The Great Tokenization Shift: 2025 and the Road Ahead

What are Tokenized Equities? A guide

This is a part of the “The Great Tokenization Shift: 2025 and the Road Ahead” report which can be downloaded here.

What are tokenized Equities?

Tokenized equities are digital representations of traditional stocks that exist on a blockchain. They offer a new way to access and trade shares like Apple or Tesla. By turning real-world equities into blockchain-based tokens, these assets become globally accessible, tradable 24/7, and compatible with decentralized finance platforms. Whether backed by actual shares or synthetically mirroring stock prices, tokenized equities aim to bridge the gap between traditional finance and the rapidly evolving world of digital assets.

Historical Context and Regulatory Considerations for Onchain Equities

Traditional equities markets have long been highly structured, operating through centralized exchanges (NYSE, NASDAQ, etc.), broker-dealers, custodians, and clearinghouses. Key features of the traditional system include:

- Centralized Clearing: Trades must clear through a central counterparty (e.g., the DTCC in the U.S.), which introduces settlement delays.

- T+2 Settlement: Buyers and sellers typically wait two days for final ownership transfer—a lag highlighted during the 2021 GameStop frenzy, when brokerages halted buying due to heightened collateral requirements during the settlement window.

- Layered Intermediation: Shares are usually held in the name of brokers rather than as direct registered ownership, leading to potential transparency issues.

While equity markets are mature and liquid for major stocks, they are operationally constrained by business-hour trading, batch settlement, and access limitations for many global investors. Similar to tokenized treasuries, these inefficiencies create an opening for blockchain-based solutions that promise 24/7 trading, near-instant settlement, and direct ownership transfer without so many intermediaries.

However, despite the clear technological advantage, regulatory barriers have prevented traditional stocks from seamlessly integrating into blockchain markets. In the United States, tokenized stocks are rigorously regulated as securities or investment contracts under longstanding laws such as the 1933 Securities Act and the 1934 Exchange Act. When a token replicates a share or delivers returns tied to a stock’s performance, it is treated like any traditional equity, subject to full registration, detailed disclosures, and stringent trading requirements. Additionally, the requirement for trading platforms to register as national securities exchanges or alternative trading systems, coupled with FINRA’s mandates on KYC/AML, makes the process complex.

In Europe and the United Kingdom, tokenized stocks are similarly integrated into existing securities frameworks, classified as financial instruments under MiFID II and the Prospectus Regulation rather than under the EU’s newly enacted MiCA—which explicitly excludes crypto-assets that qualify as regulated financial instruments. This means that public offerings require an approved prospectus unless specific exemptions apply, as illustrated by Germany’s BaFin warning against Binance’s 2021 token offerings that lacked the necessary disclosure documents, potentially exposing issuers to fines exceeding €5 million. Moreover, trading venues must secure regulated licenses, such as operating as a Multilateral Trading Facility (MTF), and national legal nuances—like Liechtenstein’s Blockchain Act and Germany’s Electronic Securities Act (eWpG)—provide pathways for issuing and managing tokenized securities on blockchain registries.

How Stocks are Tokenized in Crypto?

Despite the regulatory challenges, efforts to bring stocks onchain date back to the late 2010s. Early notions of “security tokens” envisioned digitizing shares with blockchain record-keeping, but adoption was slow due to regulatory hurdles. During the DeFi Summer of 2021, synthetic equities emerged in DeFi as a workaround: instead of representing an actual share, a synthetic token is created that tracks the price of a stock using an oracle. Users can buy and hold these synthetic positions to replicate the returns of their underlying stocks. Two protocols emerged as clear but temporary winners with this approach: Mirror Protocol and Synthetix.

Mirror Protocol allowed users to create “mAssets” that synthetically mirrored the prices of real-world equities like Tesla or Apple. To mint these mAssets, a user would lock up UST in a collateralized debt position. Smart contracts from BAND protocol monitored the real stock price via oracles that updated roughly every 30 seconds. If the stock price rose and the CDP ratio fell below a set threshold, the user had to post more UST collateral or risk liquidation. Arbitragers would keep the onchain price stable by minting and redeeming it with the current oracle price if the onchain price fell below its peg. While this approach provided immediate, global access to equities, it was inherently tied to UST’s stability. When UST depegged in 2022, the entire system experienced cascading liquidations, demonstrating the fragility of synthetic structures backed by unstable collateral.

Synthetix issues synthetic assets—”Synths”—using the protocol’s native token, SNX, as collateral. The platform sets a high collateralization ratio (commonly 400–600%) to accommodate price volatility. For example, if a user mints a synthetic Tesla (sTSLA), that user effectively owes a “debt” denominated in Tesla’s price, while holding a minted sTSLA token pegged to Tesla’s real price. Oracles (often Chainlink feeds) update Tesla’s quote, causing the total debt to fluctuate. If Tesla’s price climbs, the user’s debt increases, compelling them to lock more SNX to stay above the liquidation threshold. This design offers leveraged exposure to equities without direct custodial requirements, but it is extremely capital-inefficient and demands active management of the collateral ratio.

Regulatory Challenges and Compliance Approaches to Stocks Tokenization

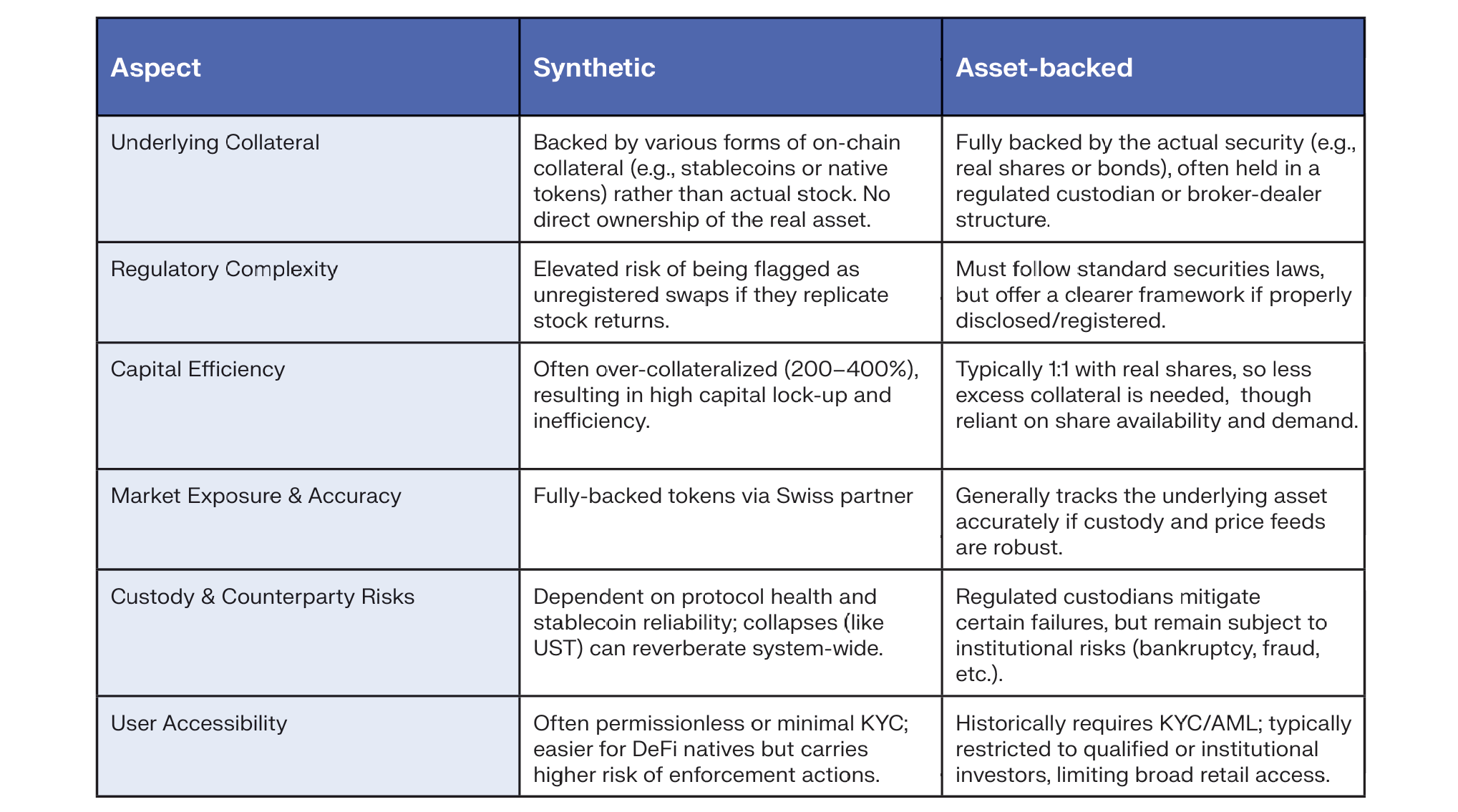

Unfortunately, these synthetic methods were not viable legal methods of creating securitized assets onchain. In the SEC’s 2021 complaint against Terraform Labs’ Mirror Protocol, mAssets were deemed security-based swaps. While a December 2023 federal court ruling rejected this, finding mAssets lacked the bilateral risk transfer required for swaps, it left their broader status as securities unresolved. These products struggled not only from a technological perspective but also from a regulatory perspective. The table below summarizes historical approaches to tokenizing stocks:

Emerging Solutions for Tokenized Stocks

More recent ventures are focusing on compliance from the ground up. A proposed “Broker-Dealer Tokenization Act” in the U.S. aims to give broker-dealers explicit authority to issue and trade securities on distributed ledgers. By classifying “qualified tokenized securities” and allowing “approved broker or dealer” designations for those meeting custody, disclosure, and operations criteria, the bill could smooth the legal path for legitimate tokenized equity markets. This would allow custodians to tokenize a share held in an RWA vault that represents a claim to the underlying asset (similar to how tokenization of treasuries works).

The momentum behind these legislative developments is further reinforced by political shifts, notably the start of the Trump presidency in 2025, which has opened new opportunities for tokenized securities. Industry sentiment reflects this optimism clearly:

“The macro situation has improved dramatically for Real World Assets. With a crypto-friendly administration in the US, strong activity from Europe, Middle East, Africa, and Asia-Pacific regions, and the world’s largest financial institutions like BlackRock making significant strides in tokenization, the time is finally right.”

Chris Yin, CEO and Cofounder, Plume Network

Below is a comparison between asset-backed and synthetic securities:

Several companies are pioneering the current market for tokenized equities with asset-backed securities, with two significant players emerging at the forefront:

Backed Finance:

Backed Finance has developed a regulatory-compliant yet permissionless approach to tokenized equities. As Adam Levi explains:

“We started about four years ago with the idea to bring major assets onchain. After stablecoins became the first kind of real-world assets onchain, we decided the next asset class would be public securities – S&P, Tesla, the big brands. For us, it was very important to have the tokens permissionless. Most security tokens have a whitelist with only 20 people on it, which isn’t very interesting.”

Adam Levi, Co-Founder, Backed Finance

This emphasis on permissionless access represents a fundamental breakthrough in the tokenized securities market. By removing the traditional whitelist restrictions that have hampered security token adoption, Backed is targeting the massive untapped market of global investors who have been systematically excluded from equities markets.

“We were very bullish that it has to be permissionless, which makes it more difficult on the regulatory side. We were able to solve it mostly by relying on Swiss DLT legislation, which is probably the most advanced in the world today. We’re a Swiss company actually issuing out of Jersey Island where the SPVs are located. We have a prospectus with the European Union through the FMA in Liechtenstein that we’ve passported throughout Europe. Our products are MiFID II retail-grade products throughout Europe with permissionless access.” Adam Levi, Co-Founder, Backed Finance

By leveraging advanced Swiss DLT legislation and strategic European regulatory frameworks, Backed has created a model that maintains compliance while achieving permissionless access.

Ondo Global Markets

Ondo has expanded into tokenized equities through their Ondo Global Markets (GM) platform and Ondo Chain infrastructure. Ondo’s approach prioritizes addressing fundamental barriers to bringing securities onchain at scale.

Ondo Chain introduces specialized capabilities designed specifically for tokenized equities, addressing key limitations of general-purpose blockchains. It natively supports corporate actions such as stock splits and dividends, which are difficult to implement within traditional DeFi protocols. Its institutional validator network, operated by financial institutions, ensures regulatory compliance while mitigating risks like front-running and enabling best execution. It also features enshrined proof of reserves, where validators automatically verify with custodians that asset tokens are fully backed by underlying securities.

“Ondo Chain is a Layer 1 proof-of-stake blockchain purpose-built to accelerate the creation of institutional-grade financial markets onchain. By combining the openness of public blockchains with the compliance and security features of permissioned chains, Ondo Chain provides the infrastructure to enable tokenized real-world assets to be used at scale.” —

Ondo Finance

This public-permissioned approach creates a model where regulated institutions can participate in issuing and validating tokenized securities, while the broader ecosystem remains open for users and developers.

This interoperability with DeFi represents a paradigm shift in capital markets access. The combination of access and composability with DeFi protocols creates unprecedented opportunities for global participants previously excluded from traditional finance. The democratization of sophisticated financial tools through non-KYC, permissionless protocols promises to unlock trillions in untapped market potential from previously underserved regions and populations.

The future of Tokenized Stocks

The evolution of tokenized stocks is at a pivotal juncture, highlighted by the necessity for robust regulatory clarity and the establishment of a sound architectural framework. Despite advancements in regulation and infrastructure, adoption has lagged. At their peak in 2021, synthetic stocks had a TVL approximately 300 times greater than that of current tokenized stocks.

For tokenized stocks, the primary challenge has shifted from regulatory concerns to demand dynamics. Unlike tokenized treasuries, which integrate seamlessly into crypto financial primitives and are accessible to a broad audience, tokenized stocks have traditionally faced significant bottlenecks due to KYC requirements. The permissionless model emerging from protocols like Backed presents a solution to this critical barrier, while Ondo’s purpose-built infrastructure addresses the unique technical requirements of securities markets that general-purpose blockchains cannot effectively handle.

Looking ahead, the future of tokenized equities appears promising as both regulatory frameworks and technical infrastructure mature. Backed envisions a future where tokenized equities become standard practice:

The addressable market for permissionless, non-KYC equity access is potentially orders of magnitude larger than the current KYC products. By removing geographical restrictions, minimum investment requirements, and cumbersome identity verification processes, tokenized equities could unleash unprecedented global retail participation.

Drawing parallels to the state of tokenized treasuries in 2023, tokenized stocks appear to be at a similar inflection point. With the proper infrastructure development, enhanced composability within DeFi, and regulatory tailwinds, the growth trajectory could be exponential rather than linear.

Overall, while the foundational infrastructure for tokenized stocks is rapidly developing, substantial market adoption is likely to accelerate dramatically through 2025 and beyond. The combination of permissionless access, specialized infrastructure, DeFi composability, and an improved regulatory landscape creates the conditions for tokenized equities to become one of the most transformative applications of blockchain technology in traditional finance.