1 December 2025

Key Insights: Stuck in the Chop

Markets Price Earlier Easing

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

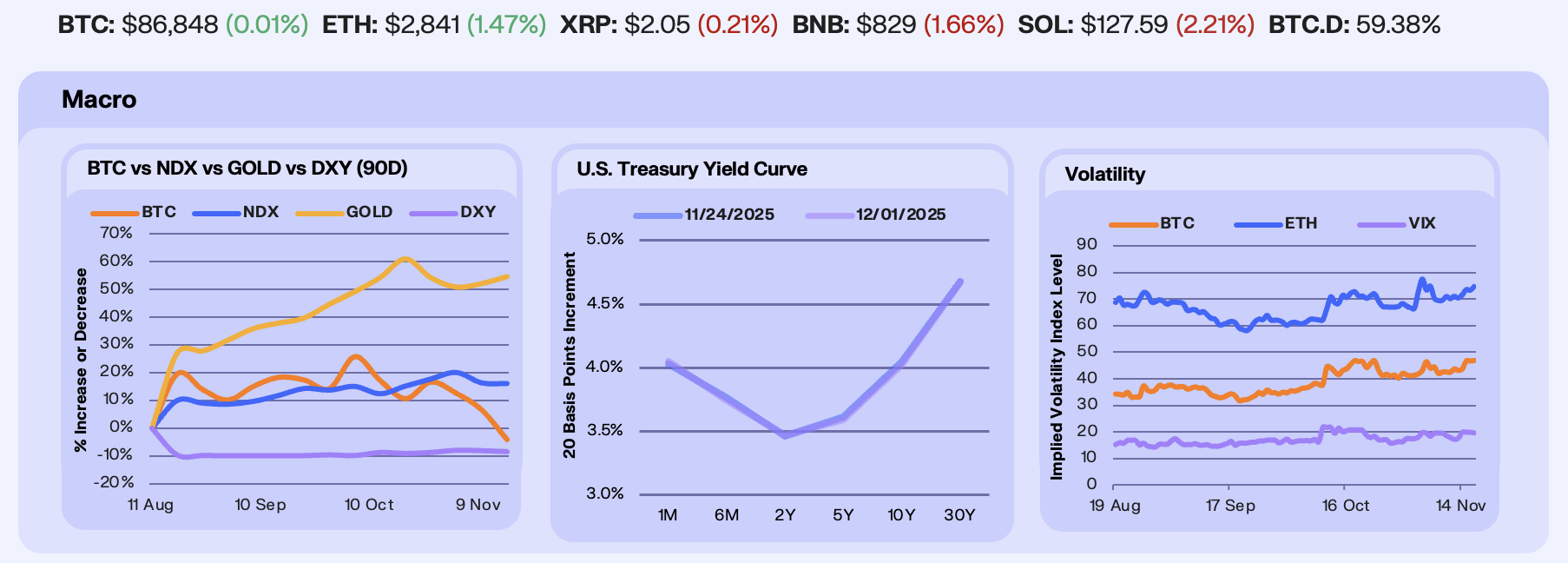

Dovish Fed remarks lifted markets last week as December cut odds jumped, but crypto retraced into Monday’s open. BTC fell –0.3%, Gold added 2.7%, and the NDX gained 4% amid light holiday flow. The DXY eased –0.5% with traders pressing early-cut expectations.

Treasury yields drifted lower across the curve last week, led modestly by the long end. The 10Y slipped 2 bps to 4.02%, while the 30Y dropped 1 bp to 4.67%, leaving the curve slightly flatter. The move reflects markets pricing in a further Fed cut in 2025 as December’s rate cut odds hit 88%, helped by Fed officials signaling that rate cuts are now a viable response to labor-market softness and that inflation is no longer the primary risk. The market is now trading the Fed’s pivot more confidently, which keeps long-end Treasuries bid and lowers the hurdle for risk assets.

Volatility bled materially into the holiday. BTC 30D ATM IV dropped 14% to 46, ETH IV fell 10% to 69, and the VIX slid 21% to 18. Dealers noted a broad pullback in near-term hedging flows as reduced trading activity and lower realized vol pulled implieds down with it. Volatility has now flipped back into a normal structure after one of the sharpest spikes we’ve seen this year.

Our Take: Last week’s moves were driven more by thin liquidity, volatility supply, and dovish Fed rhetoric than by any material shift in growth expectations. BTC still screens attractive at these levels as ETF flows stabilize and the Fed inches toward easing, but a decisive rebound will likely require firmer macro confirmation. Equity valuations remain stretched, revenue expectations are starting to feel the drag of softer data, and global debt pressures keep the broader backdrop fragile.

Crypto Stuck in Consolidation

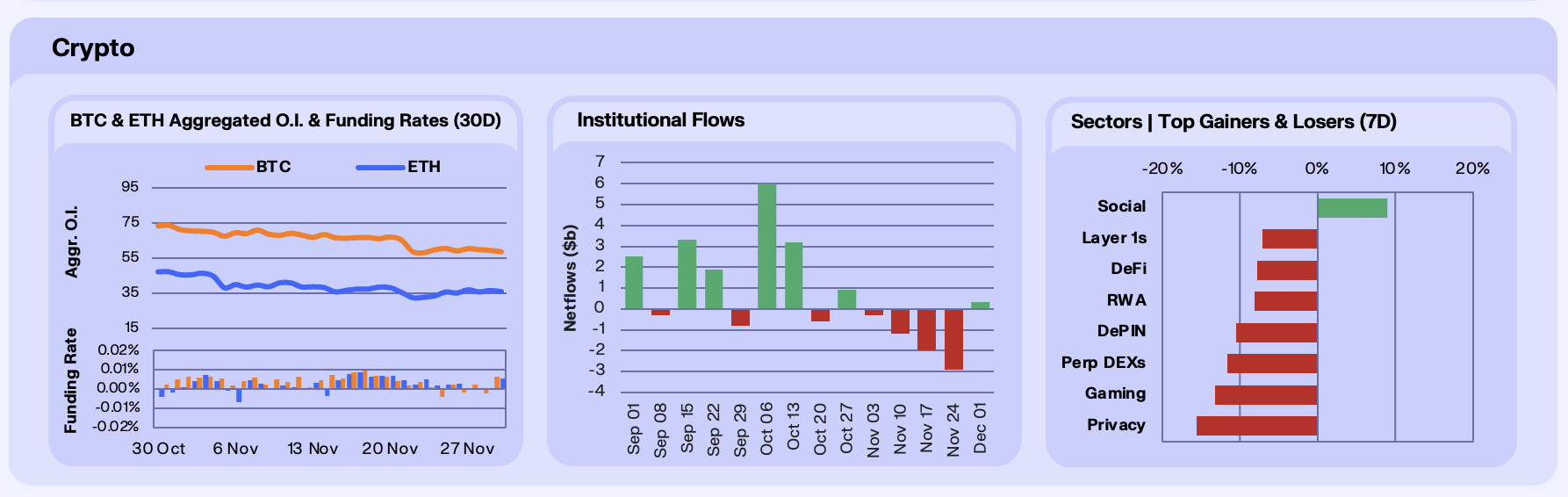

BTC open interest held steady at $59b this week muted despite the broader risk-on tone leading into the weekend, while ETH OI climbed 7% to $36b. BTC OI is still 33% below the October 10th peak and sitting near where it began 2025, underscoring how cautious leveraged participation remains. Funding flipped back to neutral with cleaner leverage across majors, but despite setups looking constructive, crypto continues to trade in step with the Nasdaq. Equity valuation concerns are still capping directional appetite and keeping the space from breaking higher with conviction. Institutional flows finally stabilized, with digital asset investment products seeing $349m of net inflows after four straight weeks of selling. November still closed with BlackRock’s Bitcoin ETF dumping $2.2b, its largest monthly outflow on record, but this week saw a clear shift as buyers returned. The bulk of demand came from Ethereum products, which drew $130m of inflows and briefly pushed ETH back above $3,000 heading into the weekend before giving up the level on Sunday. After several weeks of heavy redemptions, digital assets appear to have reached a consolidation zone where incremental inflows are starting to matter again.

Sector performance skewed weaker on the week, with Social the only segment to finish in the green at 9% as flows rotated toward event-driven names. Perp DEXs declined 11.6%, led by Hyperliquid where supply dynamics remain a headwind; roughly 270m tokens unlocked on Nov. 29, 2024, the largest airdrop in history at today’s market value of $9b, and that overhang is still being digested. Privacy fell 15.6%, marking the worst performance of the group as the recent Zcash rally lost momentum and near-term enthusiasm faded.

Our Take: Crypto continues to trade without conviction, with BTC fading into Monday and liquidity thinning into year-end. The broader market has yet to establish a durable bid, and participation remains light as investors stay focused on macro signals and the Fed’s trajectory. With positioning subdued and no clear catalyst on the near horizon, the near-term setup still favors a range-bound tape rather than sustained upside.

Onchain in Reset Mode

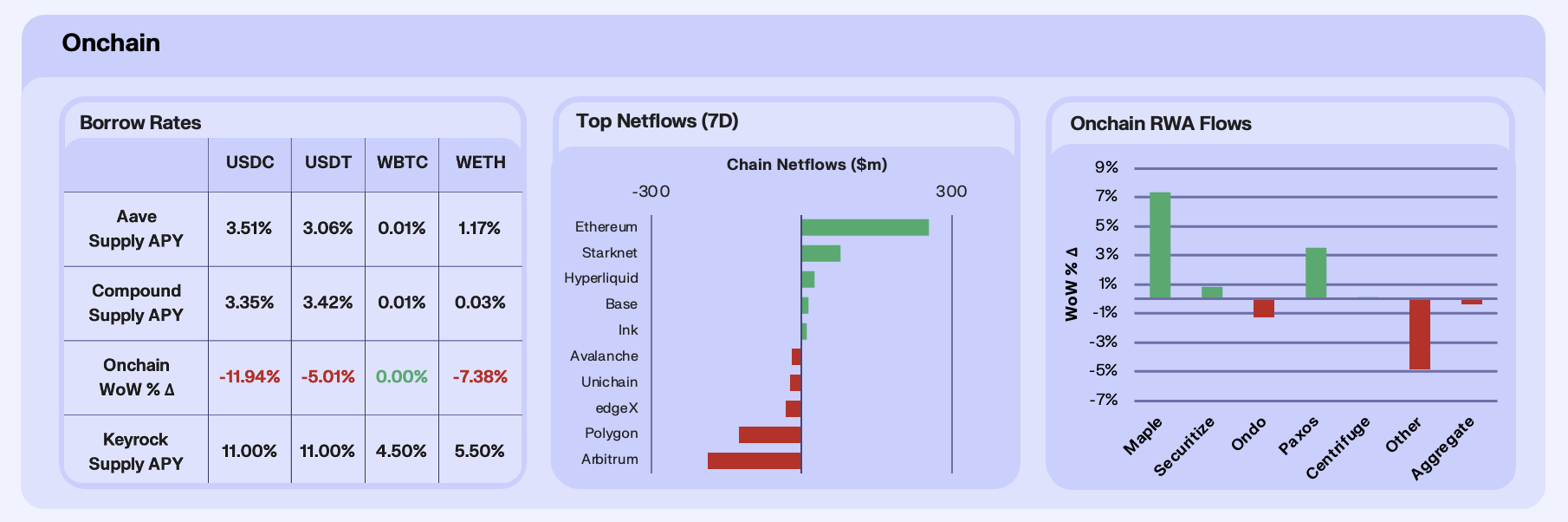

Onchain lending markets softened again this week as crypto participants remained firmly defensive. Stablecoin yields continued to drift lower, with USDC and USDT supply APYs falling 11.9% and 5.0% WoW on Aave. Interestingly, USDC supply APY rose 7.5% WoW, while USDT, WBTC, and WETH all declined, pointing towards a fall in borrow demand as the driver for lower rates. Lenders continue to park capital onchain, but demand for leverage-driven borrowing remains subdued as volatility stays elevated.

Chain netflows were more dispersed than we’ve seen in previous weeks. Ethereum led with over $308m in net inflows, reversing months of outflows. StarkNet also posted a strong $77.7m inflow, benefiting from the privacy narrative and its close connection with Zcash. Hyperliquid flipped positive with $44m in inflows, following last week’s unwind, supported by resilient perps demand. In contrast, Arbitrum, down $220 and Polygon, down $143m, saw outflows as capital shifted toward chains offering near-term catalysts. The flows reflect a market redistributing liquidity in a narrative-driven market that’s searching for positive catalysts.

RWA flows were broadly stable, with aggregate AUM down just -0.35% WoW despite macro softness. Performance varied beneath the surface, with Maple leading with a 7.3% gain as institutional credit demand stayed firm amid a narrative recovery from last week’s Core incident, while Paxos gained 3.5%. Securitize was modestly positive, whereas Ondo, down 1.3%, saw a pullback tied to rate expectations and rotation within RWAs. Overall, the sector continues to show resilience and remains one of the more structurally supported areas of onchain activity.

Our Take: Onchain activity is behaving exactly as expected in a late-stage correction. Rates are easing, flows are rotating into higher-quality ecosystems, and RWAs are holding ground aside from idiosyncratic protocol shifts. With leverage largely flushed out and capital positioning defensively, the setup into December is cleaner than headline prices imply.

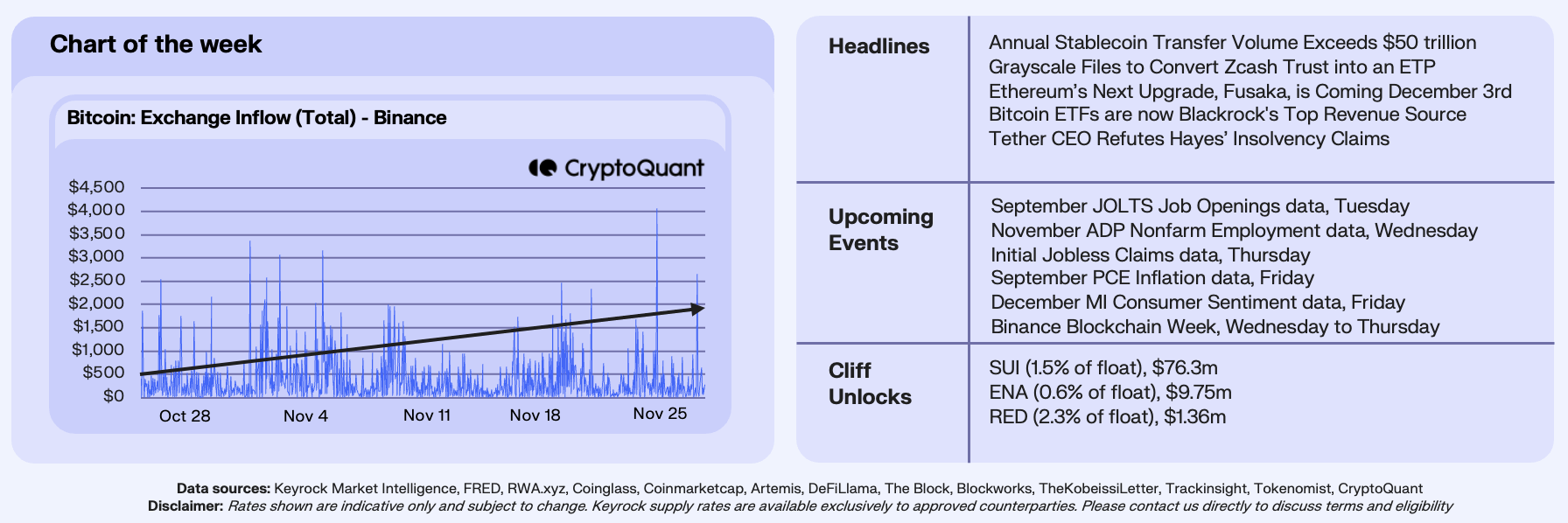

Binance’s BTC Drain

This week’s chart, courtesy of our collaboration with CryptoQuant, tracks hourly Bitcoin inflows to Binance, the world’s largest crypto exchange. The data reveals a sharp uptick in these inflows since mid-November, coinciding with Bitcoin’s price falling from $120k to a seven-month low around $87k. Notably, the average deposit size on Binance has surged from 12 BTC at the start of November to as high as 37 BTC in recent weeks, with large deposits, at 100 BTC or more, accounting for about 45% of total inflows, highlighting increased activity from whales and institutional players.

This trend suggests we have seen mounting selling pressure from major holders who were offloading Bitcoin during the recent market downturn, potentially exacerbating price declines if the pattern persists. It indicates a shift in sentiment among long-term investors, who may be capitulating or hedging against further volatility. This offloading of large sums of Bitcoin is clearly steepening the market hill that Bitcoin needs to climb to recovery, however a reversal may hint at stabalising demand and result in a V-shaped recovery for the orange coin, should the macro environment comply.

Our Take: We’re monitoring this closely as it underscores the influence of large players in driving market cycles, but it often precedes bottoms if retail starts accumulating. In collaboration with CryptoQuant, we see this as a cautionary signal for short-term traders to tread carefully, though it could present buying opportunities for those with a longer horizon.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.