13 October 2025

Key Insights: Markets On Margin

Markets Rattle on Tariffs

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

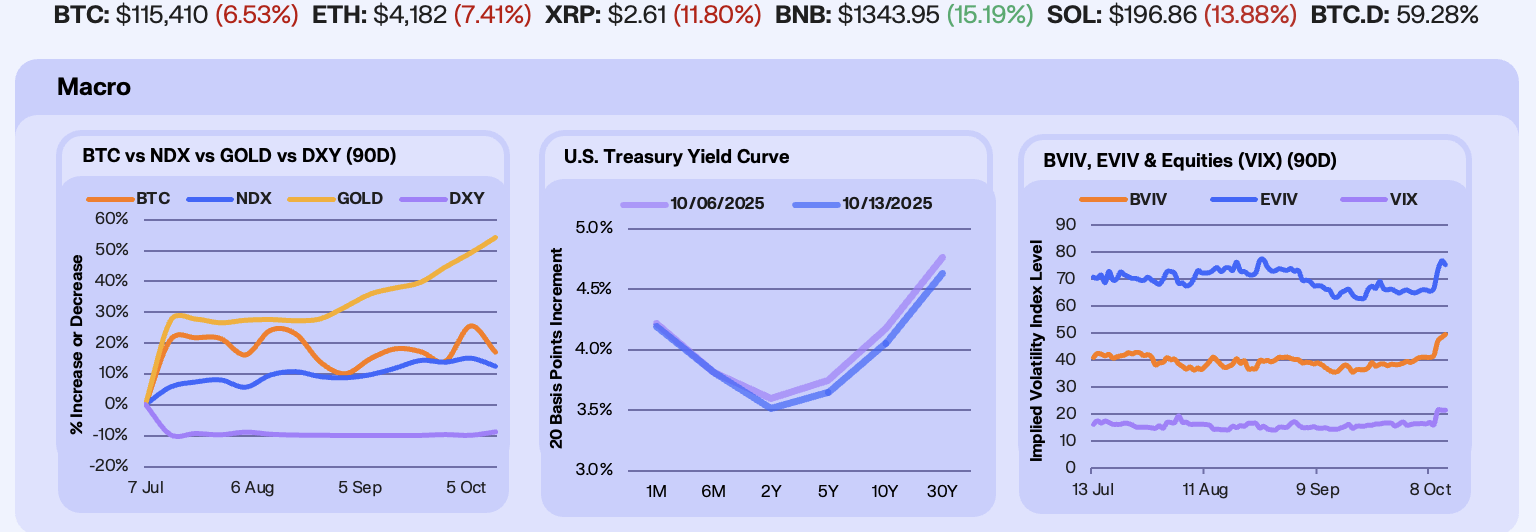

Last week, the US government extended its shutdown streak, with prediction markets now pricing a roughly 25-day closure that would surpass the 1995 Clinton-era record and become the second-longest in history. Markets were steady until late Friday when President Trump signaled higher tariffs for China and cancelled a meeting with President Xi. Bitcoin (-6.8%) led declines after briefly reclaiming record highs while the Nasdaq (-2.3%) also saw a steep drop. In contrast, Gold (+3.4%) crossed $4,000/oz for the first time, marking its fastest two-year doubling since the 1970s “Nixon Shock,” and the US Dollar Index (+1.6%) rebounded to July levels.

The yield curve shifted noticeably lower this week, with yields across the 2Y–30Y tenors falling 8–13 bps as markets reacted to renewed trade tensions following President Trump’s tariff announcement. Shorter maturities were more stable, leaving the curve flatter at the front end but decisively lower across long-duration bonds. With the U.S. government shutdown entering its third week and key data releases still suspended, investors lacked hard macro signals, making markets acutely sensitive to political headlines and policy shifts.

Implied volatility surged across assets this week. Bitcoin IV climbed sharply, with BVIV rising to ~50, its highest since May, as traders priced in bigger near-term swings across 14-, 30-, and 90-day expiries. ETH vols followed, pushing EVIV to ~75 while the VIX rose 30% to 21.6. Observers now point to a regime transition. Volatility is breaking out of complacency and demanding risk premium across markets. With option costs rising and tail hedges steepening, traders are bracing for wider short-term swings, even if we’re not yet in full panic mode.

Our Take: Markets head into next week in a fragile balance. The U.S. government shutdown, now expected to stretch toward 25 days, has frozen key economic data and left investors trading on headlines rather than fundamentals. The late-week escalation in U.S.–China tensions added to that uncertainty, amplifying volatility across risk assets. BTC and gold remain preferred hedges, though their resilience will depend on how the dollar and rates adjust to shifting risk sentiment. If the risk-off tone deepens, safe-haven demand could extend; if political compromise emerges, flows may rotate back toward yield-sensitive assets.

The Great Crypto Flush

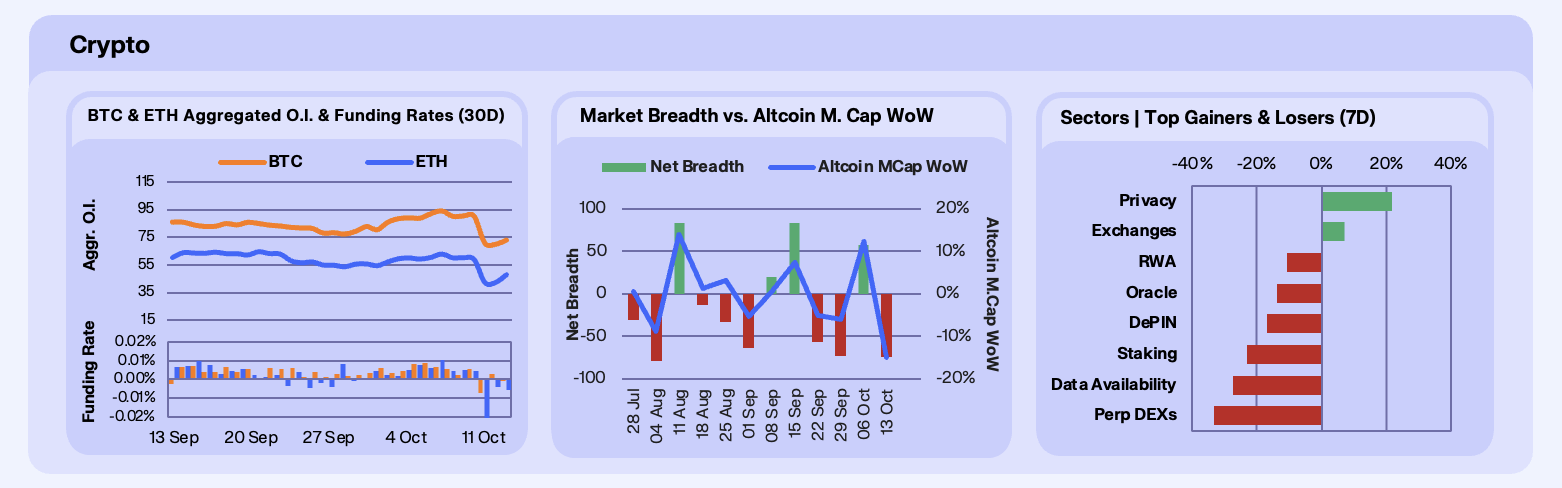

Last week marked one of the most severe liquidation events in the history of crypto markets. Broader markets were rattled by the fresh U.S.-China trade escalation, where an announced 100% tariff on Chinese exports triggered a sweeping sell-off, pulling BTC into deeper correlation with equities. Against this backdrop, liquidations surged, with October 11th alone seeing leveraged positions across BTC and ETH accounting for $4.7b of the ~$19b total market wipeout. With this price action backending the week, the result was one of the most volatile weeks crypto assets have ever seen. BTC ended the week down 7.2%, ETH down 8.5% and SOL plunging 15.9%. This comes as BTC started near $123.9k, and subsequently touched an ATH above $126k midweek, before ultimately closing below $110k. Despite the turmoil, institutional demand remained resilient when zooming out. Spot Bitcoin ETFs logged over $5b in net inflows during the early week, and ETH ETFs also drew $621m in inflows, hinting at steady accumulation from long-term allocators despite short-term volatility.

Derivatives positioning reset aggressively during the selloff. BTC open interest fell 22.6% WoW, while ETH OI declined 24%, marking one of the sharpest weekly leverage reductions since June. Funding rates flipped negative across both majors, signalling a full washout of overheated long positioning. The move reinforces how sentiment flipped from euphoria to risk aversion almost overnight, with traders unwinding high-margin bets as volatility and macro stress returned. The clean-out leaves markets less crowded, setting up more balanced and healthy positioning heading into mid-October.

Market participation collapsed this week as traders fled risk. Only 24 tokens advanced vs. 76 decliners, driving a -52 net breadth. The reversal erased last week’s optimism as the macro shock and leverage unwind forced capital up the risk continuum, away from mid-caps and altcoins, and back into BTC and ETH exposure. The shift underscores how fragile risk appetite remains. When volatility spikes, liquidity concentrates instantly in the highest-quality assets, leaving the long tail of tokens starved of bids and liquidity.

That said, while sector performance was largely defensive, we did see very specific flashes of light. Privacy tokens, up 21.7% WoW, led gains, with Zcash surging 73.8% on renewed privacy-layer adoption and speculation around integration into emerging L2 privacy frameworks. Additionally, exchange tokens, up 7.1%WoW, outperformed, led by BNB up 10.2%, which flipped Solana in market cap. Binance’s announcement of a new institutional-grade custody and settlement division fueled momentum, while rumors of CZ’s possible presidential pardon injected a speculative narrative tailwind.

Our Take: This week’s drawdown underscores that crypto’s ‘institutional phase’ doesn’t make it immune to macro volatility, it just changes who absorbs the shock. ETFs and DATs acted as stabilisers even as speculative leverage collapsed. With open interest flushed and funding normalised, structural inflows remain the anchor. If macro pressures prove short-lived, which is often the case with these major moves, the washout could mark the start of a cleaner base for Q4. One supported less by momentum and more by real capital demand.

Flight to Safety

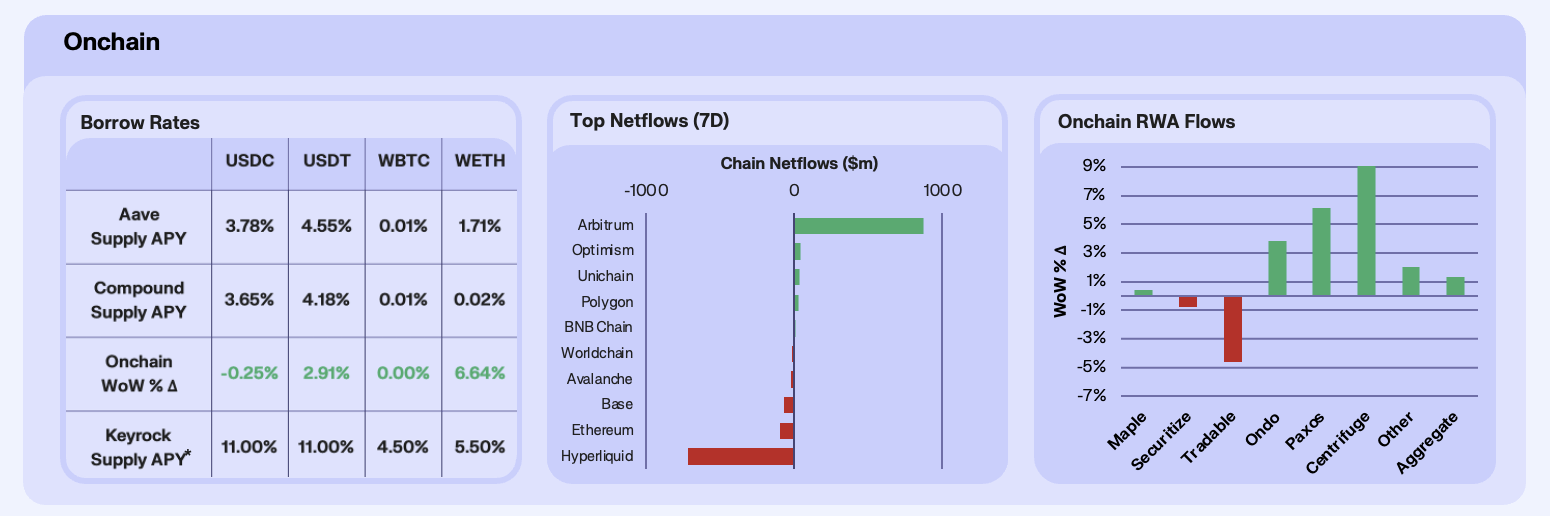

Lending markets steadied this week after the macro-driven chaos in broader crypto. USDC and USDT APYs remained largely flat, at 3.78% and 4.55%, while ETH yields rose 6.6% WoW, reflecting borrowers re-entering the market following last week’s deleveraging. ETH’s rate uptick was driven by a 16.7% contraction in supply, with holders pulling capital out of the system, potentially in fear of second order effects of the leverage flush. Overall, onchain rates signal a cautious reset where liquidity is ample, but leverage appetite remains subdued.

Netflows reflected the aftermath of the flash crash and the forced derisking that followed. Hyperliquid saw $720m in net outflows, its steepest on record, as cascading liquidations wiped over $10b in open interest and triggered over 1,000 full liquidations. The exchange’s high-leverage structure, combined with thin liquidity in smaller perps, made it ground zero for the market’s unwinds. Reports of $21m in user losses from key leaks and delayed withdrawals compounded the exodus, driving capital flight from high-beta venues. Much of this liquidity rotated back to Arbitrum, which recorded a roughly corresponding $700m in inflows as traders sought stability. Arbitrum’s deep DeFi stack provided a natural landing zone for derisked capital.

RWAs proved once again to be DeFi’s steady anchor amid volatility. Aggregate RWA AUM rose 1.3% WoW, led by Centrifuge, up 10.7%, and Paxos, up 6.1%. Centrifuge’s gains were driven by the launch of the Global RWA Alliance via Plume Network, a cross-industry consortium uniting major issuers and TradFi players like Apollo Global Management, which deployed a $50m tokenised credit fund using Centrifuge infrastructure. This milestone pushed Centrifuge’s TVL to $1.26b, highlighting growing institutional traction. Paxos also advanced after launching USAD, a privacy-focused stablecoin built on Aleo Network, tailored for compliant institutional use.

Our Take: Last week’s liquidations drained speculative excess from the system, and onchain flows show where capital hides when leverage breaks. Stablecoin lending is steady, ETH borrowing is returning, and RWAs remain the quiet winner. If volatility persists, RWAs and high-quality DeFi ecosystems like Arbitrum are poised to capture even greater market share, though we expect this will be a short-lived flight to safety.

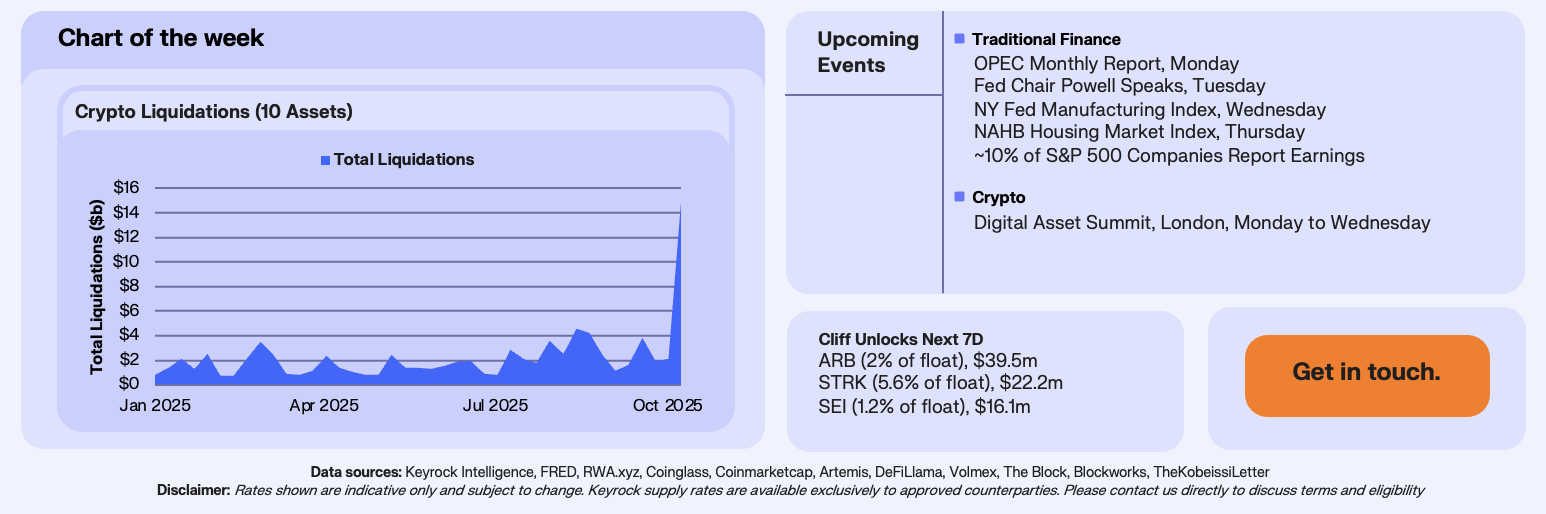

The Liquidation Cascade

On Friday, over $14 billion in crypto positions were liquidated across 10 major assets, with Coinglass data showing a broader $19.1 billion total and 1.6 million traders affected, the largest liquidation event in crypto history. The scale was amplified by leverage unwinding across both centralized and onchain venues. On Hyperliquid alone, open interest collapsed from $15b to $6b in a single session, signaling a widespread cascade as margin calls rippled through the system.

Unlike prior collapses tied to single catalysts, FTX, Luna, Celsius, this drawdown mirrors the May 2021 liquidation wave, where leverage simply exceeded structural liquidity. Months of low volatility and steady gains had pushed traders into increasingly crowded, high-risk positions. When volatility finally spiked, the feedback loop of forced unwinds erased billions in hours. The macro backdrop amplified the effect with equities hitting new highs and a weakening dollar distorted risk perception, leaving traders unsure whether their gains were real in purchasing power terms.

Our Take: The wipeout is less about one failure and more about structural fragility. Retail FOMO, synthetic collateral, and speculative narratives around perpetual DEXs masked how thin real liquidity had become. In recent months, money flowed too easily, hiding fragility beneath momentum. This week’s cascade was the reset. Builders who treat token price as a scorecard rather than a signal of robustness are being forced to confront leverage, liquidity, and risk management all at once.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.