27 April 2026

Key Insights: The Calm Before Powell

Ceasefire on Paper

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

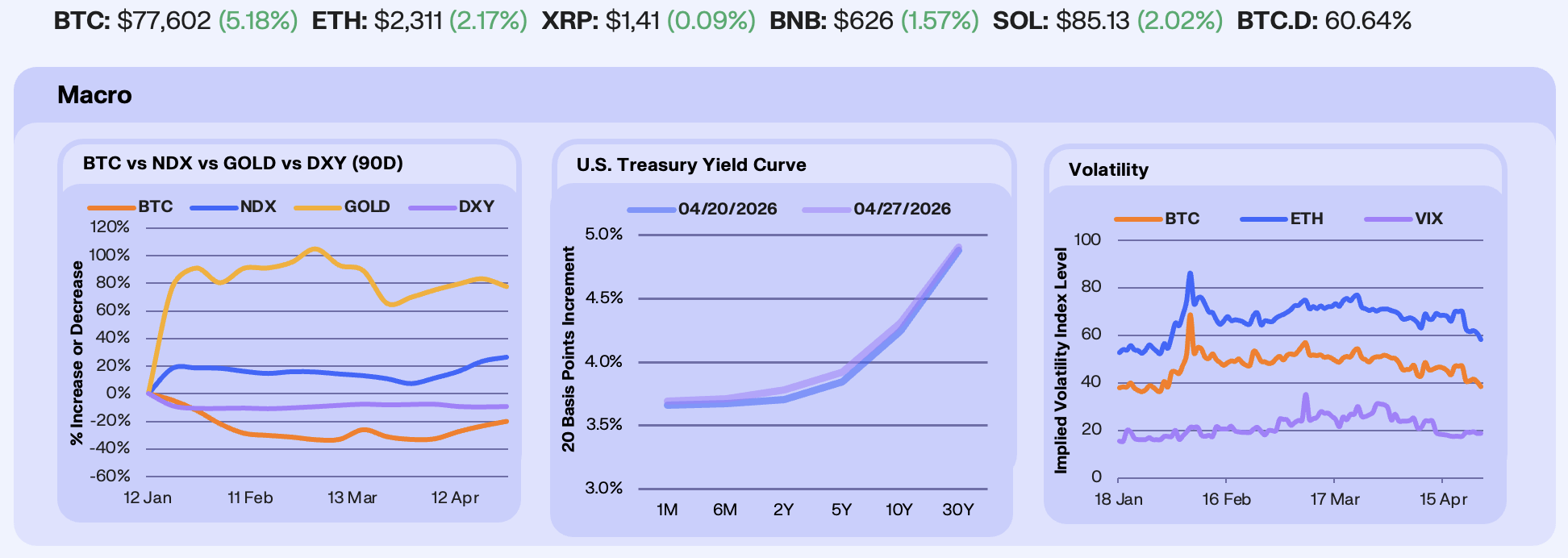

The Iran ceasefire was extended Tuesday, hours before the two-week truce expired, but the US naval blockade of the Strait of Hormuz stayed in place. Brent responded to the physical reality rather than the headline, rallying roughly +13% on the week to $107 as shipping disruption and Iranian interdiction repriced energy risk. BTC added +4.2% to $78,600 on a combination of Strategy’s $2.54B purchase of 34,164 BTC announced early in the week, and an nine-day spot ETF inflow streak totaling $2.2B led by IBIT. Gold fell -3.1% to $4,685 in a positioning unwind, with gold ETFs having posted their largest monthly outflow on record in March and CTAs de-grossing from mid-March peak long exposure. NDX added +2.4% to $27,300, digesting the crude move while extending, and DXY held essentially flat at 98.36 as rate differentials offset risk flows.

Treasury yields sold off across the curve with the belly doing the work. The shape is a textbook belly-led bear flattener, consistent with the market pricing a higher near-term path rather than a structural shift in longer-run inflation. Thursday’s flash PMI did the repricing. Manufacturing jumped to 54.0 from 52.3, the composite hit a three-month high at 52.0, and manufacturing input prices climbed to a ten-month high. Initial jobless claims at 214,000 offered no labour-side offset. Cleveland Fed’s Hammack floated the possibility of a rate hike last week, citing the Cleveland nowcast pointing to 3.5% April CPI, and the Fed enters the April 28–29 FOMC in blackout with no Powell counterweight available. CME FedWatch has roughly 99% priced for a hold, with the first cut pushed into late 2026. The belly is telegraphing a hawkish hold, and the front end is now vulnerable to any Powell emphasis on energy pass-through.

Volatility compressed across all three benchmarks . BTC 30-day ATM IV eased -8.7% to 38.5, ETH IV fell -10.1% to 58.3, and VIX declined -4.4% to 18.7 into Friday. Options positioning tells a narrower story. BTC open interest on Deribit sits at 351,000 BTC with an OI-weighted put-call ratio of 0.67, and the dominant 26JUN26 expiry holds 110,800 BTC at a 0.73 OI put-call. The front-end 1MAY expiry, the first to contain the April 28-29 FOMC, carries a 1.24 OI put-call, while 29MAY, 26JUN, 25SEP and 25DEC all sit between 0.50 and 0.73. The shape reads as targeted FOMC hedging at the front rather than broad de-risking, with medium-term tenors still leaning call-heavy and the oil shock priced as a range-bound complication rather than a directional break.

Our Take: We think the market is underpricing the hawkish risk into Wednesday. With the blockade holding, Brent at $107, and manufacturing input prices at a ten-month high, Powell has no cover to lean dovish. However, BTC is telling a different story. The passive institutional bid has absorbed every round of short-term holder distribution and is lifting spot through macro conditions that should work against it. The sub-$70k print earlier this month increasingly looks like a local floor.

Short Crowding Deepens

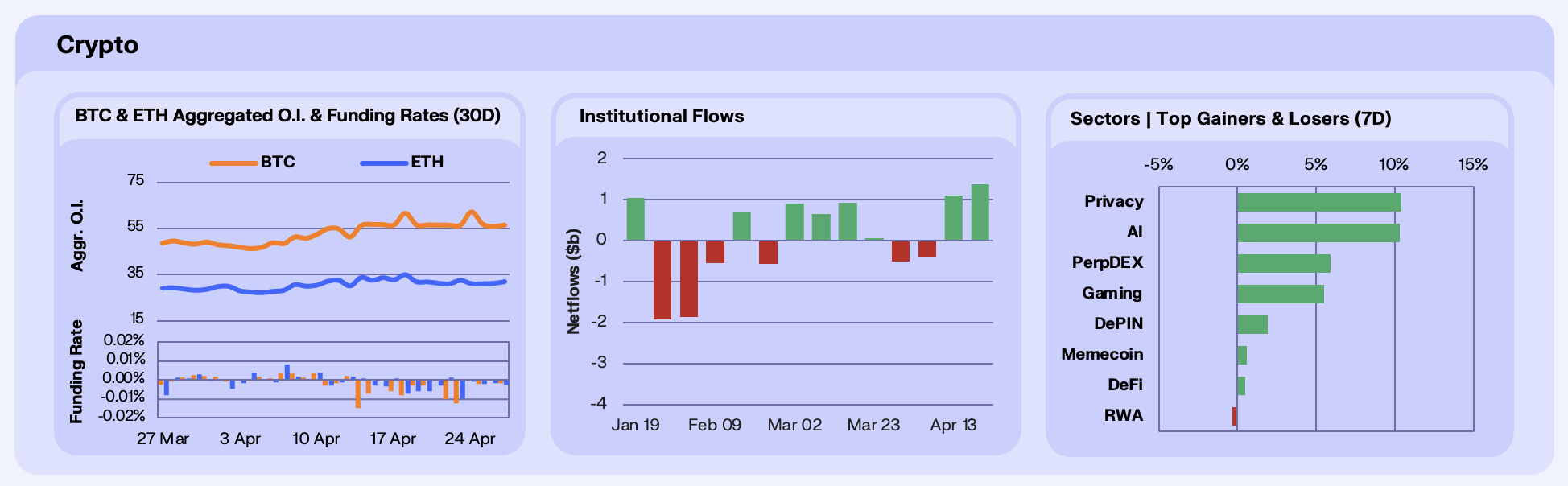

Open interest closed the week with a flat print that masks a dramatic intra-week spike and full reversal. BTC OI slipped -0.02% WoW to $56.54B, while ETH edged up +2.15% to $31.86B. The ceasefire expiry on April 22nd initially produced muted price action and deeply negative funding, suggesting traders added to short positioning into the event. Then on April 24th, BTC OI spiked to $62.27B, a $5.8B single-session build that almost exactly mirrors the April 18th Hormuz episode. The catalyst was a convergence of a $9.5B BTC/ETH options expiry across Deribit, OKX, and CME, with bulls dominating higher strikes, layered on top of the carry-through from Trump’s indefinite ceasefire extension announced April 21st at Pakistan’s request. By Friday the entire build had unwound, with OI falling back to $55.98B, the same playbook of explosive positioning, rapid unwind, and reversion to base that has now repeated twice in ten days. BTC funding briefly flipped positive several times this week, technically breaking the 46-day negative streak noted last week, but the flips were so marginal that calling this a regime change would be generous. The April 22-23rd readings around -0.01% were among the most negative prints in weeks, and ETH funding remained negative on six of seven days. The structural read remains that the market continues to default to short positioning, with each squeeze producing a violent but fleeting OI spike that fully unwinds within 48 hours, and the resting level of $56B in BTC OI has barely moved in three weeks despite price holding near cycle highs.

Institutional flows sustained their momentum for a third consecutive week, with Bitcoin ETFs recording +$823.7M in weekly inflows, Ethereum adding +$155M, Solana +$9.44M, and Ripple +$15.74M, for a combined +$1.004B. While down from last week’s +$1.36B surge, this marks the first time since January that three straight weeks have each exceeded $700M, bringing the three-week cumulative to roughly $3.06B. BTC continues to capture the lion’s share at 82% of the weekly total. BTC ETF AUM now sits at ~$103B, up from $91B last week as inflows and price appreciation compounded. YTD crypto ETF flows sit at an estimated $2B, with April alone contributing the bulk of the recovery after Q1’s persistent outflows, consolidating the reversal into what is beginning to resemble a durable re-risking trend across institutional allocators.

Sector performance was broadly positive with a growth-and-privacy tilt. Privacy led for the second time in three weeks at +10.4%, extending the EU AMLR compliance narrative that drove ZEC’s +61.3% surge on April 13th, the regulatory tailwind around viewing keys and the pending Grayscale ZEC ETF filing continue to underpin the sector. AI matched closely at +10.3%, a sharp reversal after weeks of underperformance, catalysed by Binance Wallet’s launch of its Agentic Wallet on April 24th. PerpDEX continued its quiet run at +5.9%, building on March 30th’s +7.0% as Hyperliquid’s HIP-3 staking mechanics sustained volume growth. On the downside, the week’s laggards were notable for who they were rather than the depth of losses. Memecoins faded to +0.6% after co-leading at +7.4% just a week ago, suggesting the PEPE ETF filing impulse has fully dissipated.

Our Take: The ceasefire lapsed and the market gave us a second consecutive $5B+ OI spike-and-unwind cycle that resolved without breaking the institutional bid underneath. Repeatedly we’re seeing leveraged positioning builds aggressively on event catalysts, for them to get flushed within 48 hours, yet the three-week $3.06B in ETF inflows refuses to participate in the unwind. Our desk reads this as a market bifurcating into a futures complex still trapped in effectively negative funding and a spot-driven institutional floor that keeps ratcheting higher. The next test is whether the post-ceasefire policy vacuum produces a fresh headline catalyst or whether the funding regime normalises on its own, our bias is that the longer negative funding persists against rising institutional inflows, the more violent the eventual repricing.

The KelpDAO Fallout

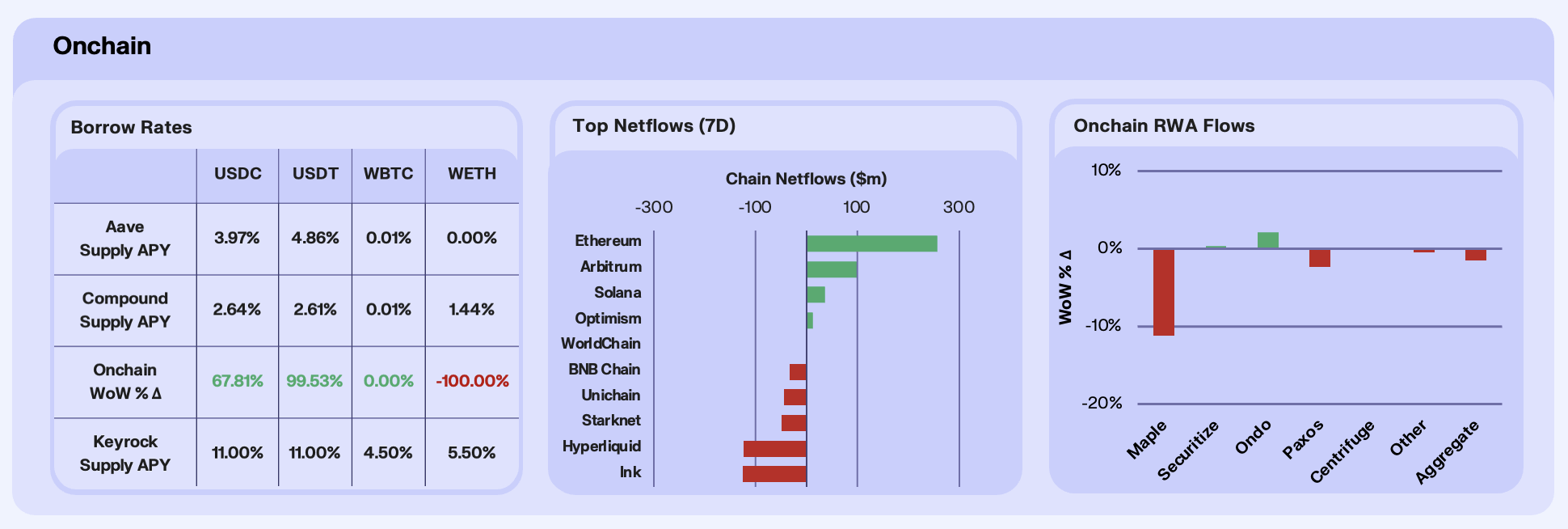

Stablecoin lending rates surged this week, with the KelpDAO rsETH exploit being the primary catalyst. USDC supply APY jumped +67.81% WoW across major venues, while USDT nearly doubled at +99.53% WoW. WETH supply APY on Aave collapsed to zero. The rate moves were driven almost entirely by a supply shock, whereby Aave deposits cratered as depositors fled post-exploit, with USDC supply down -85%, USDT -92%, and WETH -100% to zero. The freezing of rsETH markets across Aave, SparkLend, and Fluid following the $292M LayerZero bridge hack removed a significant source of collateral, while Maple’s decision to withdraw all syrupUSDT from Aave Mantle and service $800M in redemptions within 72 hours compounded the supply drain. The same borrowing demand chasing dramatically less supply pushes utilisation and rates higher, which is why USDT is printing nearly 5% on Aave even as the pool has shed over 90% of its deposits.

Chain-level flows saw Ethereum pos +$258.8M in net inflows, a sharp reversal from the persistent outflows that had defined prior weeks. The catalyst was both sustained US spot ETH ETF inflows, at $155M for the week, with BlackRock’s ETHA leading multiple sessions, and the KelpDAO exploit that triggered a broader flight-to-quality rotation toward Ethereum mainnet and established ecosystems. Arbitrum posted +$98.5M, consolidating a second consecutive strong week after last week’s dominant +$444.9M, supported by the Security Council’s emergency freeze of 30,766 ETH tied to the KelpDAO breach, reinforcing governance credibility. Hyperliquid, which had led inflows for four consecutive weeks through mid-April, reversed sharply to -$124.9M in net outflows as profit-taking and capital rotation set in amid slowing perp activity and no fresh catalysts. The overarching pattern was capital consolidating back into blue-chip infrastructure after weeks of rotating toward specialised and high-momentum venues, with the KelpDAO exploit accelerating a flight to quality that was arguably already underway.

RWA AUM fell -1.47% WoW in aggregate, the first weekly decline after five consecutive weeks of growth. The drop was almost entirely Maple-driven at -11.19% on the week after it fully withdrew all syrupUSDT liquidity from Aave Mantle on April 20th in the wake of the KelpDAO rsETH exploit two days earlier, having already exited Aave V3 mainnet. Maple serviced over $800M in redemptions within 72 hours of the incident without disruption, but a mid-week $100M institutional loan backed by BTC was insufficient to offset the outflows. Ondo posted +2.06%, adding its 18th batch of tokenised stock trading pairs on MEXC via Ondo Global Markets, while Securitize edged up +0.35% after partnering with Upshift for independent audit-ready reporting through its Vault Registrar architecture.

Our Take: The KelpDAO exploit was the week’s primary news item, it collapsed utilisation across lending markets, triggered a flight to quality back into Ethereum, and forced Maple’s withdrawal from Aave. What’s striking is what didn’t break, that being stablecoin supply rates held above the 2% floor we’ve been watching for weeks even as utilisation fell to near-zero, Maple serviced $800M in redemptions within 72 hours without a liquidity gap, and Arbitrum’s Security Council froze stolen assets fast enough to post a second consecutive week of inflows. Our desk is watching whether the utilisation snapback, when it comes, reprices lending rates higher or simply confirms that onchain credit markets have structurally decoupled from onchain credit risk.

The 1.7M Sink

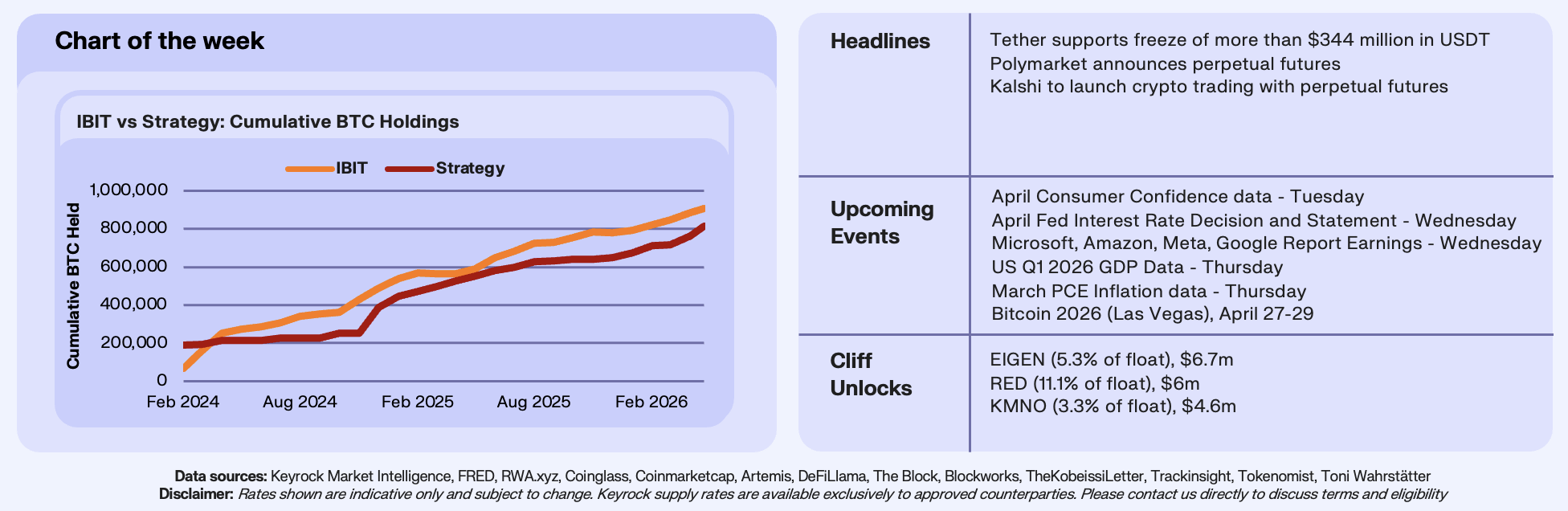

This week’s hawkish reprice in yields and the Brent rally would normally weigh on Bitcoin. Spot added +4.2% instead, and the reason sits in two balance sheets. IBIT and Strategy have been the marginal sink for BTC since early 2024, and together they now hold the largest concentrated position of any institutional structure outside legacy custodians. The cycle’s spot floor below $70k has held because two non-discretionary buyers are absorbing every round of short-term holder distribution.

IBIT now holds 907,274 BTC and Strategy 815,061 BTC. Combined that is 1,722,335 BTC, roughly 8.2% of circulating supply. IBIT crossed Strategy on March 13, 2024, just two months after launch, and the gap widened to a peak of 191,000 BTC by November 2024 as the ETF complex compounded daily inflows through the post-election window. Through 2026 Strategy has closed that gap aggressively. The current spread is +92,000 BTC and shrinking. YTD, Strategy has added 143,000 BTC against IBIT’s 116,000, and over the last six weeks Strategy has added 76,000 BTC versus IBIT’s 36,000. Strategy is now the marginal buyer.

The two engines run on different mechanics. IBIT’s flow comes from RIA model allocations and HNW conversions, daily and continuous. Strategy buys in lumps funded by convertible debt and ATM equity issuance, episodic but large when triggered. Once BTC enters either pocket the supply leaves the float, which is why realized cap has compounded through the recent drawdown even as short-term holders have distributed.

Our Take: The two-pillar bid is the defining structural feature of this cycle, and it just absorbed a hawkish reprice without flinching. As long as both engines run, the sub-$70k print earlier this month is the floor. The single catalyst that would change our view is a sustained net outflow week from IBIT combined with a Strategy issuance pause. Until then the macro narrative is noise on top of a one-way absorption mechanism.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.