14 July 2025

Key Insights, Orange Is The New Gold

The Print Is Right

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

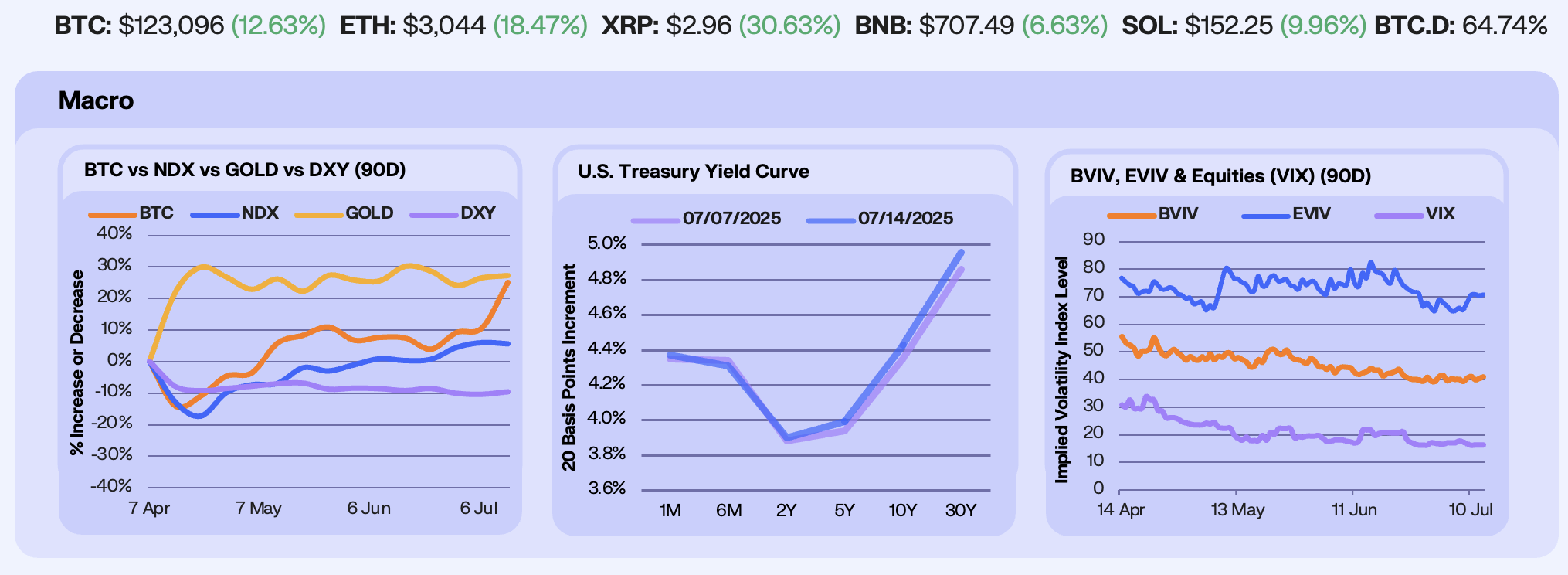

Last week, markets focused on concerns over U.S. fiscal spending and Trump’s tariff letters targeting numerous countries. Bitcoin surged to $122,875 to hit all-time highs (+12.9%), reinforcing its role as a hedge against both inflation and policy uncertainty. Meanwhile, the Nasdaq lagged (-0.4%), and the Dollar strengthened (+0.9%) on expectations of persistent U.S. yield premiums. Notably, the US Dollar is showing strong oversold signals, with speculative short positions by asset managers and leveraged funds dropping to their lowest levels since mid-2021.

The US Treasury yield curve steepened over the week, led again by longer-dated yields. The 10Y rising 8 bps and the 30Y climbing 10 bps, signalling a recalibration in duration risk and inflation expectations. Polymarket odds for no Fed rate cuts on July 30 and September 17 now stand at 93% and 42%, respectively, while U.S. recession odds for 2025 have fallen to 20%. With the next CPI print due July 15, markets appear to be grappling with supply-driven pressures in duration and shifting rate expectations at the front.

While Bitcoin’s Implied Volatility (IV) remains muted, Ethereum’s IV ticked up. Realised volatility remains compressed, and despite the slight uptick in front-end vols, gamma sellers continue to enjoy favourable carry. ETH saw a surge in call demand, led by strong open interest at the $3,200 strike. Call premiums from September onward remain elevated, signalling a growing bias toward upside risk into year end. With volatility and skew leaning upward, the market looks increasingly primed for follow-through.

Our Take: Markets are threading a delicate balance. While surface-level risk sentiment holds steady, underlying pressures from fiscal deficit and tariff-driven inflation remain unresolved. As broader markets trend higher, Ethereum is beginning to reflect shifting risk dynamics. A modest uptick in IV and its entry into a negative gamma zone (~$2,650–$3,500) suggest options flows are now fuelling volatility, not dampening it. Until ETH escapes that zone, expect sharper two-sided swings driven by dealer hedging.

The Pursuit of Orange

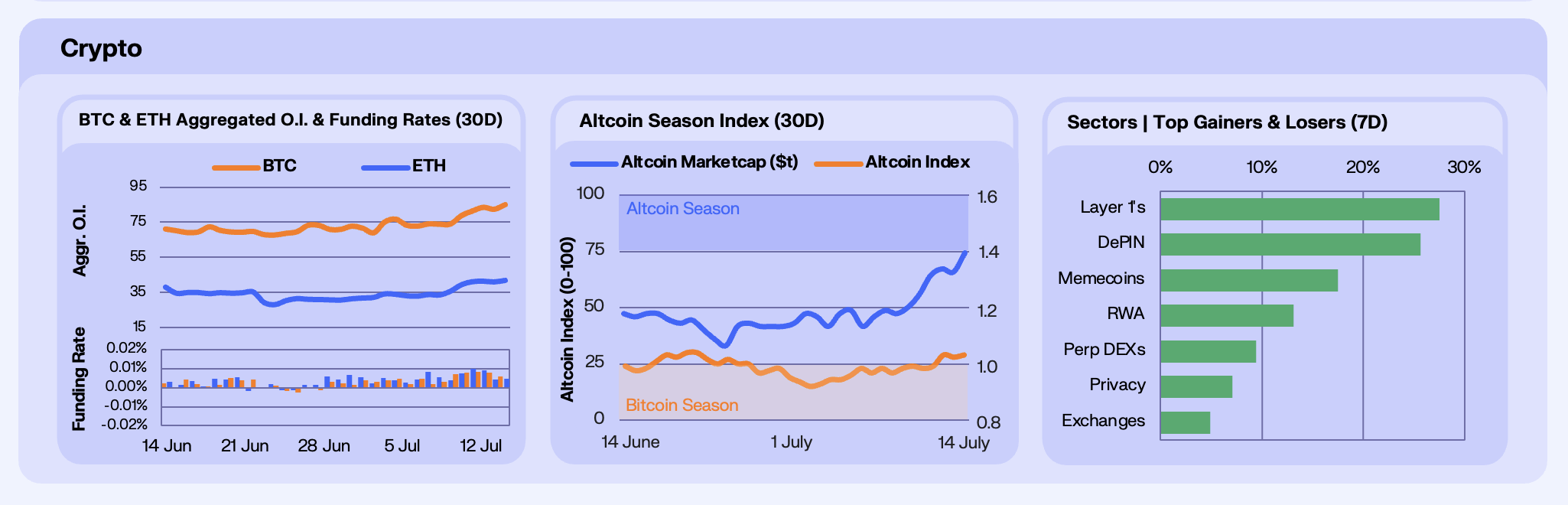

In the derivatives market, both Bitcoin and Ethereum saw all-time high open interest: Bitcoin rose from $74b to $85b (+12.2%) and Ethereum from $33.7b to $41.6b (+23.4%). This surge in positioning coincided with rising institutional ETH engagement. Large OI Holders of CME Ether Futures (≥25 contracts) climbed to 83, just shy of the all-time high of 86, and ETH CME futures open interest (7D SMA) climbed to $3.57b, its highest since February.

The increased activity drove Bitcoin and Ethereum funding rates to their highest levels so far in July while Bitcoin supply on exchanges hit all time lows. Meanwhile, futures volume data shows Bitcoin and Ethereum now share nearly identical 7DMA volumes at $51.49b and $53.52b, respectively. YTD, Bitcoin futures volume has trended down while Ethereum’s has risen, signalling a rotation of speculative interest toward ETH.

The Crypto market followed suit (+15%), led by Memecoin, DePIN, and L1 Network sectors. Memecoins surged following the Pump.fun public sale, DePIN rallied on strong user (1.04m DAU) and mobile sub growth (334k) from Helium, and L1 networks benefited from capital rotation into high-beta Ethereum-aligned plays.

Our Take: While Bitcoin continues to dominate headlines with new highs, data points to a quiet rotation beneath the surface. Ethereum is attracting sustained institutional attention, evidenced by rising CME futures engagement, 9 consecutive weeks of spot ETF inflows, and narrowing future volume gaps with BTC. This could mark the start of a broader catch-up trade, as ETH begins to reassert itself on growing interest in Ethereum-specific catalysts.

Safe Yield

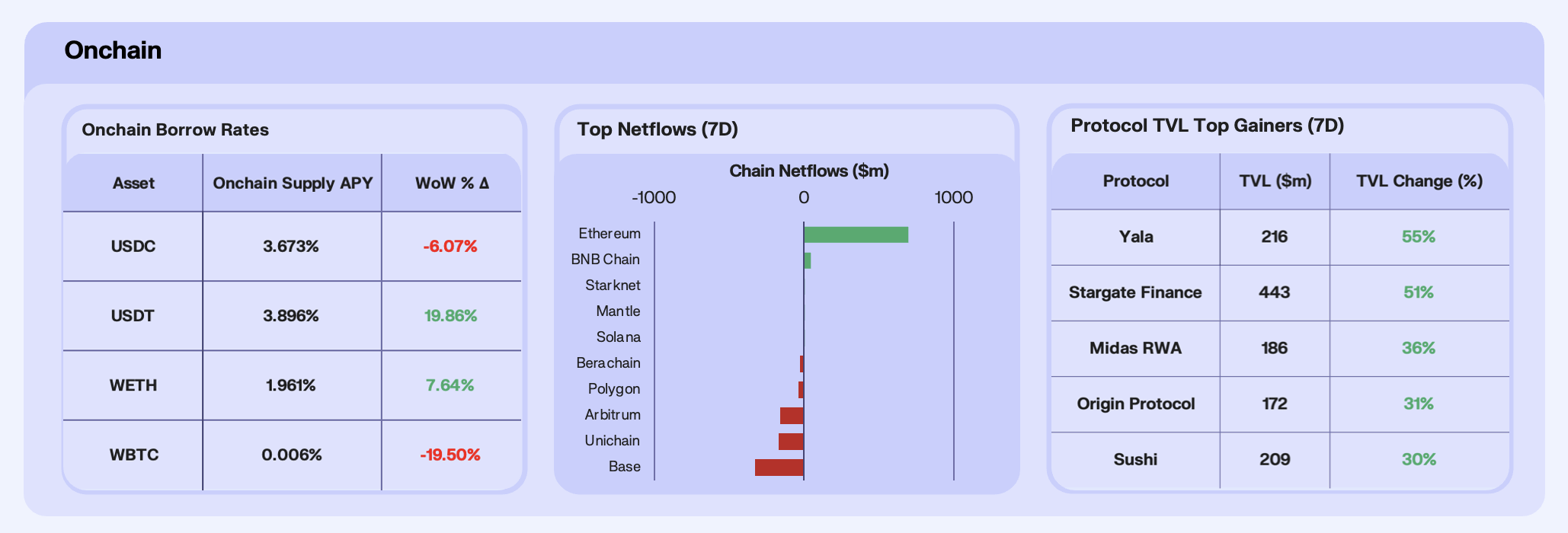

Onchain lending markets reflected meaningful shifts in token-specific supply-demand dynamics this week. USDC lending rates declined to 3.67% (–6.1% WoW) driven by a supply influx as TVL surged from $392.8m to $558m. This suggests lenders are increasingly parking capital in USDC following the recent GENIUS Act announcement, chasing yield in what’s perceived as the safest regulated dollar asset. USDT took a corresponding hit, losing ~35% of its TVL in its main Aave Ethereum pool, with rates rising 19.9% to 3.90% as a result. In the week that BTC hit all time highs, its onchain lending pool, specifically Aave on Ethereum, saw an ~$657m inflow as investors accumulated the orange coin and attempted to earn a modest yield on their investment. This supply influx, and also likely weak borrowing appetite, drove rates down 19.5% to 0.006%.

Capital rotation across chains this week saw sustained inflows to Ethereum, at $700m. Base saw the most significant outflow at ~$325m, driven by stablecoin redemptions, airdrop fatigue, and elevated fees during Base’s recent ‘blobscription’ events. Arbitrum posted ~$158m in outflows, in part due to the fallout from a recent GMX exploit that dented user confidence and liquidity across the chain. Unichain also saw ~$172m in exits, marking a cooldown after months of rapid growth. While Unichain had strong traction earlier in the year, the unwind reflects a broader post-hype adjustment, alongside likely delays or friction in deploying its validator network (UVN).

On the protocol side, Midas RWA (+36%) and Origin (+31%) benefited from growing demand for real-world assets and ETH-based yield. Capital is rotating into protocols offering tangible returns and incentives, even as altcoins gain and the market rallies.

Our Take: Capital is crowding into ‘safe yield’ despite the market moves this week, with USDC, Ethereum, and RWA protocols being the clear winners. We expect this to continue as onchain protocols and assets mature, both from a regulatory and product perspective.

ETH Locked In

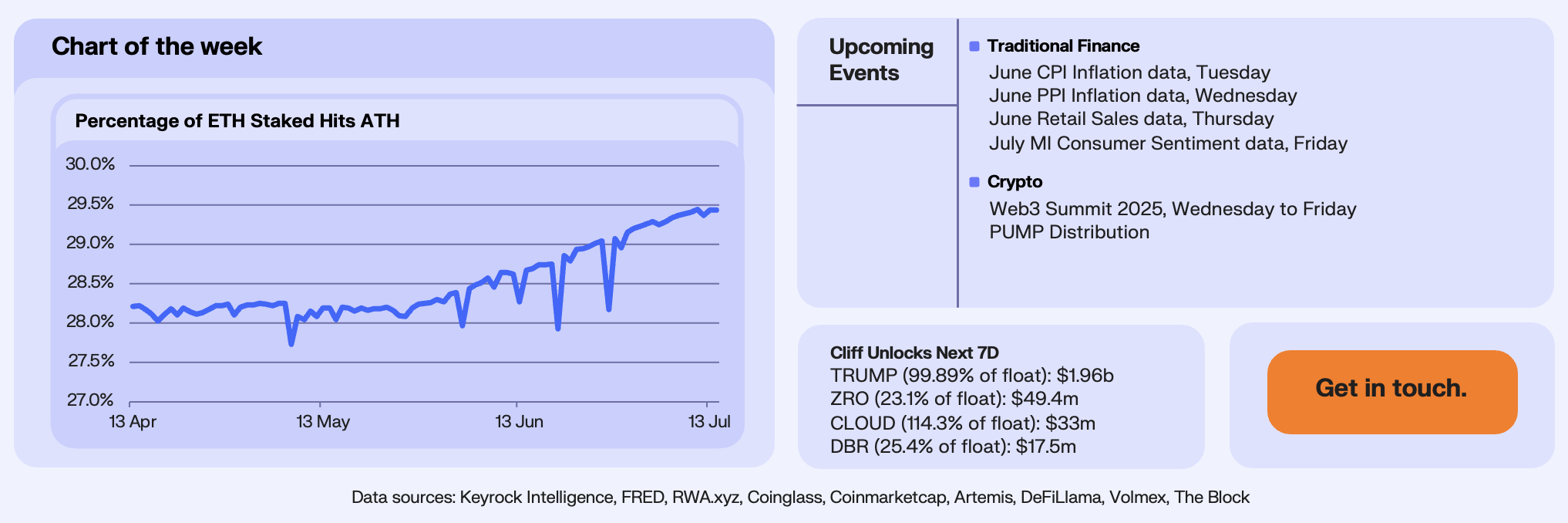

Ethereum’s supply dynamics have been shifting behind the scenes, reaching levels this week that have never been seen before. The percentage of total ETH supply staked has hit a new all-time high of 29.44%. This comes following a sharp acceleration in ETH staking rate, picking up 4.13% in the past month alone, reflecting deepening conviction in Ethereum’s long-term yield and security model.

Meanwhile, decision deadlines for ETH Staking ETFs range from June to October this year, with recent developments suggesting that momentum is building. REX Share’s SOL Staking ETF has sparked fresh optimism that that BlackRock and others are actively pressuring the SEC to approve Ethereum staking ETFs in the near future. The SEC’s guidance clarifying that protocol staking isn’t a securities offering is another development that removed a major regulatory hurdle. As mentioned previously, institutional demand for ETH is picking up, and a staked ETH ETF could provide exposure to the narrative of ‘ETH as yield-bearing crypto exposure’ that TradFi so desires.

Our Take: With staking participation at ATHs and decision deadlines for staking ETFs approaching, we see this as a pivotal moment for ETH supply dynamics. If approved, we believe this staking ETF catalyst could push the staking rate above 35% by year-end, driven predominantly by institutional demand.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.