29 June 2026

Key Insights: No Refuge

No Refuge

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

Risk assets and inflation hedges fell together on a hot print the market chose to look past. May PCE landed Thursday at +4.1% YoY headline and +3.4% core, the first headline read above 4% since April 2023, but the curve treated it as the peak as Brent retraced to pre-conflict levels on normalising Strait of Hormuz transit. BTC fell -6.2% to $60,022 and Gold dropped -3.3% to $4,062 as the geopolitical premium bled out with oil, while NDX shed -4.2% to 29,118 on an unwind in crowded semiconductor and AI positioning, and DXY firmed +0.25% to $101.2. A print that hot would normally lift gold but it fell instead, with the market looking past May toward the lower inflation that cheaper oil should bring.

Yields fell across the belly and long end as the oil relief reset inflation expectations lower. The 2Y led down 17bp to 4.07%, the 5Y fell 17bp to 4.15%, and the 10Y and 30Y eased to 4.38% and 4.87%. The pattern is a market pricing lower inflation ahead while keeping a near-term hike on the table. Fed funds futures still price 80% for a no cut in July, but a 50% chance of a hike by the October meeting, so the rally is a peak-inflation bet rather than a pivot.

Volatility rose but the move at the money stayed contained against the size of the selloff and elevated realized. BTC 30-day implied vol gained +11.6% to 42.3, ETH IV added +6.3% to 56.3, and VIX rose +5.8% to 18.5 as cross-asset vol lifted together. Our desk reads ATM as still compressed, with dealers long inventory around $60K in BTC and $1,600 in ETH damping swings at the money while skew and convexity trade rich on downside, with July $50K puts marking a double-digit vol premium to equidistant calls. The cleanest expression is an accumulator, and the desk is showing clients 6-month weekly BTC and ETH structures that buy in at a discount to spot, near 95% for BTC, adding more on further dips for flat premium, a way to leg into the pullback at better levels while the rich downside pays for the structure.

Our Take: Bitcoin printed its lowest level since October 2024 this week, a roughly 20-month low, but the move reads as macro de-risking rather than anything breaking in crypto. BTC fell as a high-beta risk asset alongside equities, dragged by a hot inflation print and an AI-led stock unwind that the same oil relief is already working against. The one thing capping it is the September hike still near-fully priced, since that is what keeps the rate-cut optionality every BTC bounce leans on off the table. Our desk treats $60K as a level to accumulate rather than a breakdown, and the tell that the low is in is the September hike fading and the Nasdaq steadying.

No Marginal Buyer

Leverage came off all week, and the heaviest drop landed over the weekend. Bitcoin open interest held a tight $45-46b band through Friday, briefly dipping to $45.45b on the 24th June before recovering, then broke down hard across the weekend to roughly $44.1b by Sunday’s close. That left it about 5.5% lower WoW and around 10% below its 16th June peak of $49.25b. Ethereum OI fell further and faster, from $24b on the 21st June to $21.7b by the 28th June, a 9.4% WoW unwind. The early damage came in the 24-26th June leg, when a cascade liquidated roughly $1.26bn and tore through over $450m of leveraged longs in about an hour. Bitcoin’s OI-weighted rate flipped briefly negative at the 24-25th June lows, but held positive through the weekend, with dip-buyers paying up even as spot slid. Ethereum funding did the opposite, staying negative right across the weekend after deep midweek dips. The bearish leverage skew sits squarely in Ethereum.

US spot Bitcoin ETFs shed about $1.79b over the week, a seventh straight weekly outflow and, on The Block’s count, the second-worst week on record. That pulled aggregate AUM toward $72b and left the average IBIT holder down roughly 40%. Ethereum ETFs lost a further $273.3m, also a seventh consecutive negative week, and Solana products stayed marginal at -$3.9m on Friday. The one bright spot was XRP, which drew about +$7.4m through Thursday, its biggest ETF inflow in six weeks, and held AUM near $1.0b while the majors bled. Our desk reads this as spot and leveraged demand pulling back together, with no marginal buyer to fill the gap. Bitcoin closed the week near $60,000, with the Fear & Greed Index at 18, its lowest of the cycle.

Against a Layer-1 proxy down 6.0%, not a single sector finished green. Perp DEX tokens held up best at -0.5%, propped almost entirely by DYDX +38%, with RWA and DEX both at -2.3% the next most defensive as tokenised-treasury and gold names like PAXG barely moved. From there it was carnage. Data availability and restaking was the worst sector at -11.6% on EIGEN -21% and NEAR -14%. The sharpest reversal was Gaming, as our top gainer into Friday gave the lot back to close -7.9% as major names rolled over across the weekend.

Our Take: The demand engine that absorbed supply all year has stopped buying. Strategy added no Bitcoin during the week, and ETF flows are now negative seven weeks running. Take the engine out and there is no marginal buyer, which is why every sector bled and Ethereum led the way down. Bitcoin funding firmed positive into the weekend as dip-buyers paid up, perp DEX tokens were the only corner to hold the line, Coinbase’s CFTC perp launch lands 21 Jul, and 21Shares listed THYP options on 22 Jun. With Fear & Greed at a cycle-low 18 and Ethereum’s RSI near 29, the setup looks conducive for a snapback.

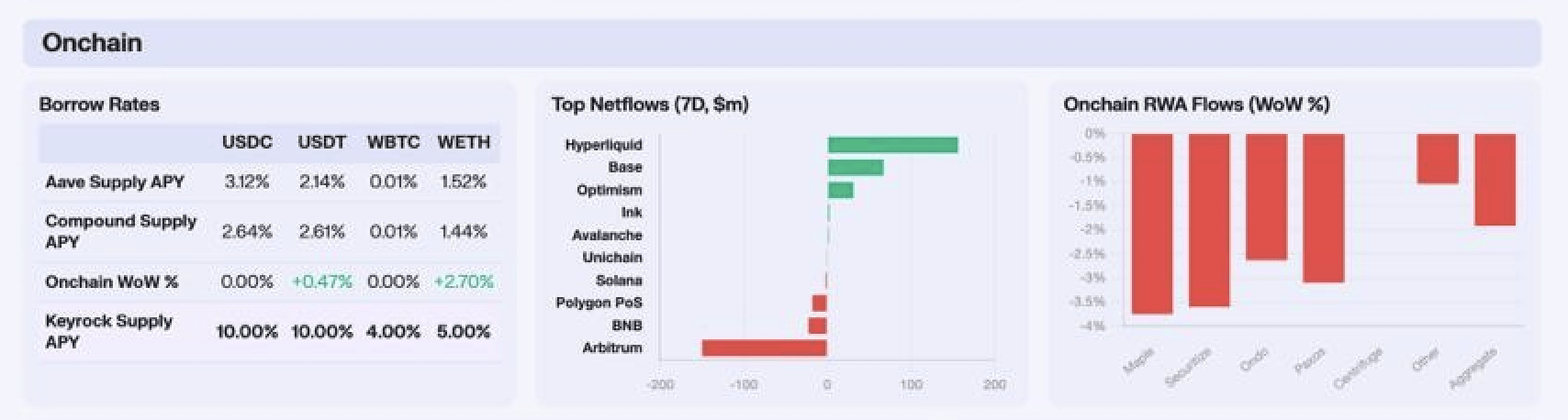

Onchain Moneyness Sort

Stablecoin supply rates compressed onchain this week. USDC held while USDT slid -14.80% WoW as deposits contracted -4.28% to $715M, the textbook signature of both sides of a pool shrinking together as leverage comes off. WBTC stayed pinned at 0.01% despite a -6.81% drawdown in deposits to $1.833B, a reminder that almost nobody borrows wrapped Bitcoin at scale. The real outlier was WETH, where the supply rate rose +8.03% as deposits collapsed -15.37% to $468M. ETH fell roughly 8% on the week to the mid-$1,600s, and the deleveraging that came with it, not any rotation into yield, did the work.

Cross-chain net flows were dominated by Hyperliquid, pulling in +$156M, the terminal phase of its USDH-to-USDC migration. Coinbase is now the official USDC deployer and the first SEPA conversion deadline lands on the 29th June, so holders spent the week converting native USDH into USDC, much of it bridged in via CCTP from Arbitrum. That migration is the cleanest read on Arbitrum’s -$149M outflow, the funding side of the same trade sitting on top of a secular L2 liquidity bleed that has run all year. Optimism’s +$31.3M is a cleaner standalone story, as Curve’s Llamalend v2 launched there on the 10th June backed by a 250,000 OP incentive grant, and the rewards campaign drew fresh deposits through the week. BNB Chain shed -$22.6M as its zero-gas 0 Fee Carnival for stablecoin transfers wound toward its 30 June expiry, pulling the subsidy that had kept dollars parked on the chain.

Tokenized RWA AUM slipped -1.92% WoW in aggregate, and the cause was the calendar, not stress. With the 30th June quarter-end approaching, institutions drained tokenized money-market and Treasury wrappers to square books, the period-end cash drain these products absorb by design. Maple led the downside at -3.75%, in line with its private-credit vaults being more redemption-volatile than passive Treasury wrappers. Securitize (-3.60%), Ondo (-2.63%) and Paxos (-3.10%) all tracked the quarter-end drain on the BUIDL and OUSG complex they administer or hold. The standout was Centrifuge, flat against falling peers because its term-locked private-credit structure is insulated from the daily-redeemable cash that bled out everywhere else.

Our Take: Strip out the migration noise and this was a moneyness sort. Capital left everything carrying duration or volatility risk, WETH out of Aave and tokenized Treasuries drained into quarter-end, while the only lines that held flat were either structurally locked (Centrifuge’s term credit) or mechanically forced (the Hyperliquid USDC switch). That makes early July the clean test. If the RWA dip was genuinely the calendar, BUIDL, OUSG and Ondo AUM should re-subscribe sharply in the first week of Q3 as institutional cash redeploys. Watch for a rebound by 6 July. If it doesn’t come, the quarter-end alibi collapses into a demand problem, and a tokenized-Treasury complex that can’t hold AUM through a benign rate week is telling you the marginal RWA buyer has gone quiet.

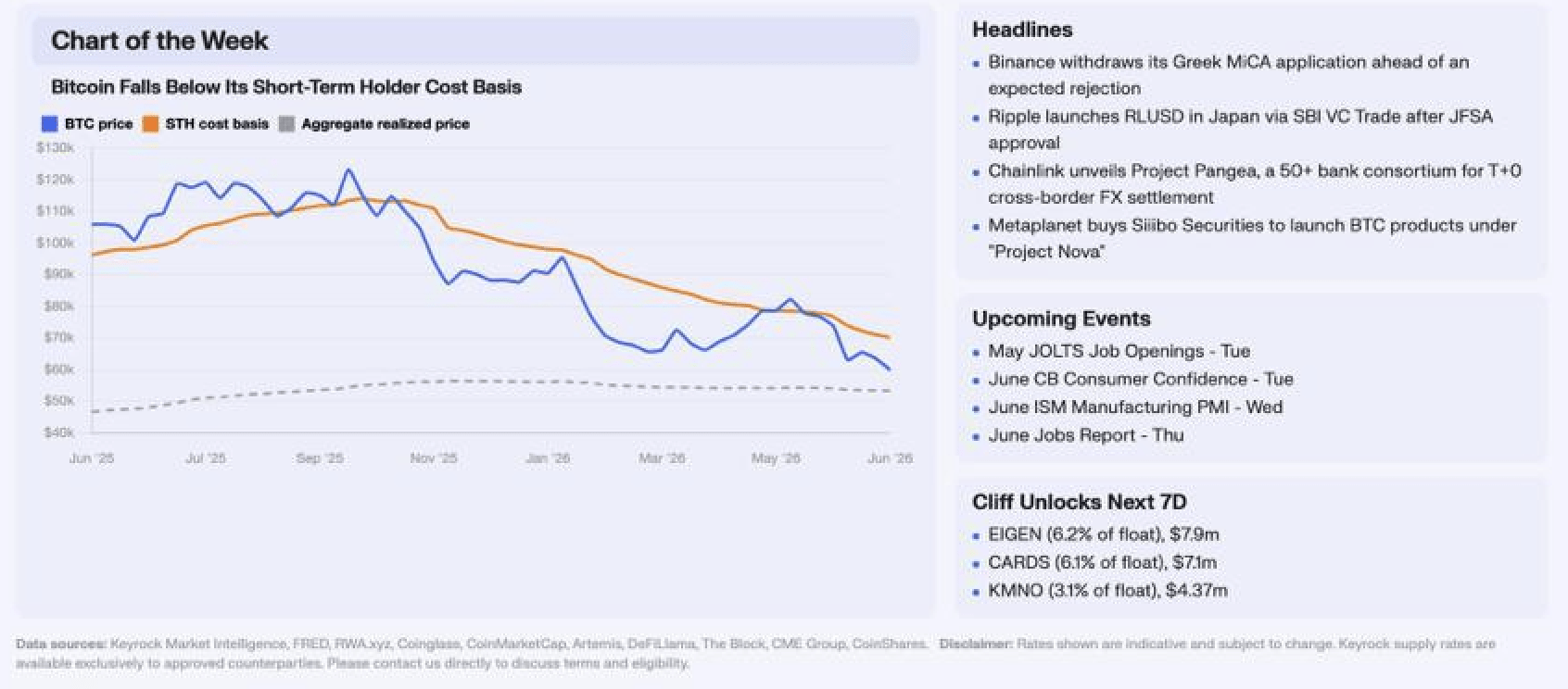

The Bitcoin Shakeout

The short-term holder cost basis, the average price paid by coins that last moved within the past 155 days, sits at $71.4k. Bitcoin fell below it in mid-February and has traded under it since, leaving recent buyers roughly 16% underwater at this week’s $60,022. The whole-market average tells the other half of the story. Aggregate realized price, the cost basis across every coin in supply, sits at $53.4k, and Bitcoin still trades about 12% above it. The network is realizing losses at a 90-day average of $205M per day, so the selling is real, but it sits with the cohort that bought near the highs.

Short-term holders are the ones capitulating. More than 95% of that cohort was underwater in early June, and the spent-output loss ratio reached levels that have marked local bottoms in past cycles. The long-term base has not moved, and the $53.4k whole-market floor has not been tested. Every genuine cycle bottom, from 2018 to the FTX collapse, has printed with Bitcoin trading below aggregate realized price, and this drawdown has not reached that point. The first signs of a floor are already showing, with Coinbase spot buying returning and short-term holders starting to accumulate at lower prices.

Our Take: This is a shakeout of recent buyers rather than a capitulation of the market. The cohort that bought near the highs is being flushed while the long-term base sits in profit and the $53.4k floor holds, the shape of a mid-cycle correction rather than a cycle-ending one. It is the onchain version of the call our desk is making in spot, treating $60k as a level to accumulate. The line we watch is $53.4k, since as long as Bitcoin holds above its whole-market cost basis the selloff reads as weak hands clearing out, and a decisive break below it would be the signal that something deeper is underway.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.