7 July 2025

Key Insights, Shares without Borders

Big Bill, Small Vol

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

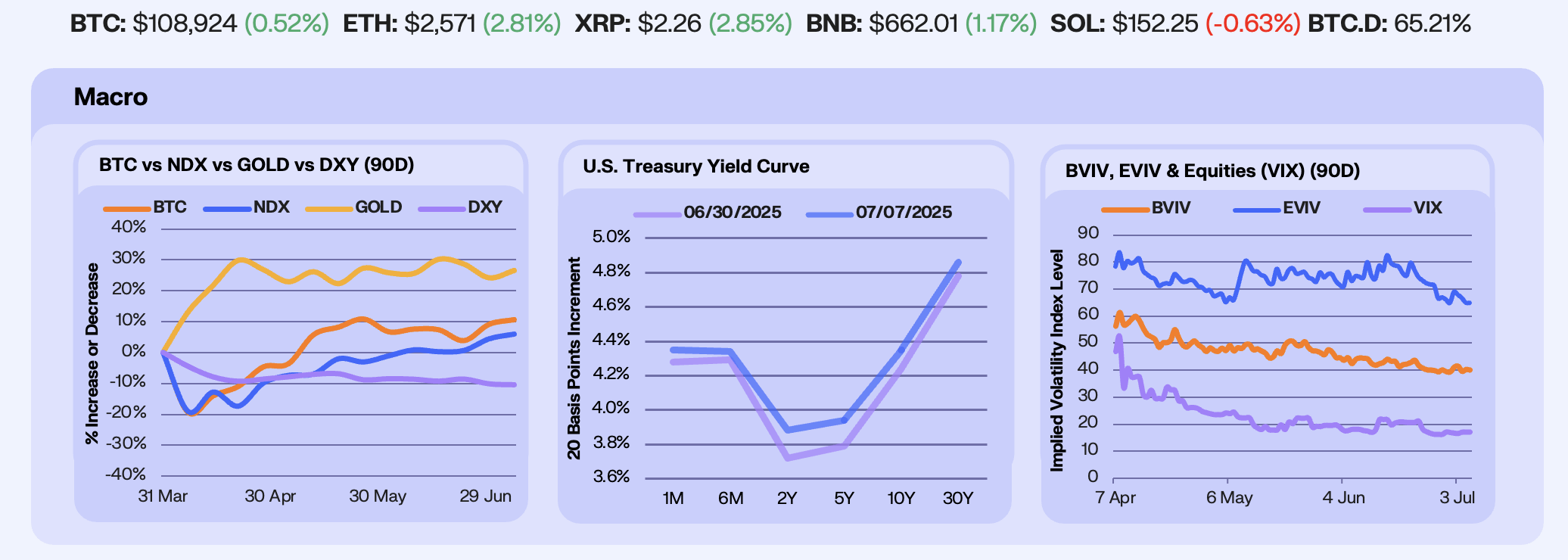

Markets digested mixed signals last week as Trump’s ‘Big Beautiful Bill’ passed final approval, raising the U.S. debt ceiling by $5 trillion and prompting Elon Musk to file a statement of organisation for the ‘America Party’. The USD extended its decline (-0.3%), bringing first-half losses to -10.4%—its worst H1 performance in 52 years. Meanwhile, the U.S. Treasury yield curve saw a bear steepening, with the belly and long end rising sharply as robust economic data from the June jobs report (+147k) and expectations of sustained fiscal expansion reduced urgency for aggressive Fed cuts. Consequently, Polymarket odds for no July Fed cuts jumped from 74% to 94%. This sends a clear signal: markets are repricing growth, inflation, and the policy path upward. The sharpest moves in the 2Y to 10Y segment reflect a hawkish reassessment of the Fed’s path, while the rise in long-end yields points to rising term premia and growing concerns around fiscal sustainability.

This macro repricing echoed across risk and inflation-hedge assets as Bitcoin (+1.4%), Gold (+1.9%), and the Nasdaq (+1.5%) gained. Despite the brief volatility spike mid-week, the fade in implied vols by Friday suggests the market remains unconvinced of a sustained breakout. Traders appear reluctant to chase upside aggressively, with continued call overwriting capping near-term IV and long-dated vols staying historically low.

Our Take: The divergence between expansionary fiscal policy and the Fed’s hawkish pivot creates a classic policy tension that historically resolves in favor of fiscal dominance, supporting risk assets over time. However, current positioning remains tactically driven rather than directionally committed. Until Bitcoin decisively clears and holds above $110K, the market seems more comfortable expressing exposure through short vol and premium-selling strategies than outright bullish momentum.

Institutional Momentum

Double clicking on crypto markets, robust institutional demand is the theme of the week. BTC ETFs recorded over $750 million in inflows for a fourth consecutive week, while Strategy, a reliable proxy for institutional BTC demand, posted a second consecutive green week. Ethereum saw a staggering eighth consecutive week of ETF inflows, while treasury plays for the blue coin are also beginning to heat up. This comes as Bit Digital raised ~$163 million to expand its ETH treasury. This institutional demand extended to SOL with the launch of the SOL staking ETF this week. Issued by REX Shares and Osprey Funds, the ETF recorded ~$33 million in trading volume and $12 million in inflows on its first day, a solid start that outperformed recent altcoin futures ETF launches.

In the derivatives markets, Bitcoin and Ethereum continue to see steady growth in OI, up 3.5% and 6.0% WoW respectively, reflecting a gradual re-risking among traders. Funding rates for both assets have normalised at an annualised equivalent of ~2%, indicating balanced positioning with no signs of overleveraged longs. The basis in Bitcoin futures, or the premium over spot prices, remains below the 5% threshold that typically signals strong bullish conviction. In the options market, Deribit data shows a 63% call/put volume ratio and a notional OI of $15.8 billion, with traders favoring $120,000 strike calls expiring in July, hinting at upside optimism. This funding rate environment, combined with rising OI and selective options positioning, points to a market that is structurally bullish yet tempered by caution.

Altcoins posted a modest gain this week, up 1.69%, with majors remaining in the diving seat despite select assets posting significant gains. Amongst the top gainers was PENGU, up 77.8% MoM, extending its rally amid sustained ETF tailwinds. Celestia also surged 14.1% WoW, helping drive a 14.5% gain for the broader Data Availability sector. This came as investors responded positively to the Lotus upgrade on Mocha testnet. The upgrade included Hyperlane-powered interoperability for new rollups and a 33% cut in TIA inflation, easing sell pressure and increasing investor appeal. Jupiter bounced back as Solana activity surged and fundamentals remained strong. Jupiter’s Perp product alone has generated ~$470m in fees since its launch ~5 months ago.

Our Take: Institutional capital continues to drive crypto markets, and this trend will sustain while the market remains cautious. If ETF inflows sustain and funding rates remain neutral, we expect BTC to lead a renewed leg higher towards $120k, though altcoins have the potential to be highly reflexive should bullish sentiment accelerate.

Quality Flows

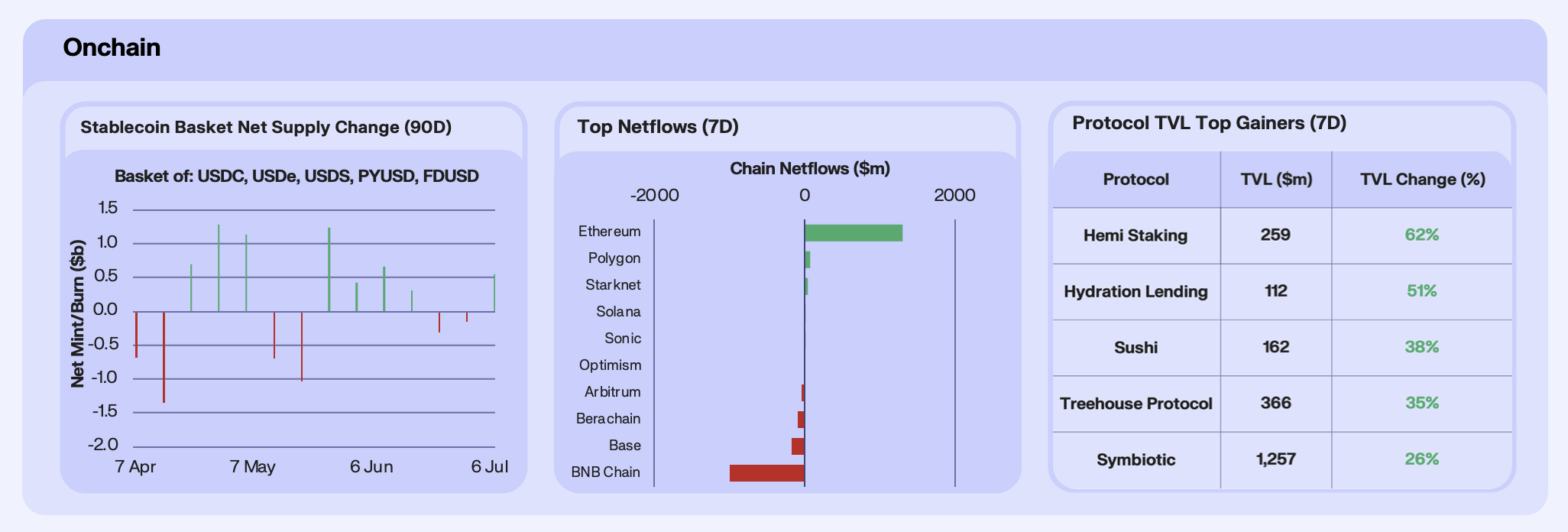

Stablecoin flows turned positive again last week, posting a net mint of ~$722 million (+0.97%), led by USDC (+$484m) and USDS (+$334m). USDC itself continues to rise in market share, reflecting sustained flight to quality as market participants react to the GENIUS Act’s regulatory shift. We expect this to continue over the coming months.

Meanwhile, capital consolidated further to Ethereum, which recorded an additional $1.8b in inflows for the week. This brings mainnet inflows to $7.2b over the past three months, with the majority of flows being derived from its Base L2. Interestingly, BNB topped the charts for outflows this week, at ~$1b. ~99% of this capital outflow ended up on Ethereum, as the DeFi leader by TVL continues to accumulate capital.

On the protocol side, one of the largest gainers for the week was Sushi, driven by its mainnet launch on Katana, the DeFi-optimized blockchain incubated by GSR. The liquidity influx was driven by incentive programs on the chain, with some pools offering dual incentives in both $SUSHI and $KAT tokens.

Our Take: The return to net stablecoin mints, led by USDC, signals renewed demand for high-quality collateral, with the GENIUS Act acting as a structural tailwind for regulated dollar assets. We expect USDC’s dominance to rise steadily as institutional flows scale. Until the market shifts to structurally altcoin driven, we anticipate capital flows will continue to be driven by incentives as opposed to sustainable narrative.

Capital Markets, Onchain

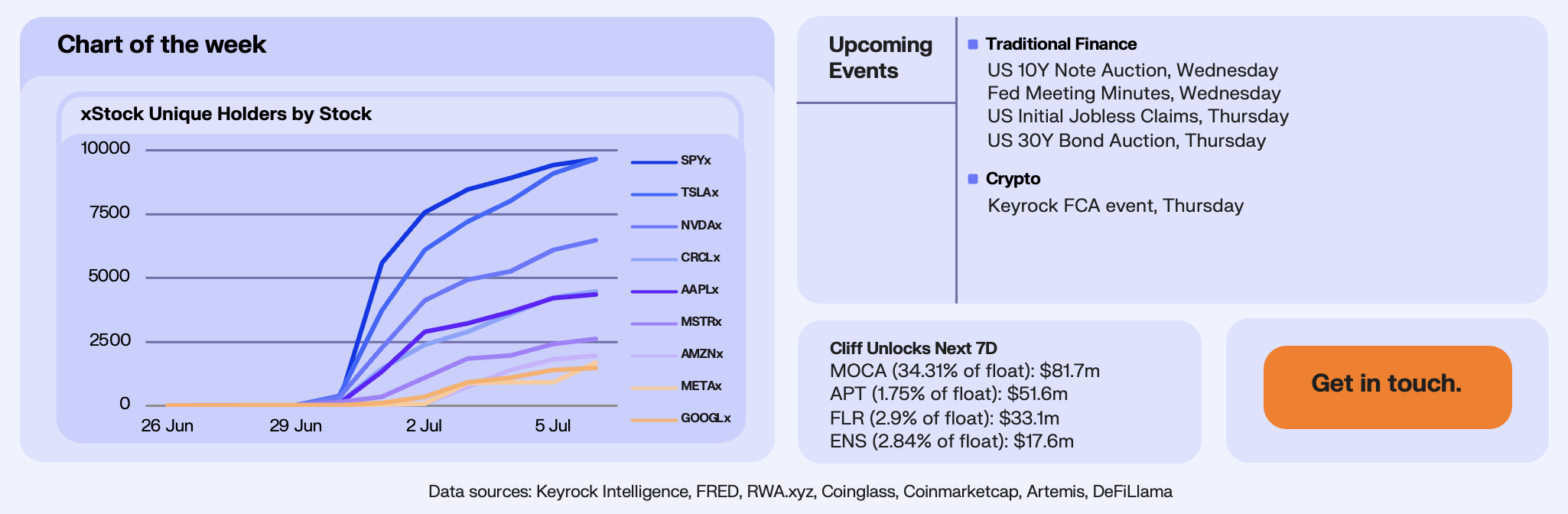

Last week, the lines between TradFi and crypto blurred even further. On Monday, Backed launched tokenized stocks (xStocks) on Solana and major centralized exchanges like Bybit and Kraken, with plans to expand to over 55 stocks and ETFs and eventually enable them to be used as collateral on Kamino. Meanwhile, Robinhood announced it will bring tokenized stocks to EU users via Arbitrum, alongside plans to roll out crypto staking in the U.S. and enable private stock trading. Centrifuge also brought the S&P 500 Index onchain.

Tokenized stocks in their current form are issued through a special purpose vehicle (SPV) that holds the real underlying shares. Users complete KYC to mint or redeem tokens at real-time cash values (xStocks uses Kraken for this), but after-hours or weekend trading requires market makers to take on price risk until redemption windows open. While these tokens don’t provide direct ownership rights or dividends, which are reinvested without rebasing the token, they offer instant settlement, and eliminate T+2 delays and counterparty risk, while enabling atomic onchain transfers. This innovation allows for global access and transforms stocks into programmable building blocks for DeFi strategies, yield generation, and derivatives.

”Tokenized stocks represent a risk mitigating opportunity for TradFi players who have long battled gap risk inherent in markets which close.” — Bradley Howell, Head of Trading at Keyrock

Tokenized stocks now have $425m in TVL with Backed issued stocks comprising $71m of the TVL. xStocks have ~21,200 unique holders, with SPYx (9,655), TSLAx (9,649), and NVDAx (6,479) seeing the highest unique holder counts. In just a week, xStocks have done $83.3m in transactional volume, with $23m of it on DEXs. July 2nd marked the highest DEX daily volume at $8.6m.

Our Take: In the near term, tokenized stocks will expand access to U.S. stocks for users in underserved markets, allow for fractional purchases, and programmatic use in DeFi. While early models of tokenized equities may serve niche needs, true disruption will come when primary issuance and traditional market infrastructure fully migrate onchain. The shift of capital markets onto onchain infrastructure is now visibly underway.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.