Defining Discretionary Onchain Strategies

While automated strategies leverage onchain financial instruments through pre-determined, static rules, and generally offer a more vanilla strategy, discretionary onchain strategies take this a step further by allowing for dynamic strategy adjustments. These are strategies in which portfolio allocation and risk management decisions are made by human managers in real time, often supported by quantitative models or semi-automated execution. Active management practices rotate between lending markets, liquidity pools, derivatives venues, and cross-chain opportunities at the discretion of individuals or systems that lay offchain, to capture idiosyncratic yield or hedge risk dynamically. These vaults combine discretionary oversight with onchain transparency, positioning them as crypto-native equivalents of hedge funds, but operating entirely on programmable, auditable rails.

In practice,discretionary onchain strategies sit across multiple layers of the stack at once, inherently spanning on and offchain. Managers deploy into money markets such as Aave or Morpho, trade through DEXs and perpetuals venues like Uniswap, GMX, or Aevo, and increasingly integrate with yield tokenisation platforms such as Pendle. Cross-chain execution has also become more common, much more so than in automated strategies, given this offchain intervention. These strategies rely heavily on analytics dashboards, bots, and private relays to protect execution quality, with discretionary calls from the manager guiding allocation shifts on top of the automated plumbing.

History and Evolution of Discretionary Onchain Strategies

The roots of discretionary onchain strategies lie in the earliest experiments with discretionary management layered on top of automated protocols. In the immediate aftermath of DeFi Summer, most onchain capital chased programmatic yield strategies, as aforementioned, with lending on Aave, farming on Compound, or pooling liquidity on Uniswap. It did however, become abundantly clear that the real opportunities were more dynamic than this vanilla, and at the time limited, way of managing capital. Funding rates swung widely, and with new protocols launching in quick succession, particularly cross-chain, the onchain asset management capabilities couldn’t keep up. This environment gave rise to the active manager, combining discretionary judgement with onchain execution, able to leverage traditional finance reputations and trust with a peaking interest in the immense alpha being generated onchain.

The strategy sector matured to what we would refer to as ‘graduation status’, in which it saw growth rates that had been seen in automated strategies, but to date had previously escaped discretionary onchain strategies, once risk frameworks and execution tools improved. Managers like Re7 and MEV Capital codified their approaches into branded vaults, blending discretionary calls with automated infrastructure to deliver consistent returns. These vaults began to attract not just retail but DAOs and institutions, drawn to the combination of professional reputation and oversight and real-time onchain visibility. Improved MEV protection, better cross-chain routing, and the emergence of portfolio analytics dashboards gave allocators confidence that active managers could operate at scale without exposing them to unacceptable operational risks.

Today, discretionary onchain strategies sit at the frontier of onchain asset management, and we’d argue is primed to onboard arguably the majority of capital into DeFi through its deep ties to institutional capital.

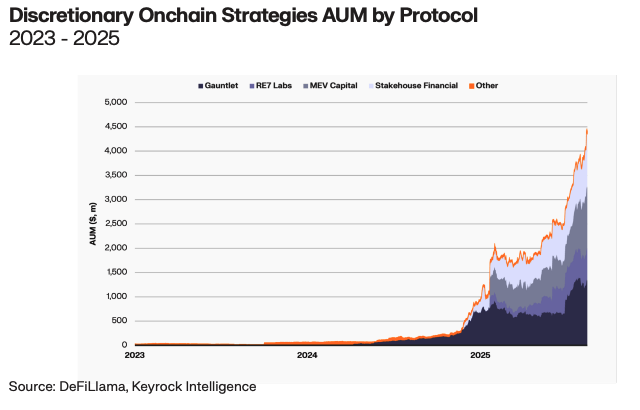

Discretionary onchain strategies have truly exploded in 2025, with aggregate AUM climbing to nearly $4.5 billion after years of relative dormancy. The sharp growth this year reflects two converging dynamics, the first being that allocators are seeking hedge-fund-like exposure without the traditional 2/20 fee drag, and the second being the maturation of firms professionalising active management onchain.

Leadership has consolidated quickly around a handful of names. Gauntlet and RE7 Labs are carving out institutional niches with multi-strategy approaches, while MEV Capital has leaned heavily into execution advantages unique to DeFi, particularly around MEV capture and order flow. Stakehouse Financial adds a layer of discretionary credit and structured products, creating hybrid offerings.

This article is a part of a series on Onchain Asset Management.

Comparing Discretionary Onchain Strategies to Traditional Finance Counterparts

Discretionary onchain strategies represent actively managed vaults where offchain input from curators, those making decisions on how to allocate capital, guides execution, rather than entirely onchain, smart contract-driven, hard-coded logic. The aim of discretionary strategies is to deliver alpha through active positioning across networks, protocols, strategies and assets. Allocators to these strategy types are typically DAO Treasuries, institutions or HNWIs.

Onchain, the strategies leveraged to generate alpha can include capturing spreads in funding, MEV, which can be thought of as exploiting the ordering of transactions for economic gain, or basis opportunities unavailable to passive vaults. In principle, this is no different from discretionary hedge funds in traditional finance, which similarly seek to monetise market or structural inefficiencies, whether through tactical asset allocation, directional macro trades, relative value spreads, or event-driven plays. The key distinction is in the context, whereby onchain managers exploit operational and structural inefficiencies unique to blockchain execution, such as composability and MEV, while traditional hedge funds draw more heavily on economic cycles and cross-asset pricing dislocations. Where inefficiencies differ, it is usually because of differences in market structure, for instance, front-running is outlawed in traditional finance but persists onchain in the form of MEV.

or discretionary strategies, the mapping is slightly more straightforward, in that traditional finance offers some clear-cut discretionary strategies, such as actively managed hedge fund strategies. We compare three flavours of these strategies as potential comparators, namely Global Macro Hedge Funds (GMHFs), Multi-Strategy Hedge Funds (MSHFs) and Quant or Arbitrage Hedge Funds (AHFs).

| Potential Comparator | Comparative Relevance | Comparative Shortcomings | Overall Suitability |

| Global Macro Hedge Funds (GMHFs) | Active managers shifting allocations across assets, rates, and strategies. | Broader mandate such as macro markets, FX and commodities, vs. narrower onchain focus. | Primary comparator |

| Multi-Strategy Hedge Funds (MSHFs) | Multiple alpha sources, manager discretion, risk-adjusted returns. | Diversified across more asset classes. | Secondary comparator |

| Quant or Arbitrage Hedge Funds (AHFs) | Systematic, capture funding spreads, arb inefficiencies. | Heavily model-driven with high-frequency adjustments. | Adds nuance, but not a close comparator. |

The primary comparator to discretionary onchain strategies chosen is GMHFs, given both represent discretionary, opportunistic, active allocation strategies. To this end, the process for both is tactical rotation of capital based on market conditions, with primary return drivers being portfolio manager edge and timing advantages. The standout difference in these strategies however, is liquidity, in which GMHFs are often gated with quarterly liquidity, while onchain discretionary strategies typically offer near-instant liquidity, but are capacity-limited. Beyond liquidity, discretionary onchain strategies provide allocators with real-time transparency into positions and performance. Portfolio data updates block-by-block onchain, offering a level of granularity and immediacy that contrasts sharply with the monthly or quarterly reporting cycles typical of hedge funds.

MSHFs are another close comparator, reflecting diversified alpha approaches similar to those seen in onchain discretionary approaches. MSHFs are very similar to GMHFs as well, in that we see manager discretion, and a focus on risk-adjusted returns. The only slight caveat here is that MSHFs operate across multiple asset classes, while discretionary vaults are still mostly confined to digital markets, although the breadth of digital asset class coverage is expanding.

The combination of GMHFs and MSHFs will be compared with discretionary onchain strategies by leveraging weighted averages for fee and performance comparisons, in conjunction with qualitative assessment.

Benefits and Drawbacks of Discretionary Onchain Strategies Relative to Traditional Finance Counterparts

Discretionary onchain strategies inherit many of the inherent advantages of operating onchain while offering distinct improvements over traditional hedge funds. Withdrawal flexibility is one of the most significant, with investors able to redeem capital near-instantly at will, in contrast to the rigid lock-ups that define much of the hedge fund industry, typically following monthly or quarterly lock-ups. This flexibility is underpinned by the same permissionless rails that support automated strategies, ensuring access and liquidity without the need for intermediaries.

Efficiency also stands out as a defining characteristic. Managers can shift capital between protocols in minutes, settle transactions instantly, and provide live reporting on positions. Strategies that in traditional markets might take weeks to execute and reconcile can be completed atomically, with full transparency and auditability onchain. For allocators, this translates into daily liquidity and real-time visibility into risk exposures.

Fee structures further highlight the divergence. Onchain, managers typically adopt flatter models, often charging only performance fees. Smart contract automation strips out much of the operational overhead, eliminating the need for layers of intermediaries and administration that justify management fees in traditional funds. This means that allocators face lower costs and fewer fee burdens, while still gaining exposure to discretionary management. That said, there is a clear tradeoff between speed of execution, and strategy protection that we’ll touch on later in the report.

Perhaps most compelling is the composability enabled by onchain infrastructure. Discretionary managers can combine protocols and assets in ways that are structurally more complex offchain, borrowing in one venue, hedging in another, and pooling liquidity in a third, all without introducing custody chains or counterparty risk. This modular toolkit allows exposures to be built in days that would take months to structure in traditional finance. The result is a uniquely hybrid model, where human judgment and programmable infrastructure reinforce one another to deliver a new, more agile form of discretionary management.

Discretionary strategies deployed onchain have many benefits over equivalent traditional finance strategies, though it’s important to note that we are not comparing apples to apples here, and as such, the onchain strategies have distinct drawbacks. As mentioned in onchain passive strategies, the primary risk most often cited is that of operational and smart contract risk. For discretionary strategies, this includes both the smart contracts of the underlying onchain strategies, and the smart contracts responsible for execution and protocol integrations, which can be exploited or fail. Hedge funds on the other hand benefit from institutional-grade infrastructure, prime brokers, custodians and compliance frameworks. In this sense, the very structure that we argue makes traditional strategies inefficient and slow protects the strategies via prudent operational processes.

We also see capacity constraints in discretionary onchain strategies, with strategies often having to implement TVL caps due to liquidity fragmentation across DeFi markets, or liquidity thinness that if challenged would compress returns. It’s worth noting, however, that discretionary strategies have advantages over passive onchain strategies here, in that they can generally deploy capital across networks, protocols and assets to manually access a broader range of yield opportunities. It goes without saying here that hedge funds can scale capital deployment into trillion-dollar markets without the same bottlenecks.

One product-specific risk aspect for onchain discretionary strategies that’s improving, but still exists, is the risk management tools deployed. We’re seeing risk management improvements through the use of offchain monitoring bots that are capable of complex risk mitigation procedures such as circuit-break strategies in the event of asset de-pegs and the simulation of incoming transactions ahead of time to identify exploits and hacks. However, the risk management tools deployed by discretionary strategies remain rudimentary compared to hedge funds’ use of sophisticated risk models, hedging instruments and compliance oversight. This is largely due to the fact that the hedge fund industry is a different beast to onchain discretionary strategies as they exist today, with customers paying millions in fees for hedge funds to employ armies of the brightest quants combined with millions of lines of systematic risk management code.

Of course, reputationally, discretionary strategies are limited by the same concerns that arise with all onchain strategies, such as a lack of regulatory and legal clarity that exists for hedge funds, operating within clear legal wrappers with fiduciary duties and investor recourse. This goes hand in hand with the fact that hedge funds have multi-decade track records and strong reputational capital that attracts institutions. That said, we are not comparing apples to apples, and onchain discretionary strategies are a new, innovative implementation that has the potential to gain trust with continued performance. All new innovations once lacked experience relative to their competitive products.

Discretionary Onchain Yield Strategies Fees and Performance

As outlined earlier in this section, the closest parallels to onchain discretionary strategies are Global Macro Hedge Funds and Multi-Strategy Hedge Funds, which similarly rely on manager discretion to rotate capital across markets and exploit inefficiencies.

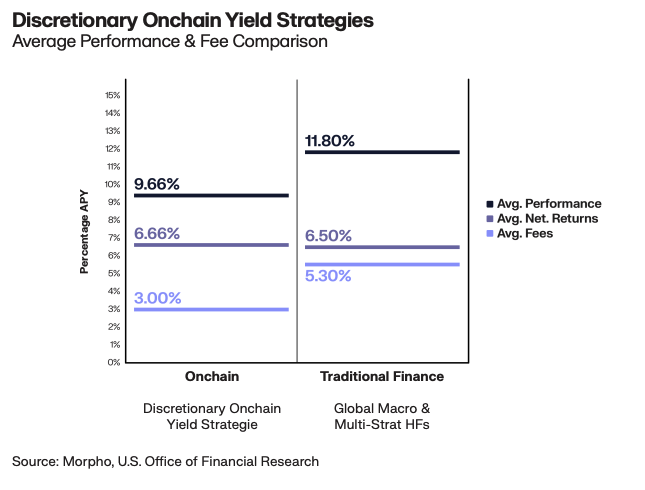

Onchain discretionary strategies delivered a weighted-average gross return of 9.66%, compared with 11.80% in the traditional hedge fund sample. Within DeFi, examples such as Gauntlet’s eUSD Core and Smokehouse’s USDT vault posted double-digit returns, while larger vehicles like MEV Capital’s USDC strategy generated mid-to-high single-digit yields. Collectively these strategies remain modest in scale, with AUM under $400 million across the sample. By contrast, our traditional finance comparators operate at vastly greater scale, with Bridgewater’s Pure Alpha II alone managing over $76 billion, while Blackstone’s Alternative Multi-Strategy Fund holds nearly $4 billion. That these funds can still deliver high single- to low double-digit performance at such size underscores the operational depth and efficiency advantages of traditional hedge fund infrastructure.

Fees remain one of the sharpest contrasts. Onchain discretionary funds average 3.00%, generally structured as pure performance-based compensation with fewer fixed layers. Hedge funds in traditional finance, by contrast, adhere more closely to the ‘2 and 20’ model, with our sample showing an effective weighted-average fee load of 5.30%. This reflects both management and incentive layers, as well as the higher operational overhead of running diversified, global mandates. Scale does not necessarily compress fees in traditional finance hedge funds the way it does in passive vehicles, but allocators often accept the trade-off given the track record, brand, and institutional processes attached to these funds.

After fees, the picture converges. Onchain discretionary funds generated a weighted-average 6.66% net return, nearly identical to the 6.50% net return from traditional peers. Despite operating in a nascent ecosystem with far smaller pools of capital, DeFi discretionary managers are delivering outcomes competitive with the largest and most established hedge funds in the world. Looking forward, the sustainability of this convergence depends on two forces. On one hand, traditional finance funds show they can scale performance even at tens of billions in AUM. On the other hand, DeFi offers structural advantages in redemption liquidity, transparency, and cost automation that could support performance resilience as these strategies scale. For allocators, the takeaway is that discretionary DeFi strategies have matured into a credible peer set, with comparable net-of-fee returns despite radically different infrastructure and scale dynamics.

Allocator Profiles to Discretionary Onchain Strategies

The audience for discretionary onchain strategies differs markedly from passive from a depositor count perspective. While anyone with a wallet can technically deposit, the target allocator base skews towards DAOs, institutions, and high-net-worth investors looking for alpha rather than steady, programmatic yield.

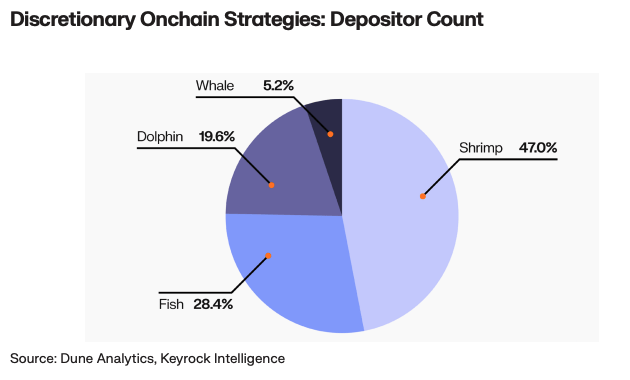

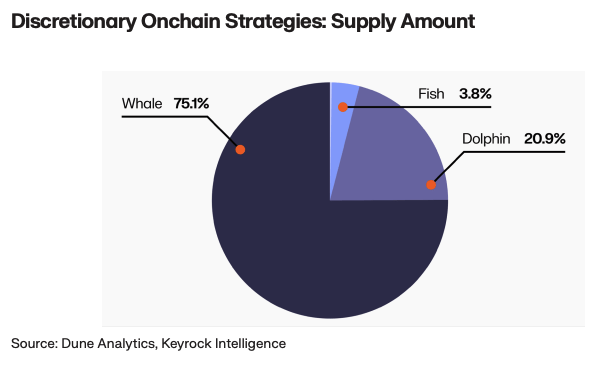

This is evident by the fact that Fish, Dolphins and Whales, defined as allocators above $10k per deposit, make up ~53% of depositors in aggregate. This comes down to slightly higher minimum thresholds in some discretionary vaults, but also reflects the more institutional nature and bespoke service that many managers provide. Access models also vary, with some vaults being permissionless but manager-directed, while others require whitelisting and KYC.

Interestingly, when looking at supply amount, we see only a 75.1% dominance from Whales, whereas in passive onchain strategies this figure sat at 94.3%. In discretionary strategies we see a higher concentration of ‘middle’ sized allocators, ranging from $10k to $1 million, at 24.7% in discretionary versus 5.61% in passive onchain strategies.

Discretionary strategies are more bespoke and experimental, and often carry higher operational or infrastructure risk. This naturally attracts smaller funds, DAOs and HNWI which make up this ‘middle cohort’. It’s also partially a reflection of product-market fit, in which passive strategies have established credibility onchain, while discretionary strategies, a newer strategy style, are yet to gain the full trust of capital allocators.

Interestingly, when looking at supply amount, we see only a 75.1% dominance from Whales, whereas in passive onchain strategies this figure sat at 94.3%. In discretionary strategies we see a higher concentration of ‘middle’ sized allocators, ranging from $10k to $1 million, at 24.7% in discretionary versus 5.61% in passive onchain strategies.

Discretionary strategies are more bespoke and experimental, and often carry higher operational or infrastructure risk. This naturally attracts smaller funds, DAOs and HNWI which make up this ‘middle cohort’. It’s also partially a reflection of product-market fit, in which passive strategies have established credibility onchain, while discretionary strategies, a newer strategy style, are yet to gain the full trust of capital allocators.

Catalysts for Discretionary Onchain Strategies Growth

Discretionary onchain strategies have, and will continue to benefit from, a shift in allocator behaviour and advances in infrastructure. After years of skepticism, discretionary managers like Re7 and MEV Capital have demonstrated that human-directed strategies can rotate across ecosystems, hedge dynamically, and capture basis or funding spreads unavailable to static vaults. This track record has attracted high-net-worth and institutional mandates that want the risk management sophistication of Traditional Finance hedge funds but executed entirely onchain. We also see the lack of experience bottleneck referenced in the automated strategies section playing out here, with many institutional managers seeing discretionary onchain strategies as a compromise, in which they are able to trust, and more importantly get bot-optimised, with human-oversight strategies past their investment committees, while still engaging in onchain strategies and benefiting from higher yield.

Technical maturity is improving, closing one of the biggest gaps. Portfolio dashboards, real-time risk analytics, and compliance-ready reporting are emerging, reducing the operational blind spots that once deterred institutions. MEV protection, which is a mechanism that protects traders from practices like front-running, is also becoming standardised, for example Jito’s BAM on Solana, and private transaction relays on Ethereum, are addressing concerns about execution integrity that would otherwise undermine allocator trust.

AI can then be brought into the conversation, as in discretionary onchain strategies specifically it’s an integration acting as a force multiplier. Real-time data feeds and adaptive risk scoring give managers the tools to operate with higher precision, while automation handles rebalancing and monitoring. For allocators, this blend of discretionary oversight and machine-driven efficiency makes active DeFi vaults look less like experimental trading desks and more like credible, technology-augmented hedge funds.

Gauntlet is the largest discretionary strategy curator onchain by assets under management, that specialises in risk-optimised vault strategies. In essence, the strategies offered to depositors look and feel very similar to those in automated strategies, except Gauntlet combines the onchain capital placement with offchain automated optimisation engines, which are codified bots overseen by human risk managers, which have been honed since 2018. These strategies are a step higher up the onchain asset management stack to automated strategies, in that they will deposit to, and rotate between, venues like Morpho and Yearn vaults, Pendle PT and YTs, and onchain credit products.

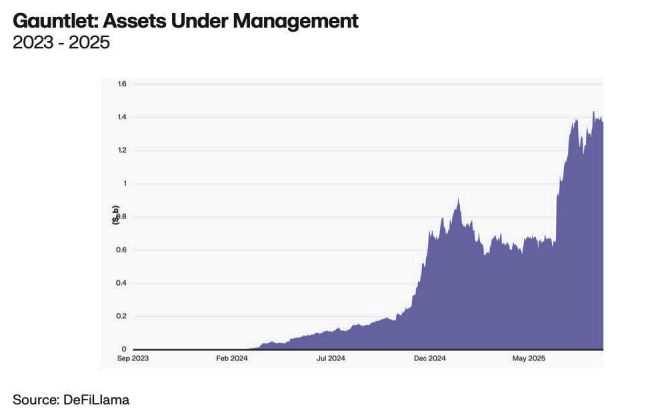

Today, Gauntlet has accumulated ~$1.4 billion in AUM, and has continuously touched between 30% and 80% of DeFi’s entire TVL via its risk models. Gauntlet uses permissionless DeFi rails to execute investment strategies that aren’t possible today in traditional finance, namely instant leveraging and looping of composable strategies. Simon Mathonnet, Product Marketing Lead at Gauntlet, highlighted the bureaucracy of traditional financial markets, and how onchain strategies offer improved solutions, “if you were an LP in a private credit fund and wanted to lever up, it’d be a nightmare of paperwork. Onchain we can do this in seconds, permissionlessly.” Underneath this, curators like Gauntlet leverage the composability of the underlying tokenised strategies, “composability in DeFi enables a lot… you supply base USDC and tap into mainnet yield, Pendle PTs, and more, all through a single vault.”

The core messaging of curators like Gauntlet is that they utilise both automated optimisation and light-touch human oversight to ensure that these strategies produce risk-adjusted yield. This was evident in a recent DEX exploit, in which Gauntlet leveraged their light-touch human intervention to prevent a $120k loss to Uniswap on an incentives scheme hack. This human oversight is not offered in purely automated onchain strategies, and highlights the benefits of the variety of onchain asset management strategies offered today.

Simon Mathonnet, Product Marketing Lead at Gauntlet highlights an interesting potential catalyst to the onchain asset management industry over the coming 12-18 months, particularly for discretionary strategies, in the rise of tokenised equities onchain. Simon expects a core growth vector to be an expanding cohort of assets available onchain, as well as deepening liquidity, with the largest potential growth being tokenised equities. With the launch of xStocks and Ondo equities, the tokenised equities AUM onchain has rapidly grown to $100 million, with further liquidity anticipated as allocators get comfortable with this new asset entrant to the onchain rails ecosystem. Aside from tokenised equities, stablecoins remain a core growth vector, having already driven the majority of onchain asset management strategies.

MEV Capital positions itself as a discretionary DeFi yield fund, with a particular focus on market neutral strategies denominated in the deposit asset. In this sense, their vaults offer exposure to the underlying asset with yield generated from their market neutral investment strategies. The core philosophy of these strategies is to be executed fully onchain, to be transparent, and importantly, non-custodial from inception, inspired by the mistrust era of 3AC, Celsius, FTX.

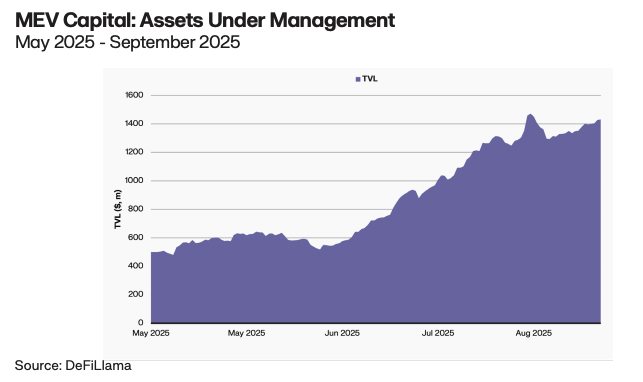

When exploring onchain asset management, MEV Capital should be on your radar as it has become one of the more sophisticated onchain discretionary managers, appealing to both retail and institutional allocators. The investment firm has seen extraordinary growth in H2 this year, increasing its AUM by 91% since late June to a total of $1.432 billion. This positions MEV Capital as one of the top discretionary strategy funds alongside Gauntlet.

MEV Capital differentiates itself through a focus on market-neutral, and asset, as opposed to dollar, denominated strategies. These strategies are becoming increasingly popular in discretionary strategies onchain, in which allocators are able to capture yield on volatile assets while maintaining the underlying exposure.

MEV Capital further differentiates itself through its trust-minimised operating model, designed to reassure allocators. Rather than handing over custody to a manager, clients retain majority control of vault assets through a multi-sig or MPC structure. MEV Capital can propose transactions, but cannot execute them without client authorisation, which can be pre-determined for certain actions. As COO Gytis Trilikauskis explained, “The majority of keys would be held by the client, allowing MEV Capital only to initiate operations, but never to validate them without the client’s knowledge.” This design ensures transparency and client oversight, aligning the vault infrastructure with institutional standards of governance, and is becoming a standard across discretionary strategies onchain.

Risk management is another cornerstone of MEV’s positioning. The firm applies a dual-lens framework to every allocation, assessing both the underlying asset issuer and the protocol in which capital is deployed. Exposures are tiered according to risk appetite, with additional monitoring conducted through third-party tools like Hexagate and Hypernative. These third-party monitoring tools are able to simulate transactions prior to block inclusion, to catch malicious attacks on protocols or wallets alike and prevent the impact in real-time. This layered approach allows the team to anticipate vulnerabilities before they become critical, providing allocators with a level of assurance that’s considered a step up for onchain asset management strategies.

It’s worth noting that MEV has refined its operational oversight by combining automation with human controls. While execution is automated onchain, all material operations are subject to a ‘four-eyes’ principle, requiring manual verification before completion. This hybrid approach strikes a balance between the efficiency of programmatic execution and the prudence of human review, offering allocators confidence that speed does not come at the expense of oversight. This is primarily where passive strategies differ from the more discretionary strategies onchain from a risk perspective.

Looking ahead to the future, MEV Capital COO, Gytis Trilikauskis, highlighted three areas in which the investment firm sees strong potential for growth in the onchain asset management industry. The first is the growth of RWAs, which will materially expand the asset and liquidity base to which these funds can allocate. Gytis sees major growth in tokenised credit and insurance, once onchain redemption cycles are engineered to match onchain liquidity norms, “RWAs will really take flight once redemption cycles align with DeFi instant liquidity expectations.”

Moreover, Gytis sees a significant catalyst for growth coming from the convergence of Digital Asset Treasuries (DATs) and traditional finance structures. Trilikauskis stressed that DATs are rapidly becoming the ‘next wave’ of allocators, driving flows into onchain strategies as they seek more efficient ways to manage balance sheets. “What excites me most is the rise of treasury companies built entirely on top of Bitcoin or Ethereum,” he noted. “These DATs are essentially listed entities that can channel institutional-grade capital directly into onchain strategies, and that’s where I think the biggest inflows will come from over the next cycle.” As more DATs spin up, they are forced to innovate and compete on ways to generate yield on their assets, both to achieve sustainability by covering dividend and debt interest payments, but also to compete on increasing their underlying assets per share over time. While the pioneers such as Strategy have opted to securitise their underlying Bitcoin and generate a yield by taking to traditional financial markets, newer DATs, particularly those focused on assets with a lesser reputation on Wall Street, are looking to DeFi. This is evident in communication from Kyle Samani, Managing Partner at Multicoin Capital and now Chairman of Forward Industries, a Solana DAT, when Samani stated that he aims to integrate SOL held on Forward Industries balance sheet to Solana DeFi in order to generate a yield on their underlying assets.