The Great Tokenization Shift: 2025 and the Road Ahead

Tokenized Private Credit: How Onchain Lending Is Reshaping Alternative Finance

Private credit built a $1.7 trillion market by filling the gap banks left behind. Now tokenisation is filling the gaps private credit itself could never close: transparency, liquidity, and access.

For decades, alternative lending has been the domain of institutional allocators with the relationships, capital, and patience to navigate opaque structures. Onchain private credit changes that equation. The same lending mechanics — senior secured loans, revenue-based financing, structured tranches — now run on programmable rails where every cash flow is visible, every covenant is enforceable in code, and participation starts at a fraction of traditional minimums.

This is not DeFi lending dressed up in institutional clothing. This is institutional credit infrastructure rebuilt from the ground up.

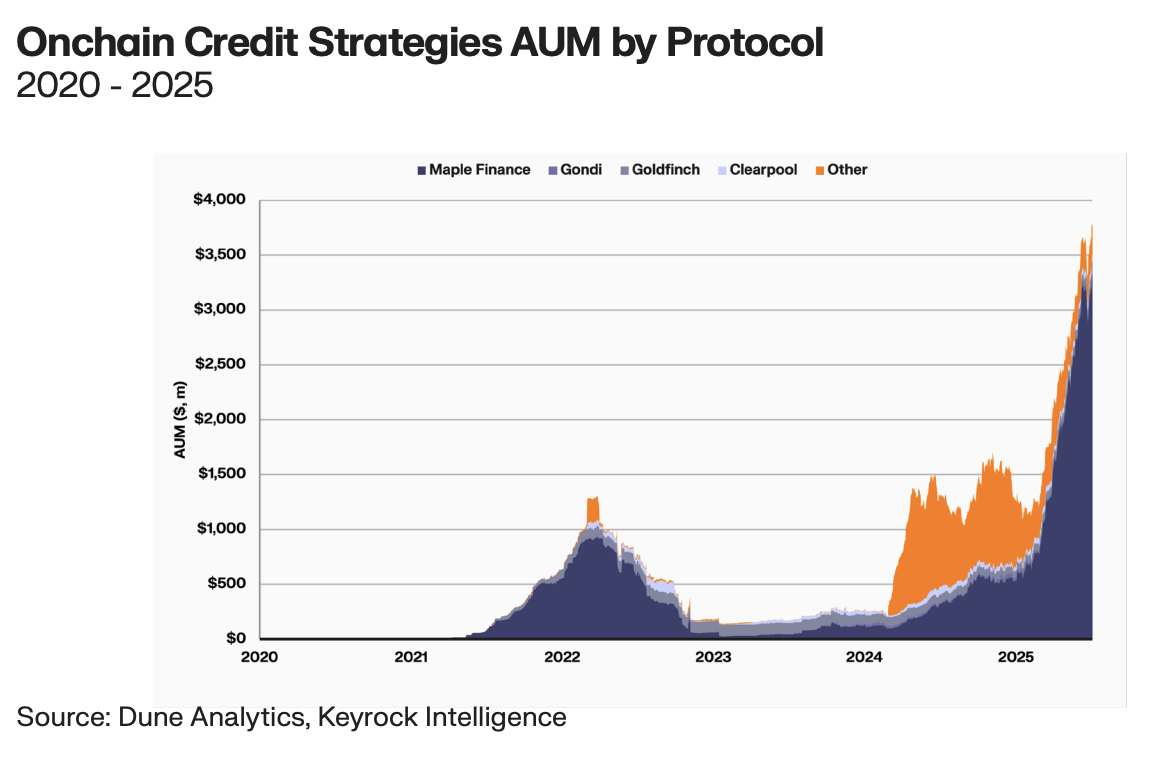

The Private Credit Market: Scale and Structural Gaps

Private credit has been one of the fastest-growing corners of alternative finance. Since 2010, the market has more than tripled as banks retreated from mid-market lending under tighter post-crisis capital requirements. Pension funds, insurance companies, and sovereign wealth funds filled the void.

But the market carries structural limitations that cap its growth:

- Opacity: Loan performance data is sparse. Investors rely on quarterly reports from fund managers with limited real-time visibility into underlying credit performance. Compare that to public bond markets where pricing, ratings, and default data are continuously available.

- Illiquidity: Private credit positions are locked up for years. Secondary market activity is minimal and typically requires bilateral negotiation at significant discounts. An investor who needs to exit a position before maturity faces steep friction.

- Access barriers: Minimum investment thresholds often start at $250,000 to $1 million. Fund structures — limited partnerships, special purpose vehicles — add legal complexity and administrative cost that squeeze out smaller allocators.

- Operational overhead: Servicing private credit involves manual processes for draw-downs, interest payments, covenant monitoring, and default management. Each step adds cost that erodes returns.

Tokenisation addresses every one of these constraints. Not theoretically. In production.

How Tokenised Private Credit Works

The mechanics are straightforward. A lending pool is structured onchain. Borrowers submit loan requests with supporting documentation. Investors commit capital to tranches — senior, mezzanine, junior — based on their risk appetite. Smart contracts govern the lifecycle: origination, funding, interest distribution, principal repayment, and default recovery.

Transparent Cash Flows

Every interest payment, every principal repayment, every default event is recorded onchain. Investors see real-time portfolio performance rather than waiting for quarterly reports that arrive weeks after the period closes. That transparency does not just improve investor experience. It enables better risk pricing.

Programmable Tranching

Tranche structures — the risk layering that defines structured credit — are encoded in smart contracts. Senior tranche holders receive priority repayment. Junior tranche holders absorb first losses in exchange for higher yields. The waterfall logic executes automatically. No discretion. No ambiguity. No operational error in payment distribution.

Fractional Participation

Tokenisation eliminates the minimum investment thresholds that exclude smaller allocators. A credit pool that traditionally required $500,000 to access can be opened to investors committing $1,000 or less. Broader participation deepens the capital base and diversifies the investor profile — both of which strengthen the structure.

Secondary Market Potential

Locked-up capital is a defining feature of traditional private credit. Tokenised positions, by contrast, are transferable. If regulatory and structural conditions are met, token holders can trade their positions on secondary markets without bilateral negotiation or forced discounts. We are not there yet for all products. But the architecture supports it.

Centrifuge: Building the Rails Since 2017

Centrifuge was the first protocol to bring real-world asset lending onchain. Since 2017, they have built the infrastructure that connects off-chain borrowers to on-chain capital.

Their model works through asset pools where originators — fintech lenders, trade finance companies, real-estate developers — tokenise their receivables and draw funding from onchain investors. Each pool has its own risk parameters, tranche structure, and legal framework.

The scale is meaningful. Centrifuge has facilitated hundreds of millions in onchain credit, partnering with protocols like MakerDAO (now Sky) and Aave to channel DeFi liquidity into real-world lending. Their co-founding of the Tokenized Asset Coalition and leadership in shaping the ERC-7540 standard reflect a commitment to infrastructure that goes beyond a single protocol.

Bhaji Illuminati, Centrifuge’s CEO, frames the opportunity directly: institutional capital needs yield. Real-world borrowers need funding. Blockchain is the most efficient rail to connect the two.

The Yield Advantage

Onchain private credit has consistently offered yields above DeFi-native lending and competitive with traditional private credit — while adding transparency and structural improvements.

Senior tranches on tokenised credit pools have delivered yields in the 6–10% range, depending on the underlying asset class and borrower profile. Junior tranches push higher, compensating for subordination risk. These returns reflect real credit risk, not token emission subsidies or governance farming.

The yield comes from genuine economic activity. Trade finance receivables. Equipment leasing. Revenue-based advances to growing businesses. That grounding in productive lending is what separates tokenised private credit from the circular yield structures that plagued earlier DeFi cycles.

Risk: The Unavoidable Reality

Tokenisation improves infrastructure. It does not eliminate credit risk.

Borrowers can default. Economic downturns compress recovery rates. Currency mismatches between onchain capital (typically USD stablecoins) and borrower cash flows (often local currency) introduce FX risk that smart contracts cannot hedge away.

Several tokenised credit pools have experienced defaults since 2022. The response to those defaults — transparent reporting, structured recovery processes, tranche-based loss absorption — demonstrated that the architecture works under stress. But it also made clear that underwriting quality and borrower due diligence remain as critical onchain as they are off-chain.

Smart contracts enforce structure. They do not replace judgement.

Where Keyrock Fits

Liquidity is the bridge between a tokenised credit product and a functioning market. Without it, tokenised private credit remains a subscription-redemption product — better structured than traditional funds, but still fundamentally illiquid.

We build that bridge. Keyrock’s market-making infrastructure provides continuous pricing and order book depth for tokenised assets across 85+ venues. As secondary markets for tokenised credit develop, our role is to ensure that investors can enter and exit positions without the friction that defines traditional private credit.

The onchain asset management ecosystem depends on liquid building blocks. Tokenised credit is one of the most important.

The Road Ahead

Tokenised private credit is growing, but it remains a fraction of the $1.7 trillion addressable market. Scaling requires three things: institutional-grade custody and compliance infrastructure, regulatory frameworks that recognise onchain credit structures, and deep secondary markets that give investors confidence in liquidity.

Each of those pieces is being built. The great tokenization shift is not a future promise for private credit — it is already reshaping how capital meets borrowers. The question is pace. And the data says the pace is accelerating.

Frequently Asked Questions

What is tokenised private credit?

Tokenised private credit refers to alternative lending structures — senior secured loans, revenue-based financing, trade finance receivables — that are originated and managed onchain using blockchain infrastructure. Smart contracts govern the loan lifecycle from origination through repayment, providing real-time transparency, automated payment distribution, and fractional investor participation.

How does tokenised private credit differ from DeFi lending?

DeFi lending protocols like Aave or Compound facilitate overcollateralised crypto-to-crypto loans. Tokenised private credit involves real-world borrowers using tangible assets or receivables as collateral. The credit risk is fundamentally different — it reflects business performance and economic conditions rather than crypto asset volatility. Underwriting, legal documentation, and off-chain enforcement remain essential components.

What yields does tokenised private credit offer?

Senior tranches on tokenised credit pools have delivered yields in the 6–10% range, while junior tranches offer higher returns to compensate for subordination risk. These yields reflect genuine credit risk from productive lending activities — trade finance, equipment leasing, revenue-based advances — not token emission subsidies or circular DeFi strategies.

What are the risks of tokenised private credit?

Credit risk remains the primary concern — borrowers can default regardless of the infrastructure. Additional risks include currency mismatches between stablecoin-denominated capital and local-currency borrower cash flows, smart contract vulnerabilities, regulatory uncertainty, and limited secondary market liquidity. Several pools have experienced defaults since 2022, testing recovery mechanisms and tranche-based loss absorption.