21 July 2025

Key Insights, License to Risk

The Long End Strikes Back

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

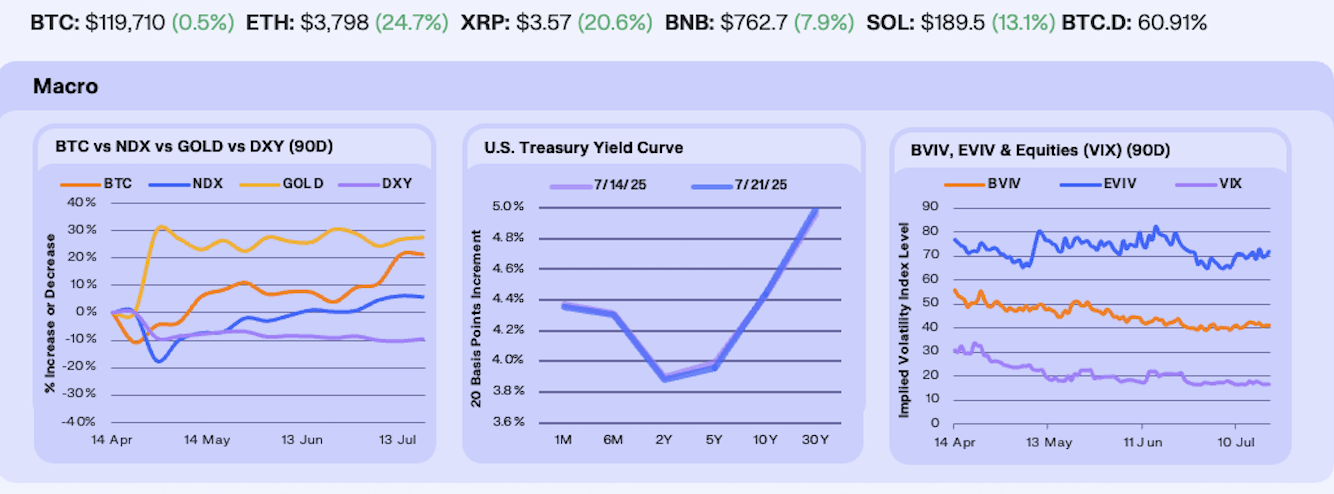

Last week, markets focused on bonds and rate cuts after June CPI came in slightly above expectations (2.7% vs. 2.6%) and PPI cooled (2.3% vs. 2.5%). Investors are balancing stable inflation with rising U.S. debt servicing costs, driven by elevated bond interest payments, and the Fed’s wait-and-see stance on the impact of tariffs. These pressures have weighed on the dollar over the past year (-9.2%), creating a backdrop where safe havens like Gold (+0.4%) and Bitcoin (+0.4%), as well as growth assets like the Nasdaq 100 (+1.3%), tend to perform well when fiscal strain and elevated debt servicing erode long-term confidence in USD.

The US Treasury curve steepened modestly over the week, once again led by the long end. Ongoing supply concerns and long-term fiscal risks are putting pressure on duration-heavy assets, pushing term premiums higher. The 30Y is now nearing levels last seen during the October 2023 selloff. Front-end yields held steady as markets digested a subdued CPI print, reinforcing the Fed’s stance. With no near-term easing in sight, longer-dated bonds are bearing the weight of higher-for-longer rates and rising debt servicing costs, driving a structural repricing across the curve.

In response to the spot market, Bitcoin and Ethereum volatility climbed in the beginning of the week, though have abated since. Bitcoin’s implied volatility fell from 42.5 to 41.1 (-3.1%), while Ethereum’s rose from 70.3 to 71.9 (+2.2%). Notably, Bitcoin, near its all-time high (~$123k) is showing the lowest volatility of any ATH in its history. With ETH implied volatility still elevated, traders appear positioned for directional upside if momentum resumes.

Our Take: The market continues to lean bullish, supported by a macro backdrop where rising U.S. debt servicing costs are pressuring longer-dated Treasuries. The resulting steepening of the yield curve is weighing on the dollar, creating tailwinds for growth assets like crypto and equities. Traders are expressing exposure through put selling and positioning for a move toward $130k, viewing current levels as consolidation rather than a peak. In contrast, ETH options positioning is more directional, with concentrated call interest around $4,000 pointing to growing appetite for upside exposure.

ETH Takes the Lead

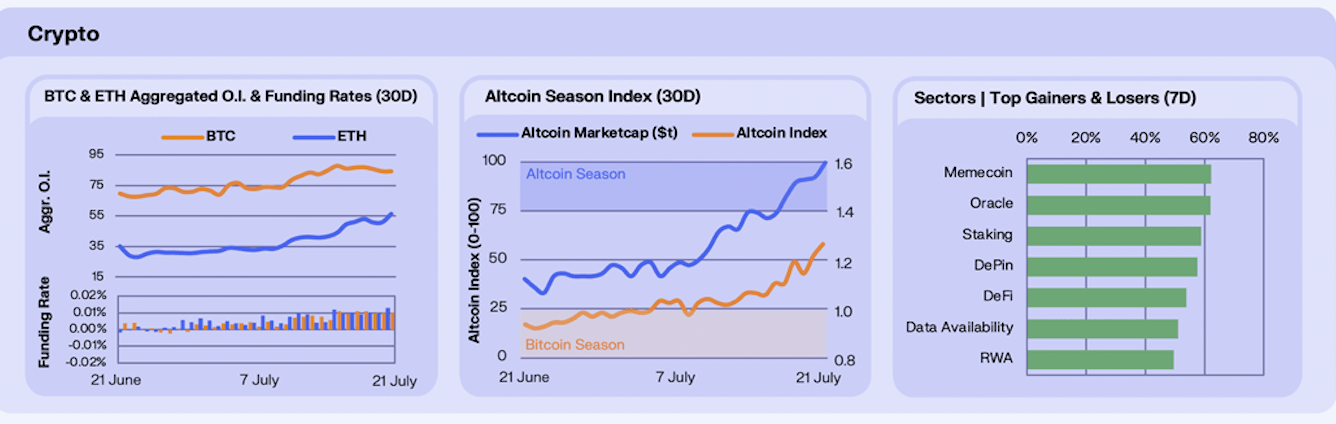

Crypto markets were euphoric this week as BTC reached ATHs, hitting ~$123k on Monday, coinciding with daily CEX deposit volume hitting its highest level since February. ETH followed suit, rebounding from months of being the crypto-native punching bag, gaining 25.3% WoW. Open interest jumped +35.1% WoW, boosted by growing institutional flows. ETH spot ETFs recorded their largest weekly inflow on record, with Wednesday setting a new all-time high for daily ETF volume. SharpLink Gaming made headlines by raising $413m to buy 215k ETH, overtaking the Ethereum Foundation as the largest public holder. Meanwhile, Peter Thiel’s Founders Fund acquired a 9.1% stake in BitMine Immersion, continuing the shift of Digital Asset treasury (DAT) strategies from BTC to ETH. Despite this shift in DAT narrative, Strategy hit a new all-time high of $129m market cap, supported by BTC price action and demand for the full stack of securitised BTC that Strategy offers.

Altcoins also saw a new lease of life this week. The Altseason Index climbed from 38 to 58, while total altcoin market cap rose to $1.49t (+7.97% WoW). Top gainers were dominated by DeFi primitives, including CRV, UNI, and LINK, with inflows into the Ethereum ecosystem and positive ETF momentum helping lift the broader market.

On the sector level, memecoins led the pack, up +62.2% as a sector, followed by Oracles (+61.9%), Staking (+58.8%), and DePin (+57.6%). This reflects a search for structural narratives beyond memes and majors. DePin and Oracle names rode the wave of renewed infra attention post-ETH ETF progress. Meanwhile, DeFi posted strong double-digit gains, catching tailwinds from the ETH-led rally.

Our Take: ETH institutional interest is accelerating, with ETF flows, treasury activity, and staking all reinforcing the narrative. We expect ETH to outperform BTC through Q3. If ETH staking ETFs are approved, the next leg of rotation could see TradFi crowd into ETH-linked protocols, especially yield-bearing and RWA plays.

Early Risk Signals

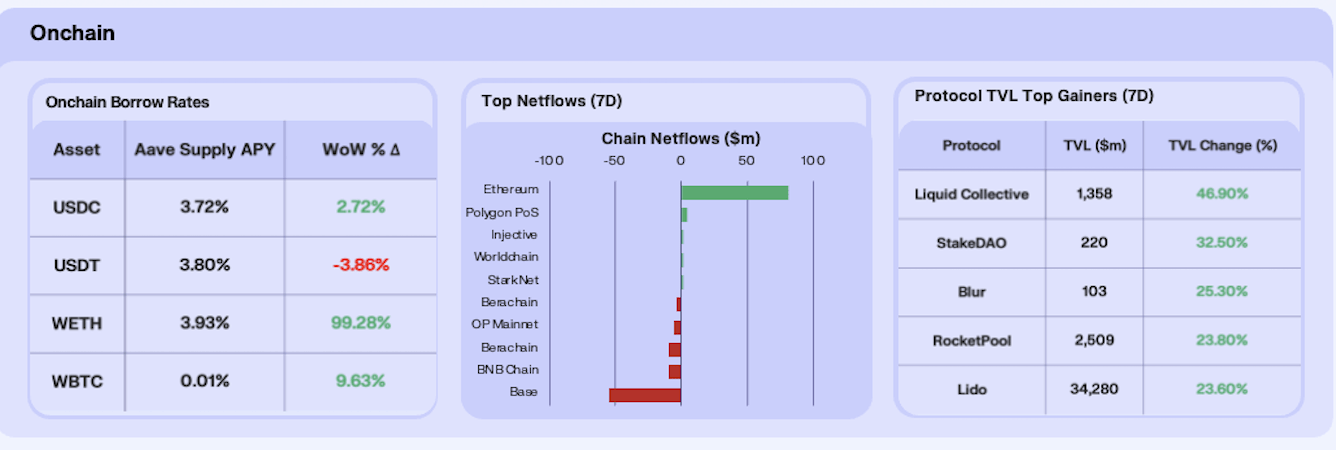

Stablecoin yields at large were little changed this week, continuing the drift downward that began in mid-June. USDC lending rates gained to 3.72% (+2.72% WoW), while USDT slipped to 3.80% (-3.86% WoW). BTC rates remain suppressed, at just 0.01%, reflecting a lack of demand for onchain leverage despite rising asset prices. ETH on the other hand, almost doubled on the week, as borrow demand rose amid growing desire for exposure to utilise in DeFi strategies.

Netflows shifted dramatically this week. Ethereum led all chains with over $8b in net inflows, while Base saw the heaviest outflows, pushing below –$5.5b over the 7-day period. Polygon PoS and WorldChain posted strong inflows, while BNB Chain, and Berachain saw net outflows.

Staking protocols saw a wave of inflows this week, with Liquid Collective (+46.9%), StakeDAO (+32.5%), and Blur (+25.3%) leading the charge. The surge reflects renewed long-term conviction in ETH as institutional flows, ETF momentum, and staking rates all rise in tandem. Capital is locking into ETH staking protocols to secure yield.

Our Take: The flows we’re seeing suggest we’re in the early innings of a sustained risk-on cycle, particularly with aforementioned shifts in the altcoin sector. This is evident in high demand for the largest gaining majors, as well as strong flows into related ecosystems.

Make It Perp

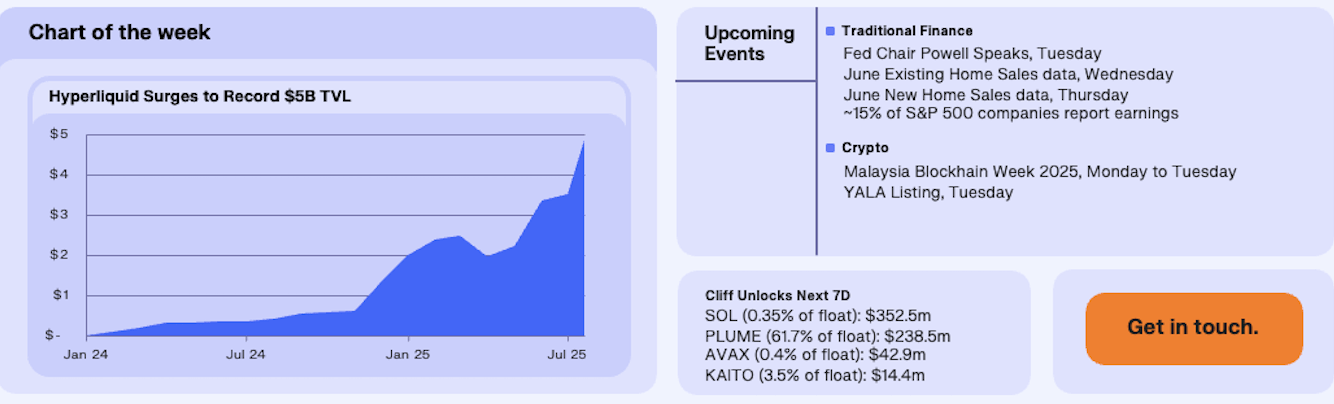

Hyperliquid, a decentralised perps exchange with sub-second finality and an onchain order book, has reached a record $5b in USDC deposits and now accounts for 66% of total perps volume across decentralised exchanges. Amid renewed risk appetite, Hyperliquid is on track to post its highest monthly perps volume yet at $290b, surpassing its previous record of $248b. It now holds 75% of all USDC on Arbitrum. HYPE’s recent rally reflects the scale of its buyback flywheel: $3.8t in cumulative volume has generated $365m in revenue to date, including $52m this month alone.

Hyperliquid’s permissionless front-end model and embedded fee-sharing turns connected apps into distribution partners, as seen recently with Phantom integrating its API to unlock access for millions of users. With HIP-3 on the horizon, developers will soon be able to spin up custom markets (e.g. FX, stocks) on top of the its shared liquidity. As new front-ends compete to attract users and innovate on design, Hyperliquid’s distribution flywheel is only getting started.

Our Take: DEXs will continue gaining market share from centralised exchanges, driven by their lower cost structure, greater design flexibility, and more equitable incentive models. Platforms like Hyperliquid demonstrate how open infrastructure and aligned incentives transform users and developers into active distribution channels, enabling builders to experiment freely, launch new markets, share in fees, and access pooled liquidity. This flexibility is becoming a powerful growth engine, with developer-led distribution emerging as a key driver of the next wave of market expansion.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.