective rather than broad-based. Our desk is watching whether prediction market volumes cannibalise perp activity or expand the total addressable market, because if it’s the latter, the capital rotation we’ve tracked for weeks toward specialised venues accelerates from here.

Difficulty Downtrend

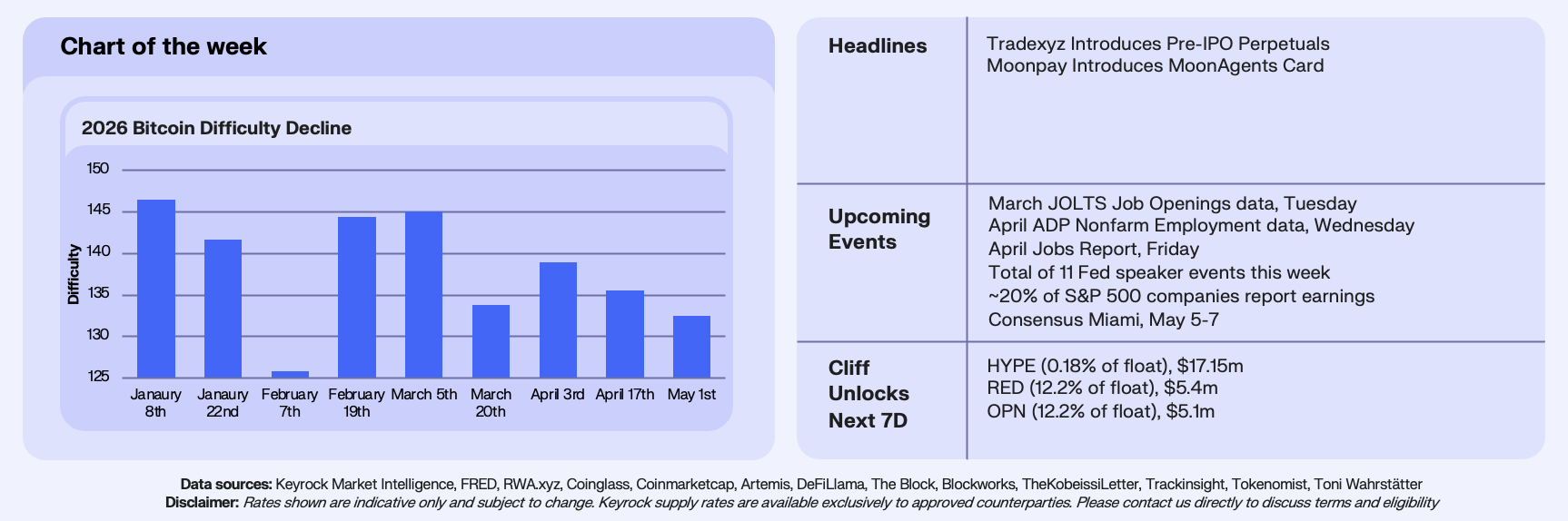

This week’s chart tracks every Bitcoin difficulty adjustment of 2026, totalling nine epochs. Six of the nine have printed negative, producing a cumulative 10.7% decline from the 148.3T level that opened the year to 132.47T today. The May 1st adjustment at block 947,520 fell 2.3%, following April 17’s 2.4% decline, the second consecutive downward revision. It is also the second such streak of the year, following Q1 opening with three straight negatives, including a -11.2% single-epoch plunge in early February, the steepest of 2026. The three positive adjustments that have occurred, including a sharp +14.7% rebound in late February, look increasingly like small, brief recoveries within a broader downtrend. Network hashrate, which hit an all-time high of 1.442 ZH/s in September 2025, briefly touched 899 EH/s at the May 1st adjustment point, down 38% from peak, and currently sits around 1.05 ZH/s.

The cause is a structural exodus of compute from Bitcoin mining into AI infrastructure. Q1 2026 marked the first quarterly hashrate decline in six years, driven by a profitability squeeze that has rendered marginal mining uneconomic. The weighted average production costs among listed miners sit near $80,000-$90,000 per BTC against a spot price of roughly $74,000. Public mining companies responded by liquidating a record 32,000 BTC in Q1, more than they sold in all four quarters of 2025 combined. Marathon dumped 15,133 BTC in March alone, while Bitdeer emptied its entire treasury. The proceeds are funding a wholesale pivot, with over $70 billion in AI and high-performance computing contracts having now been announced across the public mining sector, and CoinShares projects 70% of listed miner revenue will derive from AI by year-end, up from approximately 30% today.

As higher-cost operators exit, difficulty drops, block times normalise toward the ten-minute target, and surviving miners capture a larger share of the block subsidy at lower competitive intensity. Hashprice, i.e. the revenue per unit of deployed hashrate, has already responded, climbing from a February trough of $29/PH/day to $37.52 today, as the same 3.125 BTC block subsidy distributes across fewer machines.

Our Take: What we are watching is a repricing of hashrate as a commodity. Miners are rationally reallocating energy infrastructure toward AI workloads that currently offer superior risk-adjusted returns. CoinShares forecasts a rebound to 1.8 ZH/s by year-end, but that projection is conditional on BTC recovering toward $100,000. If prices hold in the $65,000-$75,000 range, the difficulty regime persists and surviving miners’ margins widen further. The signal we are watching is the next adjustment on May 17th. If it prints positive, it marks the floor for this hashrate cycle. If it doesn’t, the protocol’s self-correcting mechanism has further to run.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.