The Great Tokenization Shift: 2025 and the Road Ahead

Tokenised Equities: From Synthetic Assets to Fully-Backed Securities

Tokenised equities started as a workaround. Synthetic tokens that tracked stock prices without conferring ownership. Useful for speculation. Insufficient for markets. The next phase is different — and it changes who can own what, where, and when.

We are moving from derivatives dressed as equity exposure toward fully-backed tokenised securities that carry the same legal rights as shares held in a traditional brokerage account. Settlement on blockchain rails. Custody through regulated infrastructure. Ownership recorded onchain rather than in the fragmented systems of central securities depositories.

The gap between where we are and where we are heading is defined by regulation. Not technology.

The Synthetic Era: What Worked and What Did Not

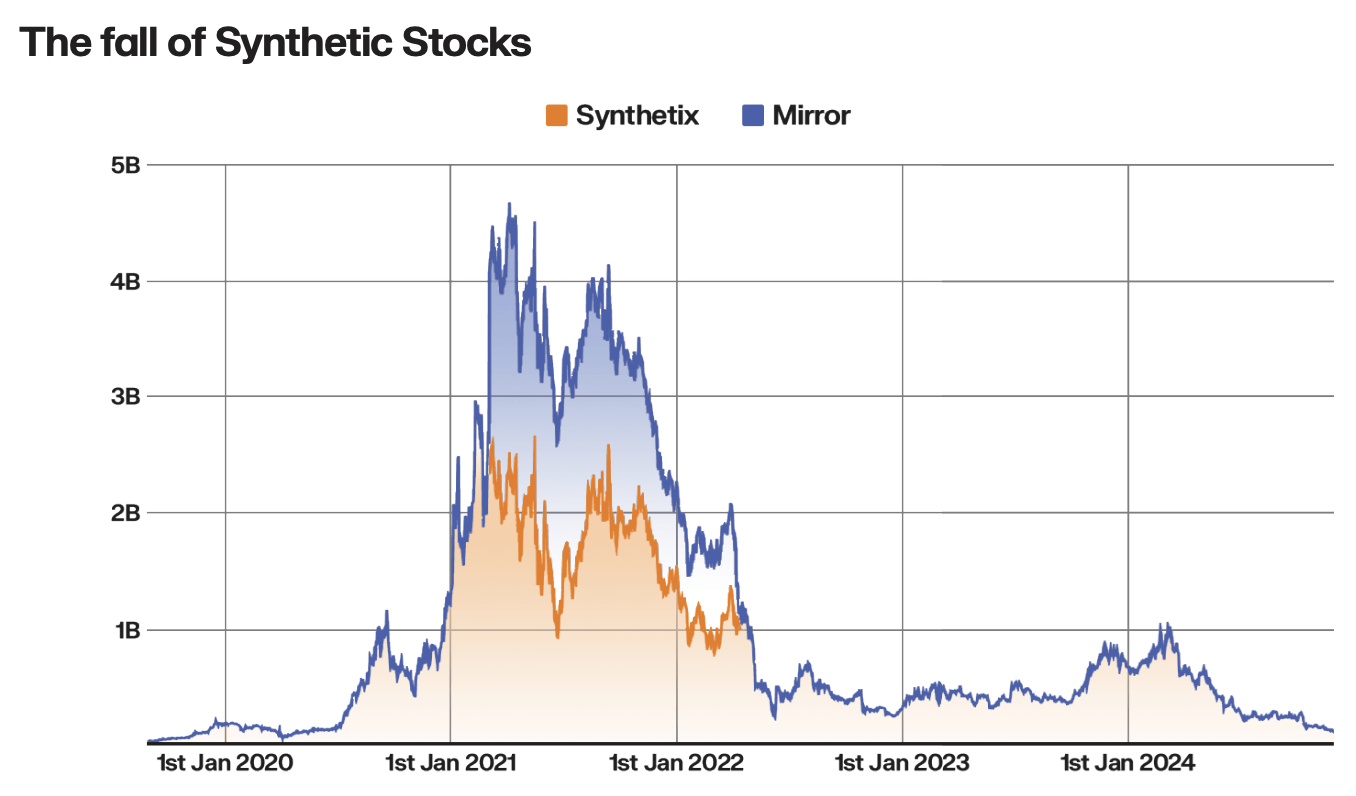

The first generation of tokenised equities were synthetic assets. Platforms like Synthetix and Mirror Protocol (before its collapse) offered tokens that tracked the price of Apple, Tesla, or the S&P 500. No underlying shares were held. No dividends were distributed. The exposure was purely derivative — a contract for difference wrapped in a token.

These products served a purpose. They gave global users access to U.S. equity exposure without the friction of international brokerage accounts, tax treaties, and currency conversion. A trader in Lagos or Manila could gain exposure to NASDAQ-listed companies with a stablecoin and a wallet.

But synthetic tokens had structural limitations:

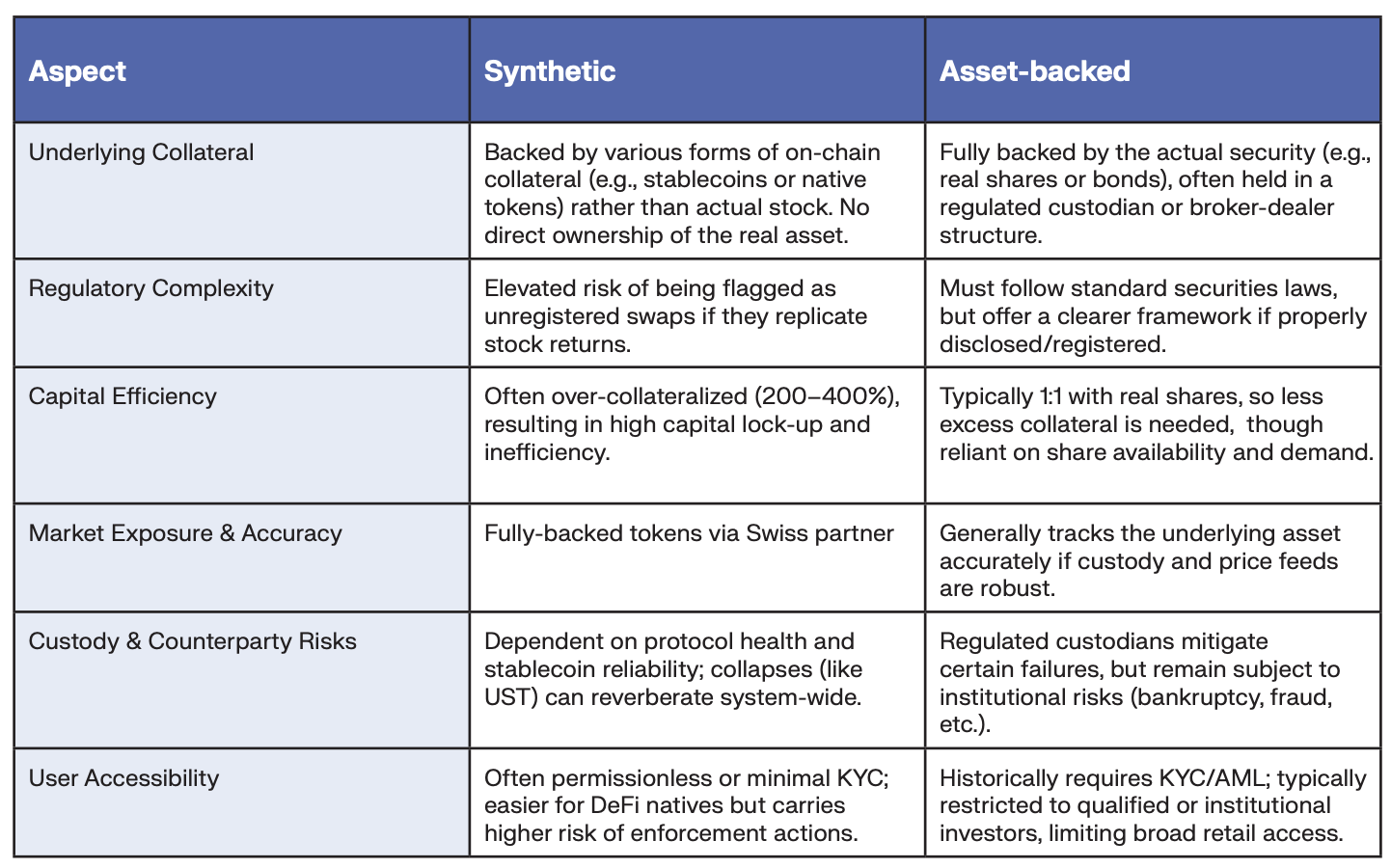

- No ownership rights: Holders had price exposure but no claim on the underlying asset. No voting rights. No dividend entitlement. No legal standing in the event of a corporate action.

- Counterparty risk: The value of synthetic tokens depended on the protocol’s collateralisation mechanism. When collateral ratios dropped — as happened repeatedly during market volatility — the peg to the reference asset broke.

- Regulatory vulnerability: The SEC made clear in 2021 that synthetic equity tokens constitute securities under U.S. law. Binance, FTX, and other platforms shuttered their tokenised stock offerings under regulatory pressure. Mirror Protocol’s tokens were named in SEC enforcement actions.

The synthetic model proved that demand exists. It also proved that demand alone does not build sustainable markets. Legal infrastructure does.

The Fully-Backed Model: What Changes

Fully-backed tokenised equities represent a fundamentally different proposition. Each token is backed by an actual share held in regulated custody. The token confers the same economic and governance rights as the underlying security. Dividend distributions, stock splits, and voting pass through to token holders.

This model transforms equity markets in four ways:

Global Access Without Intermediary Chains

Today, buying a U.S.-listed stock from Europe requires a brokerage account, a custodian chain, currency conversion, and compliance with both home and foreign market regulations. Each intermediary adds cost and delay. Tokenised equities compress that chain. A single onchain transaction can handle trade execution, settlement, and custody transfer simultaneously.

The impact on emerging markets is particularly significant. Investors in countries with limited brokerage infrastructure gain direct access to global equity markets through a wallet and a compliant onramp.

Fractional Ownership at Scale

A single share of Berkshire Hathaway Class A trades above $700,000. Most global investors are priced out of high-value equities. Tokenisation enables fractional ownership at arbitrary granularity — you can own 0.001 of a share if the economics make sense.

Fractional ownership is not new; some brokerages offer it. But tokenisation makes it native, composable, and portable across protocols and platforms rather than siloed within a single broker’s system.

24/7 Trading and Settlement

Equity markets run on fixed schedules. The NYSE operates 6.5 hours per day, five days per week. Pre-market and after-hours sessions add limited additional access at wider spreads. Tokenised equities trade continuously. Information is priced in real time. Settlement is instant.

For global portfolios, this is not a convenience — it is a structural advantage. Rebalancing, hedging, and risk management no longer wait for a bell to ring.

Composability with DeFi Infrastructure

Tokenised equities that comply with recognised standards can plug into the broader DeFi ecosystem. Use tokenised shares as collateral for lending. Include them in automated portfolio strategies. Build structured products that combine equity exposure with fixed-income tokens.

This composability is where tokenised equities meet onchain asset management. The building blocks of traditional portfolio construction — equities, bonds, alternatives — become programmable components that interact natively with each other.

The Regulatory Landscape: Where the Battle Lines Are Drawn

Regulation is both the constraint and the catalyst for tokenised equities. The challenge is not whether securities law applies — it does, unambiguously — but how existing frameworks adapt to blockchain-native issuance, custody, and settlement.

United States

The SEC treats tokenised securities under the same framework as traditional securities. Issuers must register or find exemptions (Reg D, Reg S, Reg A+). Broker-dealer and transfer agent registration requirements apply. Custody must follow the SEC’s customer protection rule.

The upside of this approach: legal certainty. The downside: compliance cost that limits experimentation and slows time-to-market for smaller issuers.

European Union

The EU’s DLT Pilot Regime, launched in 2023, created a regulatory sandbox for tokenised securities. It allows authorised market operators to trade and settle DLT-based financial instruments under modified regulatory requirements. The pilot has attracted participants from across the bloc and generated critical data on operational and regulatory feasibility.

Switzerland and Singapore

Both jurisdictions have moved furthest in integrating tokenised securities into existing legal frameworks. SIX Digital Exchange in Switzerland operates a fully regulated exchange and central securities depository for tokenised assets. Singapore’s MAS has facilitated Project Guardian, testing institutional-grade tokenised equity and bond trading.

The pattern is clear: jurisdictions compete for tokenised capital flows by offering regulatory clarity. Those that succeed attract infrastructure, issuers, and investors.

What Needs to Happen Next

Three conditions must be met for tokenised equities to scale beyond niche to mainstream:

- Cross-border regulatory reciprocity: A tokenised share issued under Swiss law needs a pathway to be held by U.S. or EU investors without duplicative compliance. Mutual recognition frameworks are needed.

- Institutional-grade custody: Regulated custodians must support tokenised equity positions with the same protections — segregation, insurance, audit — that institutional investors require for traditional holdings.

- Deep secondary markets: Issuance without liquidity is a dead end. Market makers like Keyrock — operating across 85+ venues in 37 countries — are essential to building the order book depth that institutional investors demand.

The great tokenization shift is already transforming Treasuries and private credit. Equities are the next frontier. The regulatory evolution now underway will determine how quickly that frontier opens.

The Bigger Picture

Tokenised equities sit at the intersection of capital markets reform, financial inclusion, and blockchain infrastructure development. When fully-backed tokenised shares become as easy to trade as stablecoins — with the same legal protections as shares held at a major brokerage — the addressable market expands by orders of magnitude.

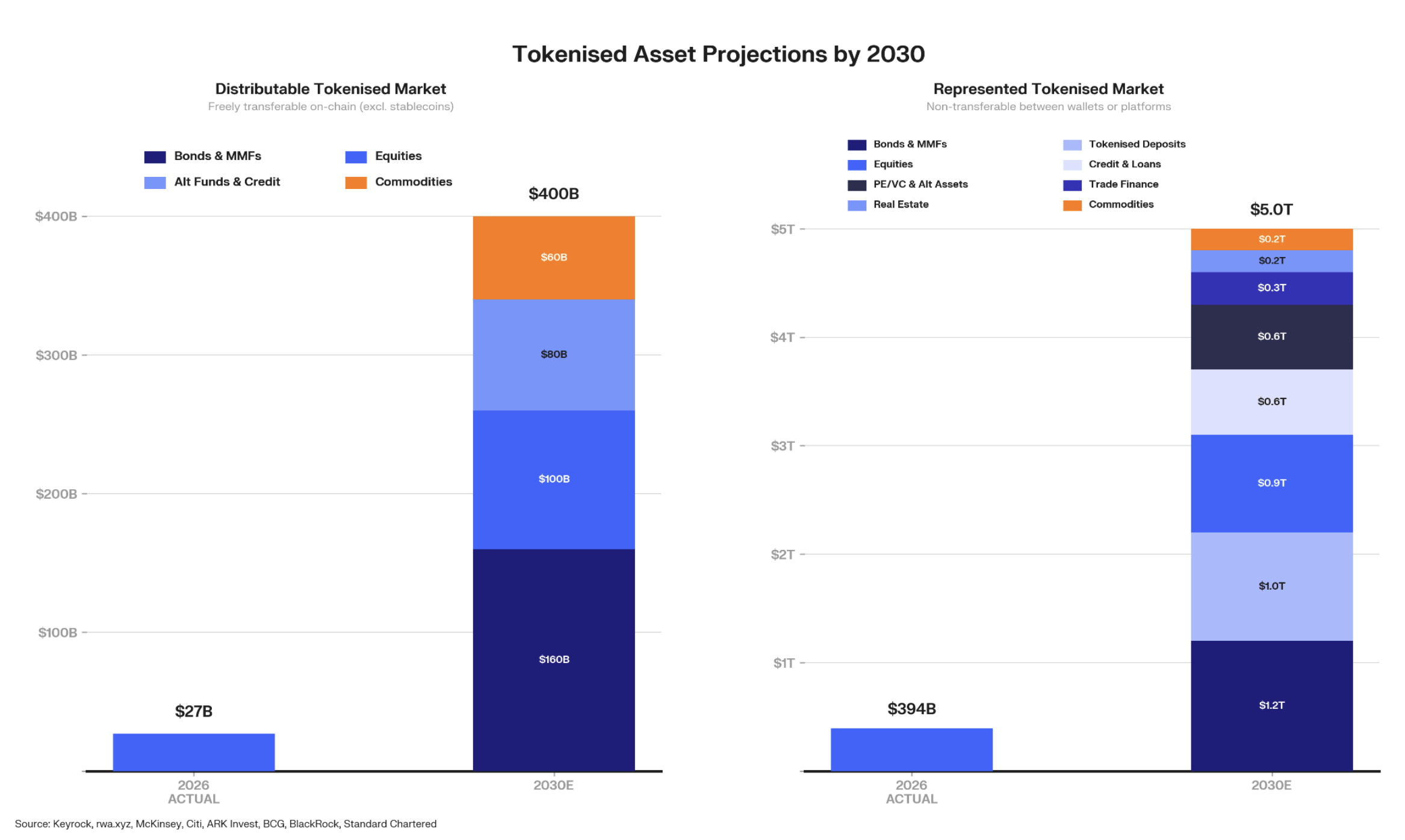

The $400 trillion vision for tokenised assets depends on equities being part of the mix. And the shift from synthetic to fully-backed is the bridge that gets us there.

Frequently Asked Questions

What are tokenised equities?

Tokenised equities are blockchain-based representations of company shares. In the fully-backed model, each token is backed by an actual share held in regulated custody, conferring the same economic and governance rights — dividends, voting, corporate actions — as traditional shares. Earlier synthetic models offered price exposure without ownership, but the market is shifting decisively toward fully-backed structures.

How do tokenised equities differ from synthetic stock tokens?

Synthetic stock tokens are derivative contracts that track equity prices without holding underlying shares. They carry counterparty risk, confer no ownership rights, and face regulatory challenges as unregistered securities. Fully-backed tokenised equities are backed one-to-one by real shares in regulated custody, giving token holders the same legal rights as traditional shareholders.

What are the regulatory challenges for tokenised equities?

Tokenised equities must comply with securities law in every jurisdiction where they are offered. Key challenges include cross-border regulatory reciprocity, broker-dealer and custody requirements adapted for blockchain settlement, and the cost of compliance for smaller issuers. The EU’s DLT Pilot Regime and Singapore’s Project Guardian are testing frameworks to address these constraints.

Can tokenised equities be used in DeFi?

Yes, when they comply with recognised token standards and regulatory requirements. Tokenised equities can serve as collateral in lending protocols, components in automated portfolio strategies, and building blocks for structured products. This composability is a core advantage over traditional equity infrastructure, enabling integration with the broader onchain asset management ecosystem.