12 January 2026

Key Insights: Stuck in Neutral

Calm With Caveats

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

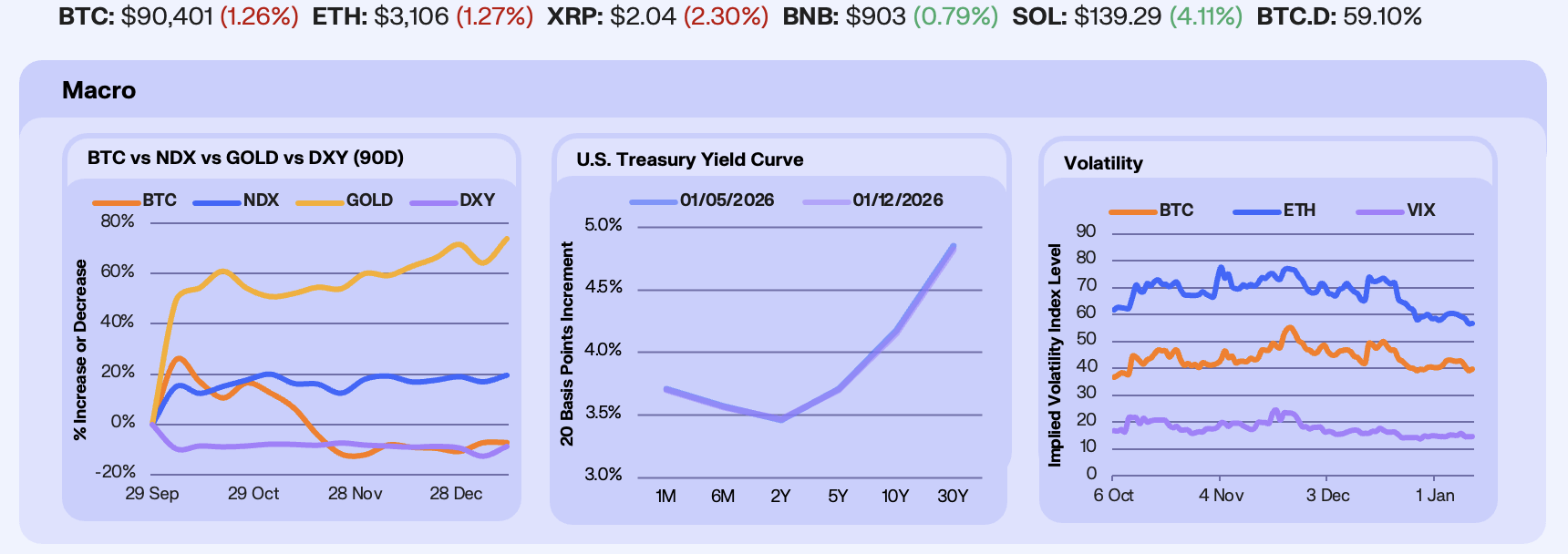

Markets largely shrugged off geopolitical risk this week, even as tensions added another layer of uncertainty to energy markets and commodities extended their rally. A resumption of official US economic data pointed to robust growth, cooling inflation, and a softening labor market. Against that backdrop, price action was relatively positive: BTC held +0.1%, Gold advanced +5.9% to a new all-time high, NDX rose +2.2%, and the DXY strengthened +0.4%. Commodities once again drew attention, supported by macro and geopolitical crosscurrents, while risk assets continued to grind. Rates markets reflected this cautious balance. Treasury yields edged slightly lower across most of the curve, with front-end rates down ~1 bp and the long end lower by ~2–3 bps, leaving the curve broadly unchanged. US job openings plunged in November, with 685k fewer openings than unemployed workers, the largest gap since March 2021. Despite that shift, rate cut expectations remain restrained, with markets pricing a 96% probability of no change in January and 69% odds of no move in March.

Volatility was modestly lower across assets. BTC ATM 30-day implied volatility fell -8% to 40, ETH IV declined -6% to 56.5, while the VIX dropped +4%. This built a favorable volatility risk premium in crypto, particularly as recent upside attempts suggest momentum may finally be returning after a prolonged period of underperformance versus other risk assets. Despite this, overall volatility remains historically subdued, underscoring how little conviction is currently embedded in price action.

Our Take: Markets continue to trade without strong conviction, with tight ranges reflecting caution ahead of key macro data and catalysts. While growth is slowing and labor conditions are cooling, policy expectations remain finely balanced, leaving investors hesitant to lean aggressively in either direction. With uncertainty lingering and positioning light, the upcoming earnings season may prove decisive in breaking the current stalemate and restoring directional clarity across risk assets.

Risk Appetite Stabilizes

Derivatives positioning remained restrained despite a modest January rebound in spot. BTC open interest rose +4.3% WoW, while ETH OI slipped -4%, underscoring a divergence between BTC-led positioning and broader risk appetite. Funding rates stayed constructive but not euphoric, suggesting leverage is being added selectively rather than chased aggressively. Notably, options markets continue to express optimism further out the curve, with traders increasingly targeting $100,000 BTC call options on Deribit.

Institutional flows remained under pressure this week, with net ETF outflows concentrated in Bitcoin and Ethereum products. Bitcoin ETFs saw roughly -$680m in net outflows, while Ethereum products recorded approximately -$69m, bringing total digital asset ETF redemptions to over -$700m on the week. Outflows were led by larger vehicles, including IBIT and ETHA, while activity elsewhere remained muted. Despite the near-term softness, aggregate AUM remains elevated suggesting institutions continue to manage exposure tactically rather than exit the space outright as markets consolidate.

Sector performance narrowed this week, with gains concentrated in a handful of attention-driven narratives. DePIN (+2.0%), Privacy (+1.5%), and Bridge (+1.1%) outperformed, with privacy, led by Monero and Zcash, once again showing relative consistency as other sectors faltered. Elsewhere, weakness was broad, led by RWAs (-11.1%), Memecoins (-8.7%), and Layer-1s (-8.0%), underscoring a market where capital is rotating toward narratives with sustained attention while the broader complex continues to grind lower.

Our Take: Altcoin markets are showing signs of base-building. Buyers are stepping in on weakness, while rallies continue to meet supply, leaving price action range-bound rather than directional. This is typically the phase where external catalysts set the tone for the next move. Until then, the recent push higher in BTC toward the mid-$90k range appears to be loosening risk constraints, allowing select altcoin segments to regain traction even as broader conviction remains restrained.

Subtle Onchain Improvement

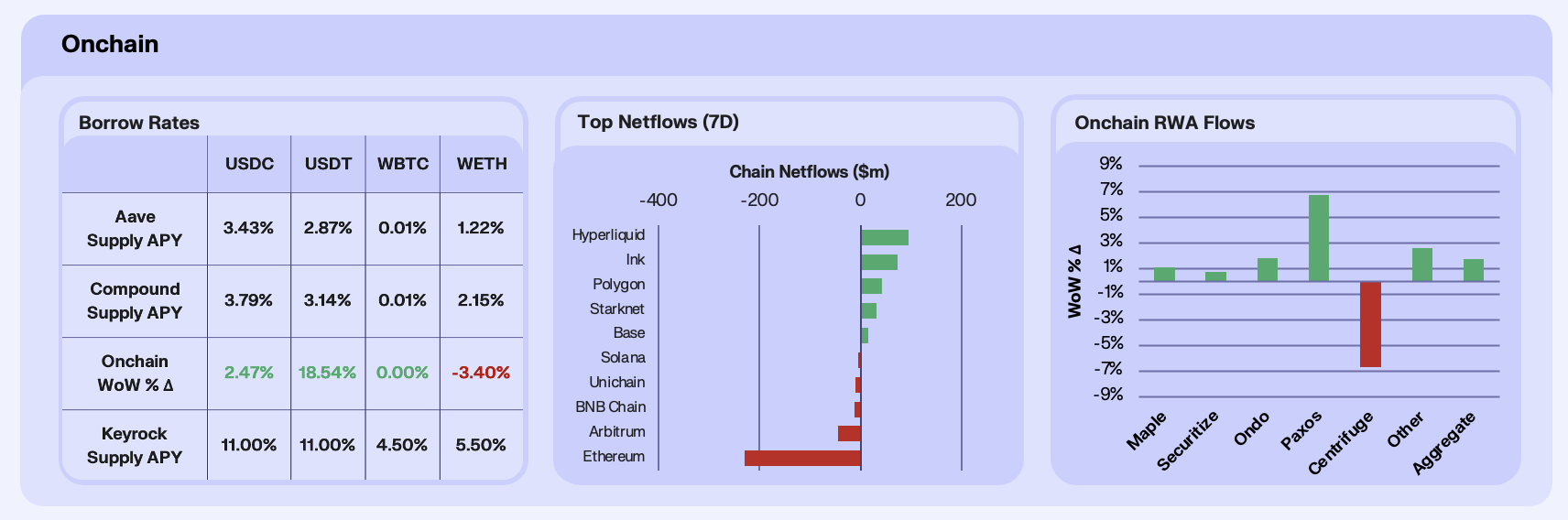

This week, we saw onchain rates firm modestly, signalling a continued shift away from December’s defensive positioning. Stablecoin yields edged higher on a WoW basis, with USDC up 2.5% and USDT up a staggering 18.5%, pointing to improving utilisation as capital cautiously rotated back into onchain activity. Beneath the headline move, however, liquidity dynamics remain nuanced. On Aave, supply declined across all major assets, most notably USDT (-9.2%) and USDC (-6.2%), suggesting that higher rates were driven more by reduced liquidity, with capital rotating either up the risk continuum, or offchain altogether. The key point here being that this was not a meaningful resurgence in borrowing demand alone. Borrowing conditions for volatile assets remained muted, with WBTC flat and WETH rates drifting lower.

Looking at liquidity flows between chains, we see a clear rotation towards volatility and execution venues, reinforcing this shift towards onchain engagement. Chain netflows reflected a clear rotation toward volatility and execution venues. Hyperliquid stood out with a sizable +$151.5m inflow, consistent with renewed speculative engagement as traders repositioned into leverage-heavy perps following recent consolidation. In contrast, Ethereum saw a notable -$253m outflow, extending recent weakness likely tied to institutional rebalancing and L2 migration.

RWA flows were modestly positive at the aggregate level (+1.75% WoW), spurred on by Paxos (+6.8%), which drew capital as institutions rotated into regulated RWA exposures with year-end positioning and attractive tokenised treasury yields. Ondo (+1.8%) and Maple (+1.1%) also saw inflows, with the catalyst being Bitget Wallet’s expanded onchain equity and tokenised securities offerings, including over 200 tokenised U.S. stocks integrated on January 8th. Securitize (+0.7%) posted modest gains, while Centrifuge (-6.7%) lagged, consistent with flows favouring more liquid, standardised RWA structures over less fungible assets.

Our Take: Onchain conditions are continuing to improve at the margin. Rising stablecoin rates alongside falling supply point to cautious re-engagement, while chain flows show capital rotating selectively into volatility and execution venues rather than core settlement layers. RWAs continue to act as a stabilising anchor, benefiting from yield demand and regulatory clarity. This appears to still be early-year positioning and liquidity normalisation.

Stablecoin Spend Flywheel

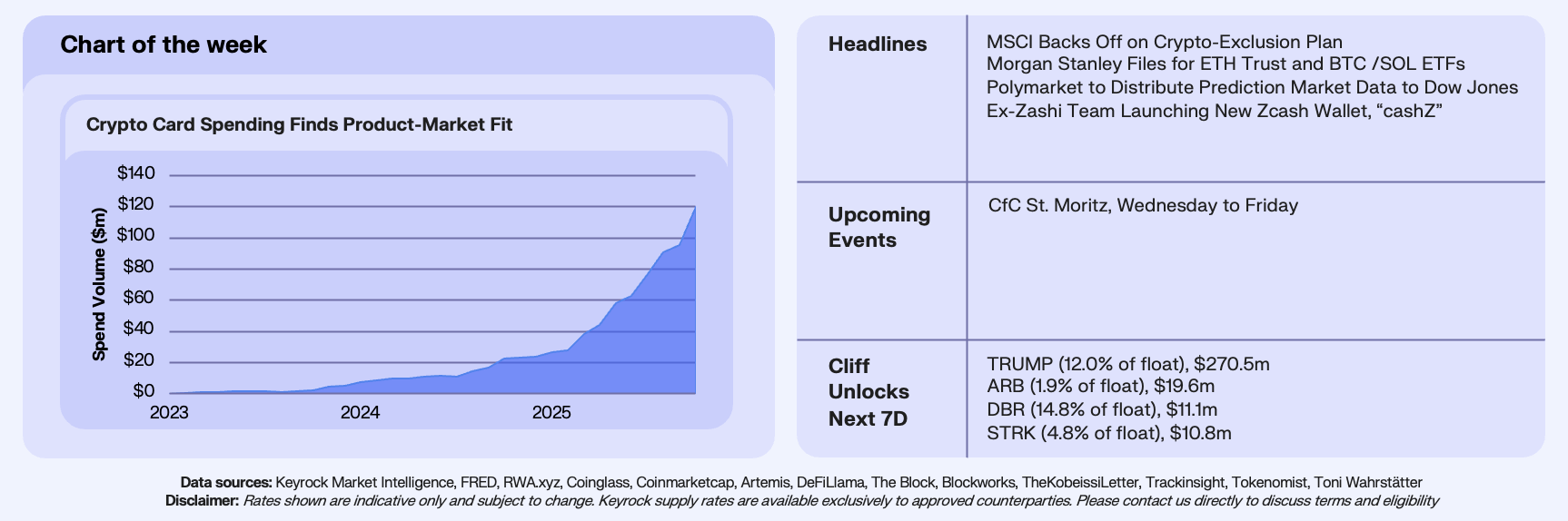

This week we’ll be highlighting a chart from our heavily anticipated ‘12 Charts to Watch in 2026’ article, being released in collaboration with Dune this week. The chart shows monthly spend volume processed through crypto-linked payment cards, using data queried from Dune by @obchakevich. Since early 2023, card volumes have grown from effectively zero to a meaningful consumer payments rail that exceeded $100m by EOY 2025. The acceleration becomes particularly striking from 2025 onward, with monthly spend rising from roughly $17m at the start of the year to over $120m by December, representing a >6x expansion in under 12 months.

Crypto cards sit at an intersection of onchain infrastructure and real-world utility. They allow users to spend crypto and stablecoin balances without changing behaviour, making them one of the lowest-friction onboarding vectors into crypto today. While the user experience looks familiar, the backend is fully crypto-native, powered by stablecoins, wallets, and blockchain settlement rails, thus also acting as a capital influx mechanism for stablecoins. The sharp inflection in spend during 2025 suggests this model is resonating, particularly as UX improves and cards are increasingly embedded directly into wallets.

Our Take: Our desk sees crypto cards as one of the most underappreciated demand drivers in the ecosystem. Despite explosive growth in 2025, this vertical still feels early. Looking into 2026, we expect spend volumes to compound again, with monthly card spend reaching at least $500m at some point during the year, and exiting 2026 at a $200m-$600m monthly run-rate. Our thesis catalysts here are tighter wallet integration, better UX, and protocol-level incentive schemes that blend spending with yield. Longer term, we expect a winner-takes-most market structure, mirroring traditional payments, though competition remains intense enough that it’s too early to back a single dominant player.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.