25 May 2026

Key Insights: No Cover to Ease

Yields Take The Wheel

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

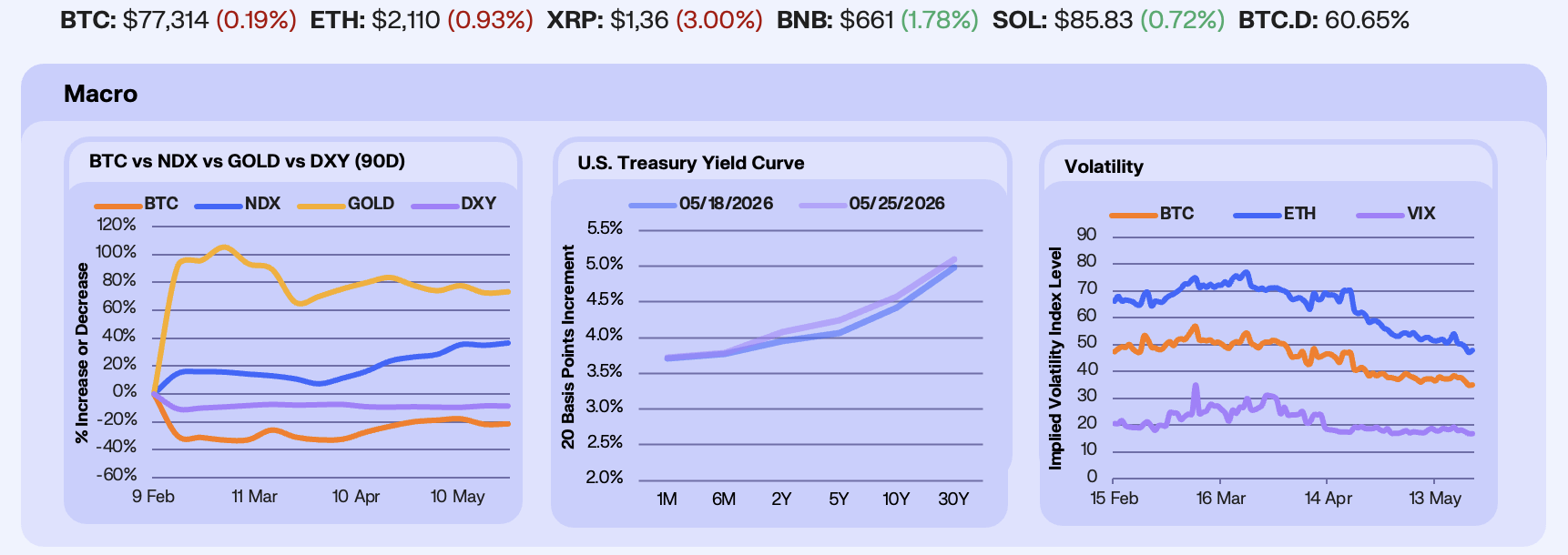

Risk assets spent the week pinned by a rate market that refused to soften, even as the year’s marquee earnings print landed. Hawkish April FOMC minutes and a weak long-bond auction pushed yields higher and kept the dollar firm, leaving a record Nvidia quarter unable to pull equities far from flat. Nvidia reported revenue of $81.6B, up 85% on the year, with data-centre sales up 92% and a Q2 guide above consensus, then closed lower the next day as a richly positioned tape sold the news. BTC rose +0.4% to $77,217, a steady line on the board after a midweek dip toward $76,000, while gold slipped 0.4% to $4,564, the NDX added +1.2% to 29,481 on a chip rally into the print, and the DXY shed -0.2% to $99.02.

Treasury yields rose for a second week, led by the belly and long end, with the 5Y up +18bp to 4.25%, the 10Y +15bp to 4.57%, and the 30Y settling at 5.10% after touching its highest since 2007 intraweek. The April 28-29 FOMC minutes released Wednesday showed many participants wanted to drop the easing-bias language, and the staff revised its inflation path higher on Middle East energy, leaving futures pricing the next move as a hike and roughly a 35% chance of one by year-end. A $16B 20-year auction the same session drew below-average demand, adding supply pressure to the long end. Crude pulled the other way, with WTI falling below $100 midweek after Trump said the US-Iran talks were in their final stages before a Friday rebound on Tehran’s refusal to ship its enriched uranium offshore.

Volatility drained out as the week’s calendar cleared without a fresh shock. VIX fell -12.57% to 16.83, BTC 30-day implied volatility -5.24% to 36.53, and ETH IV -8.98% to 49.16, the gap between the two narrowing to roughly 12.6 points as ETH vol came in faster. The overall trend remained soft for volatility as spot prices continued to pin within a tight range. Volatility was heavily sold, led by the front month, as realized volatility failed to pick up despite recent bearish price action. This spot weakness did not translate into panic; instead, aggressive put overwriting pressured both skew and convexity as investors hunted for premium to sell. Implied volatility is now compressing toward historical lows, waiting for a definitive catalyst from the spot market.

Our Take: The hawkish repricing can be closer to exhaustion than the minutes suggest. The hike now sitting in the curve rests entirely on energy-led inflation, and with Iran moving toward a deal that input would be the first to crack, which boxes the Fed in far less than the staff’s revised forecast implies. We expect this to favour BTC more than the current tape gives it credit for. Compressed vol and light positioning into a less-hawkish-than-feared FOMC is how spot can breaks its range. A sustained stay below $100 on reopens the easing path and hands BTC its first clean macro tailwind since the handover, while an Iran re-escalation snaps yields back to their highs and caps risk into the summer.

Decoupling Widens

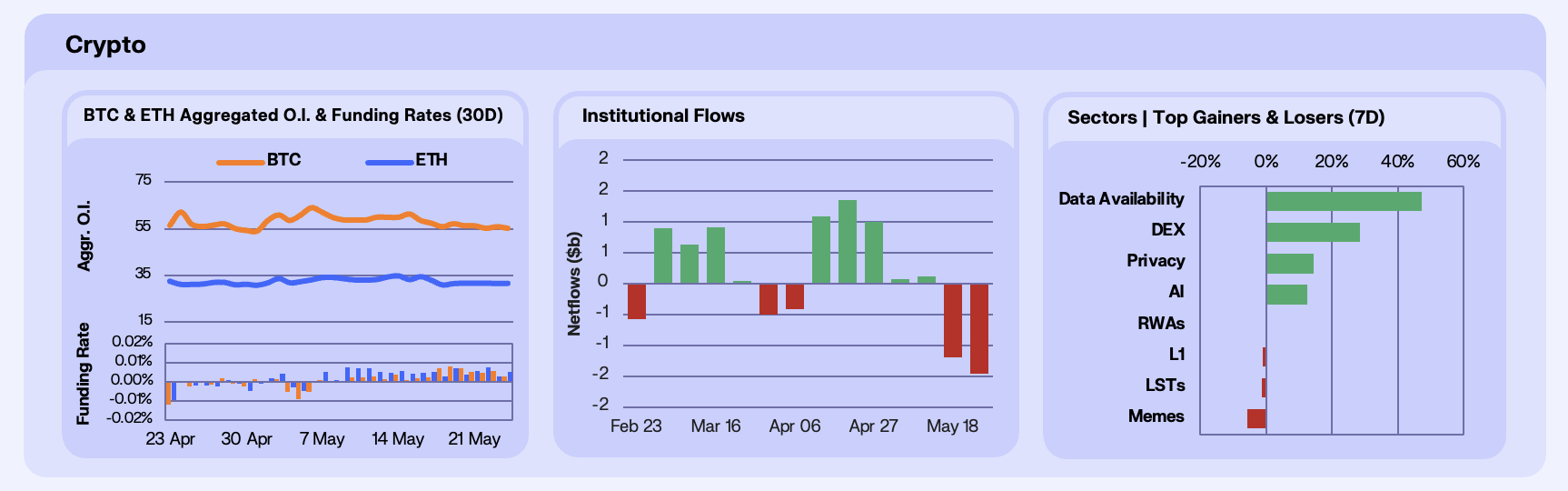

BTC open interest fell −1.24% to $55.17B, peaking at $57.17B on Tuesday before drifting lower into the weekend, while ETH open interest built the other way, rising +2.38% to $31.46B from a Monday base of $30.73B. Funding stayed positive on both through all seven days, well clear of the negative regime that ran through April, but BTC funding compressed from a 0.0083% peak midweek to 0.0029% by Sunday as longs thinned into a flat tape. ETH funding held firmer at 0.0052%. The marginal derivatives bid is leaning long but lightly, and the week’s build accrued to ETH as BTC open interest faded. The spot ETF bid stepped back for a second straight week.

Bitcoin ETFs shed −$1.256B after −$995.5M the week prior, taking the two-week outflow past $2.2B and unwinding part of the April-May inflow run that carried spot off its lows. Ethereum products lost −$216M, broadly matching the prior week’s $255.2M, while Solana funds again bucked the trend with a small +$15.6M. The flows line up with the macro tape, where a firm dollar and a second week of rising yields left allocators little reason to add. The passive bid that absorbed distribution through the spring has gone quiet, leaving the spot floor resting on prior accumulation rather than new demand.

Beneath a flat tape, the sectors pulled hard in both directions. Decentralised exchanges led at +28.4%, carried by HYPE +37.5% and ASTER +8.6%, while AI added +12.5% on NEAR +60.5% and privacy gained +14.5% as ZEC ran +24.4% alongside ARRR +62.0%. The majors went the other way, with Layer 1s down −1.1% on XRP −3.9% against a flat BTC, and memecoins the worst at −5.7% led by DOGE −6.0%. RWAs sat flat at +0.4%. The bid concentrated in a few narratives, perps, AI, and privacy, while broad beta and the speculative tail sat out.

Our Take: The selective bid is now doing all the work. With the ETF complex in outflow and BTC pinned, capital is concentrating in the names that move on their own catalysts, HYPE into its new ETF wrappers, NEAR and the AI complex, and privacy led by ZEC. We read this as rotation inside crypto, capital moving between narratives while total risk appetite stays flat. The test is whether this leadership holds through a BTC move, since a clean break tends to drag the whole tape with it. The strength in HYPE, NEAR, and ZEC is the early signal for what leads once the macro overhang lifts.

Liquidity Thins

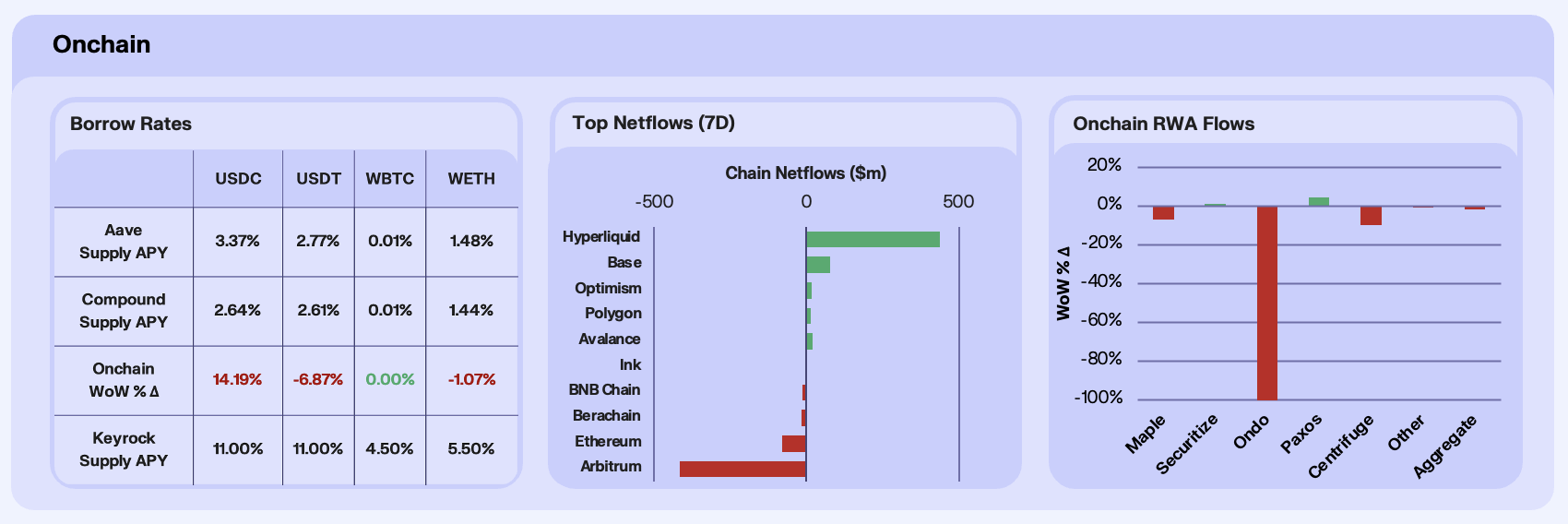

Stablecoin lending rates diverged on the week. USDC supply APY across Aave and Compound rose to 3.85%, up +13.0% WoW, while USDT eased to 2.69%, down −7.8%, and WETH firmed to 1.45%, up +8.3%. The USDC rise points to firmer dollar borrow demand as traders fund positions. The moves are modest, a long way from April’s exploit-driven supply shock, and read as leverage returning selectively rather than a broad releveraging. Keyrock continues to quote structurally higher supply yields across the stablecoins, the standing spread to the lending pools intact.

Cross-chain flows turned net negative, led out of the majors. Ethereum shed, $285M, the largest outflow on the board and consistent with the week’s spot ETH ETF redemptions, while Polygon lost −$184M. The inflows went to smaller and newer venues, with Avalanche taking +$80.3M, BSC +$28.6M, and the nascent Ink and Fraxtal chains adding +$26.3M and +$10.5M, while Solana and Monad saw only marginal outflows of −$7.7M and −$10.2M. Hyperliquid netted close to flat, a large gross inflow offset by an almost equal outflow across the week. Capital concentrated in incentive-led and newer venues while the blue-chip layer ones bled, an onchain echo of the selective rotation running through spot.

Tokenised real-world assets contracted on the week. Aggregate RWA AUM fell −1.78% WoW, the decline led by onchain credit as Maple slipped −6.68% and Centrifuge dropped −9.61%, with Paxos easing −4.80%. Securitize was the lone gainer at +1.39%, its tokenised-securities book holding up while the credit venues softened. Within RWAs, capital is favouring regulated tokenised securities over private-credit exposure.

Our Take: Onchain liquidity is following the macro tape lower, and doing it selectively. USDC borrow rates firming while flows leave Ethereum and RWA credit contracts says leverage is being put to work in pockets even as capital exits the established rails first. This is the narrow, narrative-driven behaviour visible in spot sectors and ETF flows, now showing in where dollars are borrowed and which chains they reach. We are watching whether USDC utilisation keeps climbing, which would mark real leverage demand returning rather than a one-week blip, and whether Ethereum’s outflows reverse once ETH ETF redemptions stop. The onchain read for now is capital thinning and concentrating at once.

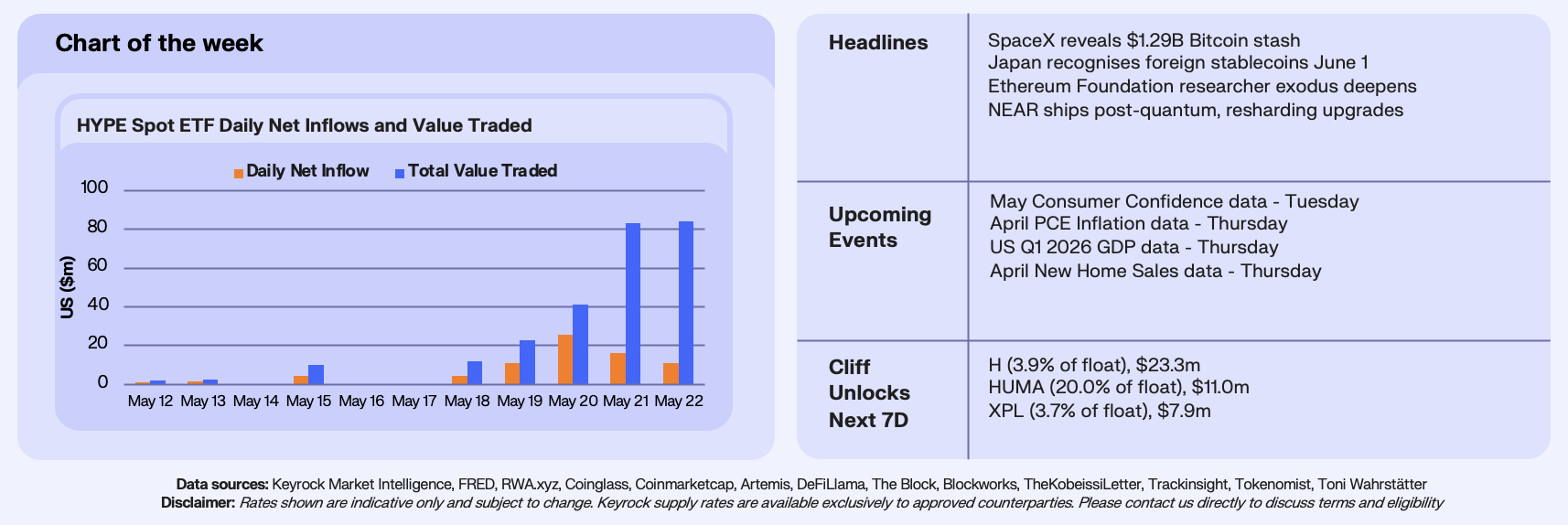

HYPE Gets A Wrapper

Hyperliquid’s token now trades through two US-listed wrappers, and last week marked their first full week of trading. 21Shares’ THYP launched the prior week, with Bitwise’s BHYP joining days later, opening a regulated access point to the token behind the largest onchain perpetuals venue. Hyperliquid routes most of its trading fees into an Assistance Fund that buys the token in the open market, so demand for the supply has run through the protocol itself from the start. The ETFs add an external channel on top of that internal one.

HYPE ETF flows ramped organically and quickly from a standing start. Daily net inflows climbed from $1.17M on 12 May to a record $25.46M on 20 May, lifting cumulative net inflows to $75M and total net assets to $81.06M by 22 May. Trading kept pace with creations, with value traded reaching $85M, slightly above the funds’ entire net assets. For a product one week old, the ETFs are being traded actively and have seen organic interest from institutional counterparts who have historically found it tough to gain HYPE exposure because of the complexities of onchain onramping.

Set against HYPE’s supply, the ETF inflows are material. The two funds hold roughly 1.4M HYPE, about 0.57% of the 238M circulating supply already. The Assistance Fund, by comparison, has bought back about 26.7M HYPE, near 11% of circulating supply, for roughly $905M since March 2025. ETF net inflows of $75M over the launch window were close to six times the roughly $13M the buyback spent across the same days, so the ETFs, not the protocol, has been the larger marginal buyer of HYPE this week.

Our Take: The HYPE ETFs have launched as a clear success, with our desk seeing funds and family offices rotate out of ETH and SOL to gain HYPE exposure through the same wrapper structure. This week’s surge, creations outrunning the buyback, is the uptrend dynamic in miniature. In a rally, ETF inflows can become the larger source of demand, while in a drawdown the fee-funded buyback keeps removing supply and matters more. For Hyperliquid, the wrappers hand traditional allocators brokerage access to a stake in its franchise, the perpetuals venue, weekend trading, and onchain pre-IPO markets.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.