10 November 2025

Key Insights: No Country For Bold Bets

Markets Stay Defensive

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

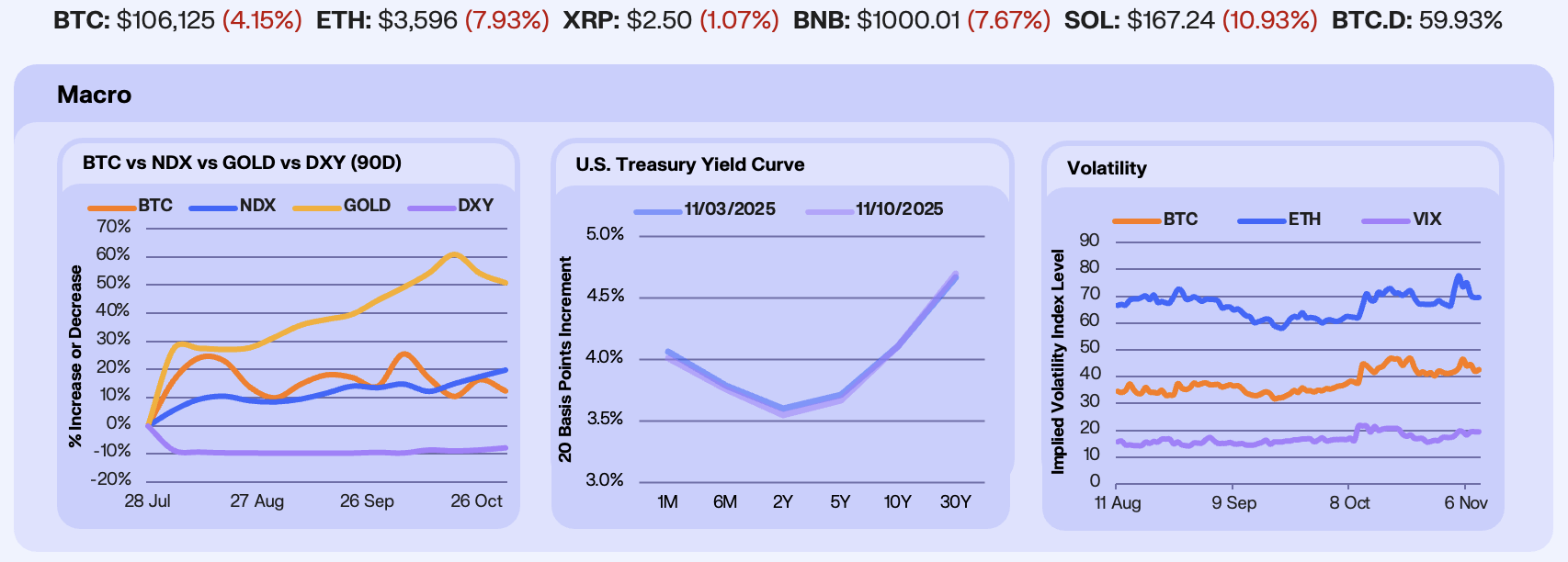

Markets entered last week positioned for a dovish Federal Reserve but were met with a more cautious policy tone, dampening expectations for further near-term easing. Bitcoin (-3.5%) and Gold fell (-2.2%) as fading rate-cut hopes and a temporary U.S.–China trade deal curbed safe-haven demand, the U.S. Dollar strengthened (+0.8%), and the Nasdaq ended higher (+2.0%) after a flurry of big tech earnings.

The Treasury curve steepened modestly as markets digested Powell’s reminder that a December rate cut is “not a foregone conclusion.” The probability of a 25 bps rate cut fell from 90% to 70%, lifting yields across the curve. The 2Y–5Y rose 10-12 bps, while the 10Y and 30Y gained 9bps and 8bps, respectively. Powell characterized the economy as “solid and stable” but noted slowing labor-force participation and reduced worker supply, reinforcing the “no hire, no fire” dynamic. Treasury demand remains cautious, capped by record issuance and fiscal strain, while gold continues to draw flows from central banks in China, India, and Turkey and renewed ETF inflows as investors seek value outside policy credibility.

Volatility held firm above baseline across assets last week as a triple whammy of Fed guidance, the temporary U.S.–China trade deal, and heavyweight tech earnings injected uncertainty back into markets. The VIX rose 11% to 17.4, while Bitcoin and Ethereum ATM30 implied stayed muted but remain elevated relative to pre-October levels. The structure of the Trump–Xi agreement, combined with Powell’s reluctance to commit to a December rate cut and his acknowledgment of “strong differing views” within the Committee, keeps volatility risk alive and underscores ongoing demand for options exposure.

Our Take: A softer labor market could give the Fed room to cut rates and support risk assets, but the balance is fragile. A rebound in hiring amid limited labor supply would reignite inflation pressures, steepen the curve, and challenge equities, while stronger productivity gains could sustain growth and keep inflation in check. Trade developments may stir short-term moves, yet domestic policy and labor dynamics remain the real volatility drivers. We stay constructive on quality risk and liquid assets like Bitcoin, where elevated implied vols suggest caution but positioning remains resilient.

Healthy Market Flush

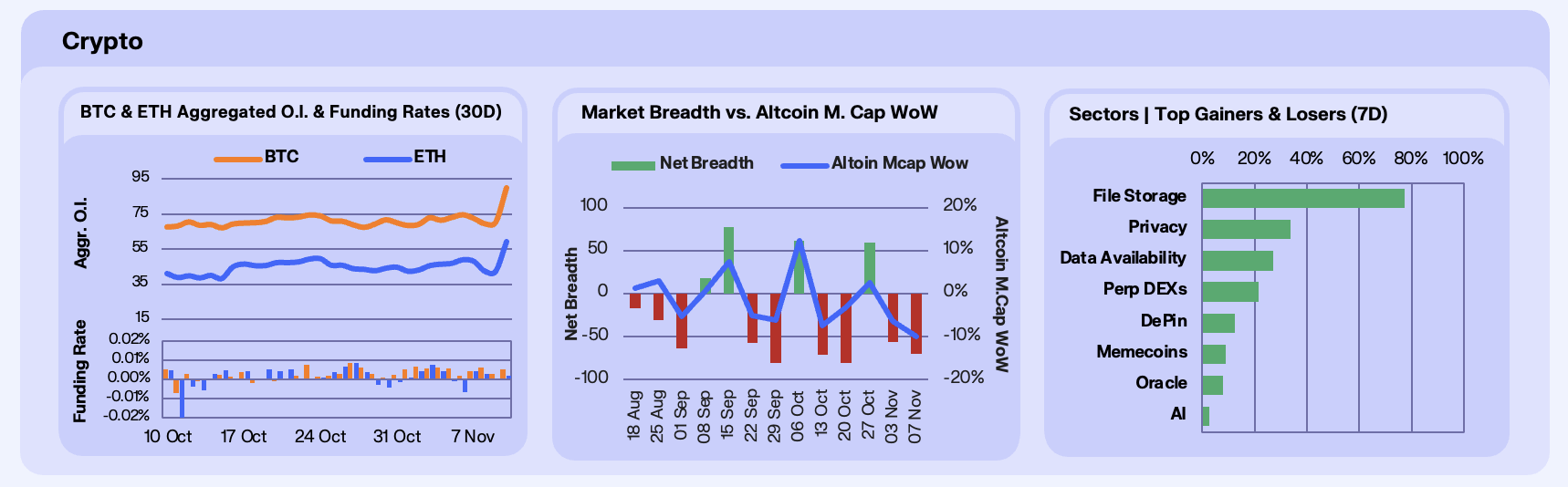

Markets endured a turbulent week as risk-off sentiment gripped global assets, with the crypto market erasing more than $1t in total market capitalisation. This huge de-risking was driven primarily by leveraged liquidations flushing speculative positions. Institutional flows were negative on the week, with BTC ETFs seeing $1.3b in redemptions and Ethereum ETFs another $500m, marking one of the largest combined weekly outflows of the year. That said, Solana $66.5m in inflows off the back of its recent launch. By the end of the week, sentiment sank to ‘extreme fear’ on the Fear and Greed index. BTC closed the week -1%, ETH -2.8%, and SOL -4.6%.

BTC OI fell 2.4% WoW and ETH fell 11.5%, wiping out nearly all of October’s buildup. Funding rates remained barely positive, showing a lack of speculative conviction. The retracement was driven more by position trimming than forced capitulation, with perpetual spreads and options skew normalising after the early-week flush, while volume concentrated on major venues as traders avoided smaller perps. It looks like leverage is being redeployed conservatively, with priority on liquidity over narrative or momentum.

Altcoins suffered a sharper drawdown as breadth turned deeply negative again, net -70 with 15 advancers versus 85 decliners. Aggregate altcoin market cap was down 10% WoW, yet several sectors bucked the trend. File Storage led, up 77.5%, driven by Filecoin (+73%) and Internet Computer (+91%), both benefiting from AI-linked infrastructure narratives. Privacy tokens continued their run (+33.6%), spearheaded by Zcash (+74%), which flipped Monero in market cap. Data Availability (+27%) and Perp DEXs (+21%) also posted gains, while Solana ecosystem names and smaller DeFi tokens lagged. Notably, NEAR (+47.6%) rode its integration with Zcash’s privacy layer, positioning itself as a cross-chain privacy enabler.

Our Take: This week marked crypto’s first real stress test since the October recovery and the system held. We’ve seen leverage clear efficiently, while ETFs absorbed redemptions without disorder, and capital rotated toward higher-quality narratives like AI infrastructure and privacy. The flush likely resets positioning for a steadier Q4.

Capital Repositions Onchain

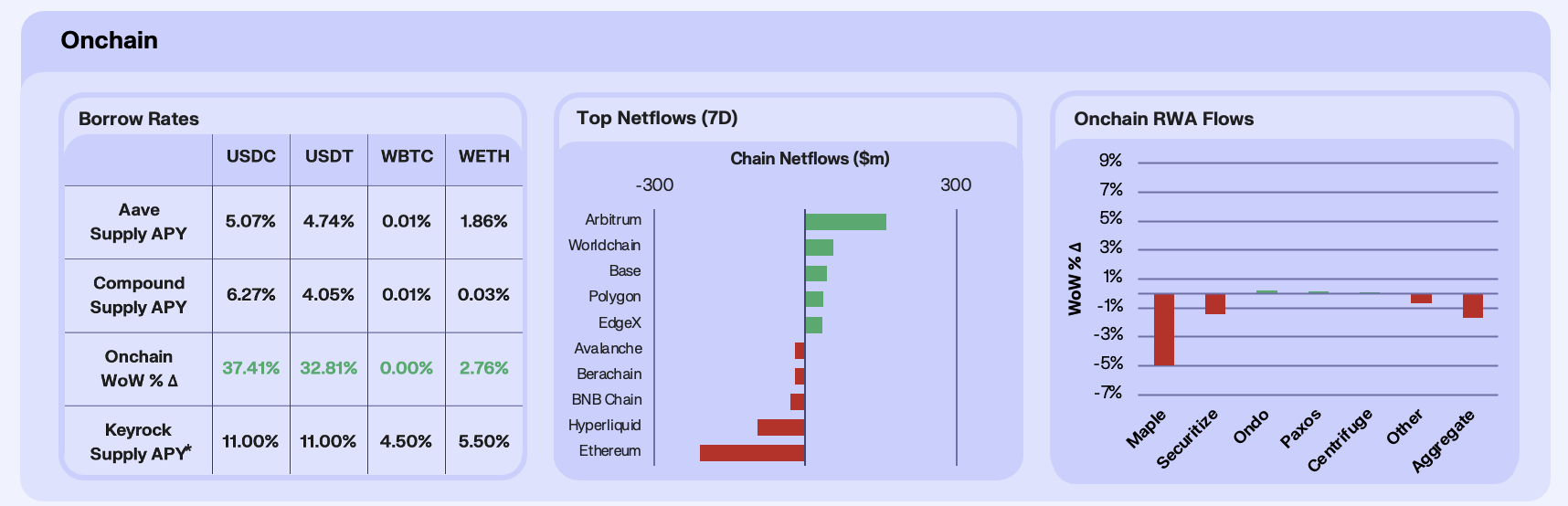

This week, lending markets onchain remained relatively subdued, with stablecoin yields ticking higher but activity softening after last week’s volatility. USDC and USDT supply APYs climbed to 5.1% and 4.7% on Aave, driven by supply balances for falling sharply, -41% and -58% for USDC and USDT respectively, suggesting lenders are rotating out of lower-yield pools into more opportunistic onchain instruments or parking capital offchain temporarily. WBTC and WETH yields rose modestly, pointing to measured risk re-entry following the liquidation cascade.

Chain netflows reflected a week of liquidations and subsequent defensiveness. Arbitrum led with $168m in inflows, as capital migrated from higher-risk venues like Hyperliquid following the $1b market-wide liquidation on November 4th. WorldChain followed with $56m in inflows, buoyed by identity and payment adoption within the Worldcoin ecosystem, while Hyperliquid, down $112m and Ethereum, down $178m, saw outflows amid risk reduction and ETF redemptions. DeFi liquidity appears to be consolidating upward, with Arbitrum anchoring the reallocation cycle.

Total RWA AUM fell 1.7% WoW, but dynamics varied across protocols. Maple, down 5% WoW, faced short-term redemptions as its SYRUP staking program sunset on November 1st under MIP-019, redirecting yield toward token buybacks and the Syrup Strategic Fund. Securitize, down 1.4% WoW, experienced a smaller pullback, largely due to post-SPAC volatility after announcing its $1.25b merger with Cantor Equity Partners, which triggered modest profit-taking in its BlackRock-backed BUIDL fund. Broader rate jitters and ETH ETF outflows added pressure to tokenised treasuries, though structural momentum remains intact.

Our Take: Onchain capital is repositioning. We’re seeing lending rates are stabalising at healthier levels, with L2s like Arbitrum continuing to absorb liquidity from riskier venues, and RWAs maturing through structural transitions. The market is rotating toward quality and yield sustainability, setting the stage for a calmer, more institutionally aligned phase of onchain growth through Q4.

Prediction Markets Gain Momentum

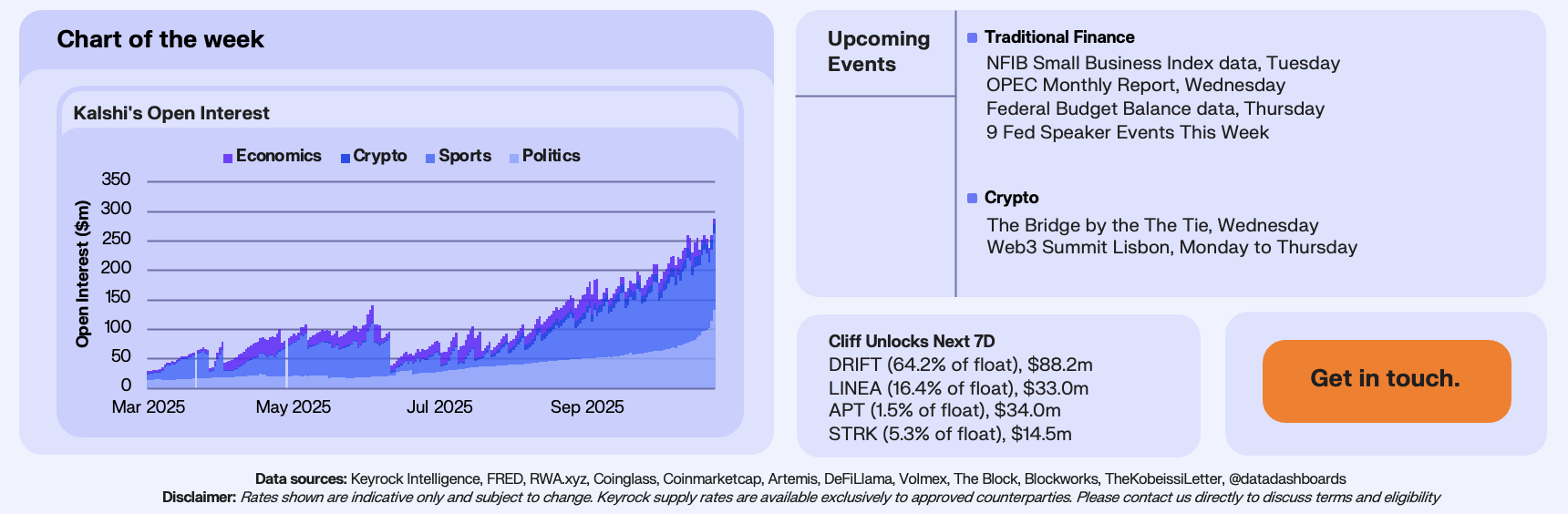

Kalshi’s Politics OI ($133 million) has officially surpassed its Sports OI ($130 million) after the New York City mayoral election, which has catalyzed heavy political trading and drawn significant retail and institutional participation. Politics tends to be a secondary category to sports, but is now again Kalshi’s largest segment by open interest, a development that underscores how prediction markets increasingly mirror real-world attention cycles.

Prediction markets once again proved to be sharper indicators of reality than polls or pundits. While traditional forecasts and expert consensus placed Zohran Mamdani at roughly 54% odds of winning, Kalshi traders had priced his victory above 80% since last year, an information efficiency gap that reinforces why markets tend to outperform surveys in aggregating collective belief. As Kalshi’s trading base has expanded, the platform has 50× its weekly notional volume since January, placing it among the fastest-scaling regulated financial exchanges globally.

Open interest across prediction categories tends to reflect what’s top of mind. Sports contracts show high turnover and frequent resets tied to weekly event cycles, while politics and economics contracts accumulate more slowly but sustain liquidity for longer horizons. The chart illustrates this dynamic clearly as shorter-term spikes in sports activity contrast with the steady climb in political exposure leading into major events. As Kalshi’s user behavior matures and the data it generates grows more predictive, major financial and information platforms have begun to take notice.

Last week, Google Finance announced integrations with Kalshi and Polymarket, embedding prediction-market data directly alongside traditional financial metrics. The move marks an important step in legitimizing prediction markets as part of mainstream information infrastructure, an acknowledgment that markets pricing probabilities may complement traditional forecasts.

Our Take: Prediction markets are becoming a primary way the public interprets information. As platforms like Kalshi scale, they’re evolving into a new layer of financial infrastructure that prices collective belief in real time. We expect political markets to continue gaining share as prediction data becomes embedded across mainstream financial and media platforms.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.