22 December 2025

Key Insights: Quiet into Christmas

Choppy After the Cut

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

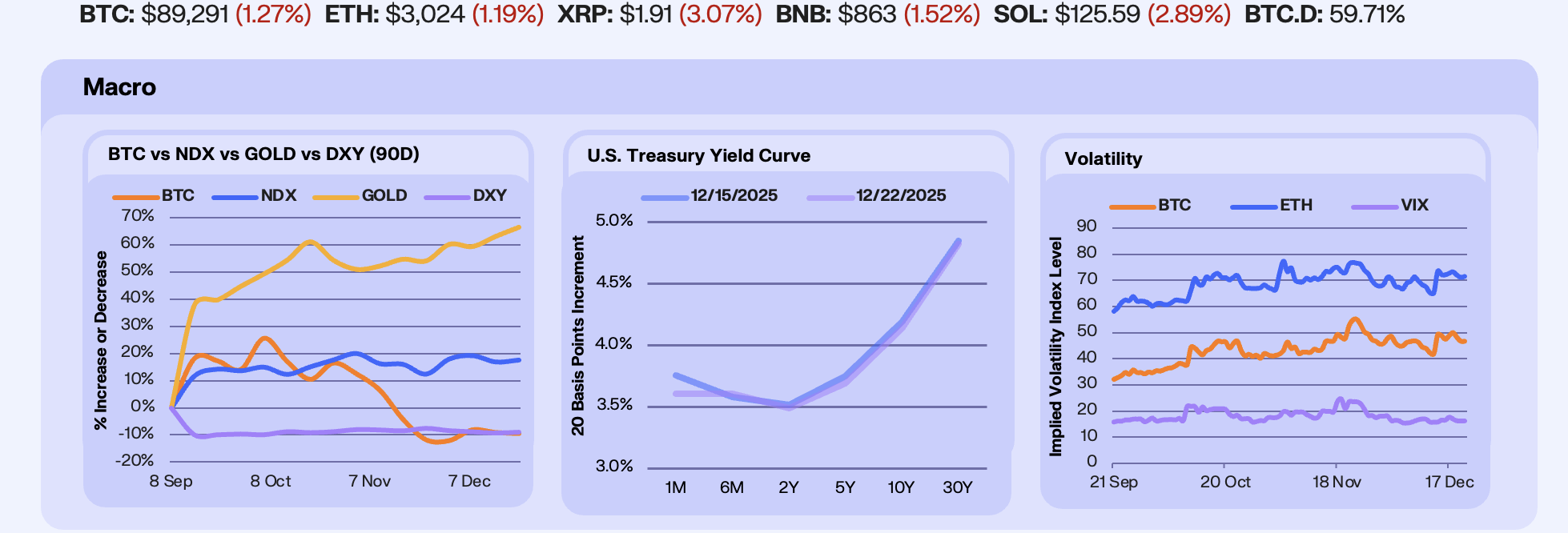

After a data-heavy and central-bank busy week, markets digested the deluge of information with a notably defensive tilt. Despite a softer than expected CPI print and confirmation of a widely anticipated 25bp Fed cut, risk assets failed to follow through. BTC slipped another 0.8% WoW to ~$89.1k, extending its drawdown to over 10% since late October, while Gold continued to grind higher, up 2.0% WoW to cycle highs near $4,387. U.S. equities remained range-bound, with the Nasdaq marginally higher, up 0.6% WoW, as AI-led optimism faded quickly after CPI and earnings-related margin concerns resurfaced. The dollar stayed heavy, with DXY roughly flat on the week but still down ~9% from its October highs, which we put down to easing expectations that are increasingly constrained by long-end rate pressure as opposed to front-end policy.

Treasury markets reflected this tension clearly, with a mild bull flattening led by the front end. The 1M yield fell 15bps WoW, while 2Y eased 3bps to 3.49%, consistent with markets anchoring around a slower, more data-dependent easing path following the December cut. The long end followed more cautiously, with 10Y down 5bps to 4.14% and 30Y easing 3bps to 4.82%, leaving the curve still deeply bowed and signalling persistent growth and fiscal concerns. Our takeaway from this data is that the market is increasingly confident that restrictive policy is behind us, even if neutral remains some distance away.

Volatility picked up modestly across assets, reflecting uncertainty and a risk-off stance. BTC 30D ATM IV rose 13.0% WoW to ~46.8, while ETH IV increased 9.5% to ~71.6, driven by short-dated demand around CPI and the Fed. Equities vol followed suit, with the VIX rising 2.9% WoW to ~16.2, still well contained by historical standards. The structure suggests hedging demand has returned, but without the disorderly positioning that typically accompanies macro stress events.

Our Take: The past week reinforced a late-cycle macro regime where easing expectations coexist with fragile risk appetite. While front-end relief from the Fed is increasingly priced in, long-end rates remain a constraint, keeping financial conditions tighter than the policy rate alone would suggest. Gold’s continued strength alongside range-bound equities and soft crypto highlights persistent demand for protection rather than duration risk. Until growth data stabilises more convincingly or long-end yields break lower, markets are likely to remain choppy, with liquidity improving at the margin but lacking conviction.

Year-End De-Risking

Price action across crypto markets remained heavy this week, with majors struggling to find traction as they become increasingly influenced by the broader defensive macro backdrop. Bitcoin drifted lower alongside equities, while Ethereum underperformed as positioning softened following last week’s Fed and CPI catalysts. The lack of follow-through after macro events kept risk appetite subdued, and crypto continued to trade as a liquidity-sensitive asset rather than an independent narrative. Solana was a relative bright spot, supported by sustained modest institutional inflows, but the broader market tone remained cautious.

Derivatives positioning de-risked further into year-end. BTC open interest fell 4.9% WoW to ~$58.2b, while ETH OI declined 3.2% to ~$37.7b, retracing a portion of the post-FOMC build-up. Funding rates stayed modestly positive for BTC but flipped negative at points for ETH, signalling fading directional conviction and a shift toward neutrality rather than aggressive shorting. The steady reduction in OI alongside muted funding suggests traders are lightening exposure rather than expressing strong downside views, consistent with a late-December positioning clean-up.

Institutional flows reversed sharply after two constructive weeks. Digital asset investment products recorded ~$529m of net outflows, driven primarily by Ethereum (-$422m) and Bitcoin (-$164m). Solana stood out with ~$58m of inflows, reinforcing its relative resilience versus ETH-linked products during this period. The return to net redemptions underscores how fragile institutional demand remains when macro uncertainty rises, and highlights that recent inflows were tactical rather than the start of a sustained allocation shift.

Privacy was the standout sector this week, up 9.7% WoW, with Zcash leading gains as capital rotated into defensive, non-yield-dependent narratives amid broader de-risking across crypto. The move appeared driven more by relative positioning and scarcity of leverage than by any single catalyst, as investors sought exposure less tied to fee growth or speculative activity. Separately, the ongoing Zcash Community Foundation (ZCF) elections drew renewed attention to the protocol’s governance and long-term direction. In contrast, risk-sensitive segments lagged meaningfully, with Perp DEX tokens falling 9.7%, and DePIN dropping 7.8%, reflecting continued aversion to leverage-dependent and growth-oriented fee narratives.

Our Take: This week marked a clear return to defensive positioning across crypto. Leverage continues to come off, institutional flows have turned negative again, and sector leadership is narrow and narrative-driven rather than beta-led. The resilience in privacy, particularly Zcash, shows capital is still willing to engage selectively where idiosyncratic catalysts exist, but the broader market remains constrained by macro uncertainty and year-end positioning.

Onchain Indecision

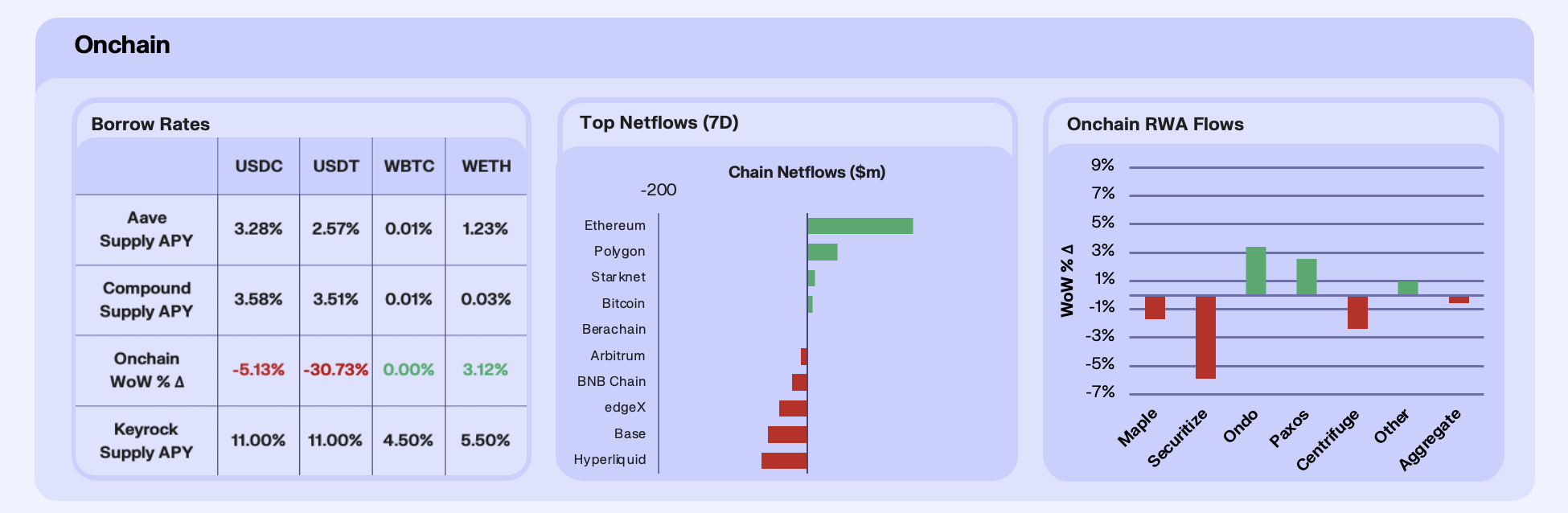

This week marked one of the first in several consecutive weeks where stablecoin yields softened across the board. On a WoW basis, USDC supply APY was down 5.1% and USDT down sharply by 30.7%, in both cases pointing to increased supply rather than stronger borrowing appetite. This supply-driven shift in APYs suggests capital is rotating back into low-risk yield generation venues and strategies as the market continues to chop, highlighting a capitulation on what appears to be a lack of sustained conviction in crypto-risk taking.

Chain netflows showed clear dispersion, with Ethereum leading inflows at +$178m, following the rollout of the Fusaka upgrade, which slashed average gas fees by ~97% and materially improved throughput. Lower execution costs appear to have pulled capital back to mainnet, even if only to test out the OG DeFi playground with its fancy new upgrade. We also believe that the above rates behaviour played a part here, with Aave liquidity and capacity being far deeper on Ethereum mainnet. On the other side, Hyperliquid, down $57m, and Base, down $55m, both saw outflows as capital rotated away from leverage-heavy execution venues synonymous with risk-taking.

RWA flows were notably strong at the aggregate level, with total AUM up 13.6% WoW, driven by a handful of large winners. Paxos, Securitize, and Ondo all saw inflows, supported by regulatory clarity and expanding tokenised equity and treasury offerings. In contrast, Maple experienced outflows, likely tied to institutional rebalancing ahead of CPI rather than a deterioration in fundamentals. It’s worth noting that the ongoing legal dispute with Core Foundation, stemming from the injunction over the syrupBTC product, likely exacerbated Maple’s TVL decline this week by fuelling institutional uncertainty, though we do not expect this to sustain. The standout came from the “Other” category, reflecting strong growth from infrastructure-led players such as Circle and emerging tokenised fund platforms. The core lesson from diving deeper here points towards consumers favouring institutional, compliant infrastructure over opaque structures.

Our Take: Onchain markets appear jittery in their willingness to commit to a risk-off, or risk-on stance. Typically this size of rotation into vanilla stablecoin lending signals a more sustained risk-off move, although recent behaviour suggests this time we may see more reactive flows should the macro lighten into the new year.

x402 Find PMF

This week’s chart of the week highlights x402, an open micropayments standard that enables low-cost, onchain pay-per-use payments for APIs, services, and AI agents. The chart shows the daily x402 payment volume share between Base and Solana, using data sourced from Artemis. Throughout the past month, the distribution across chains shifted meaningfully. Initially we saw Base consistently dominating activity, accounting for ~85-90% of daily volume, with Solana contributing only a marginal share often. However, from the 30th of November onward, Solana’s share accelerated sharply, with Solana processed ~$3m of x402 volume in the first 10 days of December alone, more than 3x its total November volume. This resulted in its daily share frequently exceeding 60-75% of total x402 volume, overtaking Base on a sustained basis.

The rotation in volume share seems to reflect a change in usage quality as opposed to activity levels. Early Base dominance coincided with elevated transaction sizes and highly concentrated bursts of volume, particularly around token launches and memecoin trading activity, which inflated notional volumes but lacked sustainability.

By contrast, Solana’s rise aligns with a sharp increase in agent-to-agent services, where volume is generated by high-frequency, low-value transactions. The data shows that as Solana’s share increased, average transaction sizes declined and total transaction counts rose, a pattern consistent with genuine micropayment usage rather than washtraded flows. Notably, despite industry-wide estimates that ~80% of x402 notional volume has been gamed, Solana-based servers accounted for the majority of the clean, recurring activity, driven by a small number of services handling thousands of payments per day at very low dollar values.

We believe we’re seeing a clear transition from speculative bootstrapping to early functional adoption. Base played a critical role in seeding x402 activity, particularly in November, when it processed nearly 90% of volume, but Solana is increasingly capturing where real usage is emerging, especially in agent-to-agent micropayments. With over $335m in cumulative x402 volume and 92m transactions since launch, there’s an underlying, constructive trend of falling transaction sizes, improving volume quality, and sustained usage on chains optimised for speed and cost.

Our Take: We see this as the early innings of a new onchain phenomenon, with the evolution from testing to the beginning of real usage. The shift in volume share suggests x402 is beginning to find product-market fit where it matters most, i.e. small, frequent, programmable payments. We expect the data to remain volatile in the near term, but structurally, this is a strong signal that x402 is evolving from narrative to infrastructure, and is here to stay long-term.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.