9 February 2026

Key Insights: Risk Comes Due

Risk Reset Takes Hold

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

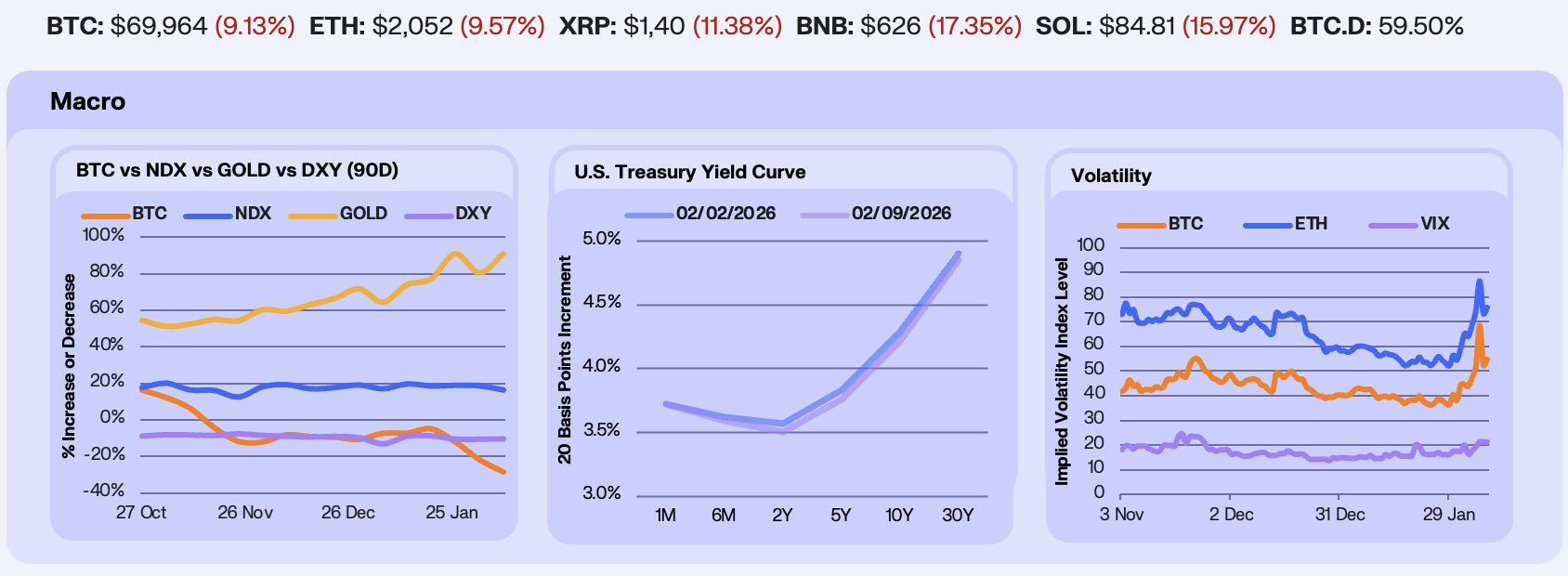

Last week was dominated by earnings, labor data, and a sharp repricing of risk across assets. Bitcoin led declines, falling -8.7% on the week and erasing its post-election rally as it slipped below $70,000 for the first time since November 2024. Momentum indicators now place BTC in its third most oversold regime on record. Equities also weakened, with NDX down -1.9% to its lowest level since late November, as software stocks faced pressure from two fronts: growing skepticism that AI capex will translate into commensurate revenue growth, and rising concern that AI disruption is becoming an immediate competitive threat rather than a distant risk. In contrast, gold rose +5.8%, supported by continued central bank demand, and the US dollar strengthened +0.3%.

Rates markets reflected a clear shift toward growth and labor market concern. Treasury yields declined across the curve, with the largest moves concentrated in the belly, following labor data that showed U.S. corporate layoffs in January reaching their highest level since 2009. Fed funds futures now reflect a growing expectation for easing, with markets pricing a strong probability of a 25 bp cut by June, near-even odds of a follow-up cut in July, and a meaningful chance of a third cut by December.

Volatility surged as spot prices broke key technical levels. BTC ATM 30-day implied volatility jumped +23% WoW to 55, ETH IV rose +27% to 76, and the VIX climbed +22% to 21. The spike was led by front-end crypto volatility, with short-dated options pricing elevated near-term tail risk while longer-dated vols lagged, leaving curves sharply inverted. Options markets are now pricing roughly a 60% probability that BTC trades below $50,000 at some point in 2026, highlighting how quickly sentiment has shifted.

Our Take: The broader takeaway is that markets are undergoing a liquidity-driven risk reset. Gold is adjusting as real yields remain attractive, equities are wobbling as growth assumptions are challenged, and crypto is cooling as speculative liquidity has further retreated. While the near-term backdrop remains fragile, periods marked by pessimism, compressed liquidity, and elevated volatility have historically laid the groundwork for stronger long-term returns once expectations reset and macro clarity improves.

Crypto Under Pressure

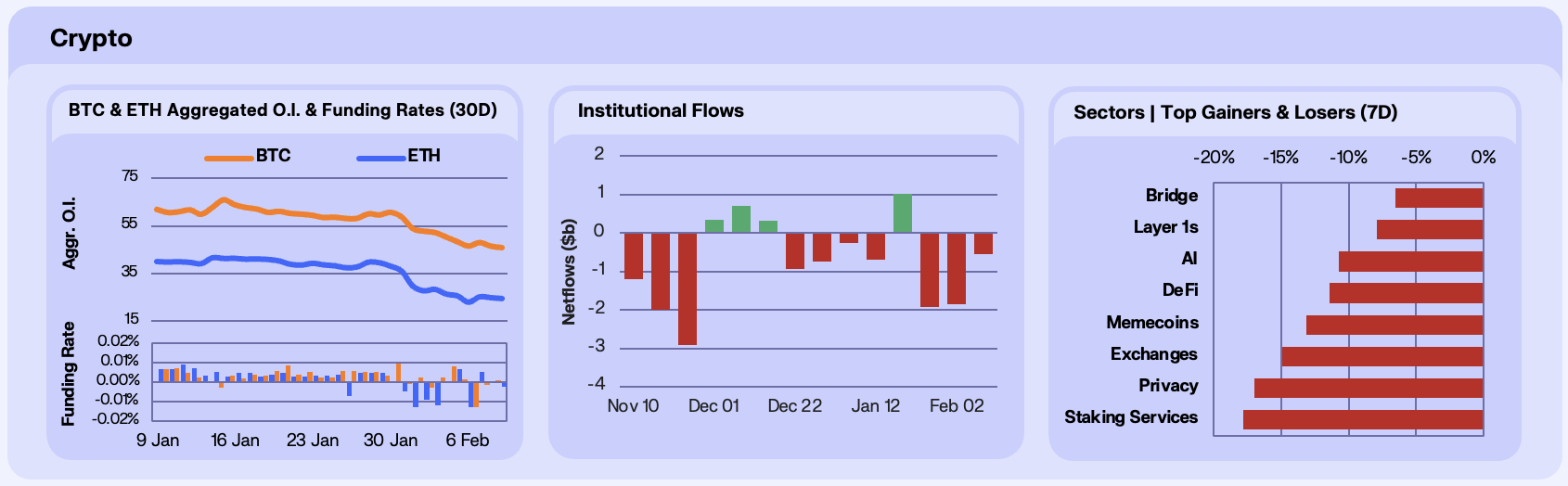

Crypto markets experienced a sharp reset as risk sentiment deteriorated alongside the selloff in precious metals and broader macro stress. Open interest dropped decisively, with BTC OI down −13% WoW and ETH OI down −12%. Funding rates briefly flipped deeply negative during the selloff, particularly in BTC. In ETH, where spot prices are now more than 50% below ATHs, short sellers were willing to pay a premium to maintain downside exposure. Volatility expectations surged to their highest levels since November 2025, exceeding those seen during the October 10 liquidation. Since Feb 1, more than $4.5b in crypto longs have been liquidated across exchanges, including Hyperliquid, with Thursday marking the largest single-day flush since October as over $1.8b was wiped out. While funding rebounded and normalized quickly after the washout, positioning remains fragile.

Institutional flows remained defensive but showed early signs of stabilization. Bitcoin spot ETFs saw continued net outflows over the week, though the magnitude was notably contained relative to price action. Despite Thursday’s sharp selloff, net BTC ETF redemptions totaled roughly $434m, followed by a rebound into Friday with approximately $331m of net inflows. This asymmetry suggests selling pressure may be losing intensity at current levels. Notably, IBIT options volatility surged alongside the price decline, pointing to concentrated hedging activity. Market speculation suggests the drawdown may have been exacerbated by a single fund reducing risk via puts, which could help explain why ETF outflows remained contained relative to the magnitude of the move.

Sector performance was uniformly negative, underscoring the breadth of the risk-off move. Losses were concentrated in higher-beta segments, with Staking Services (-17.8%) and Privacy (-17.0%) leading declines as yield-sensitive and regulatory-adjacent exposures were aggressively sold. Memecoins (-13.1%) also underperformed, reflecting collapsing retail risk appetite and lower speculative turnover. DeFi (-11.4%) followed, pressured by both declining TVL expectations and the unwind of crowded narratives.

Our Take: With ETF flows subdued and total crypto market capitalization retracing to 2024 levels, current conditions reflect sluggish institutional demand amid a Fed pause and tighter liquidity. As liquidity has contracted and risk appetite waned, crypto has underperformed broader markets and increasingly resembles the trough of a bear market rather than early recovery dynamics. Institutional flow dynamics remain a key variable to watch for signs of stabilization or renewed allocative interest.

Onchain Flight to Safety

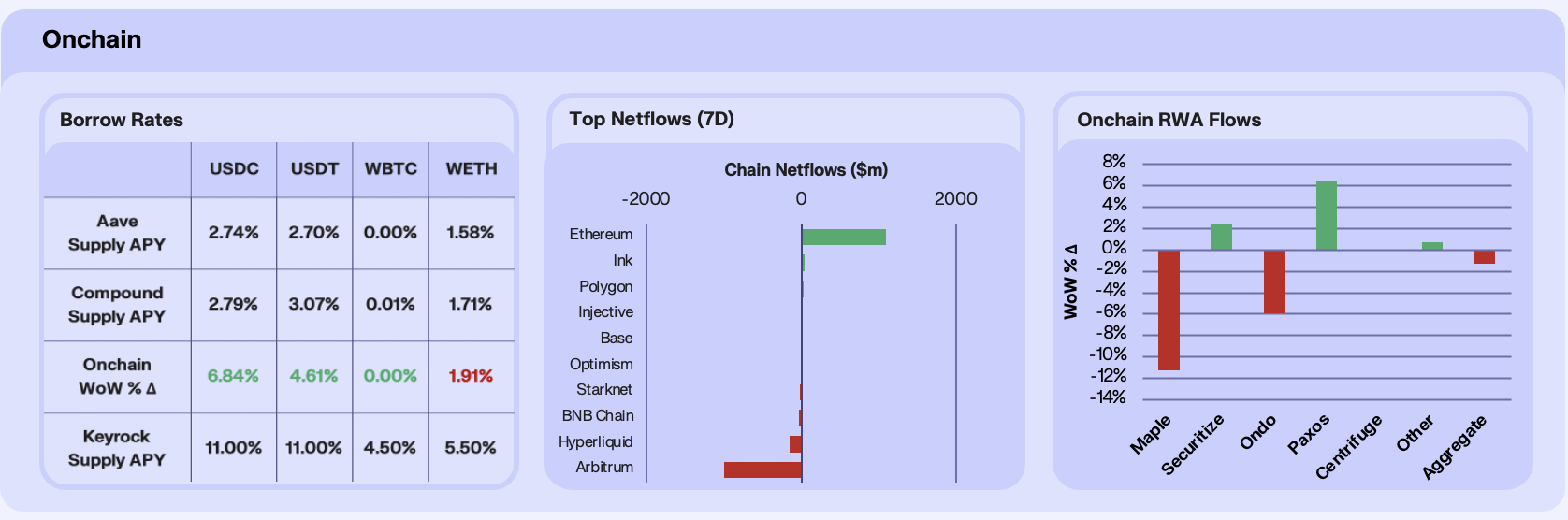

Onchain supply rates strengthened across the board this week, led by stablecoins, where we saw USDC and USDT gain 2.74% and 2.7% respectively WoW. As expected in a highly volatile market, the pool conditions look to have been liquidity-driven this week, with USDC supply rising sharply, increasing over 2x WoW, a setup that typically keeps stables sticky while beta lending stays muted. The market is opting for stable-centric positioning, while demand in borrow markets remains selective.

This defensiveness is reflected in cross-chain flows, where Ethereum led with $1.1b in net inflows, while Arbitrum and Hyperliquid saw $1b and $152m in outflows respectively. We read this as a consolidation back into the deepest liquidity ecosystem during highly volatile market conditions. Capital prefers home safety when liquidations spike and spreads widen. RWAs saw a soft contraction at the aggregate level, down 1.29% in AUM WoW, but dispersion between major RWA protocols tells a different story.

Paxos (+6.38%) and Securitize (+2.36%) held up, while Maple (-11.29%) and Ondo (-5.92%) retraced. Flows are concentrated into exposures that behave more like defensive, liquid collateral, like gold-adjacent assets, while credit and tokenised equity risk sees faster drawdowns when volatility forces deleveraging.

Our take: This week reads like an onchain re-risking pause on recent moves. If markets stabilise, the next onchain upside signal will be borrow activity returning without another liquidity shock, shown as utilisation up, not just supply down. Until then, we expect flows to keep favouring depth and, therefore, defensiveness.

Digital Gold Rush

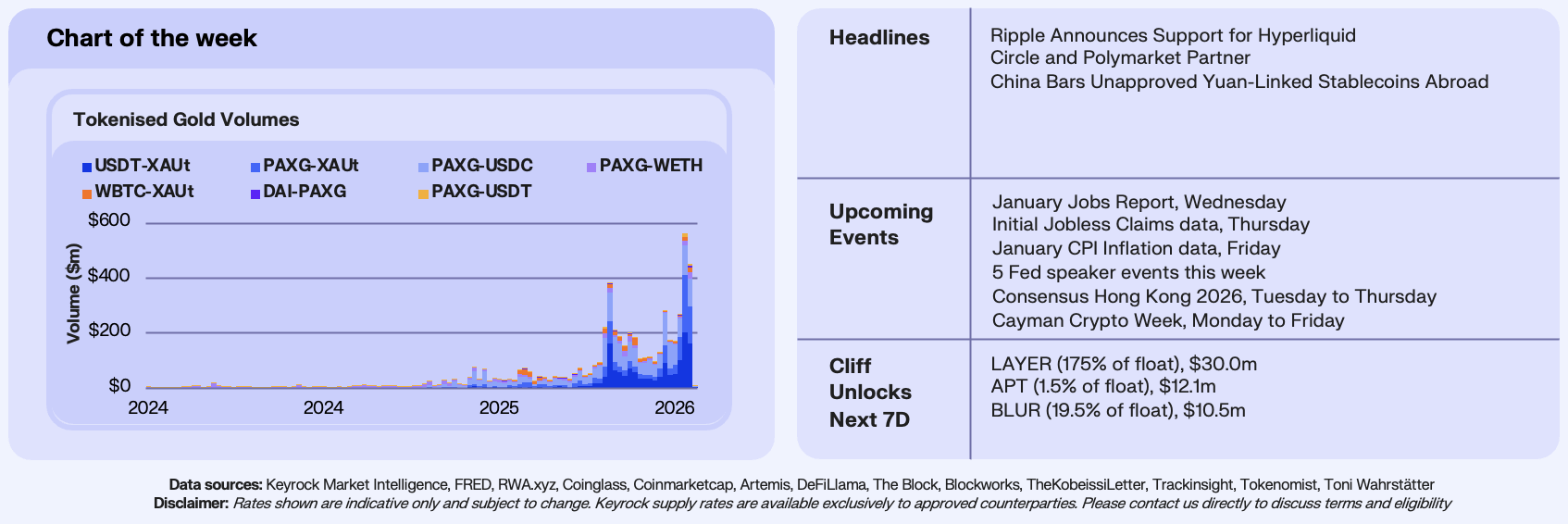

This week, our chart of the week highlights tokenised gold trading volume by pair, showing where price discovery is actually happening across gold tokens and their quote assets. Total tokenised gold volume reached $4.0b in 2025 vs. only $0.27b in 2024, a 1,370% YoY jump, with activity heavily back-ended. In fact, Q4 2025 accounted for 62% of the year’s total. The most recent standout is the week ending 26 Jan 2026, when total volume printed $570m, dominated by PAXG-XAUt ($209m) and USDT-XAUt ($202m).

Keyrock’s interpretation is that tokenised gold is becoming a high-velocity trading rail. Two things are doing the work here, the first being that heavy stablecoin quoting indicates that most gold flow is being expressed as dollar-denominated-risk, with traders taking directional bets, and secondly the size of PAXG-XAUt suggests a meaningful amount of flow is issuer-basis and cross-venue arbitrage. This acceleration also fits the broader backdrop where gold has been behaving as the global hedge trade, ironically stealing narrative strength from Bitcoin, even onchain.

Our take: Tokenised gold now looks like it’s a core onchain defensive primitive, in that it’s a stablecoin-compatible hedge that can be rotated, arbitraged, and collateralised quickly during macro shocks. If volumes stay elevated outside of pure risk-off weeks, we think the next leg is a flywheel of deeper liquidity leading to tighter spreads, thus more routing and more gold as collateral usage in DeFi.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.