1 June 2026

Key Insights: Silence of the Vols

Hedge Basket Unwinds

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

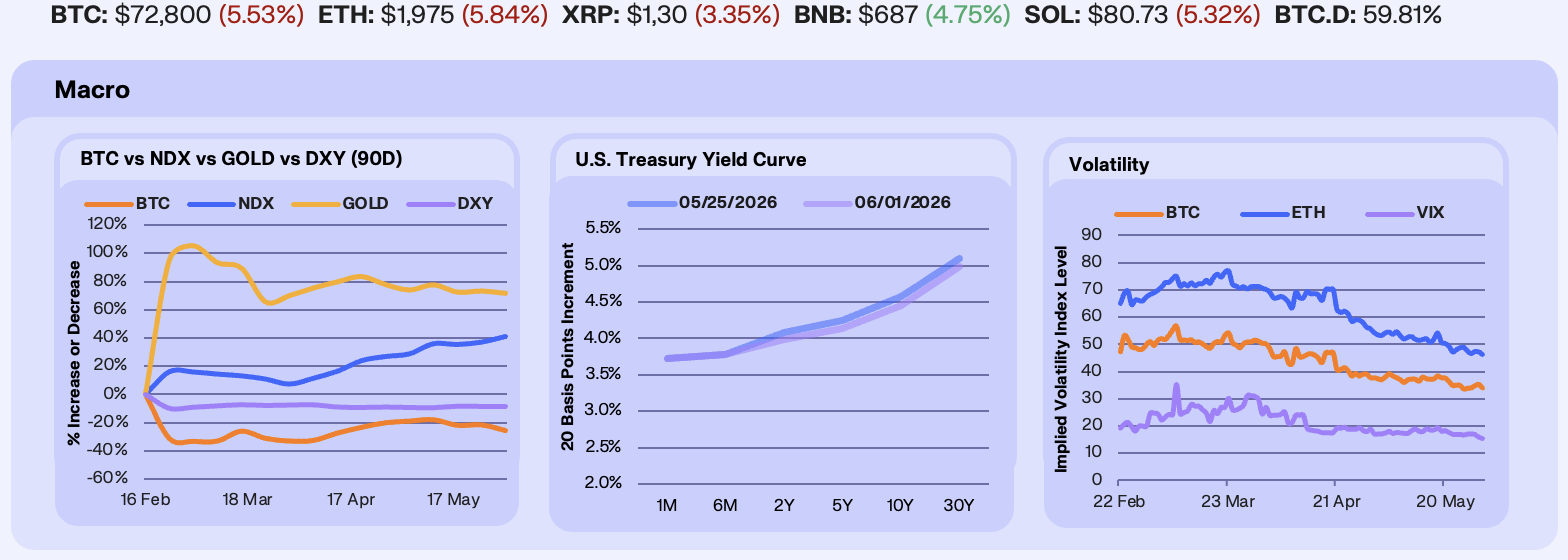

Risk assets split this week as April PCE inflation cooled by enough to pull the hawkish bid out of the long end. NDX added +2.9% to 30,333 and the DXY held flat at $99, while Gold fell -1% to $4,521 and BTC dropped -5.1% to $73,292 on its ninth straight day of spot ETF outflows. We read the cross-asset move as investors stepping out of the inflation-hedge basket at once, with both gold and BTC selling as energy prices eased and rate-cut expectations firmed. Stocks took the duration tailwind on the other side of the same repricing, while the hedge complex lost the catalyst that had carried it since the April CPI shock.

Yields fell across the curve after Thursday’s April PCE print came in softer than expected, with the belly and long end leading. The 10-year and 5-year each dropped 12 basis points, to 4.45% and 4.13%, the 30-year fell 11 basis points to 4.99% and back below 5% for the first time in three weeks, and the 2-year eased 10 basis points to 3.98% while the front-end bills held flat. April PCE landed at +3.8% year-on-year and +0.4% month-on-month, under consensus on the monthly read and enough to take the air out of bets on Fed hikes that had built into last week’s long-bond auction. Polymarket’s “Fed hike in 2026” market dropped from 48% to 36% over the week, the clearest sign the hike trade is unwinding.

Volatility stayed quiet even as spot fell close to five percent. BTC 30-day implied volatility held nearly flat at +1.08% to 34.12, while ETH IV eased -5.66% to 46.09 and the VIX dropped -8.29% to 15.32, equity vol bleeding lower as the duration relief took hold. We read the compression and tight strike clustering as a regime shift, with baseline BTC vol grinding lower as institutional liquidity deepens and the fat-tail moves that defined the prior cycle getting rarer. Our desk is quoting clients a 60-day dual-barrier structure paying 3.65% premium as long as BTC stays inside a ±20% band (roughly $58.9K to $88.4K against current spot), a way to harvest the new regime without selling vanilla options outright.

Our Take: Two debates are live for next week. The first is whether BTC’s slide is a positioning unwind that resolves into a buy, with onchain data showing a buyer drought rather than seller panic and whales trimming around 6,000 BTC across the week, or a deeper rerating that needs the Fed to actually cut before institutions return. The second is the gap between sell-side framing holding to a December cut and pricing hike odds at 31%. We lean closer to the rate read, since a softer PCE path and an easing energy backdrop make a hike unlikely without a fresh shock. The signal we watch is whether ETF flows turn before the June 16–17 FOMC, since the spot bid stopping is what flushed positioning in the first place.

Leverage Round-Trips

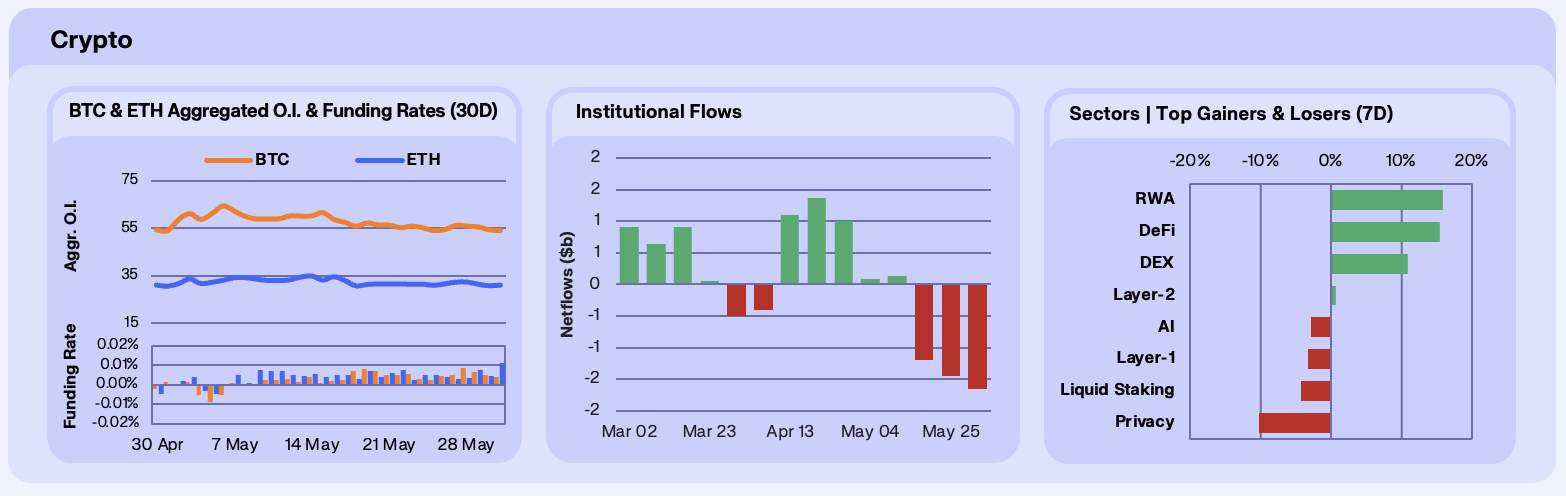

Open interest built modestly even as spot sold off. BTC open interest stayed flat on the week to $54B and ETH open interest added +1.36% to $31.38B, with the build concentrated Tuesday through Wednesday before easing into Friday. Funding stayed positive on both through all five sessions, with BTC funding peaking at +0.0084% Wednesday and ETH funding running between +0.0030% and +0.0112%. The shape is leveraged longs adding into the drawdown rather than capitulating alongside the ETF complex, with positioning leaning into a bounce that has not yet shown up in spot.

Spot ETF outflows extended to a third straight week. Bitcoin ETFs shed -$1.42B after -$1.256B and -$995.5M in the two prior weeks, pushing the streak past $3.5B in cumulative redemptions. Ethereum products lost -$242M, broadly matching the prior week’s -$216M, while Solana funds eked out +$2.4M. The HYPE wrappers ran the opposite way, with BHYP and THYP combined adding +$51M across the four holiday-shortened sessions, +$30M of it on Friday on a $20M Bitwise creation alone, lifting cumulative inflows since the May 12 launch to $135M.

Sectors weakened across the major complex even as a handful of single names ran. Layer 1s fell -3.3%, with ETH -4.2%, SOL -3.4%, and XRP -1.1% moving in lockstep and BNB the lone bid at +8.4%. Privacy was the weakest category at -10.2%, with ZEC -14.0% extending its reversal off the recent Multicoin-disclosure peak on profit-taking. HYPE stood out at +15.2%, lifting the DEX category to +10.9% and decoupling from broad weakness for the second week running on its ETF tailwind. The +15.8% RWA and +15.5% DeFi category prints are single-name outliers driven by XLM +73.7% and RAIN +88.3%, and do not read as category rotation.

Our Take: The week’s positioning sits in two camps. The ETF complex continues to redeem while perp traders quietly add leverage into the drawdown, with BTC and ETH open interest both building and funding positive throughout. We read this as dip-buying ahead of an expected June bounce rather than a leveraged short campaign, but the spot bid has to turn for it to play out. HYPE is the cleanest standout, with the wrappers absorbing $50M against more than $1.6B leaving the BTC and ETH funds.

Capital Parks Onchain

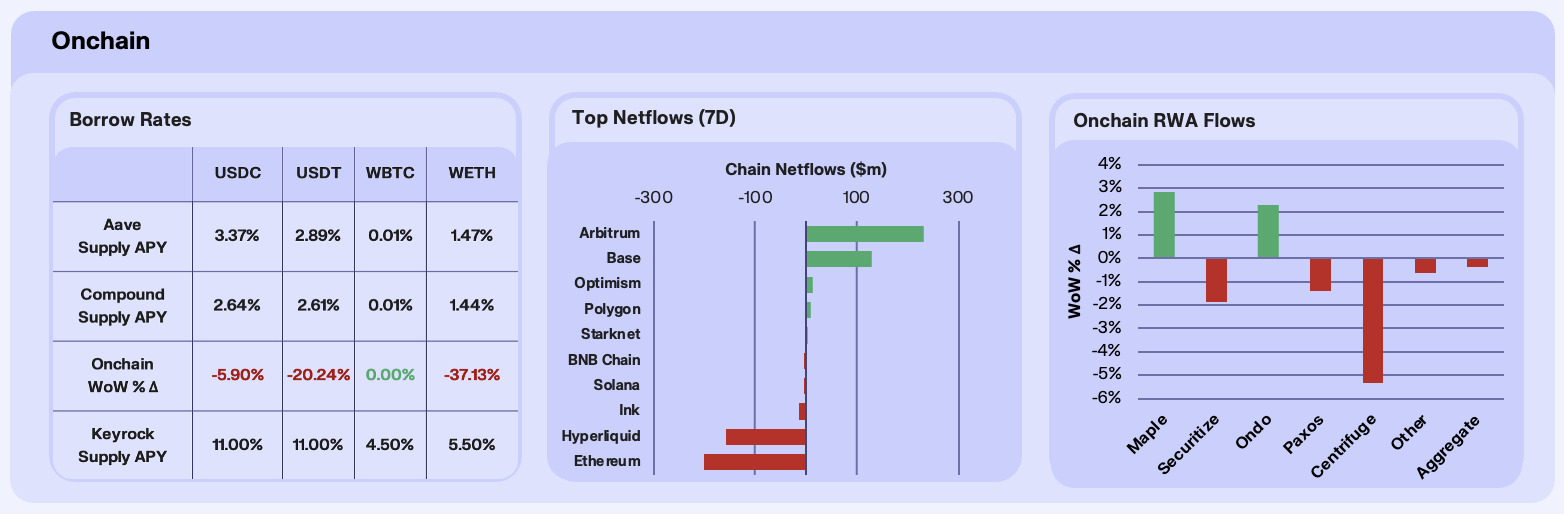

Stablecoin lending rates softened as capital parked onchain for yield while the spot tape bled. USDC supply APY across Aave and Compound averaged 3.36%, down -12.9% WoW from 3.85%, while USDT eased -4.1% to 2.58%. The move was supply-driven, with USDC TVL across the two protocols building roughly 14% as rates fell. WETH printed +6.5% to 1.54% on the weekly average but softened to 1.46% by Thursday on the same supply influx.

Cross-chain flows concentrated sharply in Hyperliquid and Base while the established L1s and L2s continued to bleed. Hyperliquid led the board at +$139M, with Base dding +$98M, Optimism +$11M, and Polygon +$10M. The outflows ran through Ethereum at -$140M, with smaller exits in BNB -$6M, Solana -$3M, and Ink -$2M. We read the Hyperliquid concentration as institutional capital rotating into the protocol layer where the perpetuals venue, ETF wrappers, and onchain pre-IPO products now stack on top of each other, with the bridge tape confirming what the HYPE wrapper flows have already shown.

Tokenised real-world assets contracted again but at a softer pace. Aggregate RWA AUM fell -0.38% WoW compared with -1.78% the prior week, with the dispersion now favouring credit. Maple reversed to +2.83% after last week’s -6.68%, the sharpest swing in the cohort, as the deposit ramp from its Ink integration started to land. Ondo added +2.30% with distributed asset value near $4B and holders up roughly 25% over the past month, while Centrifuge bled another -5.35% against a platform total of roughly $1.4B in distributed assets. Securitize turned -1.87% after last week’s +1.39% and Paxos eased -1.40%.

Our Take: The cross-asset divergence we flagged in spot and ETFs now shows up in the onchain plumbing. Capital is parking onchain for yield as ETFs redeem, with lending TVL building on the week even as rates compress, and the same flow is concentrating in Hyperliquid and Base while Ethereum and Arbitrum lose ground. We read the rate compression as defensive yield-seeking, with the perp complex adding longs at the same time deposits accumulate in onchain money markets. The signal we watch is whether lending TVL keeps building, since that would mark capital still treating onchain as a sidelined holding rather than rotating back to spot.

Vol Goes Quiet

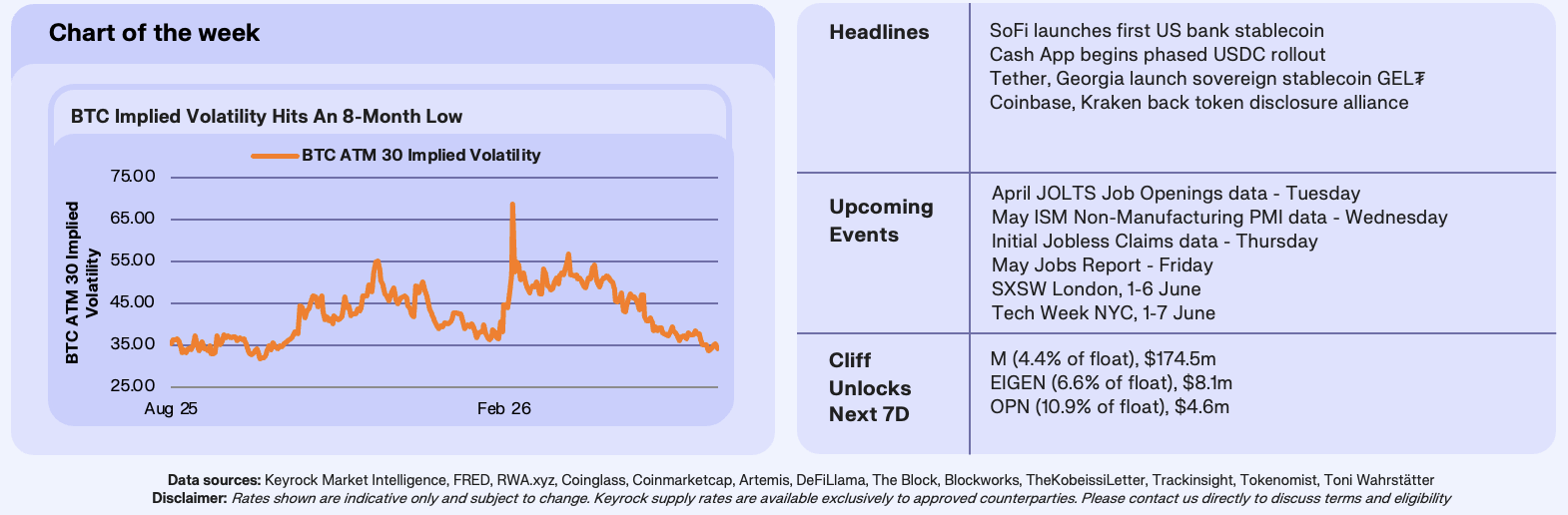

BTC implied volatility printed its lowest single-day reading in eight months this week, a quiet print against a noisy week. Spot fell -4.64%, the BTC ETF complex shed another -$1.29B in its third straight outflow week, Polymarket’s Fed-hike probability dropped 17 points, and the long end of the curve rallied 12 basis points on the PCE relief. Vol normally rises into selloffs and macro repricings. This week it compressed.

BTC 30-day ATM implied volatility closed at 33.75 on Monday May 25, the lowest single-day print since September 23, 2025, with the series holding above that floor for 243 trading days in between. The intervening stretch includes a February 6 spike to 68.66, a November 23 high of 55.17, and a steady drift lower from a March monthly average of 51.45. The weekly daily average across Monday through Thursday landed at 34.2, the lowest weekly average since last September. From the February peak, BTC IV has fallen roughly 51%. The vol compression is what a maturing market looks like, with deeper liquidity damping the gamma cycle that used to define BTC’s tail moves.

Our Take: The compression is the harvestable opportunity, and it does not break on its own. The same setup we framed in our macro section, a 60-day dual-barrier structure paying 3.65% premium for staying inside a ±20% band, reads as the cleanest expression of the thesis. Volatility can surge when the June 16-17 FOMC delivers something the curve does not already price, when an oil shock reverses the easing energy backdrop, or when an ETF flow turn restarts the gamma cycle from the long side. Until then, the path of least resistance for BTC vol is sideways, and our desk is positioned to harvest it.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.