15 December 2025

Key Insights: Rates in Control

Soft Landing Signals

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

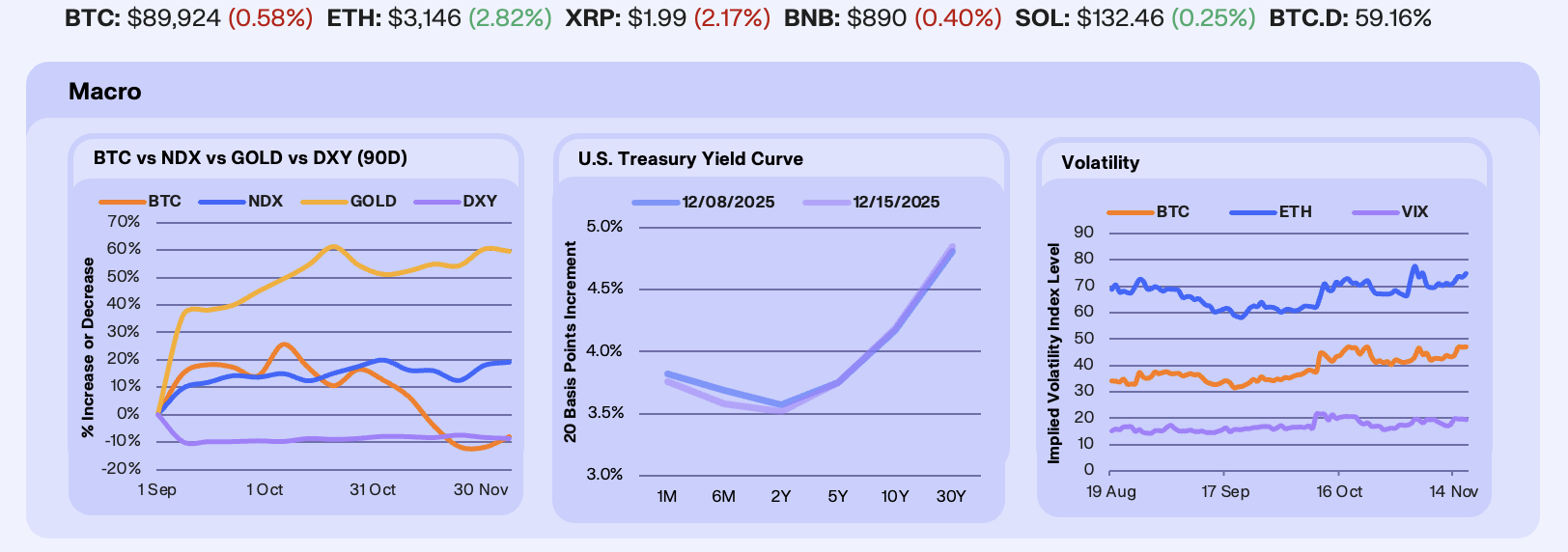

Last week was defined by the FOMC rate cut, with the Fed delivering 25 bps of easing while Powell emphasized that “conditions in the labor market are cooling” and inflation remains “somewhat elevated,” signaling cuts may be done for now. Markets read the combination as late-cycle caution rather than a green light for risk. BTC fell 1%, Gold rallied 2.3% (near record highs), the NDX slid 1.9%, and the DXY weakened 0.5% as easing expectations continued to weigh on the dollar.

Treasury markets reflected a mild front-end rally alongside a modest steepening. The curve shifted lower at the front (1M –6 bps, 6M –11 bps, 2Y –5 bps) while the long end drifted higher (10Y +2 bps to 4.19%, 30Y +4 bps to 4.85%). The move was amplified by headlines around the Fed’s balance sheet: officials diverted more reserves into short-term Treasury purchases, resisting the QE label, with Powell noting purchases may remain elevated for “a few months.” The Fed is set to buy $40b of Treasuries over the next 30 days, just 12 days after QT ended, a liquidity tailwind even if messaging remains deliberately conservative.

Volatility mostly drained despite the risk wobble. BTC 30D ATM IV fell 11.3% and ETH IV dropped 6.8%, while the VIX ticked up ~1% to ~15.7. Crypto implieds tracked lower realized movement and fading near-term hedging demand, while equities held a relatively contained volatility regime even as positioning stayed more cautious.

Our Take: There’s increasingly little rationale for the Fed to stay meaningfully restrictive if job creation is sputtering and inflation risks continue to fade. With home prices rolling over, excess rental supply building, and crude trending lower, the inflation scare looks increasingly behind us, and deflation risk is becoming non-trivial at the margin. In our view, the Fed will likely need to cut at least two more times in 2026 to reach something closer to neutral, and the re-emergence of Treasury purchases reinforces that the liquidity impulse is quietly turning more supportive.

Flows vs. Price

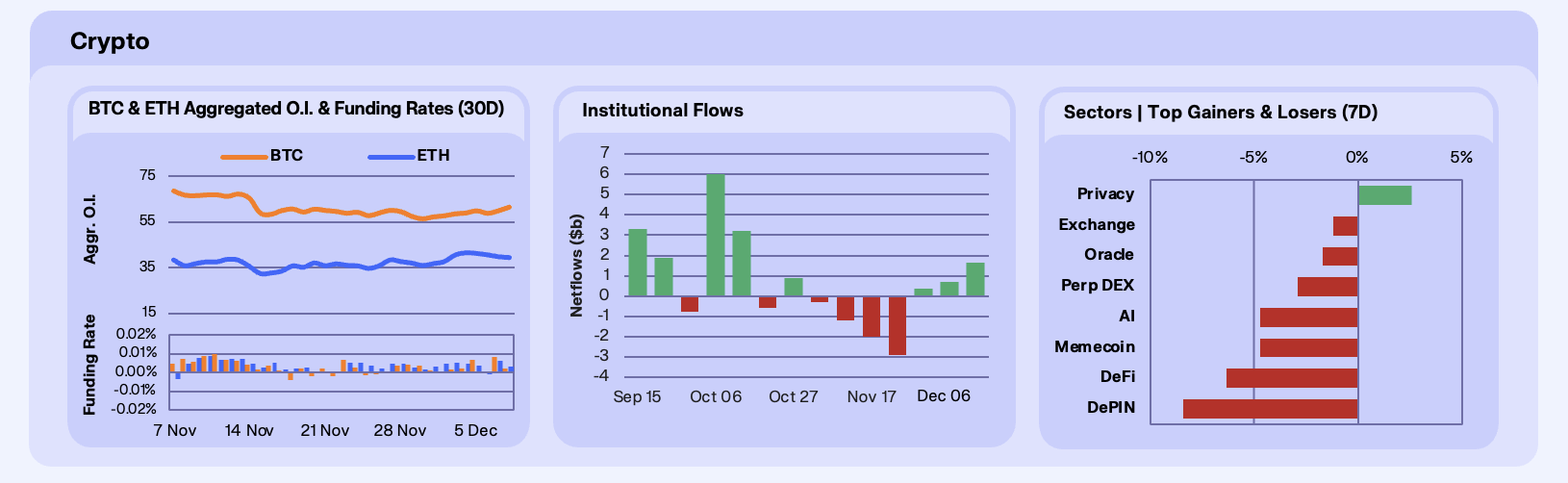

Price action across majors was again bleak this week, although final WoW figures masked meaningful dispersion beneath the surface. Bitcoin fell 2% despite institutional accumulation, with Strategy adding over 10k BTC and long-term holders, miners, and a Satoshi-era whale all accumulating aggressively, pushing exchange balances to fresh lows. These supportive flows were largely offset by distribution from mid-cycle holders and covered-call strategies, which capped upside and reinforced choppy conditions.

Ethereum traded flat as strong institutional and ecosystem developments counterbalanced short-term profit-taking. ETF-related momentum improved following BlackRock’s filing for a staked ETH ETF and BitMine’s continued accumulation, while tokenisation headlines, including DTCC approval to tokenize assets at scale on Ethereum, reinforced the long-term narrative without driving immediate price follow-through. Solana underperformed, down 2.6%, as unlock-related selling outweighed positive catalysts such as JPMorgan’s commercial paper issuance and a busy Breakpoint conference slate.

The derivatives markets turned more active this week, with open interest rising across both majors. BTC OI climbed 7.3% WoW, while ETH OI increased 4.5%, indicating fresh speculative positioning despite muted spot performance. Funding rates remained mildly positive but volatile, oscillating around neutral levels and suggesting positioning was added cautiously rather than aggressively. ETH briefly saw negative funding midweek, this bearish positioning and a lack of consensus, while BTC funding stayed positive but subdued.

Institutional flows saw their third straight positive week, strengthening materially even in last week’s extension. Crypto investment products recorded $1.64b in net inflows this week, the strongest print since early October and a clear acceleration from the prior two weeks. Bitcoin led with $432m of inflows, while Ethereum followed closely with $265m. Solana saw modest outflows, consistent with the supply-side pressures impacting price, while smaller inflows into XRP reflected selective positioning rather than broad risk-on behaviour.

A theme that’s been embedding itself of late is the uneven sector performance, reinforcing the market’s selective tone. Privacy was the sole sector gainer, up 2.6%, extending its recent narrative-driven resilience. Riskier and more speculative segments continued to underperform, with AI, Memecoins, and DeFi down 4-6% WoW, and DePIN leading losses, down 8.4%. The breadth of red across growth-oriented sectors suggests capital remains concentrated in majors and high-conviction themes, rather than rotating back down the risk curve.

This week’s price action reinforces a familiar pattern of accumulation and institutional inflows improving beneath the surface, but distribution and supply-side pressures continue to cap upside. Derivatives positioning is rebuilding cautiously, while sector performance shows capital remains highly selective. We expect majors to trade range-bound until there is a clear macro-level catalyst, but the continued return of institutional flows suggests the structural setup is improving.

Onchain Speculation Rebuilds

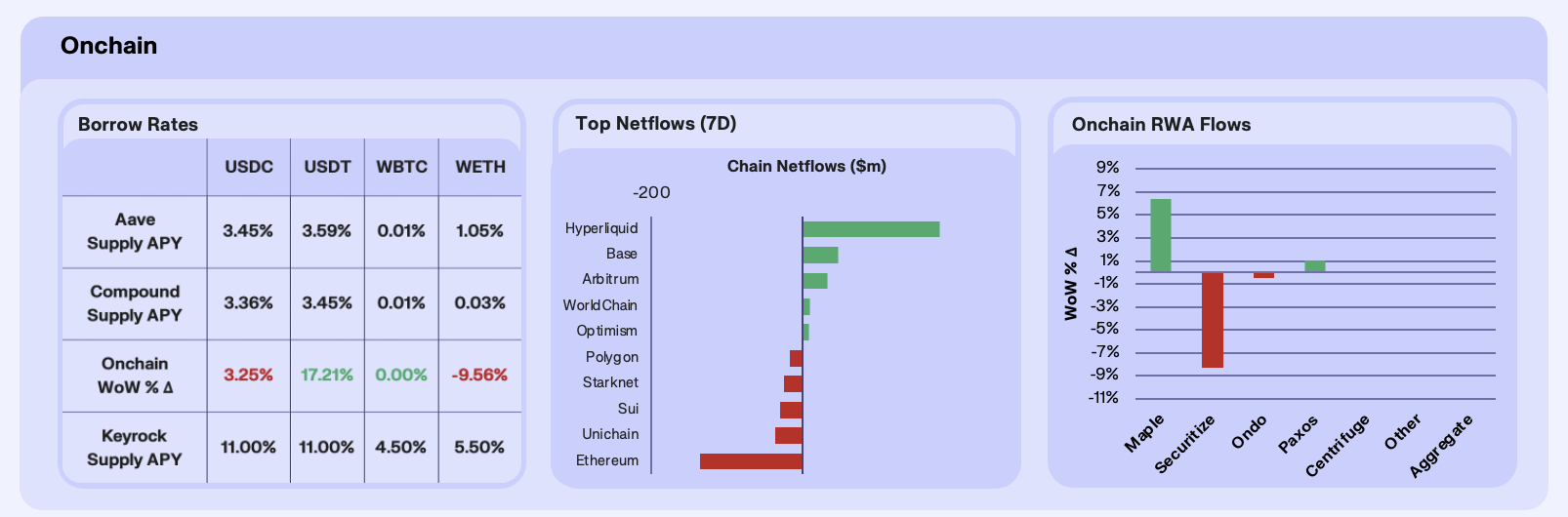

Onchain borrow rates signalled easing caution this week, with stablecoin yields ticking higher with USDC and USDT supply APYs rising 3.3% and 17.2% WoW respectively, driven largely by shifts in supply rather than a resurgence in borrowing demand. In contrast, WETH supply APY fell 9.6% WoW. This is what we typically see in the early innings of renewed confidence onchain, with capital flowing away from stables in sticky venues.

Chain netflows showed a clear rotation toward activity-heavy and speculative venues. Hyperliquid led with $182m of net inflows as traders returned to onchain perps. Base, up $48m, and Arbitrum, up $34m, also saw steady inflows, benefiting from their role as low-cost, liquid execution layers within the Ethereum ecosystem. Ethereum itself recorded $137m of net outflows as capital continued migrating to L2s, while Unichain, down $36m, saw liquidity rotate out toward more established or higher-throughput venues. The flow picture reinforces a familiar theme that capital is chasing yield and velocity, not passive settlement layers.

RWA flows were slightly negative at the aggregate level, with total AUM down 0.6% WoW. Ondo, up 3.4% and Paxos, up 2.6%, attracted inflows, supported by regulatory clarity and demand for tokenised treasuries and gold-linked products. In contrast, Securitize, down 5.9% saw outflows, likely reflecting short-term rebalancing rather than structural weakness. Despite the dip, RWAs continue to show relative resilience compared to broader DeFi activity.

Onchain markets are showing the first signs of renewed investor confidence. Borrowing demand is shifting in the right direction, and capital is rotating towards highly speculative venues. The data suggests capital is positioning selectively, leaving the onchain setup cleaner than price action alone would imply heading into year-end.

Predictive Superiority

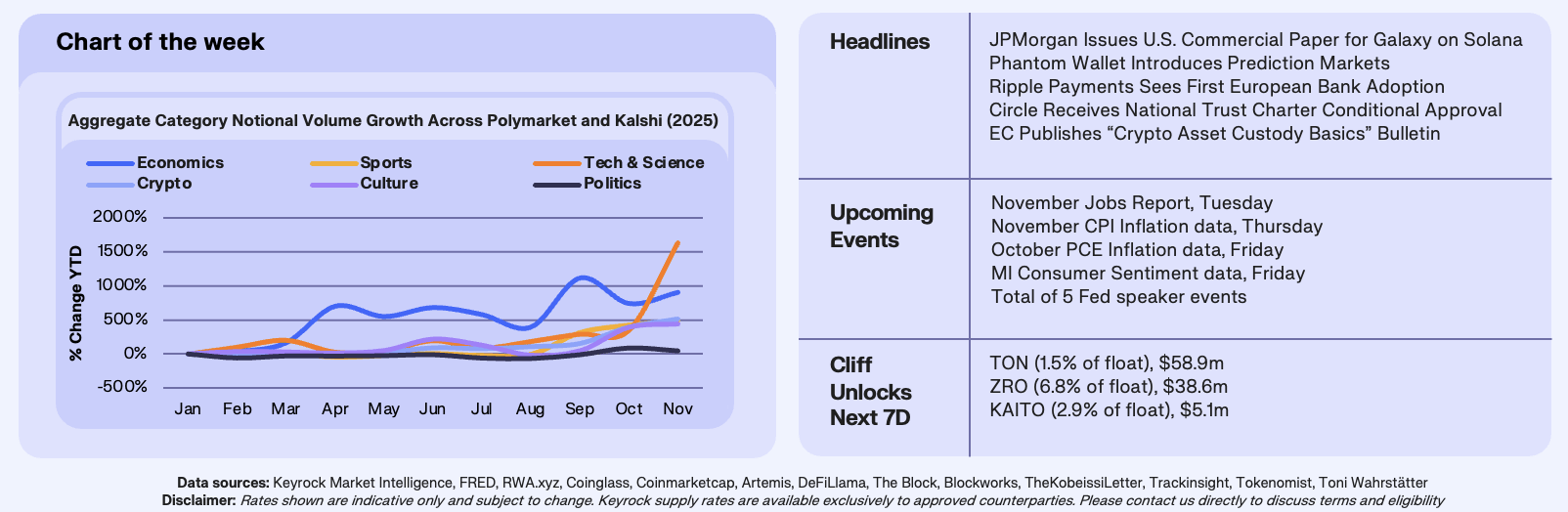

Aggregate monthly notional volumes across Kalshi and Polymarket have accelerated sharply since January 2025, highlighting a clear shift in how prediction markets are being used. Economics notional volume has grown 905% YTD to $112 million, while Tech & Science has surged 1,637% to $123 million, making it the fastest-growing category by percentage. The data suggest prediction markets are increasingly serving as tools for macro hedging and directional exposure, particularly to indicators such as inflation prints, rate decisions, and GDP revisions.

This growth contrasts with the Politics category, which remains dominant in absolute terms at roughly $1.2 billion in notional volume but is up a comparatively modest 43% YTD. The slower growth largely reflects base effects as politics has been a major category for years, so incremental volume naturally translates into smaller percentage gains. Taken together, the chart shows prediction markets broadening beyond event-driven political speculation toward continuous, economically relevant risk transfer. As macro volatility, policy uncertainty, and technological change persist, volumes are increasingly concentrating in categories that allow traders to express views on real-time economic and technological outcomes rather than discrete political events.

Our Take: The rapid growth in economics and tech-related markets signals that prediction markets are evolving into functional macro instruments, not just novelty betting venues. While politics will remain a cyclical driver during periods of heightened uncertainty, the center of gravity is shifting toward markets that enable hedging and price discovery around core economic variables. This trend strengthens the case for prediction markets as an emerging alternative venue for macro expression alongside traditional derivatives.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.