13 April 2026

Key Insights: Strait to Market

Strait Still Closed

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

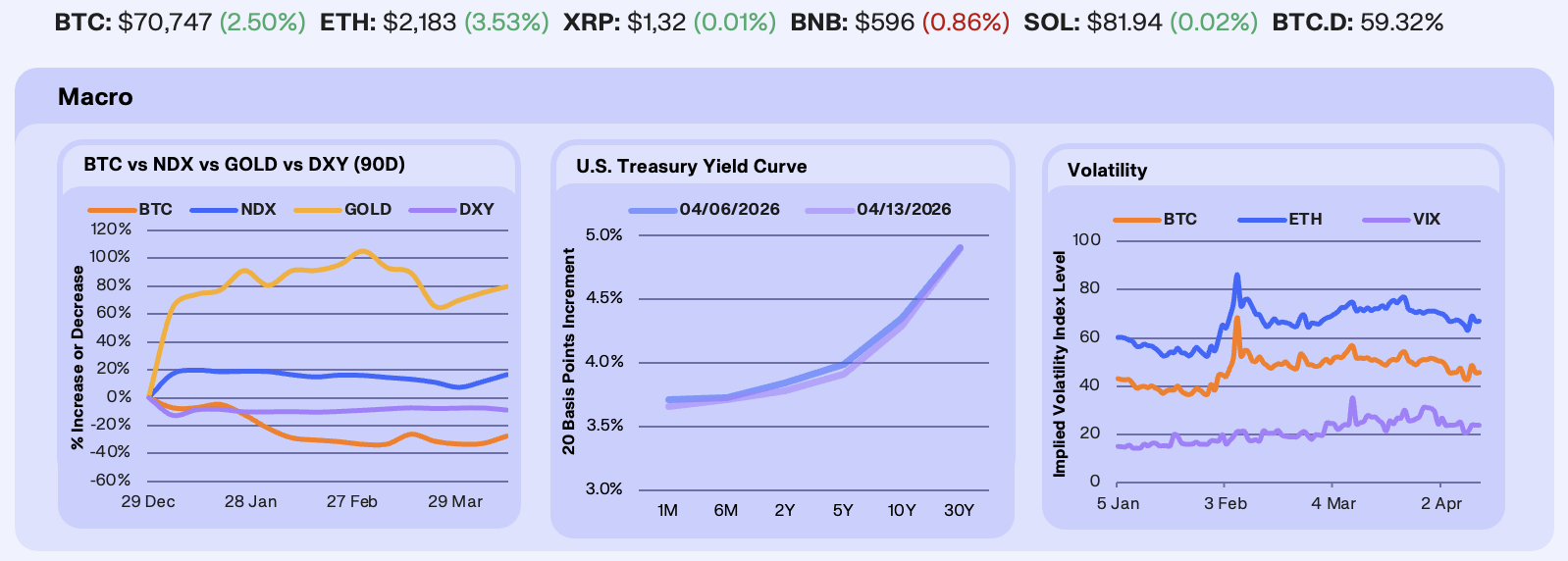

The Iran ceasefire dominated the week. A Pakistan-brokered two-week agreement, reached ahead of Trump’s Tuesday deadline to reopen the Strait of Hormuz, triggered a broad risk-on repricing. NDX surged +4.31% and BTC added +2.50% to $70,869.78, while Gold gained +1.89%. DXY fell -1.54% to 98.54, extending its 2026 downtrend as the dollar’s inflation-premium bid faded on lower oil. The rally was front-loaded, with the bulk of the move coming in the sessions immediately following the announcement. By Wednesday, however, ADNOC’s CEO confirmed the Strait was still not open, with Iran restricting and conditioning traffic despite the agreement.

Treasury yields declined across the entire curve as lower oil softened the near-term inflation outlook. The 5Y led at -8bp to 3.91%, with the 2Y falling 6bp to 3.78% and the 10Y down 6bp to 4.29%. The 30Y barely moved, declining just 1bp to 4.90% and remaining anchored near the 5% level. Front-end and belly yields declining while the long end holds reflects a market pricing medium-term easing on energy relief without revising its longer-run inflation view. Thursday’s CPI print confirmed the dynamic with headline coming in hot at +3.3% YoY (+0.9% MoM) on surging energy costs, but core held at +2.6% YoY, and the market treated it as backward-looking given the ceasefire. That assumption requires oil to hold its post-ceasefire levels.

Volatility compressed sharply across all three benchmarks. The VIX fell -12.08%, with the move concentrated in a single session as it dropped from 25.09 on Monday to 20.97 on Tuesday when the ceasefire firmed. BTC 30-day ATM IV followed the same pattern, spiking to 47.46 on Monday before settling at 43.01 by Wednesday for a -6.19% weekly decline. ETH IV dropped -6.28% to 63.28. Monday’s vol spike reflects hedging demand built into the Trump deadline, and Tuesday’s collapse marks the removal of that specific tail event.

Our Take: The March FOMC minutes, released this week, revealed a committee openly split between rate hikes and cuts, with hawks warning about persistent energy-driven inflation and doves flagging recession risk from a prolonged conflict. The ceasefire briefly revived rate cut pricing, but expectations are already being pared back as the Strait remains physically closed. The yield curve reflects that same tension and does not believe the inflation regime has changed. The ceasefire expires April 22nd, and if the Strait hasn’t reopened by then, the hike side of the FOMC debate becomes the dominant narrative heading into the May meeting.

Institutions Re-Enter

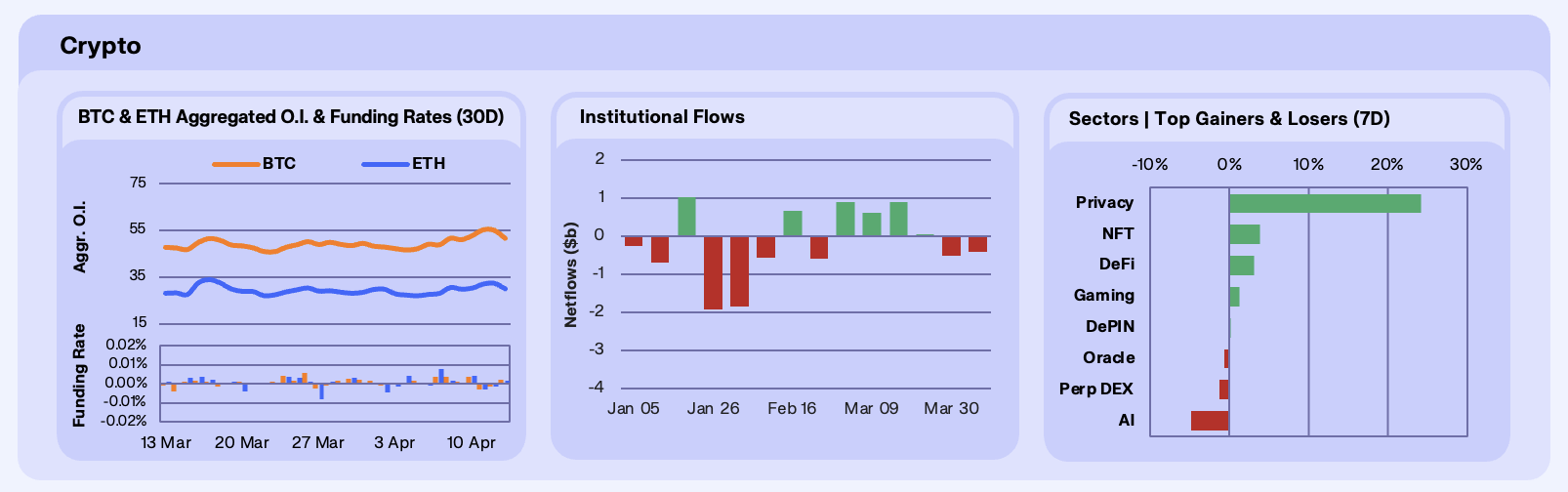

Open interest surged on the ceasefire. BTC OI rose +17.3% from $46.9B to $55.1B, adding $8.1B in new positioning and fully reversing last week’s -2.8% decline. ETH OI climbed +18.3% from $27.1B to $32.1B. The build was concentrated on Tuesday, when BTC OI jumped $2.8B in a single session as the ceasefire was confirmed ahead of Trump’s deadline. Wednesday saw a brief pullback in both assets before fresh positioning resumed Thursday. Funding rates stayed positive through Thursday before flipping negative on Friday at -0.0027%, suggesting late-week sentiment shifted as the Strait remained closed. The ETH OI spike preceded the formal ceasefire confirmation, suggesting aggressive long positioning ahead of the deadline. The late-week funding flip bears watching, if negative rates persist, it would signal bearish crowd positioning against rising OI, creating short-squeeze conditions.

Institutional flows reversed sharply. Bitcoin ETFs recorded +$576.8m in weekly inflows, with Ethereum adding +$123.1m and Solana seeing -$17.3m. The reversal from last week’s -$412m aggregate outflows is notable. BTC ETF AUM sits at $87.3B and ETH at $11.5B. The pattern across both derivatives and products is consistent, with leverage and institutional capital re-entering simultaneously on the ceasefire. The previous four headline-driven rallies moved OI and spot but failed to flip ETF flows, which had been in persistent outflow. That changed this week.

Privacy led sector performance decisively. ZEC surged +61.3% from $257 to $383, with the bulk of the move occurring on April 8 (+25% in a single session). The EU’s AMLR timeline, which restricts privacy coins at licensed exchanges by July 2027, is forcing the market to differentiate between compliant and non-compliant privacy architectures, and ZEC’s viewing keys place it on the compliant side of that divide. Foundry’s launch of an institutional ZEC mining pool and a pending Grayscale ZEC ETF application added to the momentum. XMR gained +6.7% and DCR +16.6%, confirming the bid as sector-wide. On the downside, AI continued to lag with TAO falling -12.1% and the broader AI category declining. WLFI dropped -18.3% to record lows near $0.08.

Our Take: This is the first ceasefire rally of 2026 that pulled institutional capital alongside leverage. The previous four iterations moved OI and spot but failed to flip ETF flows. That changed this week, with $700m in combined BTC and ETH inflows alongside a 17-18% OI increase. The quality of the bid is different, but the positioning is aggressive for what remains a two-week agreement. April 22 is the ceasefire expiry. If it extends, the OI build has room to consolidate. If it lapses, the combined leverage and institutional positioning creates a more crowded unwind than any of the four prior episodes produced.

Onchain Specialists Win

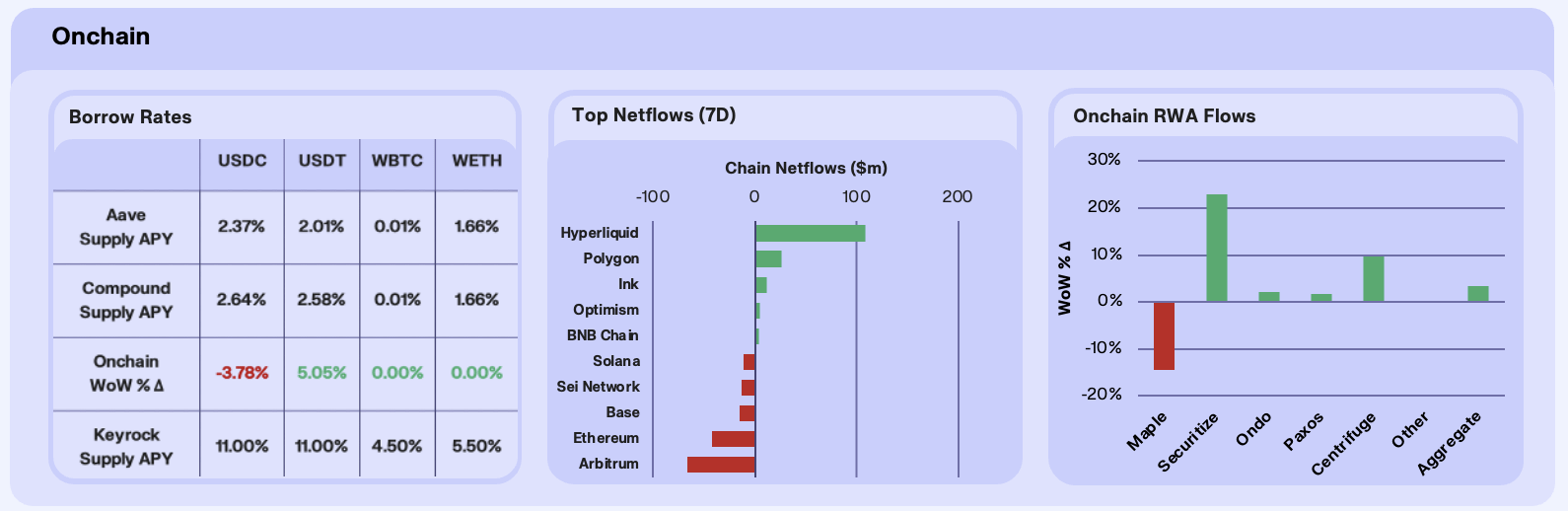

Stablecoin lending rates were mixed this week, giving back a portion of last week’s recovery. USDC supply APY declined 3.8% WoW across major venues, reversing roughly a quarter of the prior week’s 14.6% move higher. USDT was up 5.1% WoW. WETH supply APY was flat, reinforcing the pattern that ETH-denominated leverage demand remains structurally subdued even as dollar-denominated markets show signs of stabilisation. Utilisation was divergent with USDC utilisation rising from 0.69 to 0.80, while USDT, WBTC, and WETH all saw utilisation contract, suggesting that whatever borrowing demand exists is concentrating in USDC rather than broadening across assets.

Chain-level flows followed the established pattern of capital rotating toward specialised venues. Hyperliquid led inflows for the fourth consecutive week at +$108.7m, driven by continued dominance in leveraged macro products, with Bitcoin and oil perps each exceeding $1B in 24-hour volume on multiple days. The HYPE token unlock on April 6th landed far lighter than expected, with actual claims of just 330K HYPE ( approximately $12m) against projections of 9.92m, removing a key overhang. Polygon PoS posted +$26.2m, continuing to build on its payments and stablecoin infrastructure momentum as onchain stablecoin supply held near ATH levels above $3.4B.

RWA AUM rose +3.36% WoW in aggregate, but dispersion across protocols was extreme. Securitize was the clear standout at +23.04%, driven by continued momentum from its NYSE MOU as digital transfer agent for the exchange’s tokenised securities platform It was also driven by its integration as the proof-of-asset verifier for BlackRock’s BUIDL, and inclusion in the Sky incubator cohort. Centrifuge posted +9.82% on the back of the deSPXA launch, a tokenised S&P 500 Index Fund on Base licensed by S&P Dow Jones Indices.

Our Take: Capital continues to concentrate in either derivatives-driven venues like Hyperliquid for leveraged macro expression, or payments-driven ecosystems like Polygon for stablecoin utility. What’s absent is the middle ground, which we see as broad-based DeFi activity on general-purpose chains that have defined previous cycles. To our desk, it appears the onchain economy is repricing around specificity, and chains that try to be everything to everyone are the ones bleeding capital.

Digital Credit Eats BTC Supply

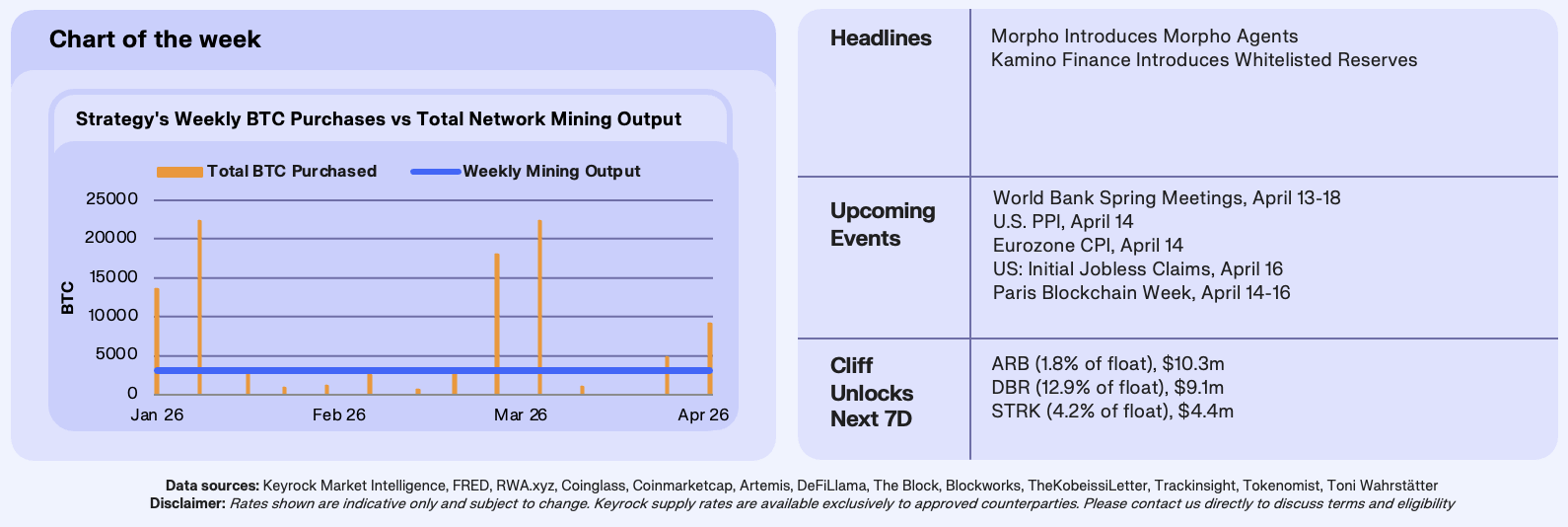

This week’s chart tracks Strategy’s weekly Bitcoin purchases against total network mining output since the start of 2026. The Bitcoin network produces approximately 3,150 BTC per week at the current post-halving block subsidy of 3.125 BTC per block, a fixed rate that will hold until the next halving in 2028. Over the same 14-week period, Strategy purchased 102,339 BTC, compared to approximately 44,100 BTC mined by the entire network, 2.3x the total new supply created.

The purchasing pattern is episodic, with four weeks in particular standing out. In the weeks beginning January 5th, January 12th, March 2nd, and March 9th, Strategy acquired between 4x to 7x the BTC mined. In January, nearly all capital raised came through the MSTR common stock ATM. By March 9th, 75% of the $1.57 billion raised that week came through STRC, Strategy’s variable-rate perpetual preferred stock, marking the first time the preferred instrument overtook common equity as the primary funding vehicle. STRC is a perpetual preferred equity instrument that trades at $100 par with two pennies of volatility and $330 million of daily volume, paying 11.5% annually. March set a record with $746 million in STRC ATM volume, and the most recent week saw an estimated 9,152 BTC accumulated via STRC alone, per STRC.live.

Our Take: STRC can be viewed as a digital credit instrument that pulls capital from traditional fixed-income allocations and converts it directly into Bitcoin demand. Saylor has framed this as digital capital (Bitcoin) underpinning digital credit (STRC, STRK, STRF), which in turn reprices the cost of capital for the entire credit market. When a single yield product can fund Bitcoin purchases outpacing the entire network’s weekly output, we need to start reframing Bitcoin absorption away from its issuance schedule and towards the demand for said yield product. The signal we are watching for is whether STRC volume sustains above $200 million daily through the next ex-dividend cycle. If it does, we will have conviction that Strategy’s capacity to absorb multiples of mining output is a structural feature of an emerging digital credit market.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.