3 November 2025

Key Insights: No Cuts, No Cry

Fed Reprices Markets

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

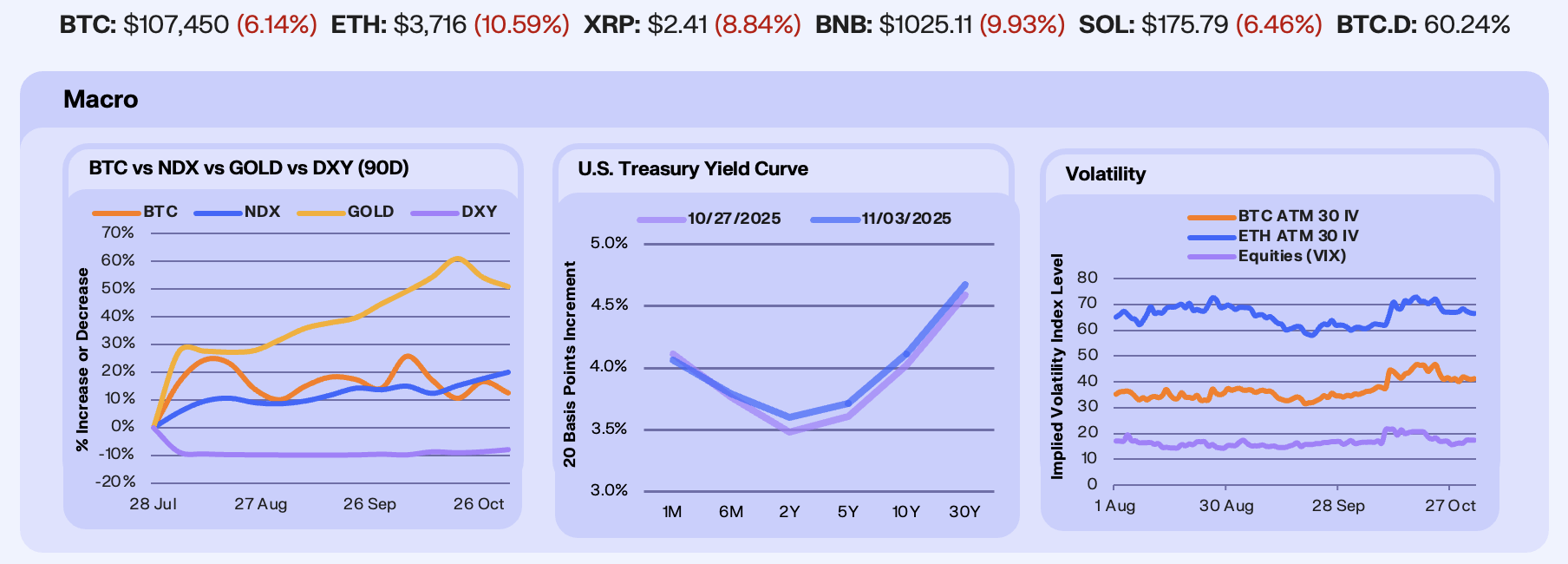

Markets entered last week positioned for a dovish Federal Reserve but were met with a more cautious policy tone, dampening expectations for further near-term easing. Bitcoin (-3.5%) and Gold fell (-2.2%) as fading rate-cut hopes and a temporary U.S.–China trade deal curbed safe-haven demand, the U.S. Dollar strengthened (+0.8%), and the Nasdaq ended higher (+2.0%) after a flurry of big tech earnings.

The Treasury curve steepened modestly as markets digested Powell’s reminder that a December rate cut is “not a foregone conclusion.” The probability of a 25 bps rate cut fell from 90% to 70%, lifting yields across the curve. The 2Y–5Y rose 10-12 bps, while the 10Y and 30Y gained 9bps and 8bps, respectively. Powell characterized the economy as “solid and stable” but noted slowing labor-force participation and reduced worker supply, reinforcing the “no hire, no fire” dynamic. Treasury demand remains cautious, capped by record issuance and fiscal strain, while gold continues to draw flows from central banks in China, India, and Turkey and renewed ETF inflows as investors seek value outside policy credibility.

Volatility held firm above baseline across assets last week as a triple whammy of Fed guidance, the temporary U.S.–China trade deal, and heavyweight tech earnings injected uncertainty back into markets. The VIX rose 11% to 17.4, while Bitcoin and Ethereum ATM30 implied stayed muted but remain elevated relative to pre-October levels. The structure of the Trump–Xi agreement, combined with Powell’s reluctance to commit to a December rate cut and his acknowledgment of “strong differing views” within the Committee, keeps volatility risk alive and underscores ongoing demand for options exposure.

Our Take: A softer labor market could give the Fed room to cut rates and support risk assets, but the balance is fragile. A rebound in hiring amid limited labor supply would reignite inflation pressures, steepen the curve, and challenge equities, while stronger productivity gains could sustain growth and keep inflation in check. Trade developments may stir short-term moves, yet domestic policy and labor dynamics remain the real volatility drivers. We stay constructive on quality risk and liquid assets like Bitcoin, where elevated implied vols suggest caution but positioning remains resilient.

Positioning Remains Cautious

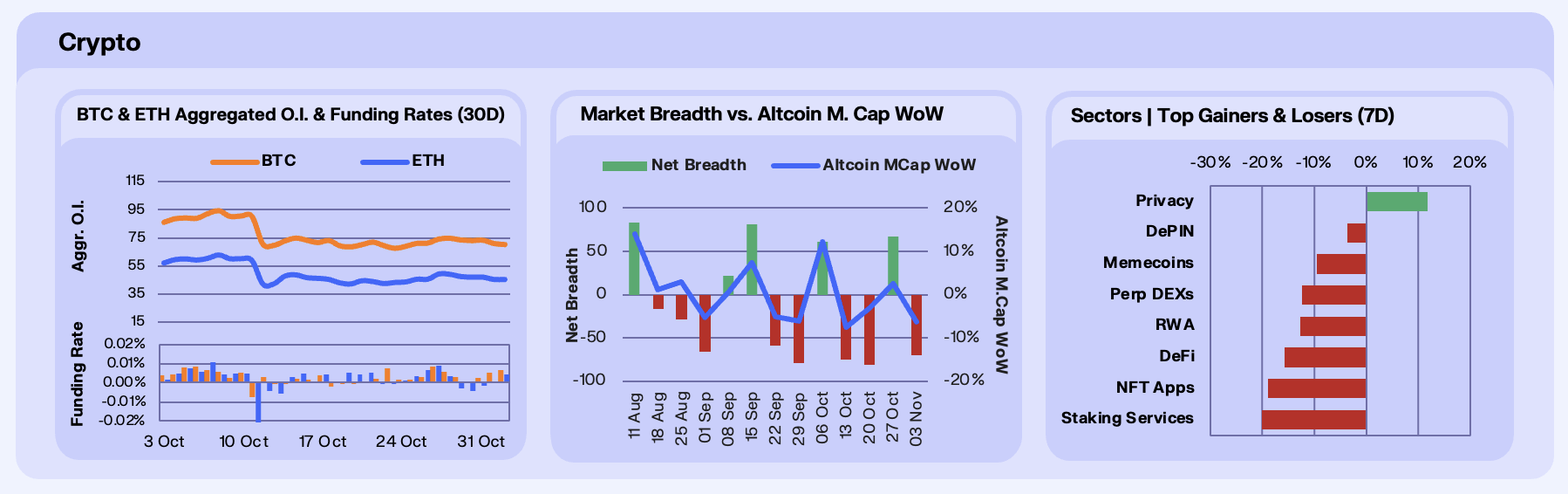

Futures positioning across Bitcoin and Ethereum remains muted following the October 10th wipeout, with traders still hesitant to re-engage in size. BTC open interest has steadied near $70.3b, roughly 30% below its prior peak, while ETH open interest sits at $45.5b, nearly 50% off the highs. Funding remains close to neutral, though BTC’s funding rate tilts slightly positive as long-biased positioning quietly rebuilds. The BTC long-to-short ratio rising from 1.1 to 2.0 over the past week reinforces that shift, suggesting renewed speculative appetite for BTC upside exposure even as aggregate futures activity remains depressed.

Market breadth, however, continues to deteriorate. This week recorded 15 advancers versus 85 decliners, yielding a net breadth of -70, alongside a -6.25% decline in altcoin market cap. The reversal underscores how fragile post-liquidation sentiment remains, capital continues to consolidate toward majors, while altcoins are losing incremental flows. The current pattern echoes early-cycle phases of recovery where liquidity and positioning first normalize through majors before risk gradually trickles back down the curve.

Sector performance was broadly negative, with most categories ending the week in the red. Long-tail narratives such as Staking (-20%), NFT Apps (-19%), and DeFi (-16%) underperformed, while Privacy names continued to hold up amid a multi-week stretch of positive sentiment. The persistent weakness in alt breadth, despite relatively stable BTC and ETH metrics, points to ongoing structural deleveraging. With less speculative capital chasing idiosyncratic risk, market rotations are increasingly driven by short-term mean reversion rather than conviction-based positioning.

Our Take: The market remains in consolidation mode, BTC is gradually regaining speculative interest, but the broader crypto complex is still under distribution. Until capital rotation broadens beyond majors, altcoin rallies will likely be short-lived and liquidity-fragile. The setup favors patience and selectivity, as sustained participation from retail has yet to return.

Selective Risk Returns

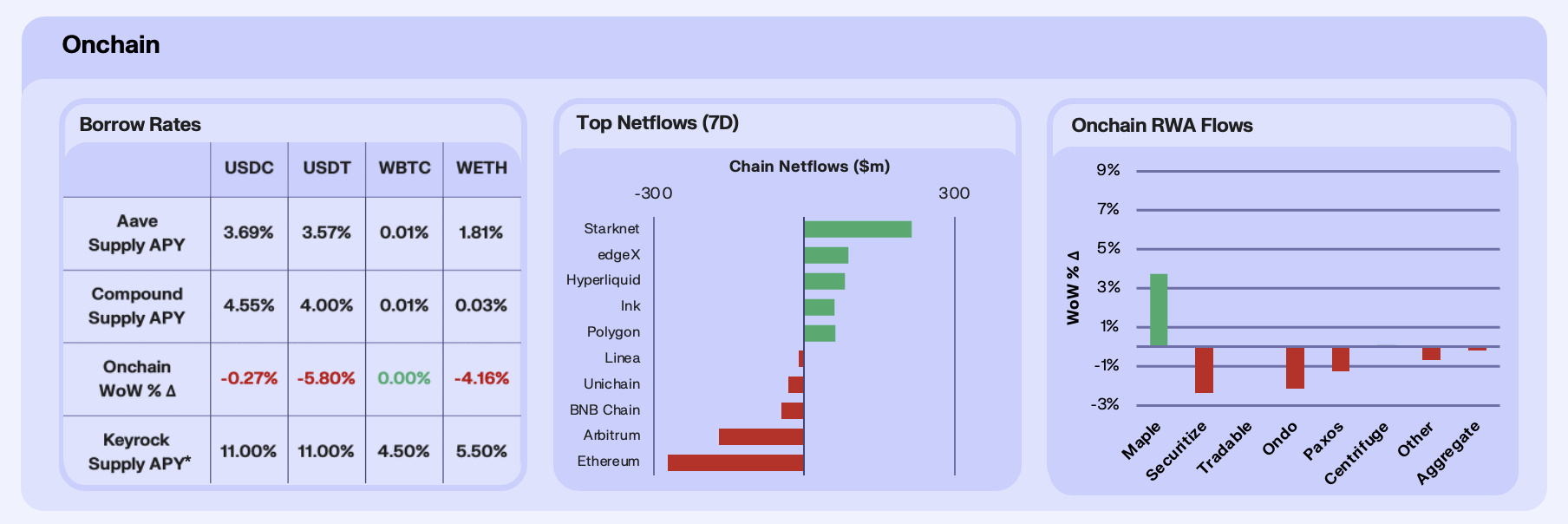

Lending markets in DeFi remained relatively stable this week, despite mild re-risking across other corners of DeFi. USDC and USDT yields softened slightly to ~3.6%, driven primarily by a supply influx, 12.6% and 12.8% WoW for USDC and USDT respectively. ETH borrowing demand dipped ~4.2% WoW, while WBTC rates held flat at negligible levels, again more supply than borrow demand driven, with ETH supply falling 11.9% WoW. This supply reshuffling underscored a rotation back towards the safety of stablecoins and passive income, as opposed to productive leverage. This pattern suggests a phase characterised by market pause, in which capital is flowing back onchain, but remains largely unutilised, awaiting clearer directional conviction.

At the chain level, flows were dominated by specific narratives this week. The gainers were led by StarkNet, with $105m worth of inflows. This gain can primarily be put down to the surge in both price and narrative surrounding ZCash, which shares the privacy-first ethos of StarkNet. Alongside this narrative drive, it’s important to mention StarkNet’s BTCFi initiatives, in which the chain enables looped tBTC staking for ~9.3% APY, and tokenised BTC funds offering up to 150% leverages APYs, as another driver for this week’s growth. EdgeX, a perpetuals trading platform, gained position upon the top gainers list this week as it pulled in $80m worth of capital. This comes as the trading platform surpassed Hyperliquid in record fee revenue of $2.6m daily. In contrast, Arbitrum’s ~$155m bleed reflected a continuation of October’s L2 drawdown. Stablecoin supply on Arbitrum fell ~$200m WoW, exacerbated by the GardenFi exploit.

Zooming in on RWA protocols, aggregate AUM dipped marginally WoW, though Maple stood out as a bright spot, up 3.7%. The protocol’s governance overhaul via MIP-019 marked a strategic pivot away from staking and toward token buybacks and credit expansion, boosting institutional confidence and catalysing inflows. Keyrock research recently released a report on Buybacks, which is available on our website, we urge you to give it a read for better context here. Securitize, down 2.4% WoW, saw mild outflows as investors rotated toward higher-yield credit protocols and commodity-linked RWAs.

Our Take: Onchain markets are quietly consolidating. We’re seeing lending onchain turn cautious but liquid, L2 flows remain opportunistic, and RWA adoption continues to deepen institutionally. The dispersion in flows underscores a more selective phase of capital deployment, one which we expect to be temporary.

Shielded and Surging

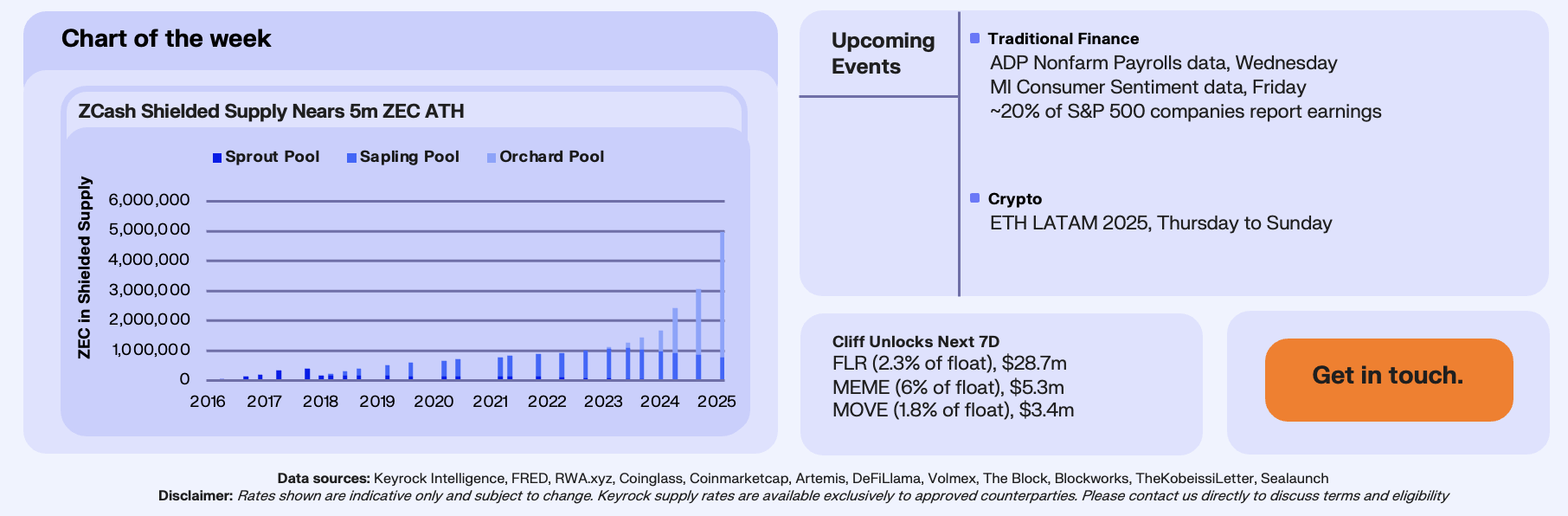

Zcash has been the standout performer of the past month, surging 195% in the past 30 days to ~$450 on October 31th, and up 967% YTD. The rally was powered by a confluence of structural and narrative catalysts, the dominant of which being growing demand for privacy assets amid tightening surveillance regimes, alongside high-profile endorsements from the likes of Naval Ravikant. The CT-driven accelerant came from Helius CEO Mert Mumtaz, whose relentless ZEC commentary on X drove retail attention, positioning ZEC as the centrepiece of the renewed privacy trade.

Underneath the speculation, we’ve seen a real shift in ZCash onchain fundamentals. Shielded pool inflows have surged to near 5m ZEC, equivalent to roughly 30% of total supply, with ~1m ZEC added in just three weeks. This marks a 125% YTD increase. Moving assets to shielded pools has historically been, and is theoretically considered to be a long-term aligned position from holders, with trading liquidity dropping dramatically for assets in shielded, privacy preserving mode. Zcash’s privacy architecture, built around zk-SNARK-enabled pools (Sprout, Sapling, and Orchard), has turned from a niche feature into a price driver, as rising shielded adoption enhances network-level privacy guarantees. Combined with Grayscale’s renewed institutional participation via their ZCSH product, Zcash is emerging as the winner of the compliant, scalable, and institutionally viable privacy-focused SoV trade.

Our Take: ZEC’s rally reflects the reawakening of the privacy narrative in crypto. As shielded adoption rises, Zcash has regained leadership in a theme that appeared only months ago to be dormant. With zk-technology now mainstream and institutions seeking compliant privacy rails, ZEC’s structural setup positions it for continued strength, even if volatility persists. The privacy cycle has turned, and this time, Zcash is the benchmark.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.