27 October 2025

Key Insights: The Calm After Xi-Storm

Markets Find Relief

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

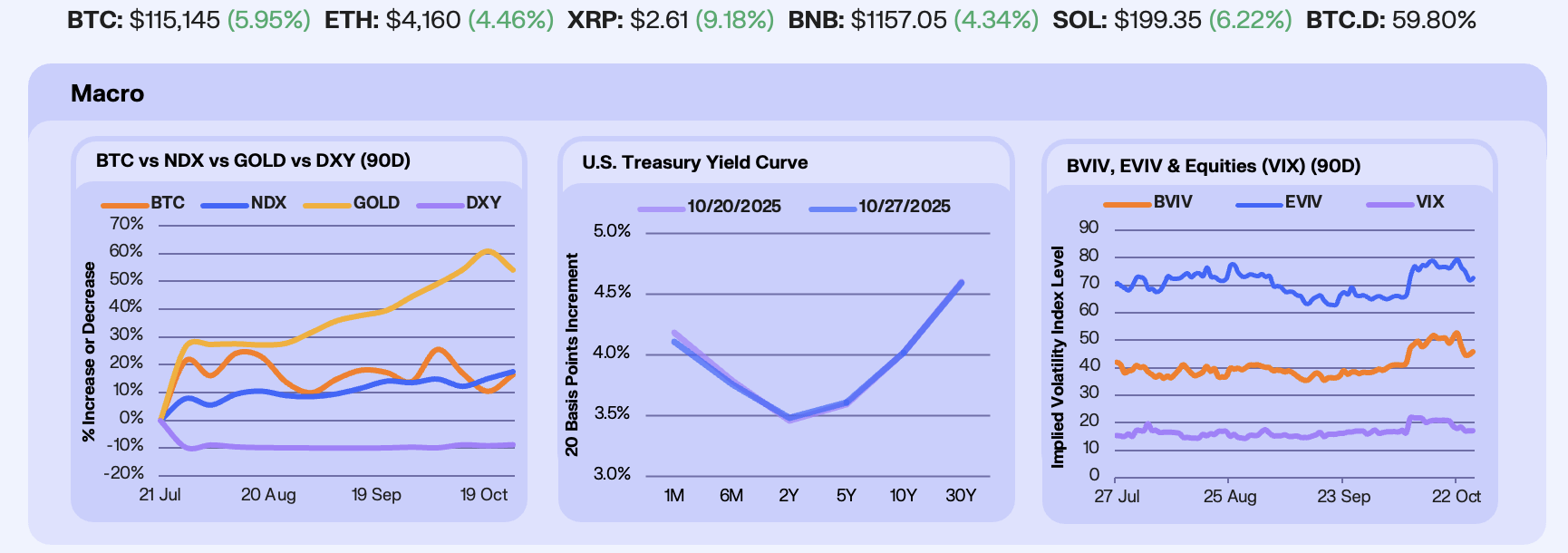

Last week, concerns over the U.S.-China trade deal, which had sent markets tumbling two weeks prior amid signs of renewed tension, eased after the White House announced that President Trump will meet with President Xi on October 30th. Meanwhile, softer September CPI data and reports of ‘constructive’ U.S.-China trade talks helped lift market sentiment. Bitcoin surged (+5.4%), Gold finally paused after nine straight weeks of gains (-4.5%), the Nasdaq (+2.2%) continued its steady climb, and the U.S. Dollar rose (+0.5%).

The Treasury curve held largely steady with modest easing at the front end as traders ramped up bets on aggressive Fed cuts. Open Interest for Secured Overnight Financing Rate (SOFR) call options, which trade on Fed interest rates falling to 3.50% by year end, reached their highest on record. Markets now price in 75 bps of easing by year-end. There’s growing conviction that the Fed will be forced to move faster.

Volatility eased across assets as markets stabilized after last week’s stress. The VIX slipped back below 20, closing near 17, while Bitcoin and Ether implied vols, BVIV (-6.4%) and EVIV (-4.8%), continued to drift lower as option premiums normalized. Softer rhetoric around trade tensions and contained regional-bank headlines helped calm nerves, while a cooler-than-expected CPI print lifted risk sentiment. With inflation data now out but reactions still settling, volatility could pick up again if rate-cut expectations shift meaningfully next week.

Our Take: Aggressive rate cuts are increasingly being priced in, and while that could bode well for risk assets, the market’s still leaning toward caution. Softer yields and easing expectations usually lift crypto sentiment, but investors remain wary of what those cuts represent. Still, as we noted last week, Bitcoin’s multi-year lows against gold marked an important inflection. It’s since found some relief, and if liquidity conditions continue to improve, we think that trend should hold.

Liquidity Flows Back

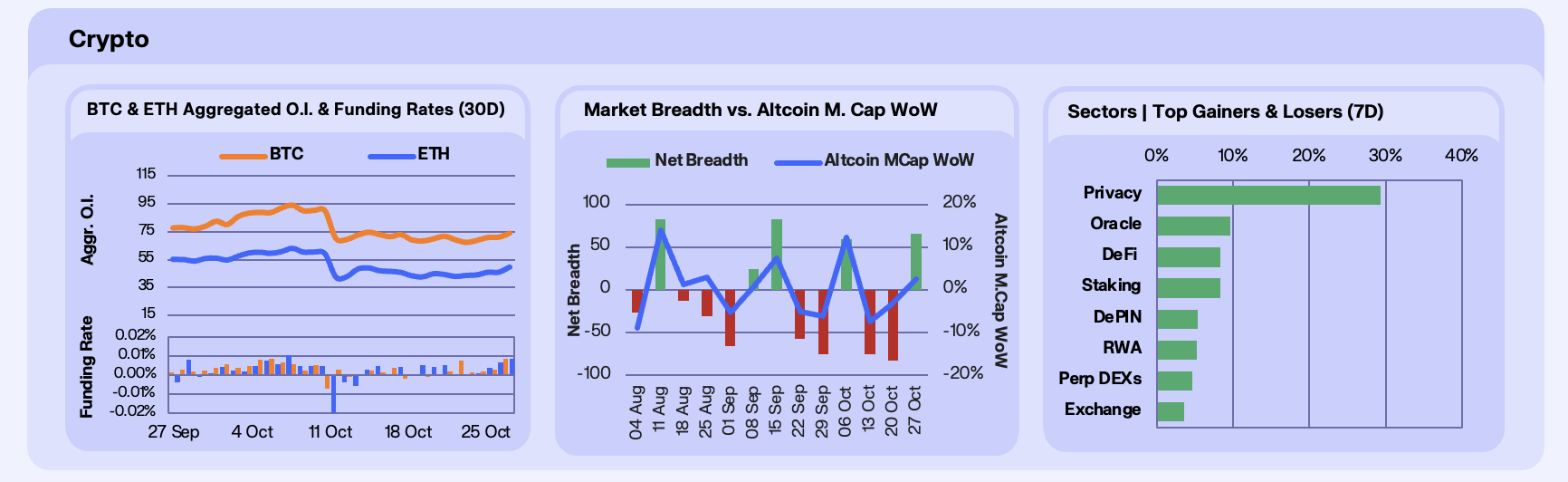

This week was particularly strong for the crypto market, with a back-half of the week rally as markets reacted to easing geopolitical tensions. Bitcoin rose 4.1% to close near $115k, Ethereum gained 3.6%, and Solana outperformed at 5.2%, regaining the psychological $200 mark. The move was spurred on by a moderation in Fed rhetoric, and renewed institutional inflows. Spot Bitcoin ETFs flipped decisively positive mid-week with $618m in cumulative inflows, reversing last week’s $1.2b bleed. Whales and institutional allocators accumulated heavily, with ARK Invest, BlackRock, and Fidelity all net buyers, signaling a revival of the ‘Uptober’ narrative. ETH mirrored the rotation, boosted by $205m in net ETF inflows and leveraged whale positioning. SOL captured high beta to sentiment, aided by Hong Kong’s SOL ETF approval and network-level catalysts such as validator efficiency upgrades and the Alpenglow release.

OI reflected the gradual re-risking, with BTC OI rising 3.1% WoW, while ETH OI jumped 12.3%, marking the strongest weekly rebound since early August. Funding rates for both majors turned modestly positive after two weeks of near-zero or negative levels, indicating cautious appetite for longs. The recovery in ETH OI notably outpaced BTC’s, underscoring trader preference for higher-beta assets once volatility stabilises. Perp market spreads narrowed sharply, basis normalised, and options skew flipped neutral, signaling that speculative capital is re-entering with more balanced positioning. The data paints a picture of a cleaner, more sustainable leverage structure, to be expected shortly after a large, marketwide liquidation event.

Market breadth improved dramatically. After two weeks of capitulation, the market flipped near-neutral at -4, with 48 advancers vs. 52 decliners. While aggregate altcoin market cap still slipped 1.9%, the breadth normalisation reflects rotation into altcoins following market recovery. Traders moved back into large-cap and mid-tier names after sitting out the prior week’s crash. The sharp reversal in breadth aligns with a classic early-stage recovery phase.

Among sectors, Privacy tokens dominated, up 29.3% WoW, led by Zcash, which surged 45.3% to highs near $340. The rally was fueled by Arthur Hayes’ viral call for ZEC to reach $10k, citing zk-proof technology as crypto’s ultimate defense against the rise of surveillance finance. The narrative was amplified by ZEC’s upcoming November halving. Beyond Privacy, Oracles (+9.6%), DeFi (+8.3%), and RWA (+5.2%) sectors also posted solid rebounds as liquidity was recycled into yield and infrastructure plays.

Our Take: This week’s bounce was a signal of resilience. Institutional capital flowed back in, leverage rebuilt in moderation, and breadth stabalised, showing the system absorbed October’s shock without structural damage. If ETF inflows persist and funding remains orderly, Q4 could evolve into a liquidity-led grind higher.

Capital Climbs the Stack

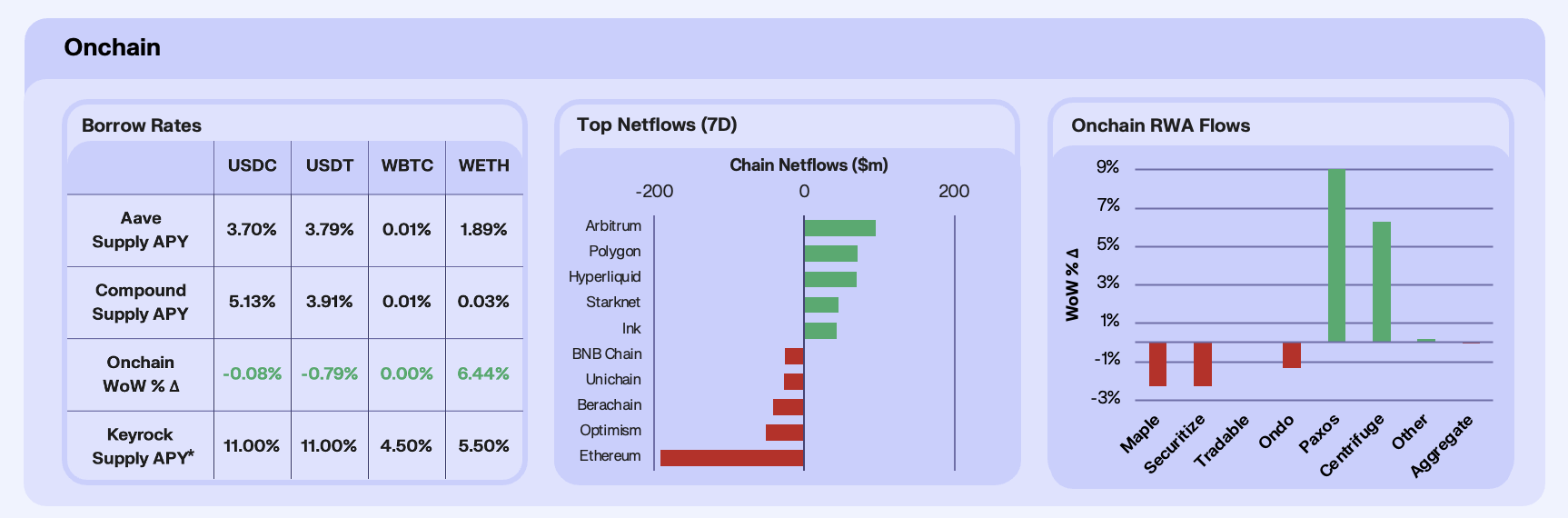

Lending rates across DeFi markets were broadly stable this week, despite the cautious re-risking seen in other areas of the market. USDC and USDT yields softened slightly to 3.7-3.8%. ETH borrowing demand increased, pushing rates up 6.4% WoW, while WBTC remained anchored at near-zero levels. On Aave, total supply balances declined for stables but rebounded for crypto-native assets, with ETH up 37% and WBTC up 6%, signaling a pivot away from passive stablecoin lending toward productive collateral.

Chain flows told a clear story of Ethereum’s capital migration toward more efficient ecosystems, likely as sentiment returned. Ethereum bled $170m, while L2s absorbed liquidity, particularly Arbitrum, up $171m, and Polygon, up $65m, while Solana was up $45m. Meanwhile, Optimism and Base both saw modest outflows amid fragmentation fatigue. Onchain data also confirmed a broader pattern, with 35% of ETH’s outbound L1 capital reappearing on L2s, suggesting this is capital optimisation as capital chases yields on more speculative venues. The cumulative effect has been a modest 2% increase in DeFi TVL.

RWA flows were largely flat overall, but Paxos, up 10.2%, and Centrifuge, up 6.3%, stood out as sector leaders. Paxos’ gains were powered by tokenised gold demand, with PAXG inflows tracking gold’s rally to $4,200/oz, while Centrifuge benefited from institutional integrations, notably its launch of deJTRSY and deJAAA on Stellar and Base, unlocking tokenized U.S. Treasuries and CLOs for DeFi credit markets.

Our Take: Lending markets are healing from the crash, with leverage returning in a disciplined fashion, led by ETH, while liquidity migrates toward the ecosystems offering better yield-to-risk ratios. Ethereum’s outflows are less a warning sign than an architectural success, proof that liquidity is finding its most efficient layer.

Echo Goes Mainstream

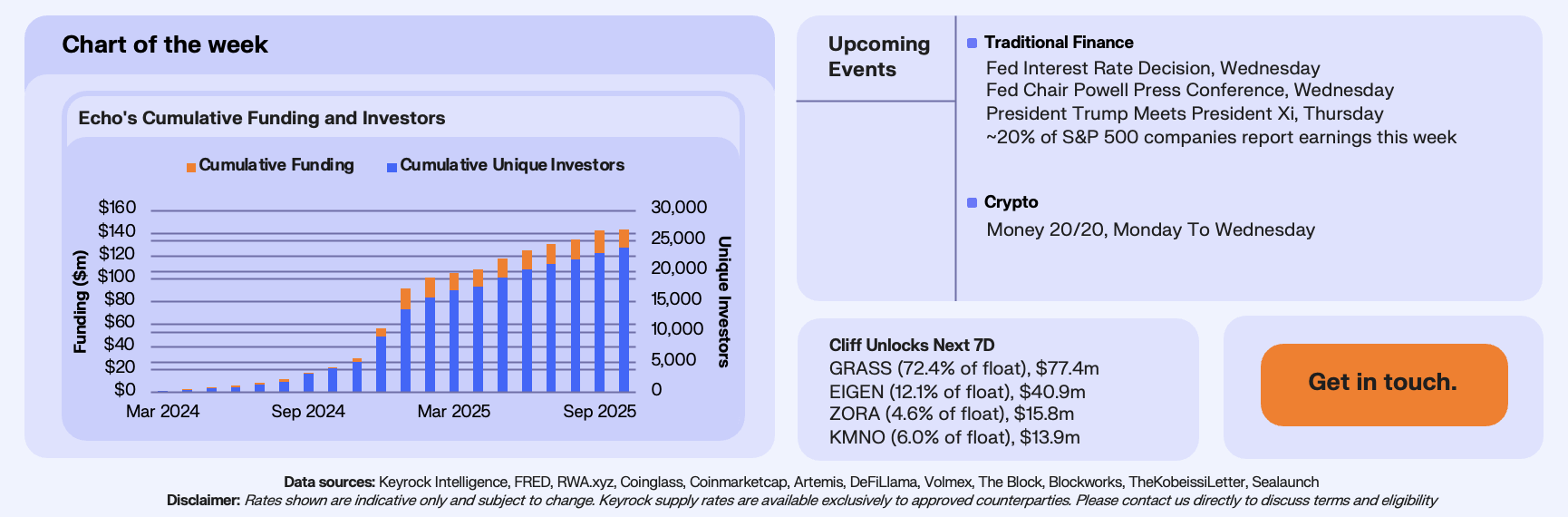

Echo is an early-stage fundraising protocol that allows projects to raise capital transparently from the public while giving investors direct onchain access to early investing opportunities. It bridges the gap between private venture rounds and eventual exchange listings, creating a more open and liquid path to token distribution. Since launch, Echo has raised $143m from nearly 24,000 unique investors, hosting several notable launches, including Plasma’s XPL earlier this year. Echo is emerging as the signal for mainstreaming onchain fundraising.

Last week, Echo dominated headlines after Coinbase announced its $375m acquisition of the platform, followed by MegaEth’s public sale announcement slated for October 27, one of the largest open fundraises to date. Rather than waiting for projects to mature before listing them, Coinbase is moving upstream, owning the earliest layer of liquidity and shaping how assets are launched and traded across its ecosystem. We believe Coinbase’s broader strategy is to control the full token lifecycle, from fundraising to exchange liquidity, while reframing early-stage access around transparency and open participation. For users, the acquisition opens the door to more high-quality projects and broader participation, but also tighter competition for allocations as Coinbase’s large user base joins the platform. The trade-off skews positive, with greater visibility, cleaner fundraising rails, and stronger post-launch liquidity, though Echo’s integration into a major exchange ecosystem will likely reshape its user dynamics and fundraising cadence.

Our Take: Echo’s acquisition can mark a shift in how major token launches will be shaped going forward. For years, early-stage investing happened behind closed doors; now, those rounds are beginning to move onchain, visible and accessible to a broader audience. Echo represents that transition from private capital to public coordination. If it succeeds under Coinbase, it could set the template for how new assets are discovered, distributed, and traded.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.