The $400T Future of Tokenised Assets

Written by Amir Hajian

Read the full report

Preface

Tokenisation solved issuance. Every major asset class now has a representation on a public blockchain, backed by the largest asset managers and custodians in the world. But putting an asset onchain is not the same as making it trade, compose, and settle like a financial instrument. Distribution is the next phase, across a global asset market exceeding $400 trillion.

What follows is a 60+ page in-depth report written with Securitize, featuring insights from contributors across the tokenised asset, crypto, and TradFi landscape, including rwa.xyz, Centrifuge, Euler, Maple, and Midas.

Introduction

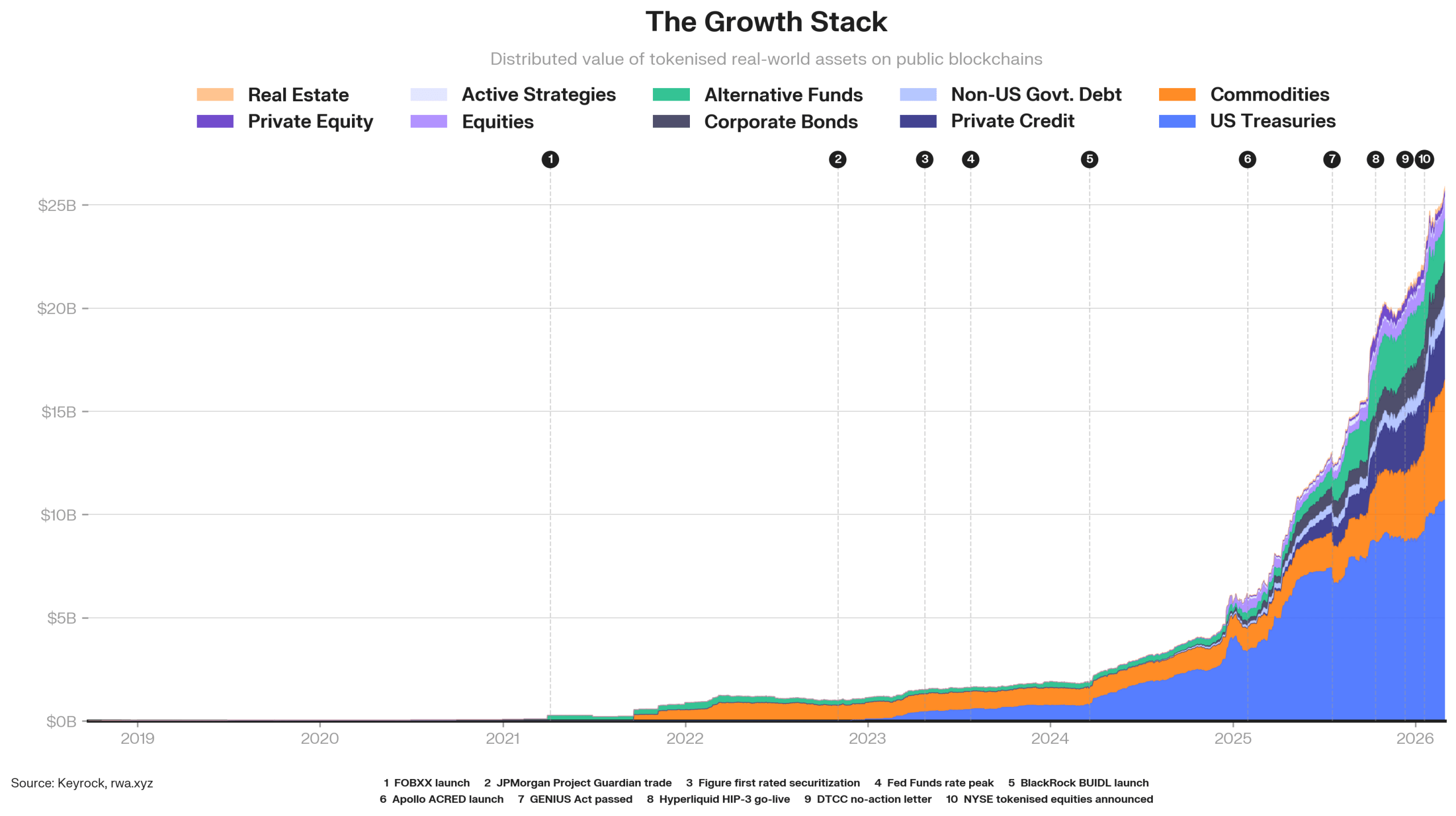

Tokenised assets on public blockchains have crossed $27 billion in transferable value. Government debt, private credit, equities, commodities, and alternative funds all sit onchain, with BlackRock, Apollo, Goldman Sachs, and JPMorgan committing capital and infrastructure.

However, penetration against traditional markets remains below 0.1% for every asset class. Most tokenised products are minted, allocated, and held. They sit on a single platform, available to a narrow set of investors, on a handful of chains, with thin secondary markets. The infrastructure needed to turn a tokenised asset into a functioning financial instrument—price discovery, market making, compliant secondary transfers, composable collateral—barely exists at scale.

This report maps that gap in three parts. We explore what exists today across five asset classes, which of those assets are structurally ready to scale, and what infrastructure is arriving over the next eighteen months to close the distance.

The State of Tokenised Assets

Five sectors define the current RWA landscape. Each solves a different set of inefficiencies in traditional markets, attracts a different buyer base, and has reached a different stage of adoption.

Treasuries

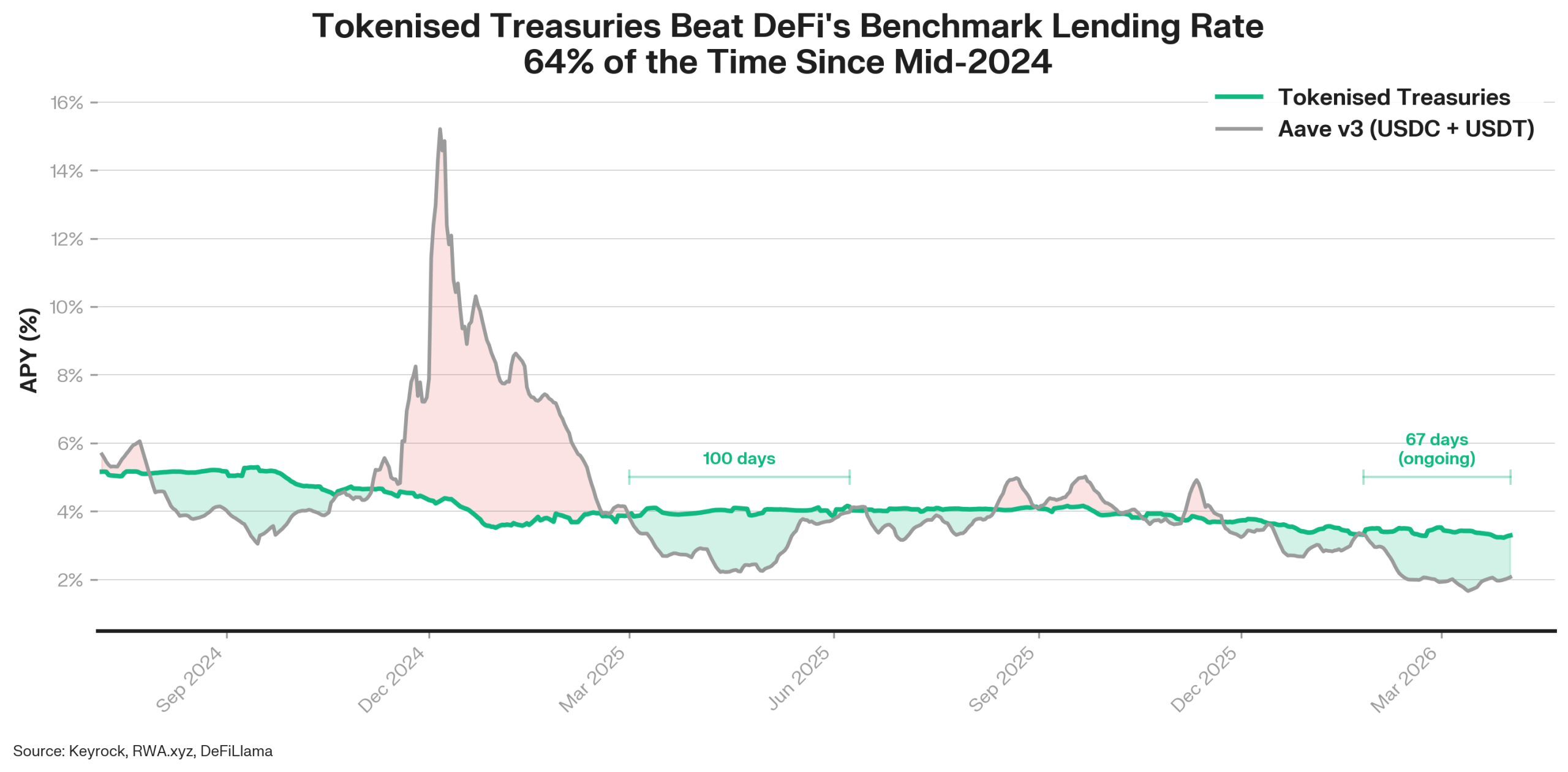

Tokenised Treasuries lead at nearly $11 billion. The value proposition is three things working simultaneously. First, T+0 settlement instead of T+1. Second, daily yield accrual directly to the holder’s wallet. And third, collateral utility, where the same token earning Treasury yield can be posted as margin on Binance and Deribit or deployed into DeFi lending protocols.

Since mid-2024, tokenised Treasuries have offered a higher return than DeFi’s benchmark stablecoin lending rate (TVL-weighted Aave v3 USDC and USDT) on 64% of all days. In Q1 2026, that figure reached 98%. DeFi lending rates ranged from 1.7% to 15.2% over the period. Tokenised Treasury yields stayed within a 3.3% to 5.3% band, with 3.6x lower monthly volatility. For a treasury manager building yield assumptions into a quarterly plan, tokenised Treasuries offer a predictable range.

Private Credit

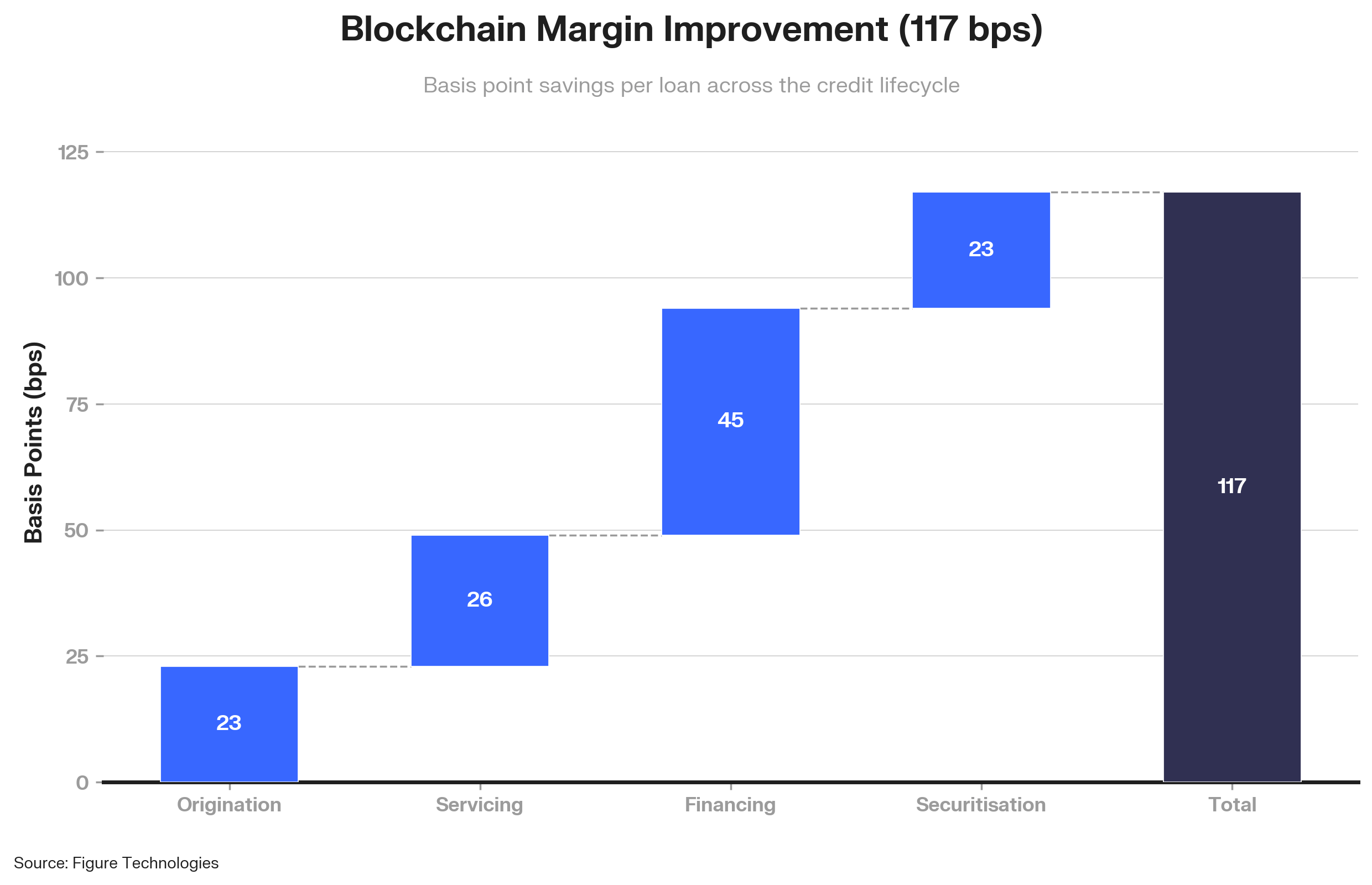

Tokenised credit has reached over $6 billion in transferable value. Blockchain-based origination compresses costs across the entire credit lifecycle. Data shows 117 basis point of margin improvement per loan, spread across origination, servicing, financing, and securitisation.

Applied to the $14 trillion annual securitisation market, that represents $163 billion in potential industry savings. The composability layer adds a second dimension. Maple Finance has grown to $4.1 billion in lending AUM, and 36% of that is actively deployed across DeFi lending and leverage protocols. In traditional private credit, a position is originated and held until maturity. Onchain, the same position generates yield while simultaneously serving as collateral elsewhere. One dollar of deposited capital does more than one job.

Equities

Tokenised equities crossed $1 billion in AUM, up from roughly $15 million at the end of 2024. Distinct tokenisation models now coexist, each representing different claims with different properties:

- Direct tokenisation through transfer agents like Securitize, where the token carries full ownership rights including voting and dividends.

- Indirect models from Backed and Ondo that offer economic exposure through wrapper structures.

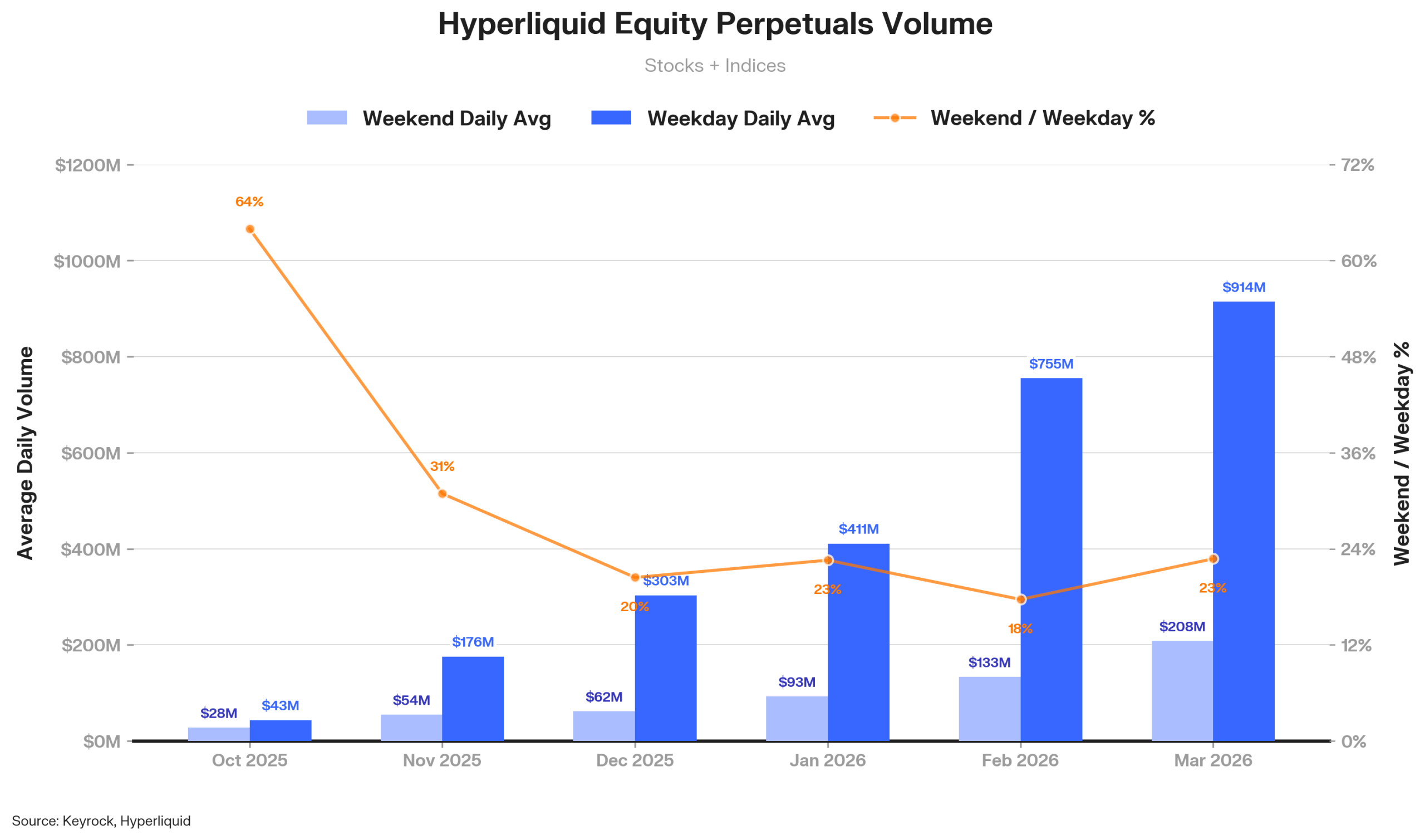

- Perpetual futures, which carry no underlying shares at all but have become the most liquid venue for onchain equity price exposure.

Monthly equity perp volume on Hyperliquid grew from $760 million to $20 billion in under six months, a 26x increase. Weekend trading on these venues provides something traditional markets cannot. A portfolio manager holding onchain equities can short the same asset over the weekend to hedge Monday gap risk while U.S. markets sit closed. The convergence of registered ownership, collateral usage, and round-the-clock liquidity is what positions direct tokenisation as the structural endgame for equities.

Commodities

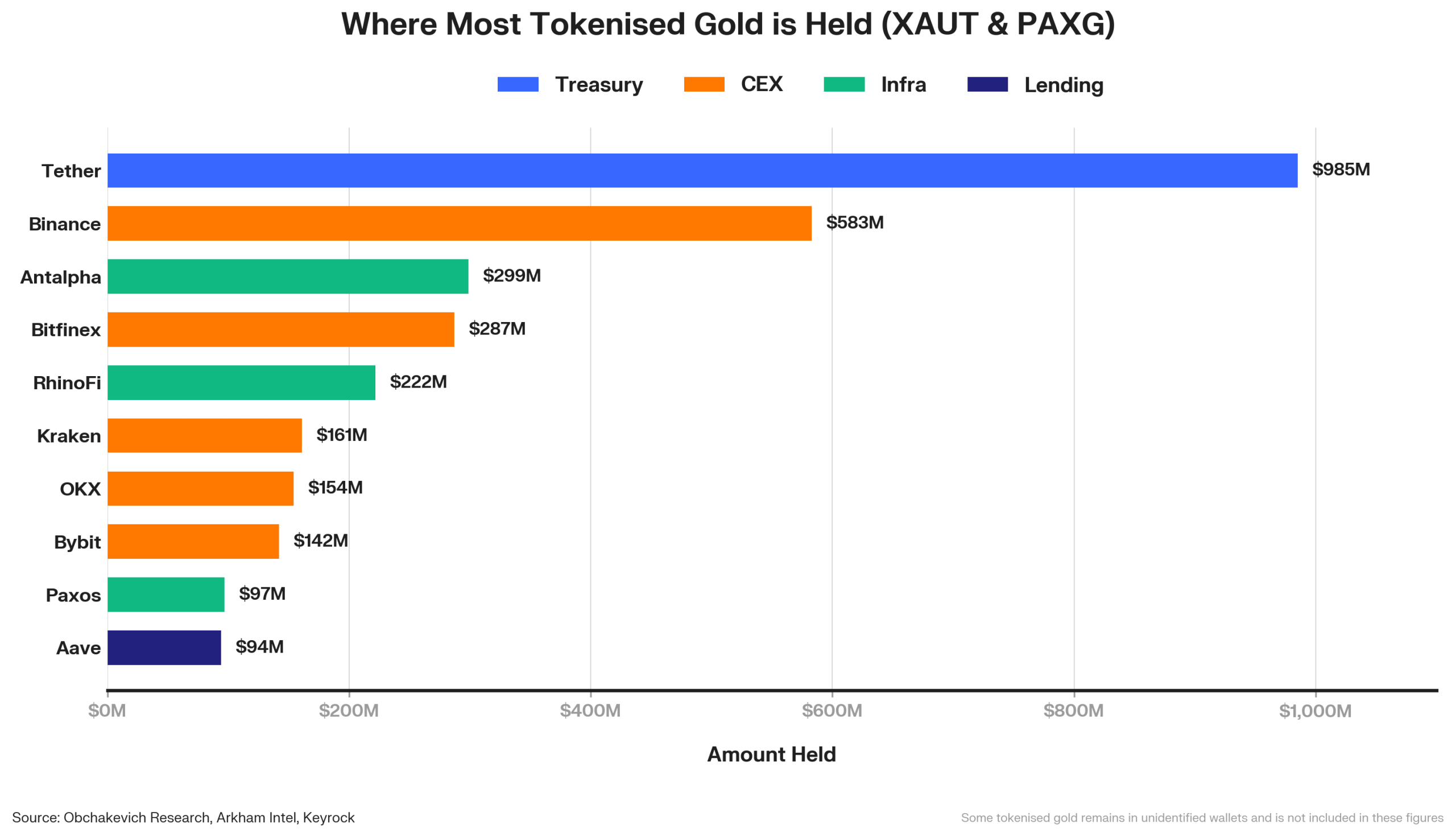

Tokenised commodities have grown to $9.36 billion, a 7x increase year-over-year. Gold accounts for $5.9 billion through PAXG and XAUT. Agricultural tokens now account for $3.1 billion and tokenised diamonds nearly $300 million.

Onchain data reveals how tokenised gold is actually being used. Corporate treasuries hold it as a macro hedge and reserve diversification tool. Centralised exchanges custody it across spot markets, margin accounts, and yield products. Infrastructure providers use it as collateral for institutional lending. And DeFi protocols accept it for borrowing stablecoins against gold exposure. Tokenised gold is functioning across the full spectrum from passive reserves to active collateral.

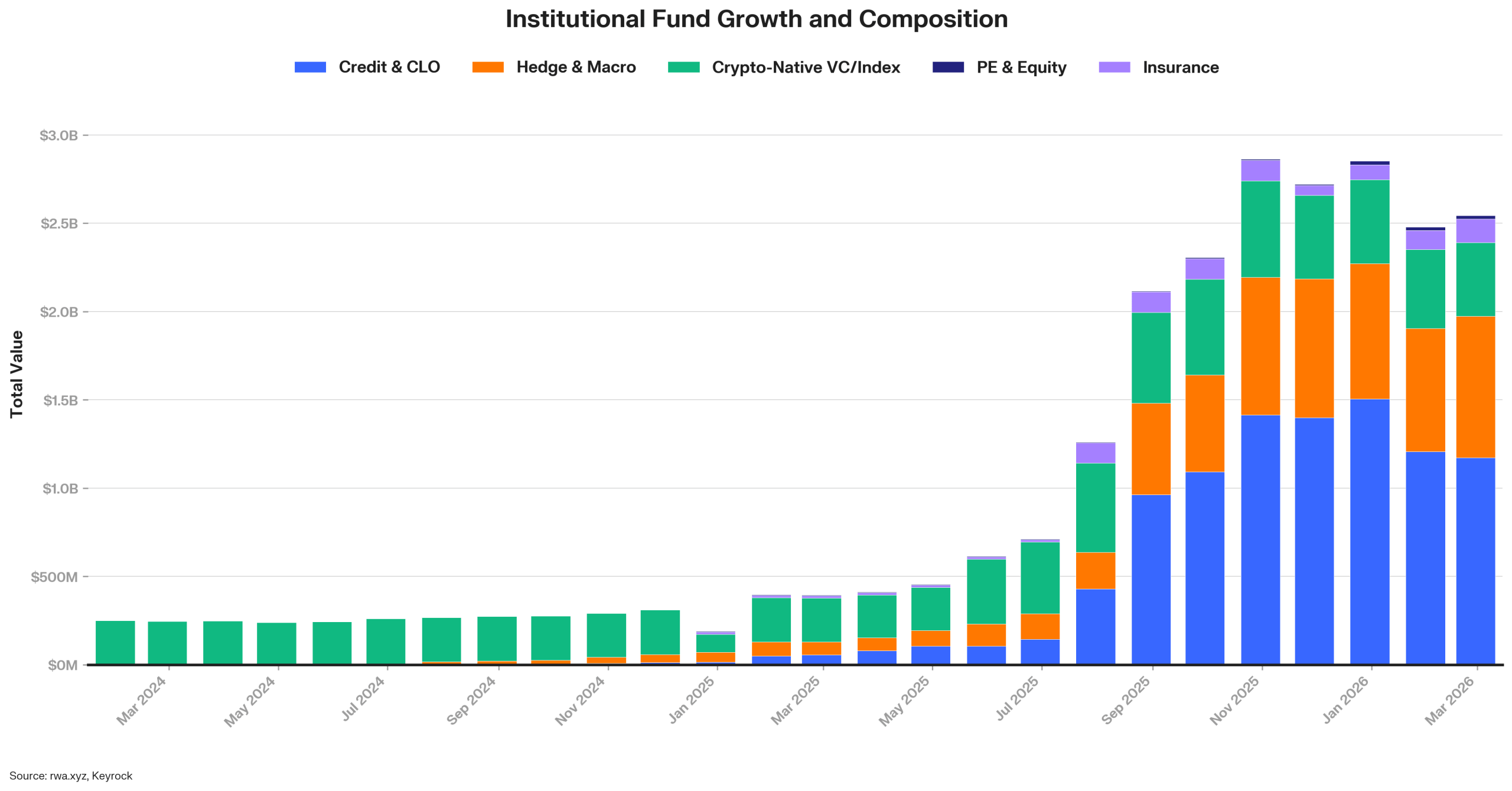

Alternative Funds

Institutional alternative funds expanded from $185 million in January 2025 to $2.56 billion by March 2026, a 13x increase in fourteen months. The composition has broadened rapidly. Credit and CLO strategies account for $1.2 billion, nearly half the market, anchored by Janus Henderson’s tokenised AAA CLO fund on Centrifuge at $739 million. Hedge and macro strategies hold $804 million. Crypto-native VC and index products contribute $419 million. Insurance and PE round out the rest. 36 products now span strategies that would have been unrecognisable onchain a year ago, from AAA-rated CLOs to reinsurance to crypto basis trades. The top five funds account for 61% of AUM, but the tail is growing.

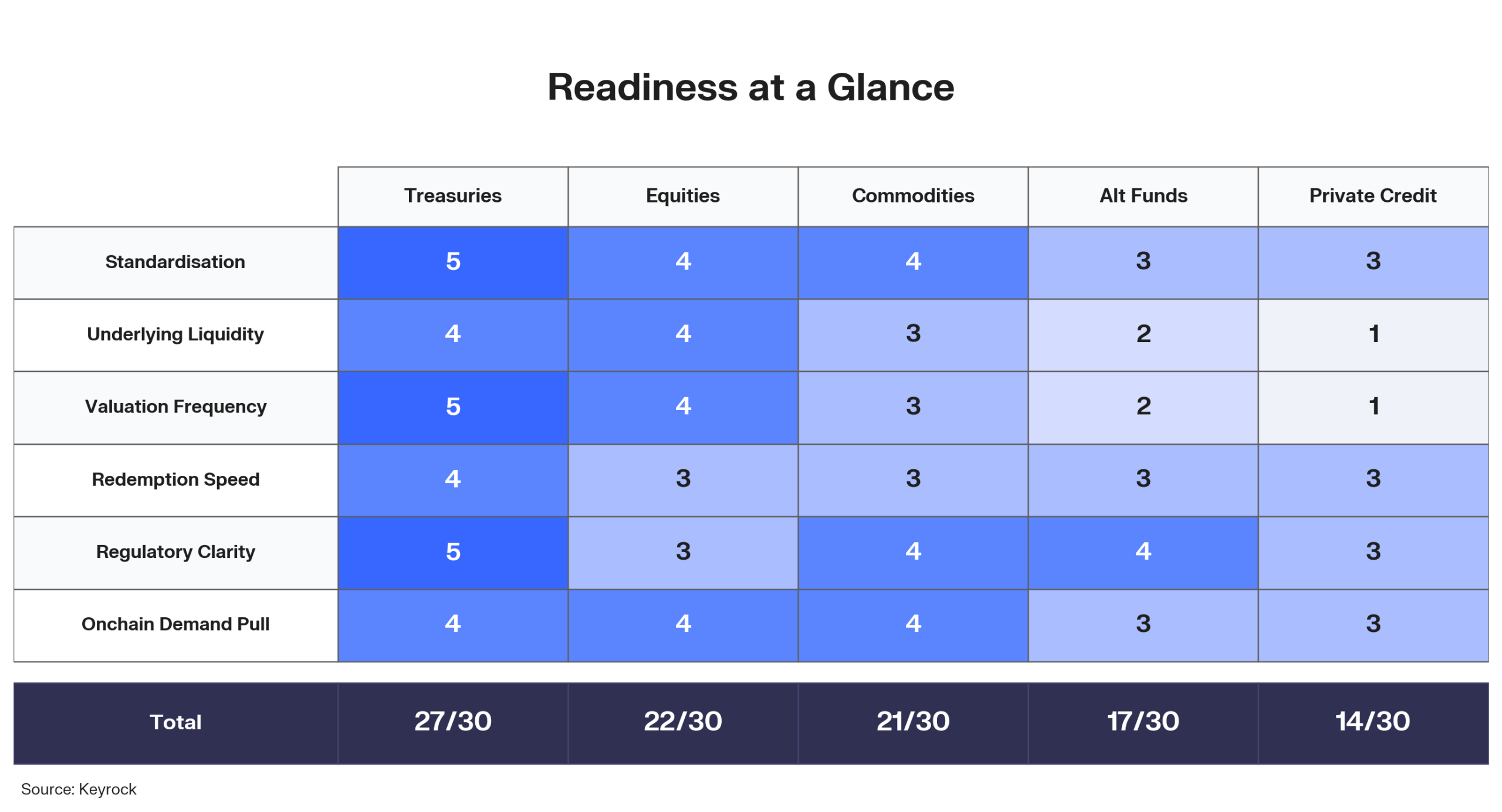

Which Assets Scale Onchain Fastest

A U.S. Treasury bill is perfectly fungible, prices in real time, and redeems same-day. A private credit facility is bespoke, priced quarterly, and locks capital for months. Tokenisation does not override these underlying properties.

The report scores five asset classes across six structural factors: standardisation, underlying liquidity, valuation frequency, redemption speed, regulatory clarity, and onchain demand pull. Each factor captures what the traditional market provides as a foundation, what onchain infrastructure enables today, and where the trajectory points.

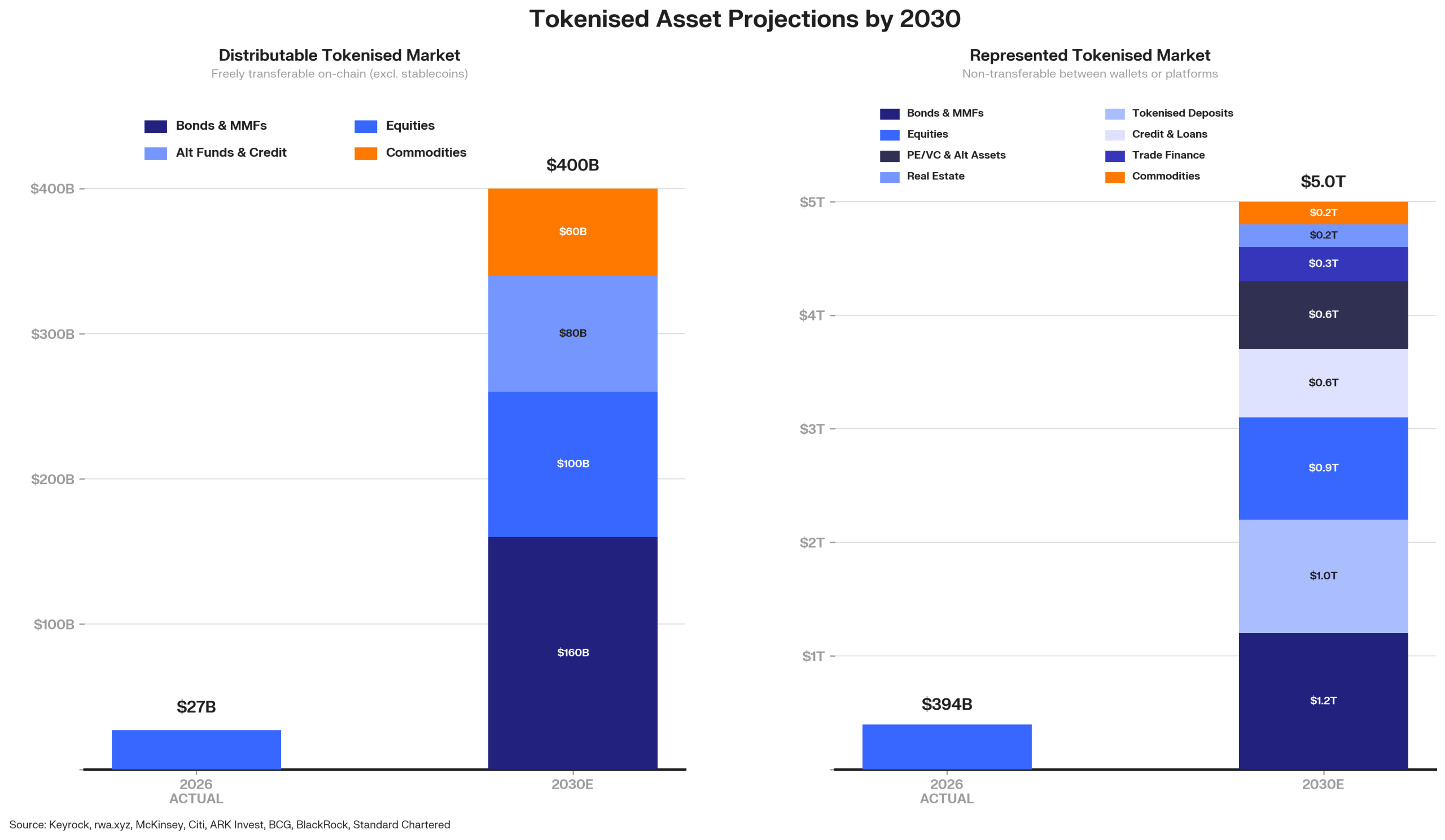

The Scaling Ahead

Our base case sees the transferable RWA market expanding from $27 billion to $400 billion by 2030, while the broader represented market: assets tracked on public blockchains but not yet freely transferable, reaches $5 trillion.

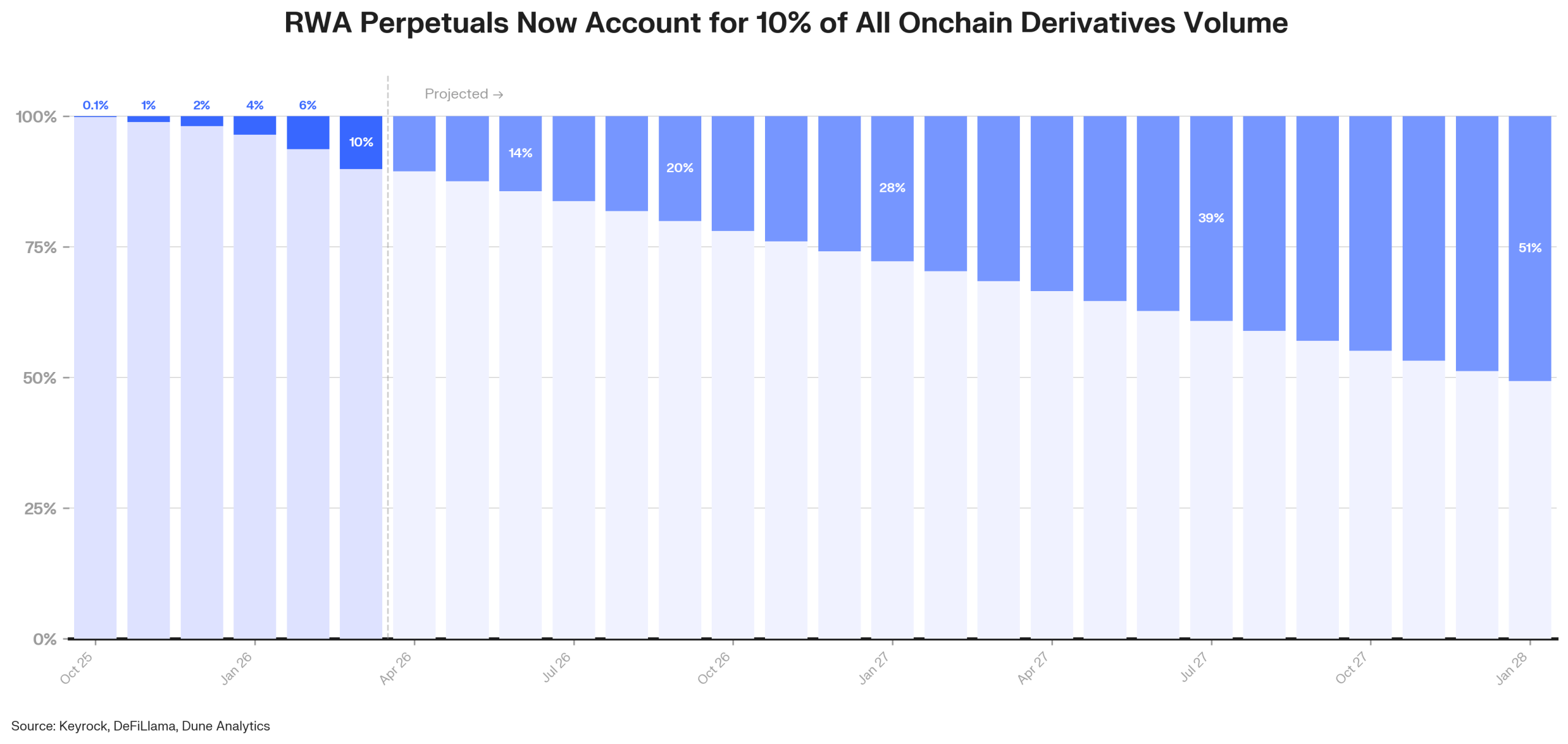

Perpetual futures have become the fastest-growing distribution channel for real-world asset exposure onchain. In October 2025, RWA perps accounted for 0.1% of all onchain derivatives volume. By March 2026, that figure reached 10.1%. Total RWA perps volume hit $67 billion in March across venues. At the linear growth rate observed over the past six months, RWA perpetuals could account for 50% of onchain derivatives volume by January 2028.

The Infrastructure Gap, and What Closes It

Four of five asset classes have more than 89% of their value concentrated in the top five wallets. Fewer than one in twenty Treasury or alternative fund holders transact monthly. Billions in tokenised assets sit onchain with almost no secondary market activity around them.

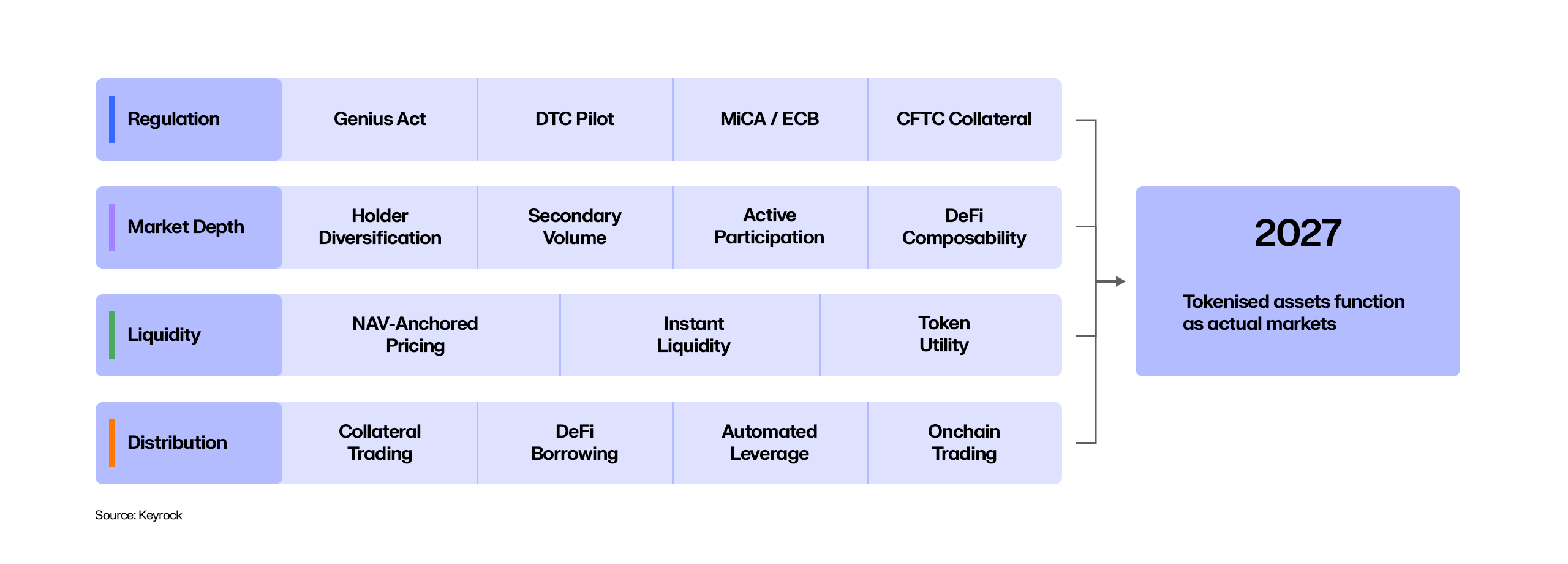

Regulation, liquidity, and distribution are all advancing on overlapping timelines to solve for RWA growth. The GENIUS Act hardwired demand for tokenised Treasuries into stablecoin reserve requirements. The CFTC cleared tokenised securities as margin collateral. The ECB began accepting DLT-based assets for Eurosystem credit operations. The UK is piloting tokenised sovereign gilts as the sole legal record of ownership.

2027 is the first period where all four forces mature together. For most of the past three years, at least one was clearly lagging. Infrastructure existed, but regulation had not caught up. Regulation turned permissive, but distribution remained early. The sequential dependencies that constrained the market are beginning to break.

The issuance era answered whether tokenised assets could be created. The distribution era will answer whether they can be traded, collateralised, borrowed against, and composed across the protocols and venues where onchain capital already sits. That answer will take shape over the next eighteen months as the infrastructure examined in this report reaches broader adoption.

For media or press inquiries, or questions related to data and methodology, please contact [email protected]

Get ahead of the next move

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.