9 March 2026

Key Insights: The Crude Awakening

Energy Drives Markets

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

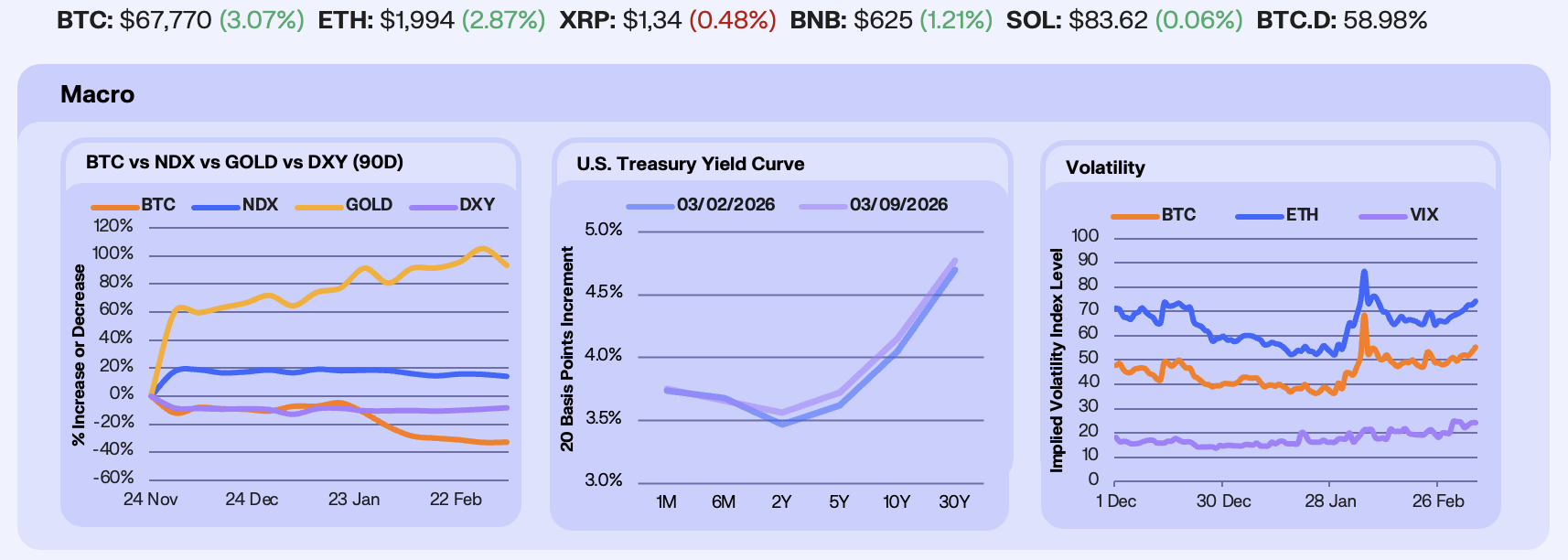

Markets remained volatile this week as geopolitical tensions escalated following continued U.S. operations in Iran. Energy markets saw a shock with WTI crude rising roughly 45% in the last month, amplifying concerns that higher oil prices could reintroduce inflation pressure in an already hawkish policy environment. Investors are increasingly assessing the risk that the conflict drags on, keeping commodity markets elevated and injecting uncertainty across risk assets. BTC rose +0.3% on the week after briefly breaking above $74,000 for the first time since early February before settling near $70,000. In contrast, gold declined −5.8% despite ongoing geopolitical tensions, while the Nasdaq edged lower -1.3%. The U.S. dollar strengthened +1.1% as energy-driven inflation concerns and safe-haven demand supported the currency.

Rates markets reflected the inflationary implications of higher energy prices. Treasury yields moved higher across the curve, led by the long end, as traders reassessed the likelihood of monetary easing. The probability of no rate cuts in 2026 has risen from roughly 12% to 20% as markets price the risk that sustained energy shocks could keep inflation elevated. Rising inflation expectations make long-duration bonds less attractive, pushing yields higher while supporting the dollar through safe-haven flows and stronger petrodollar demand as oil prices climb. A 25 or 50 bps rate cut in 2026 continues to be the most probable options, although this could drastically change in the week ahead depending on the Iran war.

Volatility dynamics diverged across markets. BTC 30-day implied volatility rose +8.4% to 55 and ETH IV increased +8.6% to 74, while the VIX declined -1.9% to 24 as equity volatility moderated slightly. Options markets reflect continued uncertainty around near-term price direction. Current pricing implies roughly a 40% probability BTC reaches $75K in March, versus 40% odds of a retracement toward $60K, while longer-dated expectations remain restrained with the probability of BTC breaking $100K in 2026 at 35%. Given the recent increase in implied volatility, combined with a decline in realized volatility as BTC continues to trade in a range, volatility appears relatively rich at current levels. In addition, the geopolitical backdrop introduces asymmetric downside risks. In this context, we favor monetizing elevated implied volatility by overwriting the upside in BTC through the sale of out-of-the-money calls, allowing investors to capture premium while the market remains range-bound:

Our Take: Energy markets have now become the primary macro transmission channel for risk assets. Sustained oil strength would reinforce inflation pressures and delay monetary easing, likely keeping volatility elevated across equities and crypto. Despite this backdrop, Bitcoin’s ability to rally alongside a strengthening dollar and rising geopolitical risk suggests sellers may be increasingly exhausted. If energy markets stabilize, BTC could continue grinding higher in the weeks ahead, though macro-driven volatility is likely to remain elevated.

Flows Signal Stabilization

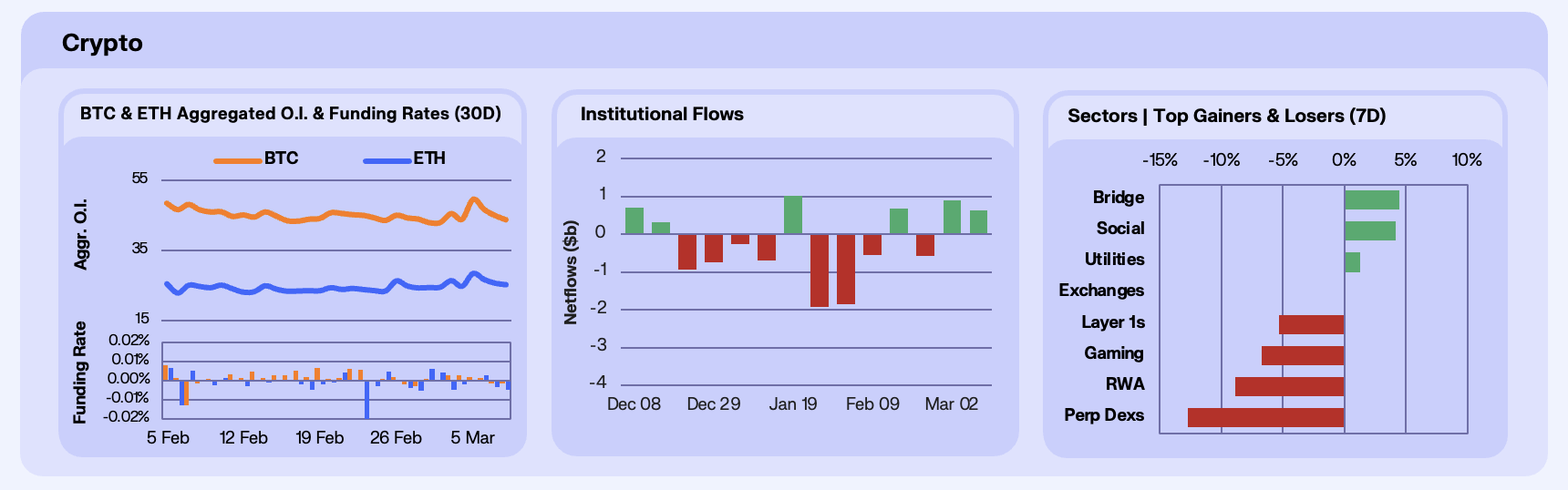

Crypto markets stabilized this week as derivatives positioning rebuilt following the geopolitical volatility triggered by U.S. airstrikes on Iran. BTC open interest rose +2% WoW to $43.8b, while ETH OI climbed +3% to $25.3b. Funding rates briefly reached a local bottom during the initial risk-off reaction as short positioning concentrated, but have since normalized back toward neutral. The aggressive downside positioning seen earlier in the week has largely been absorbed, with derivatives markets now reflecting a more balanced posture, though still hesitant amid concerns about oil prices and how the Iran war will escalate in the weeks ahead.

Institutional demand also strengthened. Digital asset investment products saw approximately $634m in net inflows last week, marking one of the strongest two-week accumulation periods since late 2025. Bitcoin spot ETFs accounted for the majority of flows, with $568m of net inflows for the week, while Ethereum products added $24m and Solana products $23m. Renewed allocations in the midst of a turbulent market suggests investors are growing more comfortable adding exposure despite Bitcoin remaining roughly 16% below its yearly highs, with recent resilience amid geopolitical stress helping restore confidence that the market may have found at least a short-term bottom. Altcoin activity was driven largely by idiosyncratic catalysts. OKB surged roughly 30% after Intercontinental Exchange announced a $25 billion investment initiative. Meanwhile NEAR rallied 3% after launching Confidential Intents, a private execution layer designed to reduce front-running and MEV through confidential accounts. Even as macro conditions dominate broader market direction, protocol-specific catalysts continue to drive relative performance within the altcoin market.

Our Take: As we have noted in recent updates, the altcoin market increasingly appears to have transitioned into an accumulation phase. Institutional interest is beginning to concentrate around protocols with tangible revenue generation, strong usage metrics, or direct engagement from traditional financial players. Tokens tied to growing onchain cash flows or infrastructure demand are likely to lead the next cycle. With Bitcoin consolidating near $70K, this environment increasingly favors fundamental differentiation rather than broad beta exposure across the altcoin market.

Perps Capture Volatility

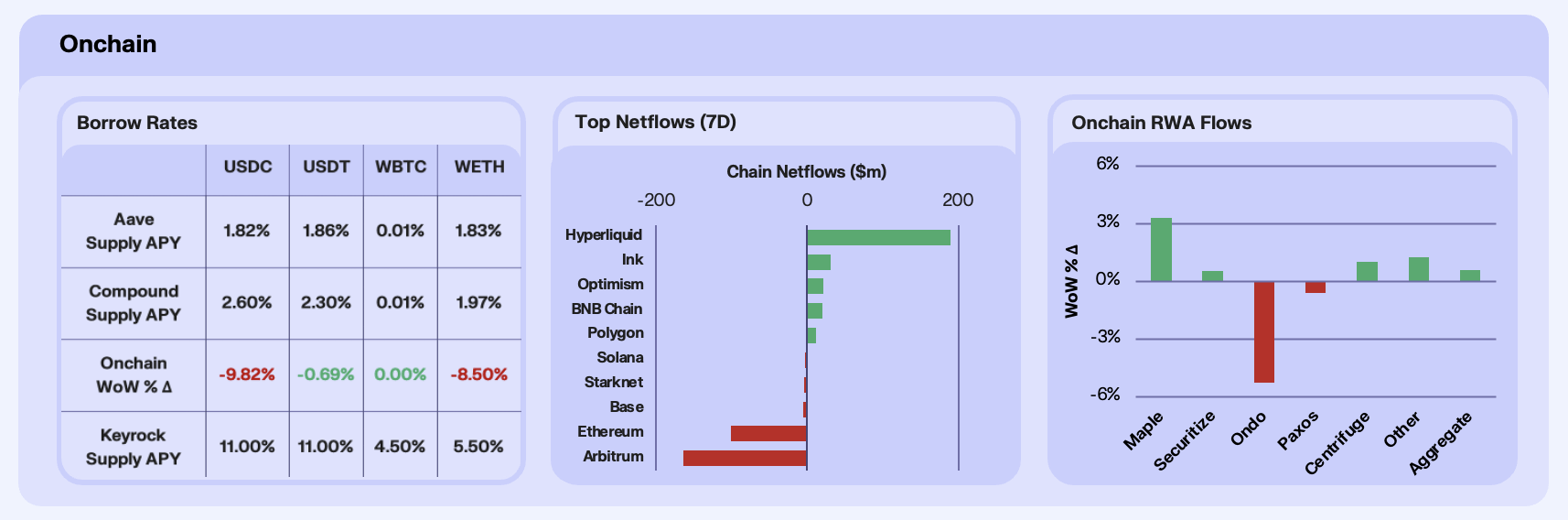

Onchain rates dropped across the board this week, continuing the gradual compression in lending yields across major assets. USDC was the stablecoin that declined the hardest, with a 9.8% drop WoW, versus only a 0.7% drop for USDT. Both stablecoin rates declined in light of constricted supply, indicating this fall in rates was demand-led. ETH-denominated yields also weakened, with WETH supply down 8.5% WoW, reinforcing the view that leverage demand remains subdued and that the onchain market is still digesting recent volatility rather than aggressively recycling liquidity through stablecoin looping. Utilisation remains muted across lending venues, suggesting capital is staying defensive despite pockets of speculative activity elsewhere in the ecosystem.

Chain flows told a more directional story this week, with capital concentrating in venues offering clear trading utility during the week’s geopolitical volatility. Hyperliquid led inflows with +$190m, benefiting from the surge in commodity-linked perpetual trading following the escalation of Middle East tensions and the resulting spike in oil volatility. The platform’s 24/7 derivatives markets attracted traders looking to hedge or express macro views outside traditional market hours. On the downside, Arbitrum (-$165m) saw continued outflows following whale distribution and security-related concerns, while Ethereum (-$101m) experienced modest net outflows as ETF redemptions continued.

RWAs remained marginally positive overall, with aggregate AUM up 0.60% WoW, though performance was again varied widely across protocols. Maple (+3.29%) led gains as institutional lending demand continued to expand, supported by strong loan origination. Ondo (-5.25%) declined as market volatility triggered rebalancing across tokenised securities exposure, while Paxos (-0.61%) saw a slight dip driven primarily by minor fluctuations in gold prices affecting PAXG’s market value. The RWA sub-sector showed resilience despite broader crypto market stress, with credit and treasury products continuing to anchor the sector.

Our take: This week again highlighted the increasingly fragmented nature of the onchain economy. As the lines between traditional finance and DeFi blur, gone are the days when DeFi universally takes a hit in risk-off environments, instead we see rotations into risk-off assets that mirror traditional finance, only onchain. Looking forward, the key signal we are watching remains utilisation returning to lending markets, as a sustained rise in borrowing demand would mark a clearer shift back toward broader and more typical onchain risk-taking.

Treasury Concentration Gap

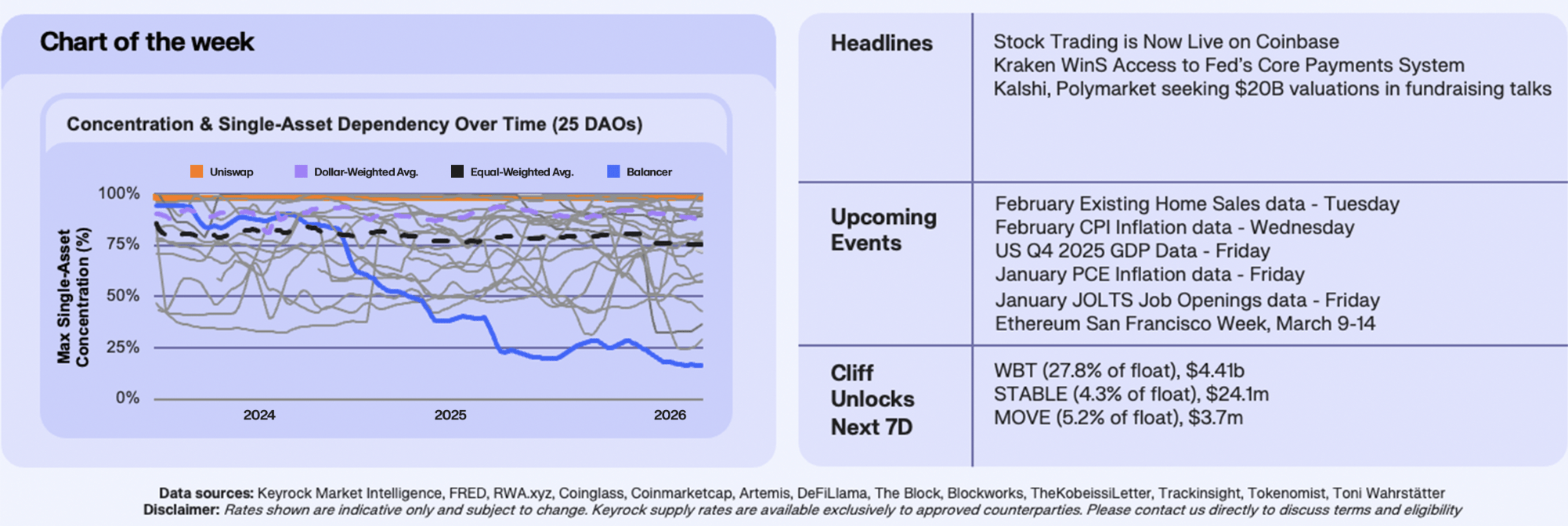

This week’s chart examines single-asset concentration across the top 25 crypto-native treasuries, tracking the share of treasury value held in the largest asset over time. Across the sample, the dollar-weighted average concentration sits around 88%, while the equal-weighted average is 76%, highlighting that the largest treasuries remain overwhelmingly dependent on a single asset, which our analysis shows is typically their own governance token. The dispersion is striking. At the extreme, Uniswap sits at effectively 100% concentration, holding nearly its entire treasury in UNI. At the other end, Balancer has reduced its largest asset exposure to 17%, demonstrating active diversification, a rare strategy in the world of crypto-native treasury management.

The implication is that many crypto-native balance sheets remain structurally dependent on a single-asset, and thus remain fragile. Our research finds that approximately 80% of aggregate treasury value across the sector is concentrated in native governance tokens, while the median treasury allocates only 7% of capital to productive yield-bearing positions. This concentration amplifies upside during bull markets but also compounds drawdowns during downturns. The chart illustrates this dynamic clearly, diversification only improves meaningfully when treasuries actively rebalance, as seen with protocols like Aave and Balancer, rather than allowing market movements to mechanically increase native token exposure.

Our take: The era of passive treasury HODLing is starting to end. As crypto-native organisations mature into billion-dollar balance sheets, treasury management is becoming a strategic differentiator rather than an afterthought. Protocols that build stable buffers, deploy capital productively, and systematically manage concentration will enter future market cycles with significantly greater resilience. In our upcoming report with Safe and DL Research, we explore how this transition from accumulation to active treasury management is already underway, and why it may become one of the most important structural shifts in crypto over the next few years.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.