Onchain Asset Management: Designing the Future of Investment Strategies

Written by Ben Harvey

Read the Full Report

Preface

The most comprehensive report on onchain asset management is here. From the early days of experimental vaults to today’s billion-dollar discretionary strategies, we map the ecosystem reshaping how capital is allocated onchain.

We break down four key categories; automated yield, discretionary strategies, onchain credit, and structured products, and analyse the flows, fees, and performance trends driving 118% AUM growth YTD. Looking ahead, we forecast the market to scale to $64-85 billion by 2026, read why in the article below, with insights from the industry’s leading companies.

Access the full report here

Executive Summary

Onchain asset management has experienced phenomenal momentum in 2025, with assets under management (AUM) across automated yield strategies, discretionary strategies, structured products, and credit more than doubling year-to-date to over $35 billion. Growth has been broad-based, but led by discretionary onchain strategies which rose 738% YTD.

Performance comparisons remain competitive. Gross APYs range from 7.5% in credit to 10.3% in structured products, with discretionary strategies averaging 9.7% and automated yield steady at 8.0%. Net of fees, returns narrow, but remain broadly in line with traditional finance equivalents.

The clearest takeaway is that onchain strategies are no longer an experiment. They are delivering competitive, risk-adjusted returns with greater transparency, programmability, and composability than traditional peers.

Forward projections see AUM reaching between $41.6 billion and $85 billion by 2026. Growth is expected to come from institutional capital, whitelisted pools, compliant treasury regimes, regulatory clarity, and ongoing infrastructure improvements.

Mapping the Onchain Asset Management Landscape

The $145 trillion global asset management industry remains weighed down by inefficiencies such as high fees, settlement delays, and limited access. Retail investors are excluded by large minimums, while back-office reconciliations still dominate operations.

Blockchain offers an alternative, with programmable, transparent systems where assets move and settle in real time. Settlements are executed in seconds rather than days, securities are tokenised and traded 24/7, and collateral can be pledged or returned automatically.

The ‘DeFi Summer’ of 2020 marked the first wave of tools enabling serious capital allocation. Uniswap proved onchain trading at scale, Aave and Compound turned lending into button clicks, and Yearn Finance automated yield aggregation. Stablecoins bridged traditional and onchain capital, growing from $10 billion in 2020 to over $263 billion today.

Onchain asset management today is defined as the allocation of digital assets, be that crypto-native or tokenised real-world assets, through blockchain-based infrastructure, executed via smart contracts and recorded on public ledgers. Within this report, we categories onchain asset management strategies into four sub-sections:

- Automated Yield: Vaults that optimise returns across lending, liquidity provision, and staking.

- Discretionary Strategies: Actively managed portfolios with real-time allocation and risk management.

- Structured Products: Derivative-based payoff profiles with automated settlement.

- Credit Strategies: Lending and underwriting onchain, including unsecured and permissioned pools.

Automated Onchain Yield Strategies

Automated yield strategies deploy capital programmatically across lending, liquidity, and staking protocols. They act as integrators, plugging into existing infrastructure to optimise yield, rather than originating it themselves.

The first generation emerged during ‘DeFi Summer’ in 2020. Yearn Finance pioneered automated vaults, reallocating funds between Aave, Compound, and Uniswap to capture the best returns. Automated yield strategies have resurged strongly in 2025, with AUM reaching ~$17.5 billion. Morpho leads with ~$9.6 billion AUM, while Yearn remains a significant player with ~$750 million.

Automated vaults most closely resemble short-duration fixed income funds (SDFIs), with money market funds (MMFs) as a secondary comparator. Both traditional and onchain products seek low-risk yield on idle capital, though onchain vaults operate programmatically with instant settlement. Whereas traditional funds derive yield from treasuries, corporate paper, or repos, onchain vaults earn from lending stablecoins, staking assets like stETH, or looping strategies.

The benefits of automated onchain yield strategies lie first in their accessibility. These vaults are permissionless, meaning anyone with a wallet can participate without going through intermediaries or account setup.

Another major advantage is liquidity, with deposits and withdrawals able to be executed in real time, with vault tokens updating instantly to reflect accrued yield. This stands in contrast to the settlement delays of traditional products, where even highly liquid funds can take one or two days to redeem.

Transparency is also radically different onchain, with every allocation, transaction, and performance metric recorded and visible to anyone. Investors do not need to rely on quarterly statements or daily NAV reports, instead they can independently verify, in real time, how capital is deployed.

However, automated vaults are not without drawbacks. Chief among them is smart contract risk. These strategies rely on code to allocate capital, and when code fails, whether through bugs or exploits, funds are at risk. The 2024 Yearn v1 DAI vault exploit, which drained $11 million, is a stark reminder of this vulnerability. Unlike traditional funds backed by regulated custodians, automated vaults have no equivalent safety net.

Average costs for automated onchain yield strategies are around 1.50% annually, reflecting layers of management, withdrawal charges, and operational costs of deploying capital across protocols. Traditional passive products, on the other hand, operate at razor-thin margins, with the Vanguard Federal Money Market Fund charging 0.11%, while leading ETFs like iShares and SPDR short-duration bond funds charge as little as 0.04-0.07%, averaging just 0.08%.

Despite this disadvantage, onchain vaults retain a performance edge. Gross yields averaged 7.95% in 2025, compared to 4.67% in traditional benchmarks. After deducting higher fees, net yields landed at 6.45%, still ~186 basis points above traditional funds. This suggests that investors are effectively paying a premium for programmability, transparency, global accessibility, and composability. These are all features that are either unavailable or complex to structure in the legacy system. While scale advantages will likely compress fees in the future, today the spread demonstrates that automated onchain yield strategies are structurally capable of outperforming their traditional peers.

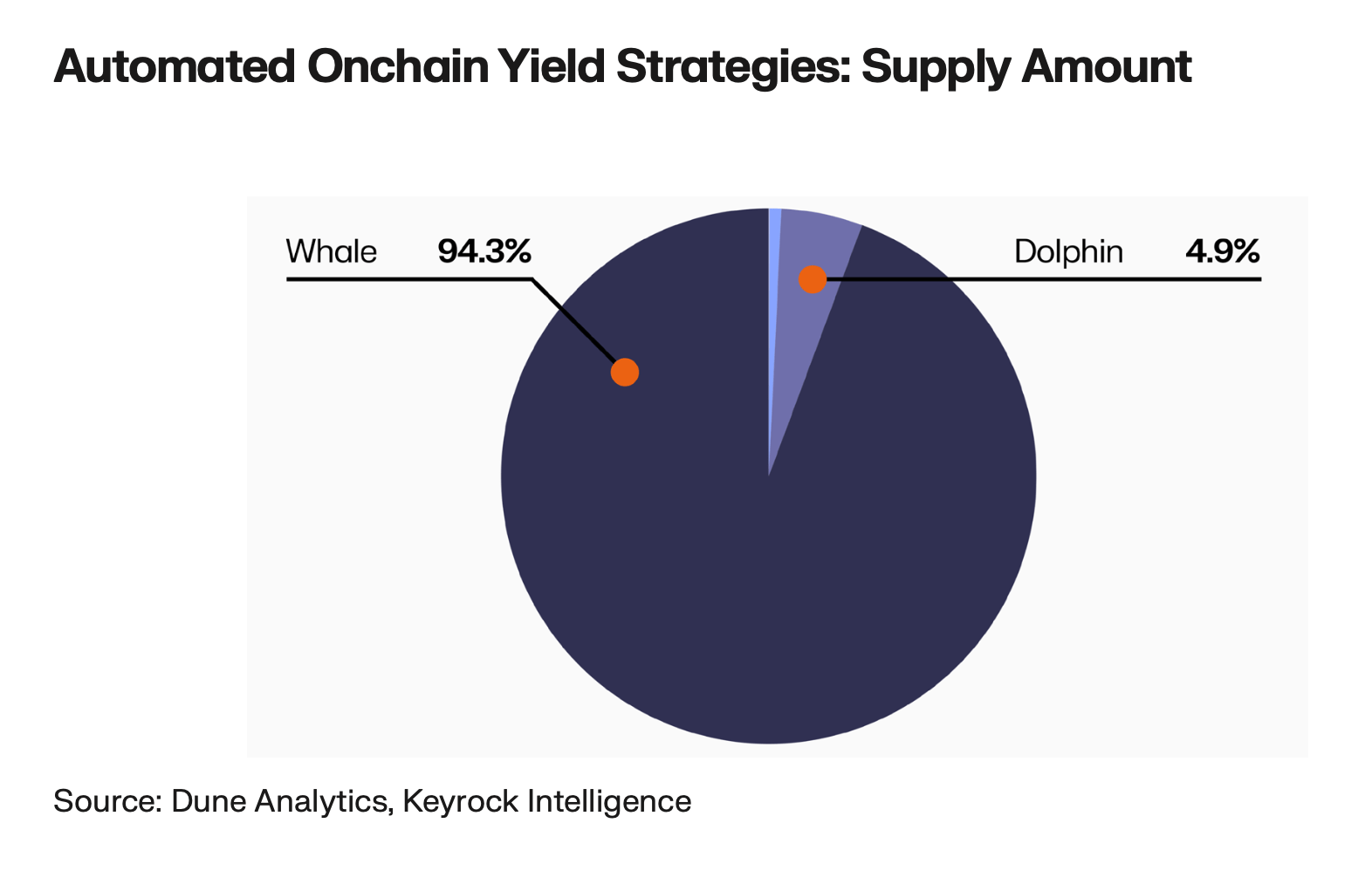

Most depositors are retail addresses (<$10k), but their capital share is negligible. Instead, whales (> $1m) and dolphins ($100k–$1m) account for over 99% of AUM, highlighting that institutional allocators are driving flows.

Several forces are set to drive further growth, which you can read in detail by downloading the full PDF report. The introduction of ERC-4626 has standardised vault tokens, turning them into plug-and-play building blocks. This enables easier integration into fund-of-fund structures, simplifies accounting, and lowers the cost of developing new products. For institutional allocators, this standardisation is critical, as it reduces the technical barriers to adopting vaults at scale.

Integration with new asset classes is another driver. Vaults now include strategies that package liquid staking derivatives like stETH and cbETH, as well as tokenised T-bills, producing yields that are both competitive with traditional markets and instantly liquid. This expansion beyond purely crypto-native assets makes vaults attractive to more risk-averse allocators seeking transparent, dollar-denominated products.

Discretionary Onchain Strategies

Discretionary onchain strategies involve active management of positions across DeFi protocols, with portfolio allocation and risk management decisions made in real time. Unlike automated vaults that rely on predefined logic, discretionary strategies are directed by managers who rotate between opportunities, hedge exposures, or capture inefficiencies using proprietary research and execution.

Discretionary strategies emerged later than automated vaults, initially as niche experiments run by crypto-native managers. Their growth accelerated as infrastructure matured and more sophisticated tools became available. Managers began to design bespoke strategies that could react to market shifts on short notice, using live onchain data to inform allocation. This approach blurred the line between traditional hedge fund strategies and onchain execution, combining discretionary decision-making with the speed and transparency of blockchain rails.

The segment has grown rapidly in 2025, with AUM rising by 738% year-to-date. This surge reflects both the credibility discretionary managers have built and the appetite allocators have for strategies that go beyond passive yield. Today, discretionary strategies represent one of the fastest-growing segments of onchain asset management, commanding billions in AUM and attracting both crypto-native and traditional allocators.

The closest analogues in traditional finance are hedge funds and actively managed mutual funds. Both rely on manager discretion to identify opportunities, allocate capital, and manage risk.

The primary benefit of discretionary onchain strategies is flexibility, in that managers can respond instantly to market conditions, shifting exposures in minutes rather than days. This agility allows them to capture inefficiencies, rotate between yield sources, and dynamically manage leverage or hedges.

Many discretionary strategies also allow investors to redeem capital on demand, rather than being locked into quarterly or annual redemption cycles, making redemption liquidity a major benefit. This combination of hedge-fund-style management with daily or even instant liquidity makes them an attractive option for allocators seeking both active management and flexibility.

However, discretionary onchain strategies are not without challenges. They carry all the inherent risks of DeFi, including smart contract vulnerabilities, collateral volatility, and reliance on still-maturing infrastructure. Manager discretion introduces an additional layer of risk, as outcomes depend on the skill and judgment of individuals or teams, rather than purely on code. Performance dispersion can be high, with successful managers delivering strong returns while others underperform.

Gross performance has been strong, with discretionary strategies delivering average APYs of around 9.7% in 2025. Net of fees, returns narrow but remain competitive with traditional hedge funds. This suggests that discretionary onchain strategies are capable of matching their offchain counterparts, even when factoring in costs. Importantly, the liquidity advantage remains intact: investors gain hedge-fund-like performance but with the added benefit of being able to enter and exit more fluidly.

Fees themselves are still higher than those of automated vaults, reflecting the active management involved. Yet allocators appear willing to pay for the combination of discretion, transparency, and liquidity that these strategies offer. As competition intensifies and institutional capital enters at scale, fee structures are likely to compress, but today they remain a meaningful source of revenue for managers.

Discretionary strategies are increasingly attracting larger allocators. While retail participants remain present, the bulk of capital comes from whales and institutions seeking differentiated exposure. The transparency and liquidity of these strategies have made them appealing to allocators who want active management but are wary of the opacity and lock-ups typical of hedge funds. Crypto-native funds and family offices have been early adopters, with traditional institutions beginning to explore allocations as infrastructure matures.

Several factors are expected to drive continued expansion, led by the growing sophistication of onchain infrastructure, the availability of real-time data and analytics, institutional adoption and, as touched on already in more passive style strategies, composability.

Credit Strategies in Onchain Asset Management

Onchain credit strategies bring the mechanics of lending and borrowing into a blockchain-native environment. At their core, these strategies involve underwriting, structuring, or tranching credit risk directly onchain, often through permissioned pools or tokenised loan instruments. Rather than simply facilitating peer-to-peer lending, credit strategies aim to replicate and enhance the functions of traditional credit markets, with programmatic repayment flows, transparent performance, and smart contract-based risk management.

Platforms like Maple Finance introduced permissioned lending pools, enabling institutions to borrow unsecured capital from onchain depositors. Others, such as Gondi, applied similar concepts with different structures, targeting both crypto-native borrowers and traditional entities seeking blockchain-based financing. These innovations marked the transition from simple overcollateralised lending to true credit markets onchain.

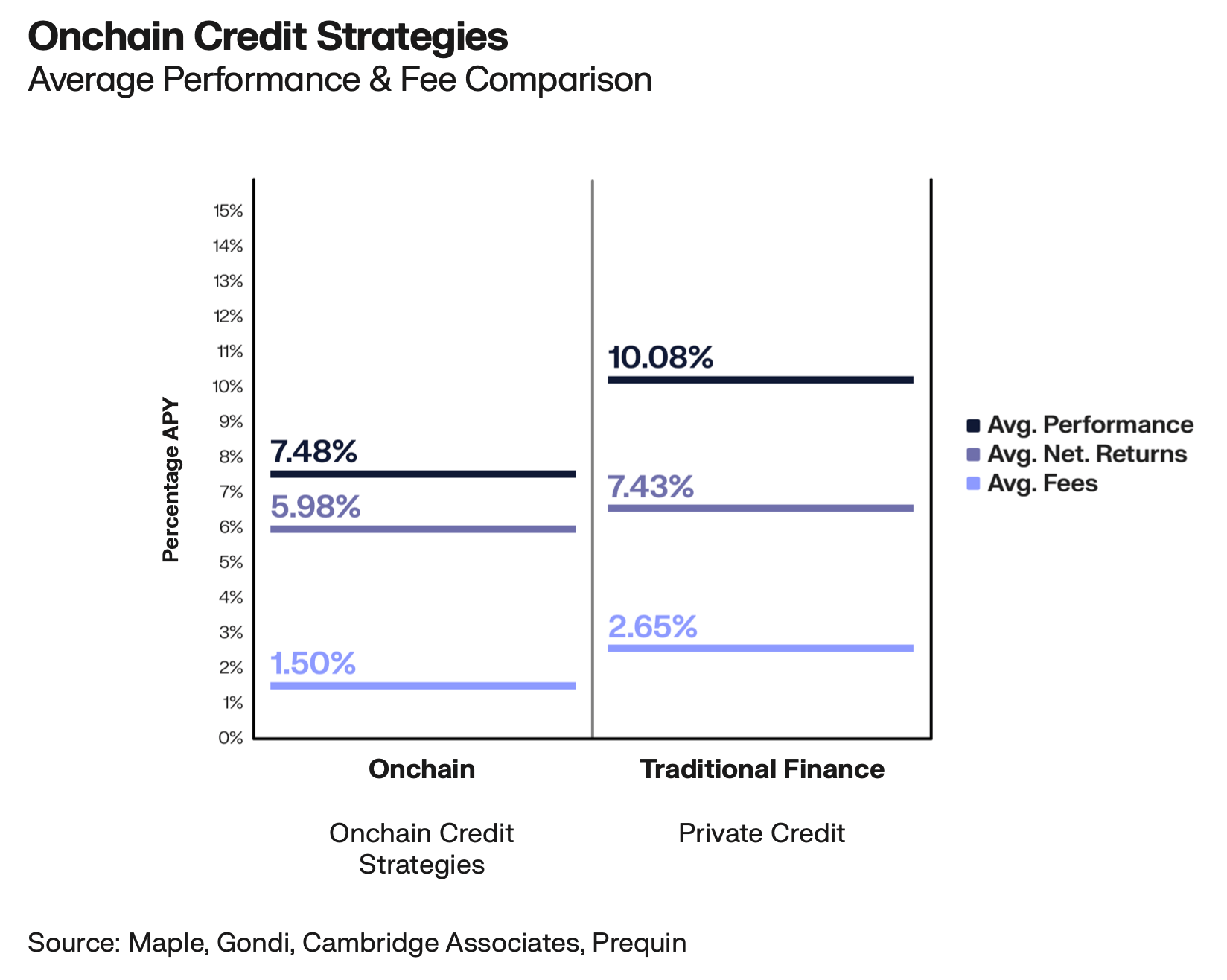

Credit strategies have grown steadily and now represent a significant share of onchain asset management. Products such as SyrupUSDC illustrate the increasing demand for unsecured or undercollateralised credit. In 2025, AUM in this segment expanded meaningfully, as institutional borrowers sought onchain financing and allocators pursued yields above those available in automated vaults. Gross APYs across credit strategies averaged 7.5%, making them competitive with other strategy categories.

The closest traditional analogues are private credit funds and direct lending vehicles. Like their onchain counterparts, they provide loans to businesses or institutions, often outside the scope of public markets. However, traditional credit funds typically operate with limited transparency, quarterly reporting, and illiquidity.

Onchain credit strategies differ by embedding transparency and programmability into the process. Loan issuance, repayment schedules, and collateralisation are recorded onchain and can be monitored in real time. Settlement is faster, and in some cases, programmable repayment flows can automate what would otherwise require manual back-office work. That said, scale and regulatory frameworks remain far more developed in traditional credit markets, limiting how quickly onchain strategies can compete head-to-head.

Gross yields for onchain credit strategies averaged 7.5% APY in 2025. After fees, performance narrows, leaving net returns slightly below those of automated yield or discretionary strategies. Fees typically range between 1-2%, reflecting the higher operational costs of underwriting, borrower monitoring, and structuring loans.

Compared to private credit funds, which often charge management and performance fees, onchain protocols are relatively lean. However, the smaller scale of these platforms means that allocators cannot yet access the same diversification benefits available in multi-billion-dollar traditional funds. Despite these limitations, onchain credit remains attractive because yields remain competitive while offering programmability and transparency not available in traditional markets.

Allocators to onchain credit are typically larger, more risk-tolerant players. Retail participation is limited, as permissioned pools and KYC requirements often restrict access. Instead, the bulk of capital comes from crypto-native funds, family offices, and increasingly, institutional investors experimenting with permissioned environments. These allocators are motivated by the potential to earn above-average yields while gaining early exposure to an emerging market segment.

The future growth of onchain credit strategies will be driven by several factors. Institutional adoption is at the forefront, as permissioned pools and compliant frameworks give traditional allocators the confidence to deploy capital. As regulatory clarity improves, these pools are likely to scale significantly, bridging the gap between DeFi-native credit and traditional private lending. For more detail here, please download the full report PDF.

Onchain Structured Products

Structured products in traditional finance are derivative-based instruments that package yield and payoff profiles to meet specific risk-return preferences. Onchain structured product strategies take this concept into the blockchain environment, creating programmable payoff tokens that deliver defined exposures such as covered calls, puts, or basis trades. By embedding payoff logic directly into smart contracts, these products replicate and extend traditional structures in a transparent, composable, and accessible way.

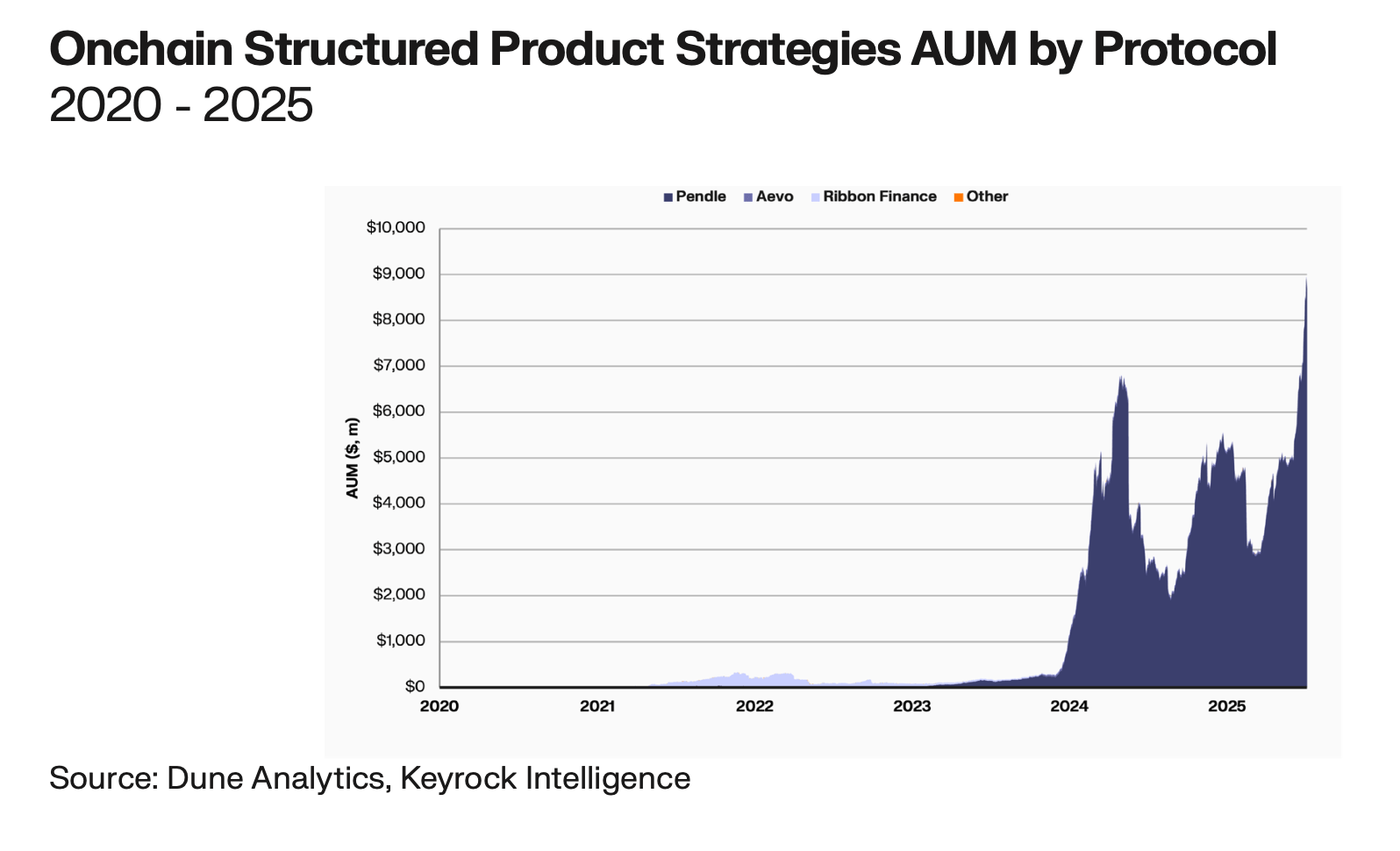

The sector’s turning point from an adoption perspective came with the rise of Pendle, which allowed users to split yield-bearing assets into principal and yield components. This innovation enabled traders and allocators to speculate directly on interest rates, duration, and yield curves in a way that traditional markets had never offered with the same transparency and composability. By 2025, onchain structured products had matured into a multi-billion-dollar segment, with offerings spanning from option-based yield vaults to structured tokens backed by RWAs.

The closest comparisons are structured notes and derivative-based yield enhancement products offered by banks. Both provide defined payoff profiles that tailor exposures to specific investor needs. However, the differences are stark. Traditional structured notes are typically illiquid until maturity, involve counterparty risk with the issuing bank, and offer limited transparency into underlying exposures.

The benefits of having structured products onchain stem from the strategies being freely transferable, programmability, and composability. The drawbacks, however, remain significant. The products rely heavily on smart contracts and oracles, creating new vectors for technical failure or manipulation. Fee structures can also erode returns, with multiple layers of protocol, trading, and liquidity costs embedded in some products.

Structured products have delivered the strongest gross yields among onchain strategies, averaging 10.3% APY in 2025. After fees, which range from 1-2%, net performance narrows but remains competitive. Fees are justified by the operational complexity of managing derivatives and ensuring continuous market-making for structured payoffs.

The primary allocators to onchain structured products are sophisticated retail traders, crypto-native funds, and high-net-worth investors seeking yield enhancement. Unlike automated vaults, where whales dominate, structured products attract a more diverse set of participants. The allure of double-digit gross yields and the ability to tailor exposures has drawn in a wide spectrum of allocators, from individuals experimenting with small deposits to funds managing institutional-size positions.

Institutional participation remains limited but is beginning to grow, particularly in permissioned environments. As compliance frameworks mature and whitelisted pools become standard, larger allocators are expected to increase exposure to structured products as part of diversified yield strategies.

Future growth will likely be driven by innovation in product design. The ability to tokenise and tranche cash flows expands the range of possible payoff profiles well beyond traditional finance. Integration with RWAs is another catalyst. By linking tokenised treasuries, loans, or commodities to structured payoffs, protocols can create products that directly mirror traditional financial exposures, while adding onchain advantages like programmability and liquidity.

Infrastructure improvements, particularly in oracles and risk management, will also drive adoption. More robust oracle systems will reduce manipulation risks, while enhanced margining and collateral management will allow structured products to scale safely. Finally, regulatory clarity will be critical. As structured products gain attention, frameworks that allow institutional allocators to participate without fear of compliance breaches will unlock the next wave of inflows.

Capital Flows, Fees & Performance

Capital concentration is high, with whales and dolphins accounting for 70–99% of AUM, while retail users supply less than 1% of capital despite making up most depositors.

Generally speaking, fees are materially higher than in traditional finance. Automated yield vaults charge ~1.5%, compared to ~0.08% for money market funds. Despite this, net performance skews in favour of onchain strategies, with outperformance of 230-380 basis points across most categories.

Performance, however, is not universally higher. Credit and structured product strategies lag slightly after fees, while automated yield vaults and discretionary strategies remain competitive.

Forecasts and Trends

Institutional adoption will be the next growth driver. Whitelisted pools, compliant treasury management, and tokenised treasuries are expected to accelerate inflows. DAO treasuries and stablecoin integrations are already major depositors.

Our base case forecasts AUM reaching $64 billion by 2026, with a bull case of $85 billion and a bear case of $41.6 billion. Catalysts include regulatory clarity, infrastructure improvements, and institutional capital deployment.

Conclusion

Onchain asset management has reached a turning point. Strategies now operate at billion-dollar scale, delivering competitive returns with programmability, composability, and transparency embedded by design.

As institutional adoption grows, onchain strategies will increasingly sit alongside traditional funds as core portfolio allocations. The industry is on track to become a $64 billion market within two years, with upside potential far greater.

Capital markets are being rebuilt onchain. Those who adapt fastest will capture the opportunity of a generation.

We’ve launched Keyrock Asset & Wealth Management, if you’re interested reach us out to learn more.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.