30 June 2025

Ticking into Tariffs

From Caution To Charge

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

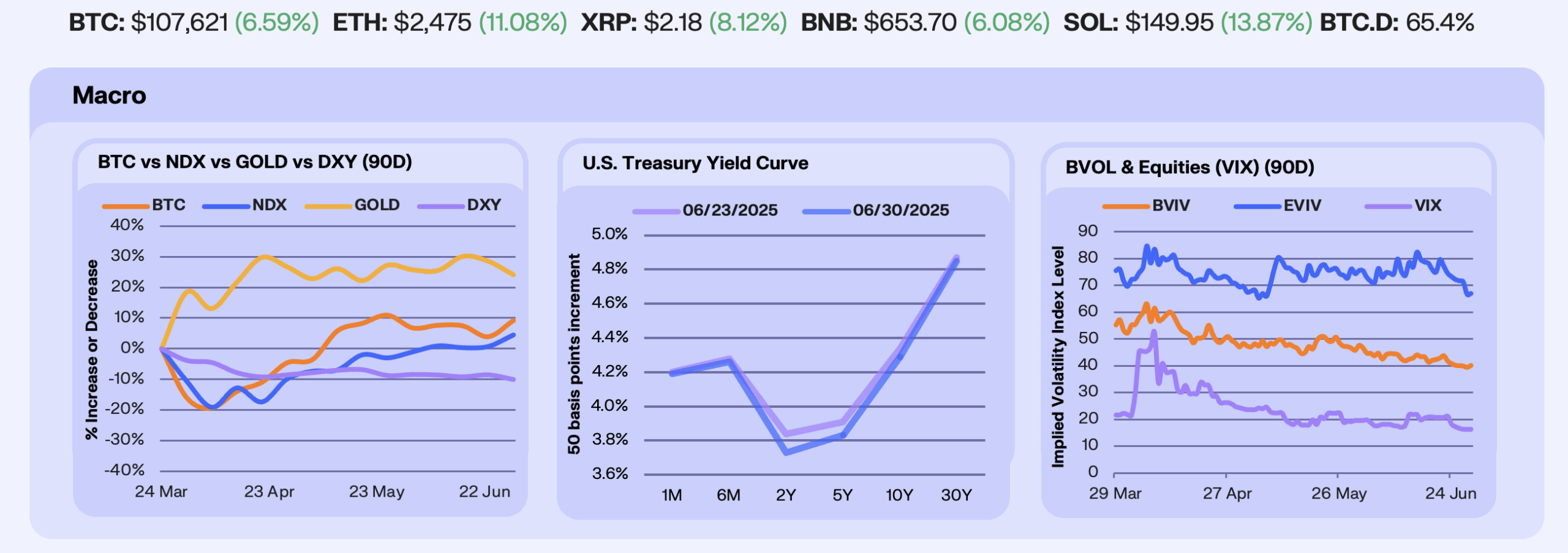

Last week’s Israel-Iran ceasefire shifted sentiment away from flight to-safety as Gold (-3.5%) fell, Bitcoin rallied (+5.1%), and the Nasdaq hit all-time highs (+3.8%). A weaker Q1 GDP (-0.5%) print, negative MoM income growth, and a potential for Fed Chair leadership change reinforced expectations of an earlier Fed pivot as the U.S. Dollar (-1.7%) sold off to 3 year lows. This was reflected in a mild bull flattening of the U.S. Treasury yield curve, led by the belly. The 2Y yield fell 11 bps on growing confidence in near-term Fed easing amid weakening growth and negative income data, while longer-dated yields (10-30Y) declined only marginally, signaling persistent inflation concerns. This flattening dynamic suggests traders are positioning for policy easing in the near-term while hedging against structural inflation risk in the longer-term.

Bitcoin volatility hit August 2023 lows while Ethereum remains range bound YTD, with over $17b in options expiring last Friday across both assets, representing 30% of current positions and marking a key reset point for positioning. With Bitcoin volatility subdued, traders are shifting focus to Ethereum options and positioning for potential July downside. This shift suggests growing demand for directional exposure in ETH and may set the stage for increased volatility-led flows in the weeks ahead.

Our Take: With Trump’s tariff pauses ending July 9th (EU) and August 12th (China), markets face renewed uncertainty, which could reprice rate expectations and reignite volatility. While Bitcoin volatility remains subdued, ETH’s IV stays elevated at nearly 71%, offering more room for defined-risk trades and creating opportunities for option strategies like put spreads and call selling to express downside views while collecting premium in a low-conviction market.

Fundamentals Fuel Altcoins

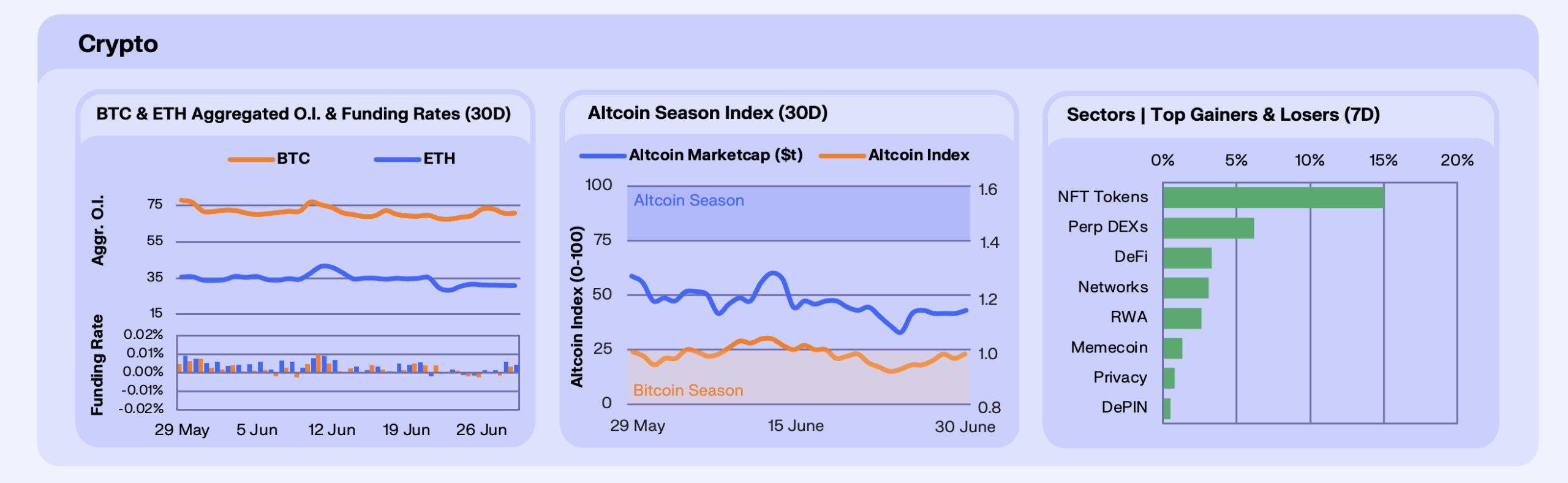

In the derivatives markets, both Bitcoin and Ethereum saw increases in open interest, with Bitcoin rising from $67.6b to $70.9b (+4.9%) and Ethereum climbing from $28.2b to $30.7b (+8.9%), while SOL CME Futures volume hit an all-time high of 1.75m contracts. However, Bitcoin’s funding rate keeps trending lower, indicating traders are scaling back leveraged long exposure in favor of more defensive positioning. This is especially notable given Bitcoin is just ~4% off all-time highs and shows no signs of excessive leverage, reinforcing the idea that this range may be establishing a new floor.

As macro catalysts drive renewed positioning across risk assets, altcoins (+6.4%) rebounded on improved sentiment and stronger fundamentals. Among the leading performers this week were PENGU, SEI, and EULER, driven by strong fundamentals and growing interest. SEI reached all-time highs in 30D MA transactions (1.3m), active addresses (~570,000), and TVL ($609m), while also being selected as one of 11 finalists for Wyoming’s stablecoin (WYST). On the institutional front, PENGU and SEI saw ETF filings from CBOE and Canary, respectively. Euler Finance set a new TVL record, with $2.3b in supplied assets and $1.1b in outstanding borrows, demonstrating strong confidence in the protocol’s updated risk framework.

Our Take: Capital allocation patterns reveal a decisive shift toward protocols demonstrating both operational excellence and institutional validation. SEI’s surge across multiple growth vectors, Euler’s record TVL expansion, and the CBOE/Canary ETF filings signal that the market is prioritizing proven execution over speculative narratives. As allocators grow increasingly selective, projects without tangible progress risk being left behind in favor of those delivering measurable results.

Safety Bid, Selective Risk

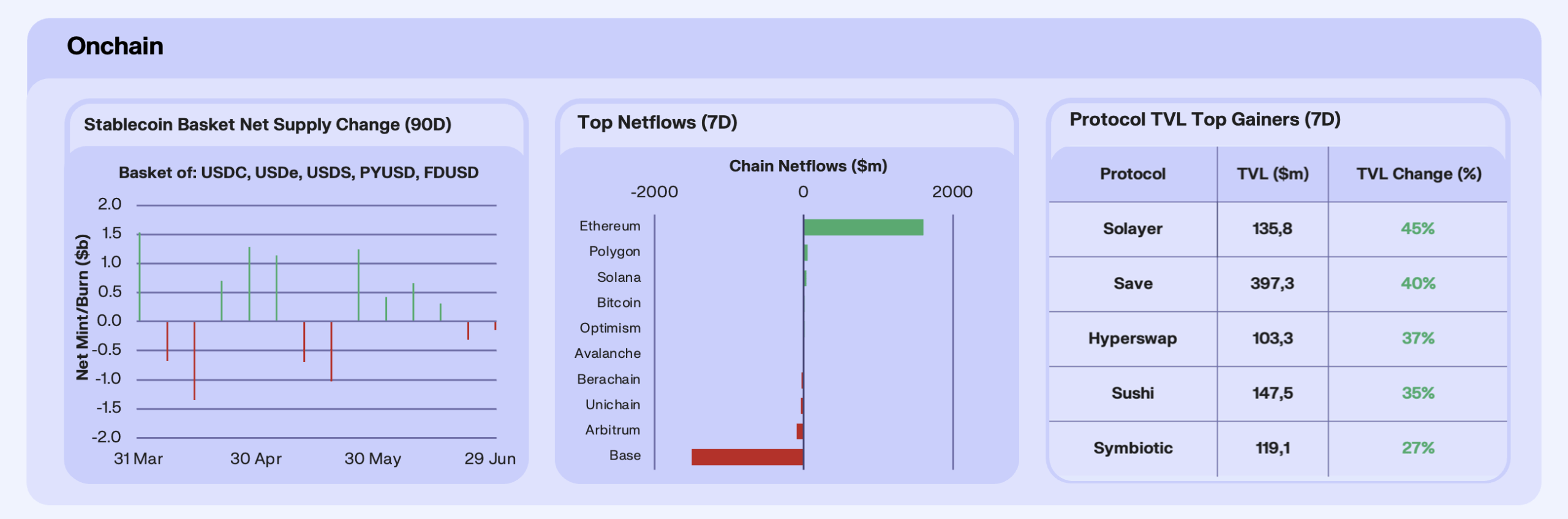

Stablecoins saw a second consecutive week of redemptions for the first time since early May, with a $148m net burn led by USDe (-$297m) and USDS (-$147m). USDC (+$366m) was the only major stablecoin to see positive net issuance amid confidence following GENIUS Act clarity. Declines in FDUSD and PYUSD reflect growing investor caution towards smaller stablecoins as the GENIUS Act enforces stricter reserve and licensing rules. USDC’s market share among tracked stablecoins (excl. USDT) rose from 78.8% to 79.2% in June, signalling a flight to quality.

This trend of consolidation could also be seen at the chain level, in which we saw a second week of extreme netflows from Base (-$1.5b) to Ethereum (+$1.6b). While this is generally considered to represent a flight to safety amid rising geopolitical jitters, diving deeper shows us exactly which protocols are suffering. Aerodrome DEX volumes are down ~47% since mid-May, representing weak demand for Base’s speculative venues, once buzzing with memecoin and high-yield DeFi opportunities. Aerodrome TVL is also down ~38%, again reflecting a drop in demand for high-risk strategies.

Outside of the EVM ecosystem, where capital flows have remained driven by cautious sentiment, flows appear to be rotating into protocols offering risk and upside potential. This contrasts sharply with the EVM user base, which appears to be adopting a more conservative approach in these uncertain times. Non-EVM chains like SVM and HypeEVM are seeing their communities pivot into (re)staking with Solayer and Symbiotic, and memecoin-driven venues such as HyperSwap.These shifts indicate investors are selectively deploying capital into platforms offering credible security and strong integrations, favouring yield with manageable risk over speculative bets.

Our Take: As exchanges like Binance prioritise compliant issuers and DeFi yields soften, capital is consolidating around battle-tested, regulated stablecoins like USDC. The Base-to-Ethereum flight underscores a broader risk-off move, but the yield chase in non-EVM chains like SVM hints at untapped potential. Watch Solayer and Symbiotic for breakout growth if security holds. We predict a bifurcated market by year-end: a dominant EVM core versus a resilient non-EVM fringe chasing higher returns.

A Spectrum of Leverage

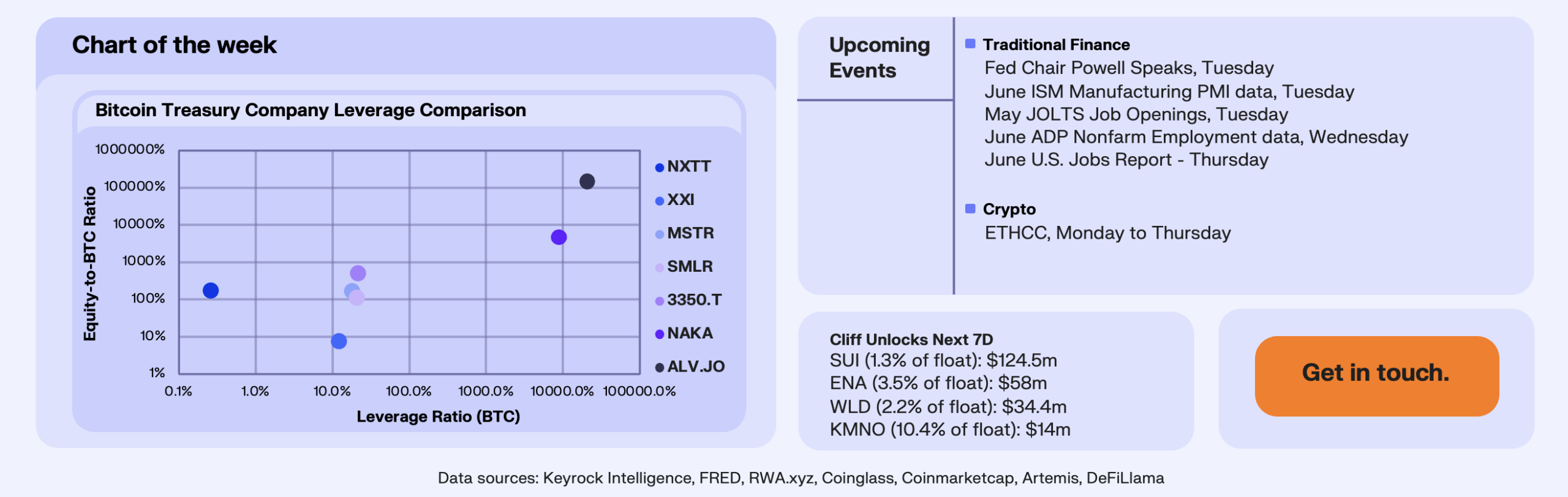

One of the more interesting charts we’re tracking in DeFi today is that of Maple Finance’s AUM, which has exploded in recent months, crossing the $2b mark at the start of the month and subsequently pushing to ~$2.36b on the 19th June. The standout contributor to this AUM gain has been Syrup USDC, a retail-friendly lending product that’s rapidly become the protocol’s growth engine. Syrup USDC now ranks as the third-largest yield-bearing stablecoin behind Ethena’s sUSDe and Sky’s sUSDS, yielding at 6.4% at the time of writing.

However, Maple’s material growth in AUM reflects only a drop in the ocean relative to the onchain Private Credit market in general, falling short of the leaders from a market share perspective at only 5.5% relative to Figure and Tradable at 75.0% and 14.5% respectively. The former focuses on Home Equity Lines of Credit, and the latter on tokenised strategies.

Our Take: Maple’s recent growth demonstrates product-market fit for institutional grade DeFi products in a yield hungry market. As the credibility of onchain yield providers strengthens, we forecast this is an area that will see material growth, particularly with improving regulatory clarity. To stay competitive, Maple will need to continue strengthening its distribution channels and underwriting transparency or risk being outpaced by more reputable or capital-efficient allocators.

Join our Telegram Channel to get it delivered directly to your phone.

Follow our Telegram Channel

Get the edge before markets move. Join our Telegram channel to receive our market update straight in your inbox.