8 June 2026

Key Insights: The Hawkish Repricing

Hawkish Reset

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

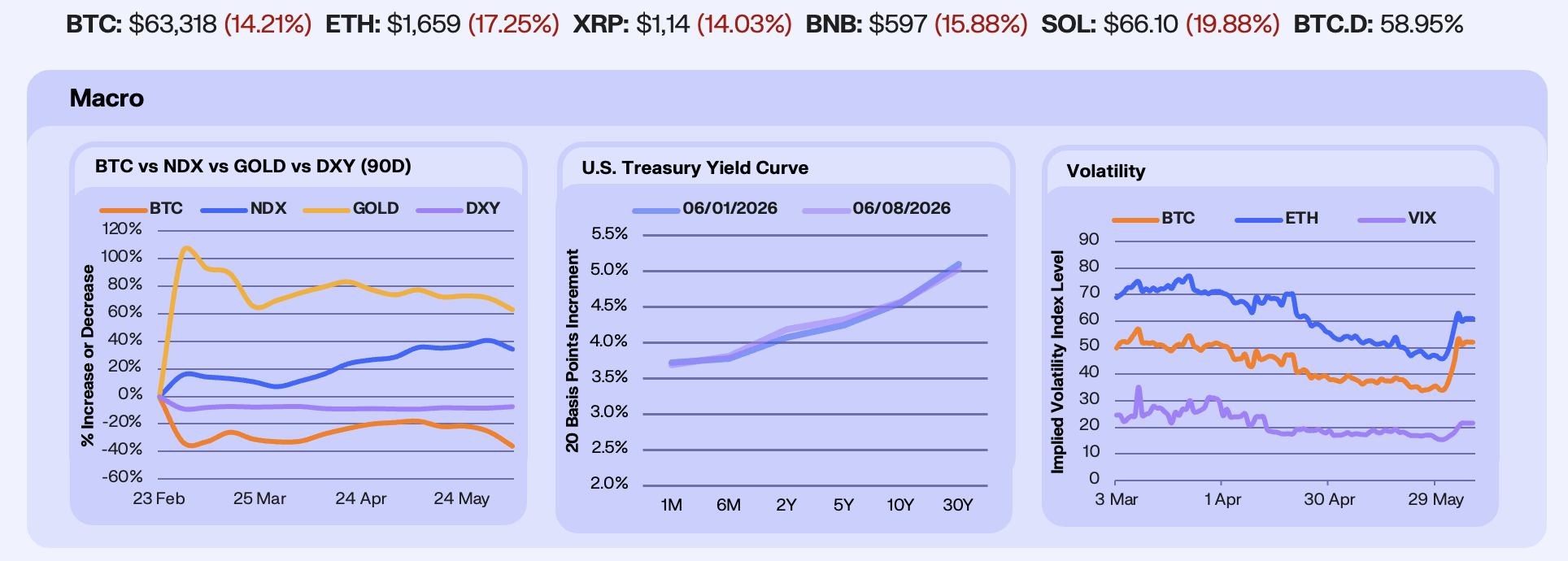

This week we saw a clean risk-off tape on the back of a hawkish data shock. BTC fell 14.20% WoW to $62,882, breaking the $60,000 psychological level intraday on Friday for the first time since late 2024. Meanwhile, the NDX dropped 4.53%, ending a nine-week winning streak. Gold provided no safe-haven bid, falling 4.87%, and the DXY climbed 1.11% to 100.10, taking the haven flow instead. The driver was a blowout May NFP, in which 172K jobs were added against an 80K consensus, with April revised +64K and March +29K. CME FedWatch repriced the probability of at least one rate hike before year-end from 45% the prior week to 67% on Friday’s close. The ‘good news is bad news’ reaction function reasserted itself, and Bitcoin caught the worst of the cross-asset deleveraging.

The bond market did the heavy lifting on the repricing, where we saw the 2Y yield jump 12 bps to 4.20%, the 5Y add 7 bps, the 10Y drift up 1 bp, and the 30Y fall 7 bps. The spread between the 30Y and 2Y Treasury yields compressed 19 bps in a single week, a read our desk sees as a bear flattening signal consistent with hawkish front-end Fed repricing and long-end growth concern. ISM Manufacturing registered 54 on Monday, the highest reading since May 2022, while JOLTS showed 7.6M openings on Tuesday, a sign that demand is still sticky. ADP added 122K versus a 110K consensus on Wednesday, and ISM Services beat at 54.5 against 53.8. Friday’s NFP and the upward back month revisions were the headline, but the curve had already started moving by Tuesday afternoon.

The VIX added 40% WoW to close at 21.51 on Friday, with an intraday high of 21.57. Crypto vol moved harder, however, with BVIV spiking to 53.17 on Thursday, its highest since the 2nd April, before settling in the low 50s on Friday. EVIV surged in parallel as desks bought put protection through the selloff. Friday alone delivered $1.5B in BTC long liquidations as price broke through $60K. Spot BTC ETFs printed a record 13-day outflow streak totalling $4.4B, the first stretch heavy enough to flip 2026 cumulative ETF flows negative. BTC-SPX correlation re-tightened sharply, with cross-asset deleveraging dominating intraday flows.

Our Take: The week stitched a hawkish-Fed-repricing impulse to a deteriorating risk setup, and the two now feed each other. Wednesday’s May CPI is the pivot to watch. A 3.0% headline or hotter and the 2Y has room to extend through 4.30%, the ETF outflow streak likely runs into the 16-17th June FOMC blackout, and Bitcoin trades the $59K support that last held in late 2024. An easing print, however, would reset all three. The dot plot at the SEP meeting is the second test. If 2026 medians shift from one cut to flat or one hike, the dollar gets a second leg and risk takes another draw. Our desk leans short duration into CPI.

Funding Flips Negative

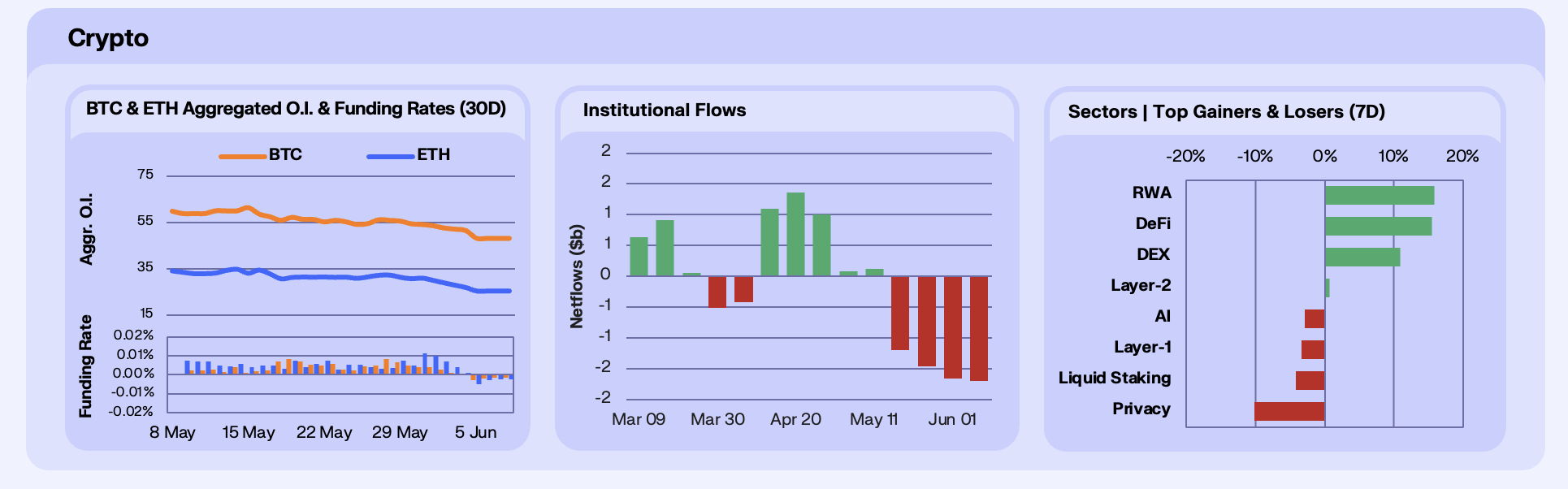

The crypto leverage complex took the brunt of the cross-asset selloff, with BTC futures OI falling roughly 11% WoW. Friday alone saw a near 5% single-day deleveraging as $1.5B in long liquidations cleared through the book. ETH derivatives took it harder, with OI dropping roughly 18%, the sharpest week of unwinds in months. The funding rates inverted during this period, with BTC perpetual funding flipping from a healthy +0.0041% to roughly -0.003% by Friday, and ETH funding moving from +0.0112% to roughly -0.005%. Both inversions were held into the weekend. The pattern is classic forced deleveraging, where longs got flushed, fresh shorts did not aggressively step in, and the residual book is now small enough and short-biased enough that any light macro print into next week could trigger a squeeze.

Spot ETF flows tell the structural side of the same story, where we saw BTC funds drained roughly $1.4B over the week, with Wednesday alone losing $396.6M. The 13-day outflow streak ended Friday with a +$3.05M inflow, but the damage was done. 2026 cumulative spot BTC ETF flows are negative for the first time since launch, with roughly 59,400 BTC liquidated out of the wrappers at depressed prices. ETH ETFs lost $241M for the week and ended their own 17-day outflow streak Friday with a +$19.3M print, entirely from BlackRock’s ETHA. SOL ETFs shed $30M as Bitwise’s BSOL led the redemptions, although the category cleared $1B in cumulative AUM during the week. XRP funds drained $20M, snapping the longest 2026 inflow streak after a record +$118M May. The four together mark the first week of 2026 where every major spot ETF wrapper printed net outflows in tandem.

Despite the majors’ double-digit drawdown, six of eight sectors we track posted positive WoW returns. Memecoins led at +16.5%, AI at +13.2%, DeFi at +9.1%, RWA at +6.4%, Perp DEX at+3.7%, with Layer-2 modestly down at -1.5%. The losers were concentrated in DEXes, as spot venues lost share to their perp counterparts, and Privacy, on regulatory and liquidity weakness. The Perp DEX/DEX gap of nearly 10 percentage points in a single week is the cleanest read of the rotation, where leverage venue tokens outperformed spot venue tokens by an unusually wide margin, consistent with this week’s Hyperliquid HYPE ATH print at $75.52 and the broader thesis that onchain derivatives infrastructure is taking share regardless of price.

Our Take: The pattern this week was selective, with capitulation in majors, and rotation into long-tail narratives. That is constructive on a CPI-cool tape and dangerous on a CPI-hot one, because the same long-tail beta that held up this week gets crushed on a second leg of forced selling. The signal to watch is BTC perpetual funding. If it flips back positive inside the next two sessions, the local bottom is in and the squeeze into CPI is the trade. If it stays negative through Tuesday, deleveraging has further to run and $59K support gets tested.

Yield Refuge

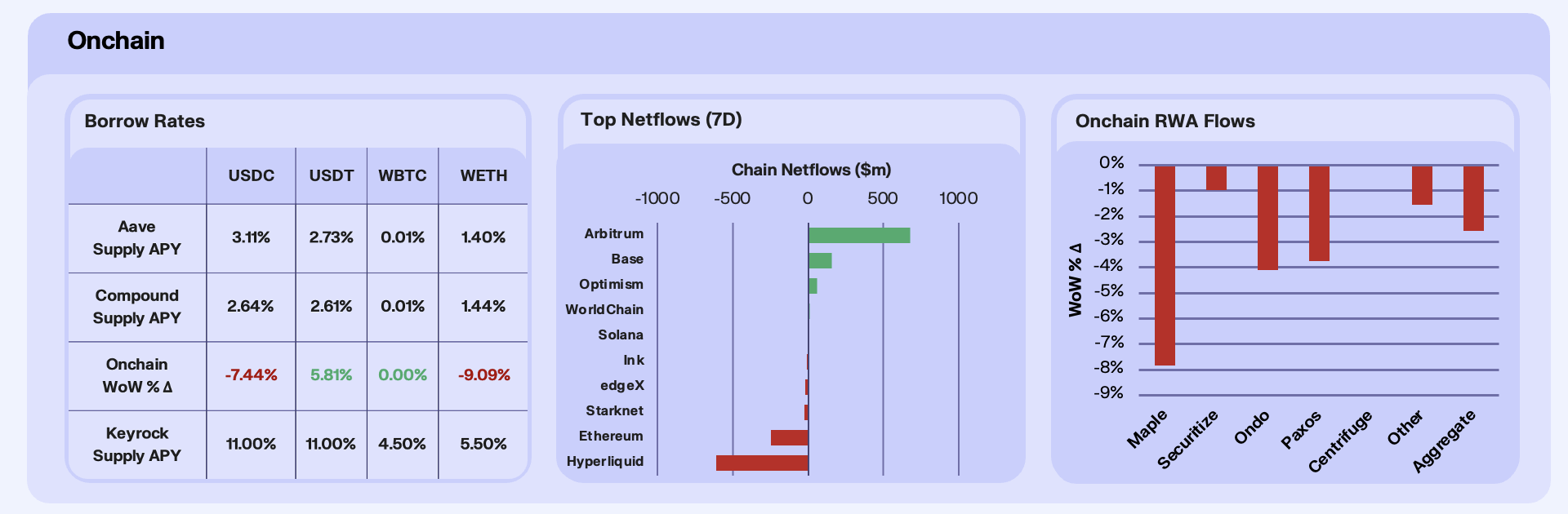

The onchain lending markets printed a deleveraging pattern this week, where we saw WETH supply surge 78.68% WoW, while the supply APY collapsed 37.13%, the cleanest yield-refuge signal of the week. Ethereum bulls are parking inventory for yield, while borrow demand is not keeping up, consistent with the 18% OI drop and the funding flip seen this week. USDC supply grew 28.40% as the rate ticked down 5.90% to 3.37%, classic capital parking on the stable side. USDT told a sharper version where supply was up only 4.31%, but the rate down 20.24%, meaning borrow demand for stables collapsed faster than supply grew.

Chain-level net flows showed a clean rotation, with Arbitrum leading inflows at +$682M on the back of an ongoing DeFi and RWA build, the largest single-week net inflow we have tracked since the early-2026 incentive cycle. Base added +$157M on the Coinbase-funnel default flow, while Hyperliquid was the headline outflow at -$609M, a sharp reversal after last week’s HYPE ATH. Ethereum mainnet bled -$246M as the rotation to L2s accelerated into the volatility. The aggregate read is capital fleeing higher-beta and higher-leverage venues toward DeFi-rich L2 defaults.

RWA AUM fell -2.56% in aggregate, a notable down week for a category that normally trends one-way. Maple was the worst at -7.84%, consistent with redemption demand at the institutional lending end of the stack as macro vol forced reallocations. Every protocol we track was red on the week, with the magnitude clustered tightly around the aggregate. The asymmetry matters, given when leverage flushes in the spot and perps complex, RWA AUM bleeds in sympathy but at a fraction of the magnitude. That makes RWA a softer-beta hold through risk-off environments.

Our Take: The onchain markets confirmed the deleveraging signal. The cleanest forward signal is WETH supply, if it is above $700M on the next print, that would mean Ethereum bulls have not yet finished de-risking and the squeeze into a CPI-cool tape would look to be delayed. Back below $400M within two weeks means leverage is returning to the pool and the squeeze trade is on.

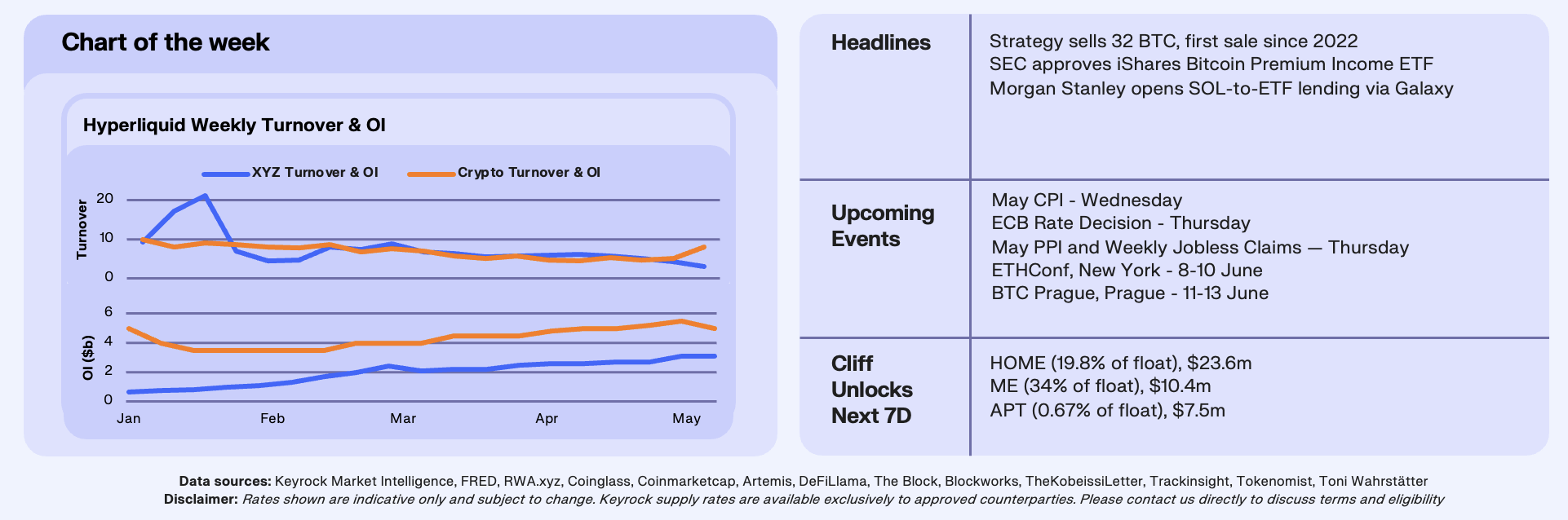

HIP-3 OI Up, Turnover Down

This week’s chart plots weekly turnover, which measures volume divided by open interest, alongside weekly OI for two sides of Hyperliquid. This being the TradeXYZ HIP-3 markets, the dominant deployer at roughly 97% of category volume and OI, against Hyperliquid’s core crypto perp book. This week, TradeXYZ weekly OI printed a fresh ATH at roughly $3.1B, up 50% since late March, while weekly volume collapsed to roughly $9B, down 31% WoW and 57% off its late-March peak of $21B. Implied weekly turnover ran from roughly 9x to roughly 3x over ten weeks. The crypto core book, that being BTC, ETH, SOL and HYPE in aggregate, did the opposite. Volume bounced 43% to roughly $40B as HYPE printed an ATH on the 3rd June. Aggregate OI sat broadly flat near $5.0B, masking a HYPE OI build through the run-up, and turnover snapped back to roughly 8x. The two turnover series sat close through April and most of May inside a 5-8x band, before the gap opened cleanly this week. An onchain equity-perp deployer is now turning over its book at less than half the rate of the crypto perps that built the venue.

Given that TradeXYZ runs roughly 97% of HIP-3 volume and OI, this means we are really analysing one deployer’s portfolio of markets with rounding around it. The read is that two interpretations of the data look the same from outside, the first being that there are position-takers warehousing equity-index exposure onchain, and the second being that the deployer’s market-making book is parked as resting OI to harvest fee rebates. We cannot fully separate them, though what pushes us toward the first reading is the parallel behaviour of the crypto core book this week. OI being flat on a 43% volume jump signals to our desk as a textbook churn tell, the inverse of what TradeXYZ is showing. If the OI build were purely MM inventory, it should scale with TradeXYZ volume, not run counter to it. The mechanism on the position-taker side is straightforward, and we have heard versions of it from desks all year. TradFi-native participants are using onchain equity perps as a synthetic prime-brokerage rail, sizing positions and holding them through the week rather than flipping them intraday.

What matters for derivatives desks is that long-duration positioning changes the economics of liquidity provision. If holding periods on TradeXYZ’s markets are extending on the order of 3x relative to the spring regime, realised vol on the book gets quieter and funding skew gets persistent. The basis between XYZ100, which is TradeXYZ’s Nasdaq 100 product, and listed Nasdaq 100 futures becomes a real basis trade. Hyperliquid took a record 6.63% share of global perp futures volume in May, meaning the venue demands serious attention. If the next HIP-3 deployers (commodities, equity singles, RWA credit) reproduce the same OI-up, turnover-down pattern once they reach scale, onchain equity perps cross from a single market into a category with its own flow signature. If they do not, this week’s pattern is TradeXYZ specific market structure, and the warehouse read collapses back into deployer-MM behaviour. Both outcomes are informative for venue selection and product design.

Our Take: Our desk has a soft preference for the warehouse reading but cannot prove it from outside the venue this week. Watch TradeXYZ OI through the next macro risk-off. If it holds above $2.5B on a 20% equity drawdown, the cohort is real money sizing through volatility, not deployer inventory unwinding on stress. Then watch the next two HIP-3 launches at scale. If commodity or equity-single perps clear $1B OI and post sub-5x weekly turnover inside eight weeks, the warehouse archetype is portable and the basis-vs-CME desk product gets built. Until then this is the first clean structural maturation print on a HIP-3 deployer.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.