20 October 2025

Key Insights: The Golden Standard

The Herd’s Back to Gold

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

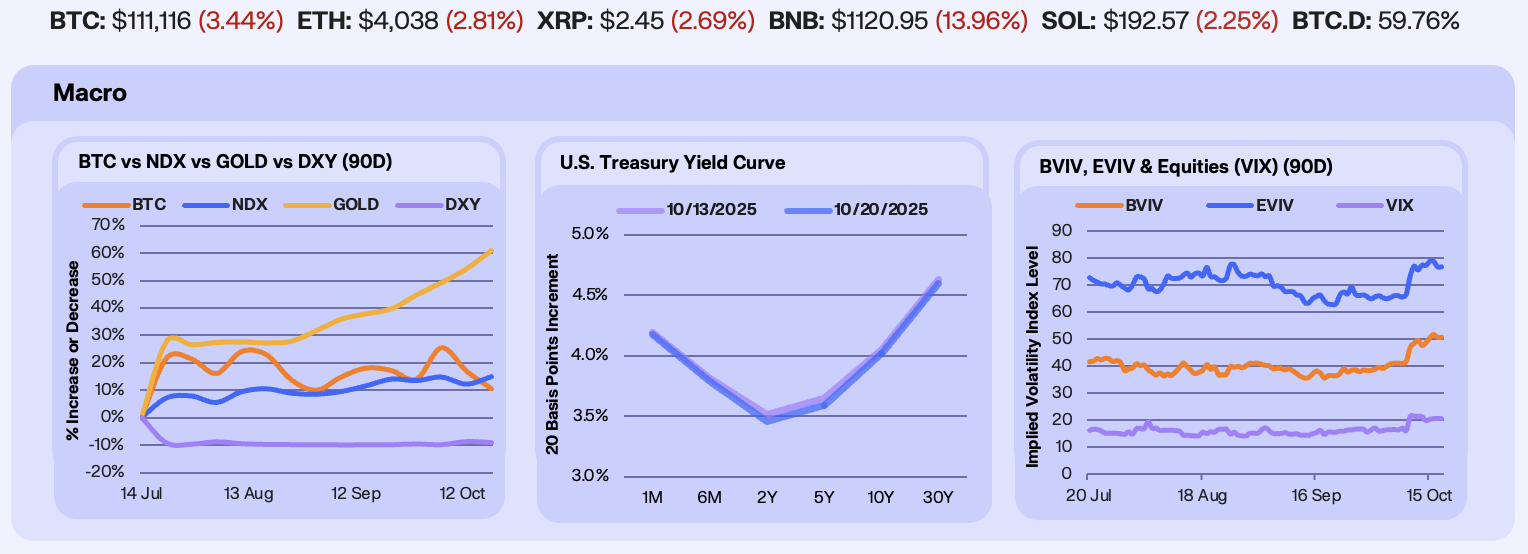

In a week marked by rising fear and fading risk appetite, gold once again stole the spotlight. NDX (+2.5%) rebounded from recent lows, even as the U.S. government remains shutdown and regional banking concerns kept broader risk sentiment fragile. Bitcoin (-5.6%) remains under pressure, with ETF inflows cooling sharply from early-month peaks and sentiment turning cautious. Gold (+4.4%) extended its dominance and marked new all-time highs, with central banks recording a 27-month streak of net purchases, the longest in history, while the DXY (-0.4%) resumed its downtrend amid weaker yield correlations and persistent fiscal uncertainty.

The yield curve shifted lower again this week, led by declines across the 2Y–30Y tenors as investors rushed into Treasuries following Powell’s remarks on a cooling labour market, and mounting stress in regional banks. Losses at Zions and Western Alliance tied to loan fraud and troubled exposures reignited doubts over banks’ private credit positions, driving short-term Treasury yields to three-year lows and deepening Wall Street’s unease. The rush into 10-year Treasuries underscored investors seeking shelter from growing market strain, a sign that stress is building across the financial system. Rate cuts are starting to look less like insurance against risk and more like an attempt to contain it.

That shift in tone reverberated across risk assets, with volatility spiking as investors positioned defensively. Bitcoin IV climbed to ~50, its highest since May, while ETH’s EVIV pushed toward 79, the highest since June. Equity volatility followed suit, with the VIX surging to 28, one of its largest weekly spikes of the year amid the ongoing credit crunch. Investors are hedging broadly across markets as liquidity tightens, reflected in rising repo rates, elevated use of the Fed’s standing repo facility, and widening high-yield spreads. Much like the rush into 10-year Treasuries, these moves suggest that underlying stress is building in the system, even if it’s not yet visible at the index level.

Our Take: The herd’s back to gold, the oldest trade in the book. Last week, bond yields and equities fell together, a rare combination that usually signals a bear market as investors move to protect. Bitcoin’s performance against gold has slipped to multi-year lows and is worth watching. The same pressures driving this rush to safety are exactly what Bitcoin was built to hedge against. Whether it holds or cracks from here will say a lot about how the market still views that promise.

Long Tail Unravels

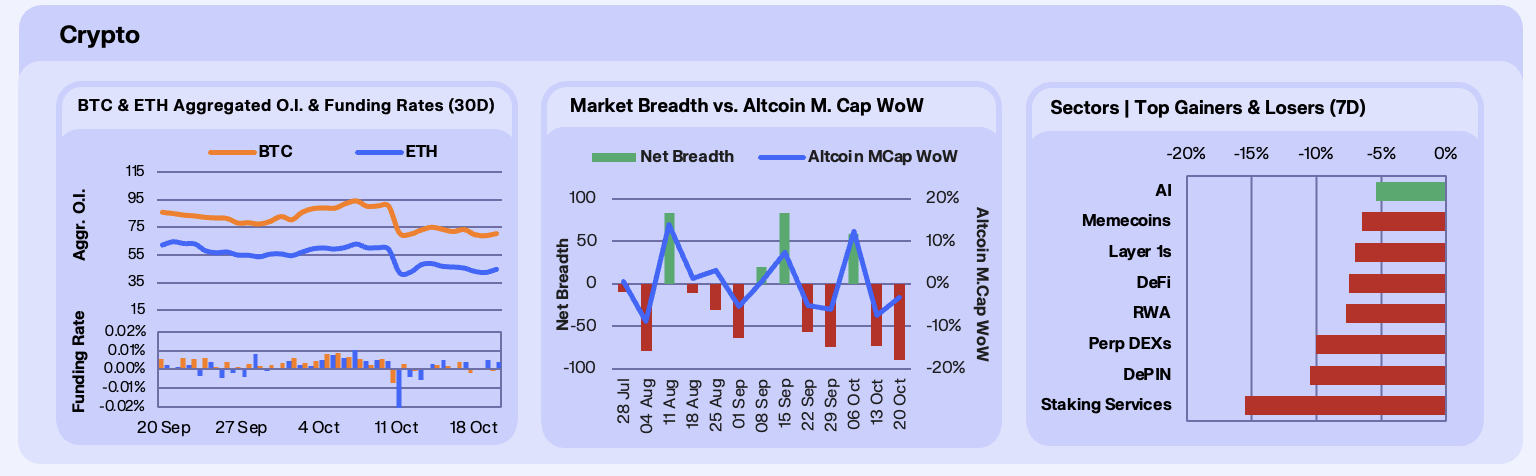

Futures positioning across Bitcoin and Ethereum remains subdued following crypto’s largest liquidation cascade. BTC open interest edged lower by 3.5% to $70.3b, while ETH slipped 7% to $44.6b, a natural reflection of the risk-off tone that intensifies further down the risk curve. Notably, for the first time since 2021, CME has now overtaken Binance in BTC, ETH, and SOL open interest, underscoring growing institutional participation. Although funding rates have normalized around neutral for both majors, BTC’s long-to-short ratio has surged 230% over the past two weeks, suggesting speculative positioning is rotating back toward Bitcoin as futures activity consolidates away from long-tail assets.

Across crypto, last week marked the most uniform and severe breadth decline since we began tracking it, 95 decliners versus 5 advancers, for a net breadth of -90. The liquidation cascade hit long-tail assets hardest, amplified by the growing leverage embedded in the system. The rise of new perpetual DEXs has made it easier for traders to take leveraged positions in assets that previously lacked such access, making drawdowns sharper when positioning unwinds. Liquidity providers also struggled to move inventory across centralized exchanges, leading to thinner books and wider spreads for assets that needed it most. It underscores how critical it is for projects, especially those with long-tail assets, to have professional liquidity support, and begs the question of whether centralized exchanges are doing enough to strengthen the infrastructure needed to cushion such drawdowns.

Sector-wise, the selloff was broad and indiscriminate, with every major category finishing the week in the red. The heaviest losses were concentrated in yield-linked and infrastructure sectors like staking and DePIN, while even stronger narratives such as RWAs weren’t spared. The uniformity of declines reflects a market still under deleveraging pressure, where capital is consolidating back toward majors and speculative appetite across altcoins remains muted.

Our Take: The liquidations hit hardest across altcoins, where there are now far more tokens competing for a smaller pool of capital. Selectivity has become essential, there’s less speculative money to go around, and the bid for long-tail assets will likely stay weak for now. Retail participation will eventually return, but in the short to medium term, an altcoin rebound still feels distant.

Flight to Quality

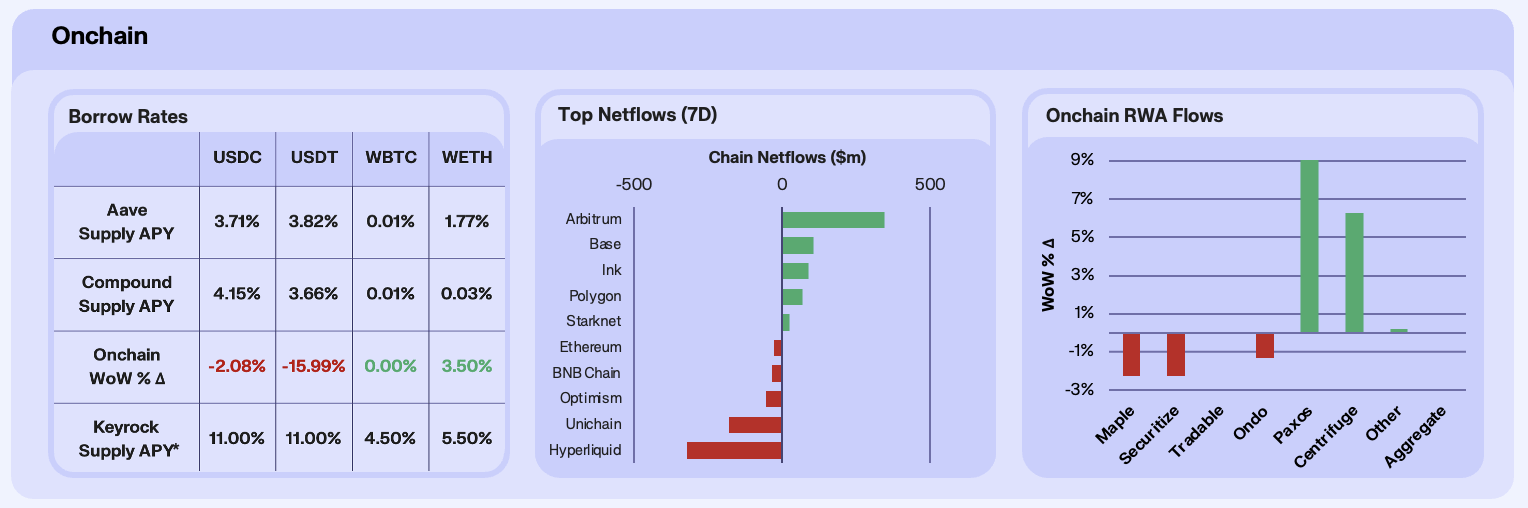

Lending rates have softened across DeFi markets this week, reflecting the post-crash environment seen throughout digital assets markets at large, still defined by deleveraging and risk aversion. USDC and USDT fell to 3.7% and 3.8% respectively while ETH yields edged slightly higher, up 3.5% WoW, as borrowing demand cautiously returned. Aave’s supply base shrank across most assets, down 18.8% for USDC and 16.2% for ETH, suggesting that lenders withdrew liquidity amid uncertainty, compressing available collateral and marginally lifting borrowing rates. These data points suggest onchain lending to be in ‘reset mode’, where participants are reluctant to recycle capital into leverage-heavy strategies.

Chain flows told a clear story of rotation towards stability. Arbitrum led all ecosystems with $344m in inflows. This was potentially buoyed by Arbitrum’s $400m DRIP incentive program, but we note that the inflows almost entirely align with Hyperliquid outflows, following the October 10th liquidation shock. This is the second consecutive week of capital flight from Hyperliquid, which has seen an ~61% drop in OI. Unichain, down $181m WoW, also suffered from post-hype rotation, while Base, up $105m WoW, benefited from institutional activity tied to J.P. Morgan’s USD token pilot and permissionless fault-proof upgrades.

Aggregate RWA AUM remained flat as sector rotation offset individual gains. Paxos led the week, up 10.2%, driven by inflows into PAXG and regulated tokenised treasuries amid a post-crash flight-to-quality. Institutional participants sought tokenised safe havens, a trend reinforced by Pantera’s bullish call on multi-trillion-dollar RWA potential. Centrifuge followed, up 6.3% WoW, propelled by its governance restructure and institutional integrations with Janus Henderson and Apollo. Across the board, the RWA segment absorbed risk-off capital that might otherwise have left DeFi entirely.

Our Take: The onchain landscape this week was defined by reallocation, not retreat. Liquidity didn’t exit crypto, instead it moved up the quality curve from speculative perps and yield farms to Arbitrum, Base, and regulated RWA platforms. Lending remains cautious but stable, with early signs of risk re-entry via ETH borrowing. If volatility continues to ease, capital should gradually flow back down the curve.

Leverage Wiped

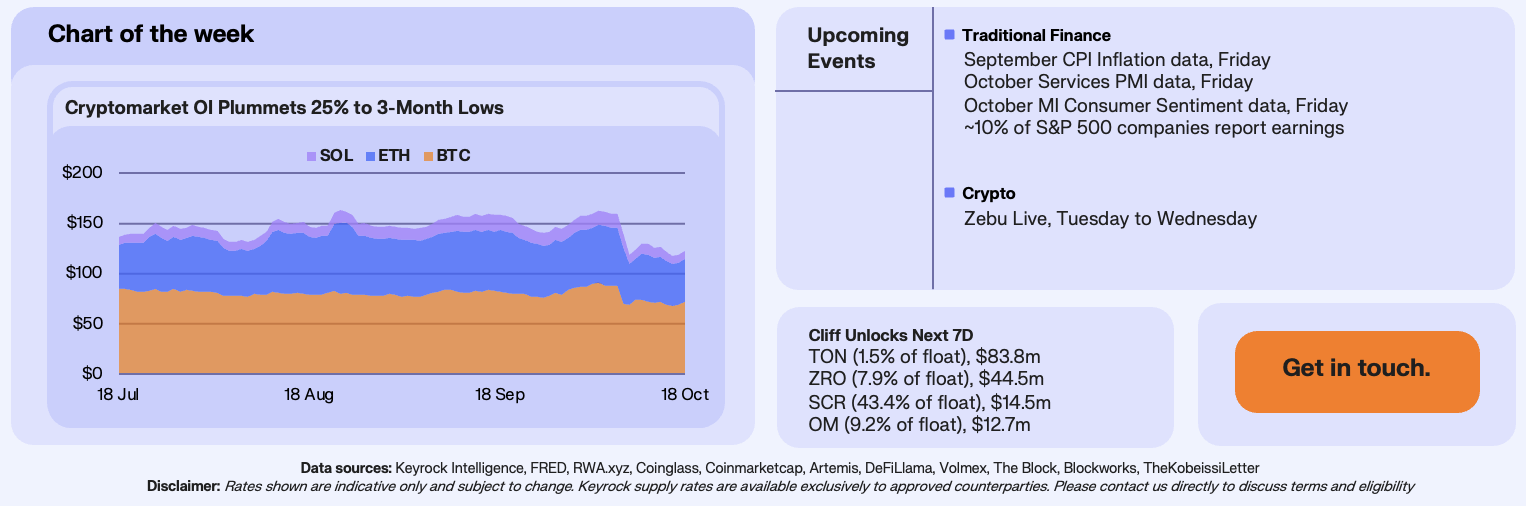

Open interest across majors collapsed ~25% to the lowest level in three months following the October 10th flash crash, and have remained at suppressed levels for the entire week. The tariff-driven risk-off shock triggered an historic liquidation wave of ~$19b market-wide, forcing rapid de-risking across perp venues and spot-hedged basis trades. By week’s end, BTC OI fell ~23%, ETH OI ~24% and SOL OI ~37% off a smaller base. Funding flipped negative across majors, basis compressed, and OI mix shifted up the quality curve with BTC share of total OI increasing, as traders sought cleaner collateral and deeper liquidity.

Despite the deleveraging, onchain derivatives surged in volumes. Hyperliquid posted its highest-ever weekly perp volume of over $120b, even as more than $10b of OI was wiped and roughly $720m net capital flowed out afterward. Crucially, the chain had no downtime, a sharp contrast to several CEX frictions during the break. Across the industry, venues that rely on internal order-book prints for oracle pricing saw costly wicks and ADL episodes, with some facing partial trade reversals and refunds after off-market prints. Onchain perps that route price discovery transparently, generally handled the volatility better.

Our Take: The OI purge looks more like a reset than a regime change. With leverage rinsed and funding normalised, rebuilding should start from a healthier base, led by BTC and ETH. The week also served as a stress-test for market structure, with onchain venues clearing the volatility with uptime and transparency, which should keep liquidity gravitating toward onchain perps through Q4.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.