Onchain Value: Stablecoins Now Drive Over ⅓ of DeFi Revenue

Key Findings

- Stablecoin revenue share rises in bull markets, not just in bears, powered by their central role in leverage loops, yield generation and vault strategies.

- Stablecoin revenue share is on the rise across DeFi after sinking to just 4.7% in June ’24, it’s now rebounded to a YTD high of 30.8%.

- Ethereum (25%) and L2s (23%) pull far more stablecoin-driven revenue than Solana (13%), highlighting their continued dominance in DeFi flows.

- In 2023, lending protocols earned far more from stablecoins than DEXes (65% vs. 20%) but that gap has now tightened to just 15% vs. 11%.

Prefer to listen? Dive into the audio version of our latest research and catch the insights on the go.

Introduction

Stablecoins, defined as dollar-pegged digital tokens offering price stability, are no longer simply a means of value transfer, they are now the backbone of the way DeFi works. They have evolved to become the de facto medium of exchange, collateral, and settlement for nearly every prominent DeFi application. Stablecoins facilitated more than $35t in on-chain settlements in 24’ alone, more than double Visa processes in a year, emphasising the role as crypto’s working liquidity financial stack.

Yet, while stablecoins are situated at the intersection of transactional flows, liquidity provision, and DeFi user behavior, there is an important axis left uncharted: How much do stablecoins actually contribute economic value to protocols? More precisely, what fraction of DeFi revenue, via trading fees, lending interest, etc., is triggered through stablecoin use?

Most existing work is concentrated on stablecoin supply, adoption, or transfer volume. Excellent headline growth and market penetration metrics that aren’t able to tackle the root problem of value capture: who gets financially rewarded from stablecoin activity and how much? As the stablecoin ecosystem evolves, and expands, albeit in a fragmented manner, across chains, protocols, and assets, quantifying its economic footprint matters.

This article fills that void. Through the analysis of stablecoin-driven revenue in top DeFi verticals, namely Decentralised Exchanges (DEXes) and lending protocols, and chains (Ethereum, Solana, Base, Arbitrum), we map the economic role of stablecoins in protocol revenues, how they have evolved over time, by chain, and how they respond to changing market conditions.

Whether you’re an investor tracking protocol viability, a developer evaluating product-market fit, or a stablecoin issuer searching for fresh integration opportunities, this report aims to help you better understand where and how stablecoins provide real financial value onchain, and what it means for the future of decentralised finance.

Resurgence in Stablecoin Revenue Contribution

Stablecoins, once thought of primarily as transactional rails, have grown into central building blocks of DeFi. But their influence hasn’t been static, the share of revenue they generate for protocols has been surprisingly volatile. Recently, however, this share has spiked upward again, and this tells us something deeper about the evolving dynamics of capital, risk appetite, and yield-seeking behavior across DeFi. In this section, we explore the drivers behind these shifts, from rising onchain stablecoin supply to changes in user behavior and market sentiment, to better understand the forces reshaping stablecoin-linked revenue generation in DeFi.

Since 21’, the share of DeFi protocol revenue attributable to stablecoins has been volatile, fluctuating between ~3.0% and peaks of ~35.8%. Most recently however, we’ve seen a renewed surge in stablecoin utility and usage in DeFi, through a sevenfold increase in stablecoin-driven revenue contribution, having compressed to just ~4.7% in June 24’ and since rebounded to a YTD high of ~30.8%.

This resurgence in stablecoin-derived revenue points to an important shift in DeFi; a renewed reliance on stablecoins, driven by a multitude of factors that we’ll explore, including onchain stablecoin supply, market sentiment, market volatility, and onchain stablecoin yields.

Onchain Stablecoin Supply

One key driver behind this surge is the rapid expansion of stablecoin supply. Since early 21’, total stablecoin market capitalisation has grown by ~$206b, a staggering ~750% increase, underscoring growing demand for dollar-pegged assets. But the critical question is: how much of this capital is being deployed into DeFi protocols, and what does it mean for revenue?

We can answer this by looking at how much of that fresh stablecoin capital remained on exchanges versus flowing into DeFi. The largest contributors to overall stablecoin growth during this period were USDT (+$129.86b) and USDC (+$54.25b), which we can use as a proxy for stablecoin flows. According to CryptoQuant, exchange wallet balances have absorbed around $39b in USDT and $8b in USDC since 21’, suggesting that the remaining $159b, ~77% of the increase in these two assets alone, likely resides onchain, where it has the potential to power DeFi protocols. This is a significant injection of stablecoin capital onchain over the past five years.

Here’s how this impacts DeFi, and specifically the extent to which it drove stablecoin revenue contribution increasing since June 24’. The injection of stablecoin capital boosts DeFi’s economic capacity. More capital onchain means greater support for lending markets, deeper DEX liquidity, and broader participation in yield-bearing strategies. So, as stablecoin liquidity grows, capital efficiency improves: spreads narrow, slippage falls, and protocols that monetise stablecoin flow generate more revenue.

Market Sentiment

Market sentiment also plays a key role. Stablecoins are DeFi’s native risk-off instrument, offering safety when markets turn. In volatile conditions, users rotate into stables, borrowing them, pooling them, and trading against them, reinforcing both demand and utility across lending protocols and DEXs alike.

Surprisingly, and rather counterintuitive to this, stablecoin revenue often rises alongside bullish market conditions. Since January 24’, we’ve seen the share of stablecoin-derived fees increase even as crypto prices rally. During these periods, capital doesn’t rotate out of stables, it accelerates into them, powering leveraged strategies, stable-pair trading, and deeper engagement across DeFi.

Of course, not all moves are linear. In June and October 24’, the correlation broke down as crypto momentum faded. During these slower months, stablecoin activity was likely driven by capital preservation rather than aggressive DeFi engagement. Generally speaking though, our analysis shows that market sentiment is a strong driver of the extent to which stablecoins contribute to DeFi revenue.

Market Volatility

Looking at stablecoin revenue alongside market volatility, a deeper story emerges. By comparing stablecoin revenue share to BTC’s implied volatility, we uncover shifting behavior across regimes that reveal how volatility influences stablecoin usage.

Interestingly, as you can see above, the percentage of revenue derived from stablecoins tracks market volatility incredibly closely. We even see stablecoin revenue contribution leading volatility ever so slightly, likely as sentiment shifts and markets move towards capital-efficient, stablecoin-centric strategies, such as looping on lending platforms.

Of late, there has been a decoupling between the two, with volatility suppressing while stablecoin revenue contribution continued to grow. Bitcoin as an asset is heavily macro-influenced, and this volatility suppression can be traced back to VIX suppression, which measures the market’s expectation of 30-day volatility in the S&P 500. For the driver here, we don’t have to look much further than the White House. At the beginning of the year we saw volatility spikes due to U.S. tariff announcements. However, by May, markets began pricing in these risks more efficiently, with BlackRock’s Q2 outlook noting stabalising sentiment. This adaptation reduced fear as traders grew less reactive to trade policy shocks. So why, then, did this buck the correlation between BVOL and stablecoin revenue contribution? We attribute this to our aforementioned market sentiment analysis, in which price action and derived sentiment drove stable-centric leverage strategies.

Onchain Stablecoin Yields

A final factor we’ll explore as a potential driver for the percentage of revenue coming from stablecoins in DeFi is stablecoin yields in onchain lending protocols. Using USDC borrow rates on Aave V2 and V3 as a proxy, we observe a clear relationship between yield levels and the proportion of DeFi revenue derived from stablecoin activity.

This relationship is intuitive: when users aggressively borrow stables to execute looping strategies or chase yields elsewhere, they push borrow rates up, and in doing so, drive revenue for the protocol. Conversely, when demand to borrow stables falls, rates compress, and so does revenue. These two metrics aren’t just correlated, they’re causally linked. The more users borrow stablecoins, the more they pay for that privilege, and the more the protocol earns as a result.

Through November 24’ to February 25’, we see this dynamic play out as borrowing demand softened and yields fell from ~16% to ~6%, dragging stablecoin-derived lending revenue down with it.

The big picture takeaway is that borrow rates aren’t just a cost of capital, they’re a real-time signal of how deeply stablecoins are being used in lending protocols. High yields tell us users are paying up to access stablecoin liquidity, often to chase risk or amplify exposure. Low yields suggest stablecoin borrowing is less appealing, and that DeFi capital may be rotating elsewhere. Either way, yields act as a barometer for the intensity of stablecoin activity onchain.

Stablecoin Cyclicality on DEXes

As stablecoins continue to evolve, their influence across DeFi becomes more nuanced. To truly understand their impact, we need to move beyond the top-line figures and examine where, and how, stablecoins generate revenue. Not all parts of the DeFi stack rely on stables equally. Some, like DEXes, use them for liquidity and composability, while others, like lending platforms, rely on them as the primary engine of economic activity.

DEXes remain the dominant source of protocol-level revenue in DeFi. Their role as a proxy for capital flows and user behaviour makes them a useful lens into how stablecoins function within the broader ecosystem. This said, not all DEXes follow the same underlying protocol design. The relative contribution of stablecoins to DEX revenue varies meaningfully over time, shaped by shifts in sentiment, strategy, and market infrastructure. In this section, we’ll explore how this composition has evolved, and what it tells us about DeFi’s increasing structural reliance on stablecoin capital.

Since 21’, the stablecoin share of DEX-derived revenue has exhibited clear cyclicality, reflecting the interplay between market sentiment, liquidity conditions, and protocol design. At its peak in mid-22’, stablecoins accounted for approximately 30% of total DEX revenue. This spike coincided with the aftermath of the Terra/Luna collapse and broader systemic deleveraging, during which traders increasingly turned to stable-paired swaps, such as USDC/ETH, as a risk-off hedge in the face of acute market stress. Onchain pair dominance data confirms this temporary behavioral shift; the share of USDC/ETH trading volume surged relative to WBTC/ETH, underscoring the elevated demand for stable-paired liquidity as volatility spiked. In parallel, deteriorating liquidity in volatile assets led to widening slippage, making stable pairs more attractive for execution from both a cost and predictability perspective.

Over the past year, however, stablecoin-derived DEX revenue has begun to recover, climbing from ~10% in early 24’ to ~20% by mid-25’. This rebound is not simply a return to risk-aversion, it is the product of structural tailwinds that are reshaping how stablecoins are used across DeFi. One of the most important of these drivers is the rapid growth of onchain yield protocols and AMM vaults. From January 24’ to February 25’, TVL in onchain yield products grew from ~$3.8b to ~$12b, with platforms like Pendle leading the expansion. Pendle, in particular, enables fixed and variable yield trading by tokenising future yield streams, most of which are backed by stablecoin deposits. This model has created a self-reinforcing flywheel: rising demand for yield-bearing stable assets deepens stablecoin liquidity pools, which increases trade volume on those pairs, in turn generating more fees and attracting further liquidity.

What we’re seeing is a transition in how stablecoins are used within DeFi. No longer confined to risk-off positioning, stablecoins are increasingly embedded within proactive capital allocation and yield optimisation strategies. Their rising contribution to DEX revenue is a reflection not just of macro volatility, but of DeFi’s growing sophistication and structural dependence on stablecoin infrastructure.

Uniswap

Uniswap’s multichain deployments provide a powerful view into how stablecoin dynamics shift across different DeFi environments. While Uniswap remains a dominant venue for volatile asset trading, our analysis shows that stablecoins are increasingly embedded in fee generation, albeit unevenly across chains.

On Ethereum, stablecoin activity tends to spike in response to moments of macro stress or product-driven surges. On Arbitrum, the trend appears more structural, with stable-pair usage supported by low gas costs and strategy-heavy user behavior. Meanwhile, Base remains primarily speculative, with stablecoins only just beginning to play a role in its fee mix. These divergent patterns reflect how stablecoin usage is shaped not just by market conditions, but by infrastructure, user intent, and the maturity of onchain financial products. In the sections that follow, we unpack each chain’s unique trajectory in detail.

Ethereum’s Macro Sensitive Stablecoin Contribution

Ethereum L1 remains the dominant stablecoin chain, as of May 25’ accounting for 53.6% of onchain stablecoin supply. It would be expected that this centrality would give it a structurally higher baseline of stablecoin derived revenue relative to most chains. However, due to high gas fees and complex transaction costs, DeFi use cases that drive stablecoin revenue such as yield strategies and looping aren’t practical on mainnet. As a result, stablecoin revenue on Ethereum tends to be episodic, spiking during periods of market stress, rather than persistent or transactional in nature.

Up until mid-22’, non-stablecoin pairs were consistently growing in their contribution to Uniswap revenue, peaking at ~37% in June 22’, during the aforementioned post-Luna contagion period. We’ve since seen volatility that’s culminated in a gradual increase in stablecoin revenue contribution since early 23’, which we attribute to renewed demand for structured DeFi products, many of which rely heavily on stablecoin liquidity. There are other potential factors at play here, such as the introduction of Uniswap v3 in May 21’, which introduced custom fee tiers, where stable-stable pairs trade at significantly lower fees due to their tight price ranges, however the impact of these factors are relatively muted.

On Ethereum, stablecoin-derived revenue remains a product of macro-driven flow, not day-to-day usage.

Arbitrum’s Favourable Stablecoin Environment

Arbitrum differs structurally to Ethereum, in that it is a lower fee environment designed for higher transaction count with lower latency. This environment makes frequent swaps viable, especially for LP strategies, arbitrage, or vault executions that involve stable assets. The result is that on Arbitrum, Uniswap exhibits a consistently higher baseline of stablecoin revenue compared to Ethereum. From 23’ through early 25’, stable pairs contributed ~20-30% of total DEX revenue, without the same level of macro-driven spikes as on Ethereum.

Arbitrum’s user base is also more DeFi-native, with active participation in looping protocols, stablecoin borrowing, and yield farming. Many of these users rely on frequent stable pair interactions as part of their core strategy. Additionally, ecosystems like GMX, which historically used USDC as a core margin and liquidity asset, have conditioned trader behavior toward stablecoin usage even outside of derivatives protocols using fee mechanisms.

The stablecoin revenue share here appears to be structural, driven by user behavior and protocol design, not reactive like on Ethereum.

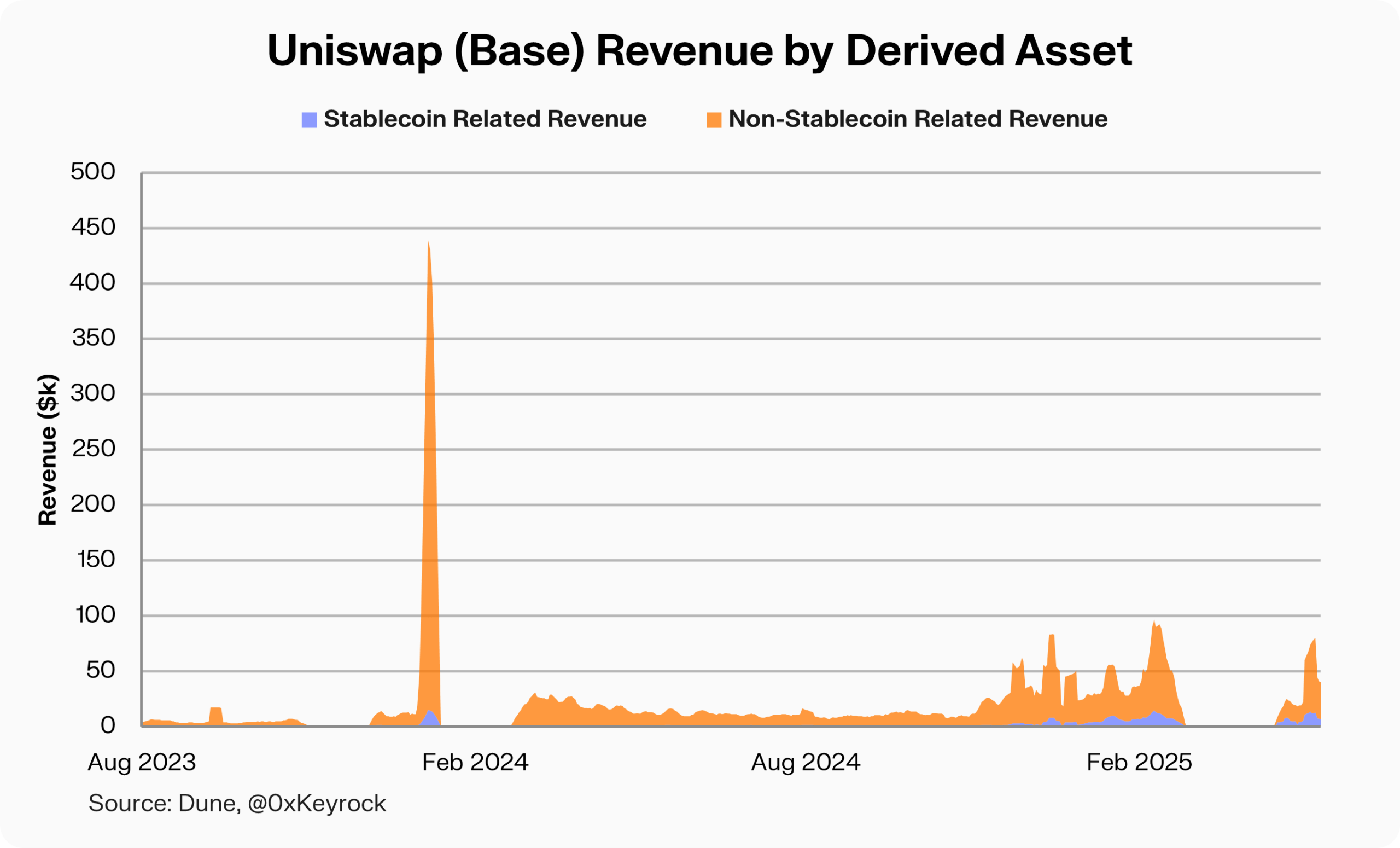

Nascent Base’s Underdeveloped Stablecoin Stack

Uniswap on Base has historically told a different story altogether, that reflects a nascent ecosystem dominated by speculative, predominantly memecoin, activity.

Since Base’s launch in mid-23’, non-stablecoin revenue consistently exceeded 90%, with stable-paired swaps contributing only a small fraction of protocol fees, until recently. This is characteristic of new chains where altcoin trading and memecoin speculation dominate early usage. Liquidity is often concentrated in volatile assets, with fewer structured products or stablecoin yield loops in play.

However, since the start of the year we’ve seen stablecoin revenue on Base pick up materially, peaking at above 25%. This shift reflects more than just a maturing market, it marks Base’s emergence as a stablecoin-native chain. Transaction fees are low, throughput is high, and USDC enjoys native integration thanks to Coinbase’s deep alignment with Circle. This alignment has enabled stablecoins to flow more easily onchain. The uptick corresponds loosely with a sharp increase in stablecoin supply on Base, which grew from less than $0.5b in January 24’ to ~$4.5b in May 25’, per Artemis. The rise in stablecoin revenue contribution also coincides with broader infrastructure tailwinds, most notably Chainlink’s CCIP, which makes it seamless and secure to bridge stables across chains. This interoperability, coupled with the growing footprint of stable-backed DeFi strategies and enterprise-grade payment integrations, is steadily enhancing Base’s ability to act as a hub for stablecoin liquidity.

Curve

Curve was purpose built for stablecoins, and for years, this showed up in the data. As a protocol built for low-slippage trading between pegged assets, Curve established itself early on as Ethereum’s stablecoin liquidity backbone. This was primarily driven by the dominance of its flagship 3pool, comprising USDC, USDT, and DAI.

But by 22’, the picture changed. Stablecoin revenue collapsed as Curve’s ecosystem pivoted to volatile-asset pools via its Factory architecture. Users utilised these pools for governance bribes and CRV emissions, with non-stable swaps at one point generating over 75% of fees. The Curve Wars era rewarded protocols that could mobilise liquidity, not necessarily in stablecoins.

This trend has since reversed, and stablecoin-derived revenue recovered to ~40-50% by early 25’, as emissions-fueled speculation cooled and demand returned for lower-risk, predictable yield. MetaPools and interest-bearing stable derivatives also added new fuel to stablecoin derived revenue streams. While Curve now supports both stable and volatile assets, its core remains rooted in stablecoin efficiency, a sharp contrast to Uniswap’s volatility-driven design.

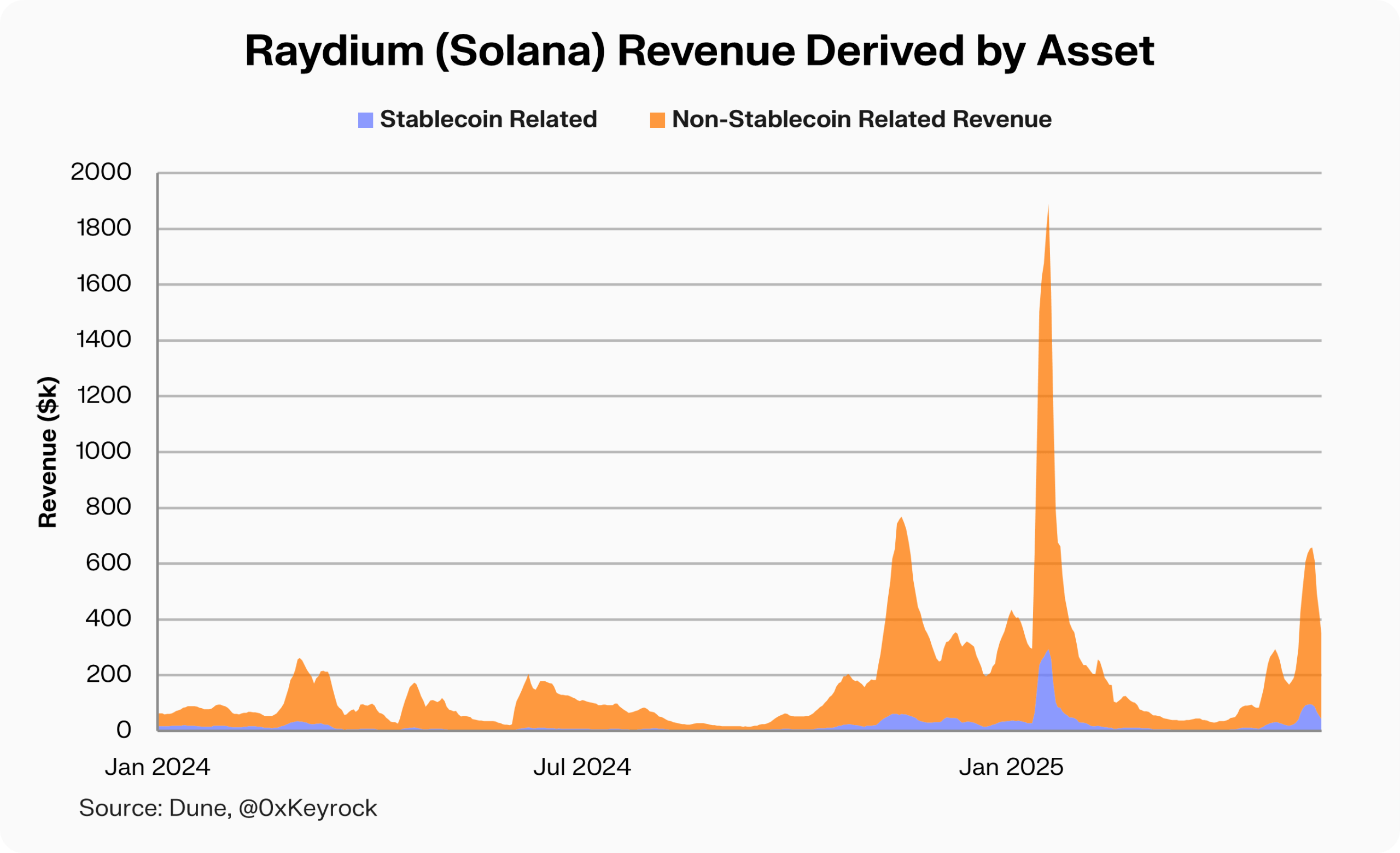

Raydium

Solana as a blockchain has a vastly different user base relative to its EVM counterparts, in which it is more akin to nascent Base activity, dominated by speculation and memecoin activity. As such, the revenue derived by Raydium, the dominant DEX on Solana, is, and has consistently been, dominated by non-stablecoin assets. Since early 24’, more than 80% of Raydium’s revenue has consistently been derived from volatile trading pairs, far higher than Uniswap or Curve. This is no anomaly. On Solana, memecoins are overwhelmingly paired with SOL upon graduation from Pump.Fun, not USD-pegged stablecoins. As a result, stablecoin swaps play only a marginal role in driving protocol revenue.

This is as much architectural as it is behavioural. Solana lacks a native stablecoin-first DEX like Curve, and its low gas fees encourage high-frequency trading of volatile tokens. With fewer structured products or stablecoin farming strategies in place, activity tends to cluster around speculative trades, reinforcing Raydium’s double-sided volatile pair dominance. Moreover, Solana has been slow in its stablecoin onboarding, with only $13b in stablecoin AUM versus $127b on Ethereum mainnet, which structurally limits the extent to which stablecoins can contribute to revenue on the chain. This is seen more as a consequence of the user behaviour and architectural design, as opposed to a driver of the lack of stablecoin revenue contribution.

While signs of a stablecoin stack are emerging, via UXD, Kamino, these remain early-stage. Until stable-backed strategies mature and gain traction, Raydium’s fee flows will continue to reflect Solana’s identity as a memecoin-led, SOL-denominated trading hub.

Erosion of Stablecoin Dominance in Lending Markets

Lending protocols have long been powered by stablecoins, but 25’ marks a break from the norm. For years, platforms like Aave were defined by stablecoin activity, borrowers sought USDC and DAI for leverage or hedging, and lenders supplied them for steady returns. As a result, stablecoins routinely drove the majority of protocol revenue, often exceeding 70% of lending fees. But today, that dominance is fading.

What we’re now seeing is a structural shift in borrower behavior. Stablecoin-derived revenue has declined sharply since late 24’, hitting a multi-year low of just 12% in April 25’. This drop signals more than a temporary blip, it’s a reflection of both rising risk appetite amongst users and the growing use of volatile assets as loan collateral. This is partly a result of deepening liquidity of volatile assets on DEXes, which in turn pushes said assets over liquidation requirements for listing on lending protocols. The lending stack is evolving, and with it, the economic role of stablecoins.

Aave

As the largest and longest-standing lending protocol in DeFi, Aave provides one of the clearest windows into how stablecoin activity manifests across chains and market regimes. When viewed across Ethereum, Arbitrum, and Base, Aave’s data reveals both structural similarities and meaningful differences in revenue composition, driven by distinct liquidity profiles, user behavior, and cost structures on each network. The key findings here are that relative Aave stablecoin revenue has been gradually declining across all chains, while there have been sporadic fluctuations in stablecoin revenue contribution. Note, this does not take into account revenue derived from GHO.

Ethereum’s Established Stablecoin Activity

Aave on Ethereum is synonymous with stablecoin lending. For much of DeFi’s history, over 75% of revenue here came from borrowing USDC, USDT, and DAI, a pattern driven by institutional use, high loan sizes, and the preference for stable leverage. However, Ethereum mainnet is costly, and this has shaped usage. While large users are still willing to absorb high fees for size and security, strategies that require frequent looping or transaction-intensive yield farming, the kinds that drive persistent stablecoin revenue on L2s, are less viable here.

The most interesting thing about this Aave on Ethereum chart is the sporadic spikes seen in revenue. Note this graph utilises seven day average data, which slightly stretches the impact, but the driver here is temporary, event-driven. For example, in October 24’, USDC borrow rates on Aave v3 Ethereum briefly spiked to ~41%, likely triggering users to borrow volatile assets instead of stables, shifting the revenue mix temporarily and spiking stablecoin revenue. These moments often align with sharp market moves or incentivised lending programs, and do not indicate a sustained change in lending behaviour.

Consistent Stablecoin Lending on Arbitrum

If Ethereum is where stablecoin lending pulses with market cycles, Arbitrum is where it thrives structurally. From mid-23’ onwards, stablecoin revenue on Aave Arbitrum has consistently dominated, often accounting for over 70% of protocol fees. This reflects Arbitrum’s design as a low-fee, high-throughput environment, the ideal setting for strategies that involve borrowing stables, looping into LPs, or deploying capital into leveraged yield positions.

Unlike on Ethereum, these behaviors don’t require macro stress to materialise. They’re woven into the day-to-day usage of the network. Borrowing is cheaper, rates are more responsive, and users, often more DeFi-native, optimise for capital efficiency. This creates a reliable flywheel for stablecoin demand. Volatile asset borrowing still exists, but it’s secondary to the utility of stablecoins as tools for strategy execution. In this way, Arbitrum Aave represents the blueprint for stablecoin-led lending activity on modern L2s.

Base’s Expanding Stablecoin Supply

Aave’s deployment on Base is the newest of the three, and its revenue profile is still taking shape, much like our observation with Uniswap’s deployment here. At launch, stablecoins made up most lending activity, consistent with initial capital being parked in low-risk strategies. But by Q4 24’, that flipped. Stablecoin revenue briefly dipped below non-stable assets, as users began to borrow cbETH and wstETH to gain directional exposure, a sign of the speculative culture that has characterised Base’s early usage.

That’s started to shift again. Since Q1 25’, stablecoin borrowing has accelerated, with stables once again contributing the majority of Aave Base revenue. This rebound coincides with a broader rise in Base’s stablecoin supply, alongside a push from Coinbase and Circle to make Base the chain of choice for stable-backed finance. Combined with CCIP integration and deeper onchain liquidity, Aave on Base may yet evolve into another stablecoin-heavy venue.

Kamino

Kamino launched as Solana’s first structured lending protocol, attracting users with delta-neutral loops and yield strategies built on stablecoin liquidity. In these early months, over 75% of lending revenue came from stables, reflecting a preference for lower-risk, income-generating strategies on a platform explicitly designed to support them.

From mid-24’ through early 25’ we see stablecoin dominance decline, coinciding with Solana’s explosive memecoin season. Tokens like $WIF and $BODEN captured enormous market attention, fueling a broader wave of speculative trading and leveraged positioning. As these memecoins graduated from platforms like Pump.fun and became tradable on major Solana DEXes, demand surged for native tokens like SOL and related volatile assets. Kamino, which had by then expanded support for non-stable collateral and borrow options, saw a significant shift in activity.

With the decline in memecoin attention, stablecoin revenue contribution has been revived. This underscores an interesting truth about stablecoins contribution to revenue in Solana DeFi, in that it is highly dependent on speculative secular trends. We forecast this to continue, given the user base and lack of demand for stablecoin-centric use cases.

Implications

For protocol design and strategy, the data is clear: stablecoin heavy protocols deliver more consistent, defensible revenue during market downturns. Their reliance on dollar-denominated activity makes them less sensitive to risk sentiment, positioning them as infrastructure-like plays in DeFi. By contrast, protocols dependent on volatile assets see revenue expand rapidly in bull markets but suffer sharp contractions during risk-off periods. This dynamic introduces a strategic trade-off between stability and upside. Protocol architects must ask whether they want predictable, yield-like flows or volatile, beta-driven spikes. Emerging DeFi products should consider embedding stablecoin mechanics, i.e. looping, leverage, fixed yield, as core design elements. These mechanisms not only attract sticky capital but also create opportunities for recursive demand.

When looking at infrastructure, gas costs remain one of the most important drivers of stablecoin activity onchain. Low-fee environments like Arbitrum and Solana have unlocked stablecoin strategies that are impractical on mainnet Ethereum. These include high-frequency trading on stable pairs, recursive leverage via borrowing loops, and frequent rebalancing in vaults. Protocols looking to grow TVL and volumes should optimise for integration with the stablecoin yield stack, i.e. Pendle, Ethena, Euler, Kamino. These platforms have created new financial rails on top of stablecoin primitives, catalysing activity in both lending and trading. The implications for a chain like Ethereum appear daunting, even though mainnet currently dominates in terms of stablecoin TVL. We predict this dominance will decline gradually over the coming year as lower-fee environments are adopted for yield generating primitives. For newer chains like Base or ecosystems still in formation, building native stablecoin infrastructure should be a top priority to capture consistent, sticky revenue flows.

But what about the issuers themselves? The most economically impactful stablecoins are those deeply embedded in leverage, trading, and yield primitives. Issuers must prioritise integrations that drive velocity: lending markets with looping strategies, AMMs with deep stablecoin pools, and yield protocols that tokenise rate exposure. Platforms like Pendle, Ethena, Euler, and Kamino are now among the highest-value targets for strategic alignment. These integrations not only deepen usage but also create sustainable demand for the underlying stablecoin. Issuers that don’t embed themselves in onchain economic engines risk stagnation.

Conclusion

Stablecoins continue to underpin DeFi’s economic foundation, serving as the primary medium for lending, trading, and structured financial strategies. While their dominance has historically been assumed, this report shows it is far from static, instead, stablecoin-derived revenue fluctuates meaningfully across time, chains, and market conditions.

We find that stablecoin fee share rises during periods of market uncertainty, and contracts as risk appetite returns and speculative assets surge. Lending markets still lean heavily on stablecoins, though usage is increasingly cyclical, while DEX activity reflects each chain’s infrastructure maturity and native user behavior.

In sum, the percentage of revenue derived from stablecoins is a useful lens into broader DeFi sentiment, a live indicator of how risk is being priced, how users behave, and how protocols monetise the shift between safety and speculation.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.