23 June 2025

Key Insights, Hedging In Plain Sight

Volatility on Standby

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

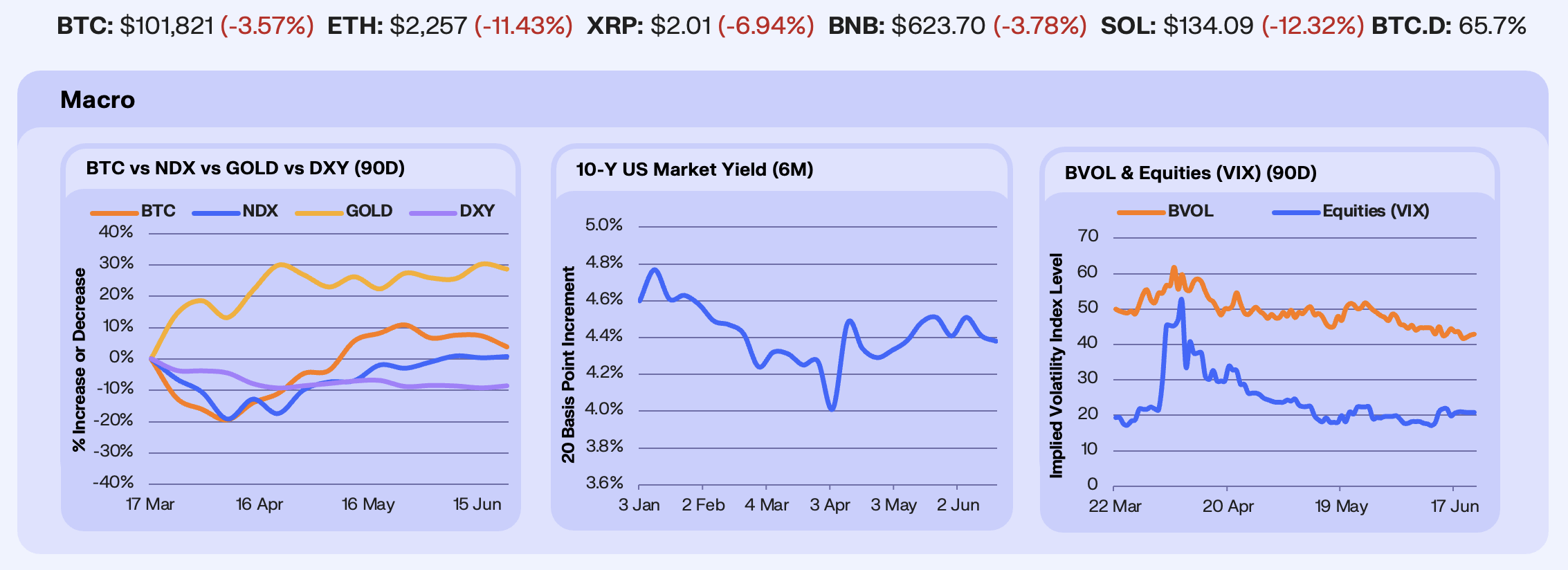

Last week’s Israel-Iran conflict heightened global economic uncertainty, threatening sustained energy price surges that could drive inflation higher alongside existing tariff pressures. Despite Middle East tensions, Bitcoin (-3.3%) continues to avoid full panic mode, buoyed by institutional accumulation with $1.02b in net Bitcoin ETF inflows last week. Meanwhile, Gold (-1.2%) hovered close to all-time highs, while investors sought safety in the U.S. Dollar (0.7%) and the U.S. 10-Year Treasury, as evidenced by a (-0.7%) drop in yields.

However, volatility metrics told a different story. Bitcoin implied volatility sits near 40 and is declining across the curve, reflecting seasonal slowdowns, while the VIX hovers around 20. Both levels are historically low given the geopolitical backdrop and looming tariff deadlines in July (Europe) and August (China). Markets may be underpricing risk, as surprises that blindside investors typically trigger the sharpest volatility spikes when participants rush to buy protection.

Our Take: Bitcoin and Gold’s modest retreat from all-time highs suggests markets are reassessing geopolitical and tariff risks that could reignite inflation through higher energy and consumer prices, explaining Fed Chair Powell’s rate-cutting hesitancy. However, downward price pressure remains limited for both assets as investors maintain inflation hedges. Meanwhile, implied volatility has limited downside but meaningful upside potential amid mounting uncertainty.

Signals of Stress

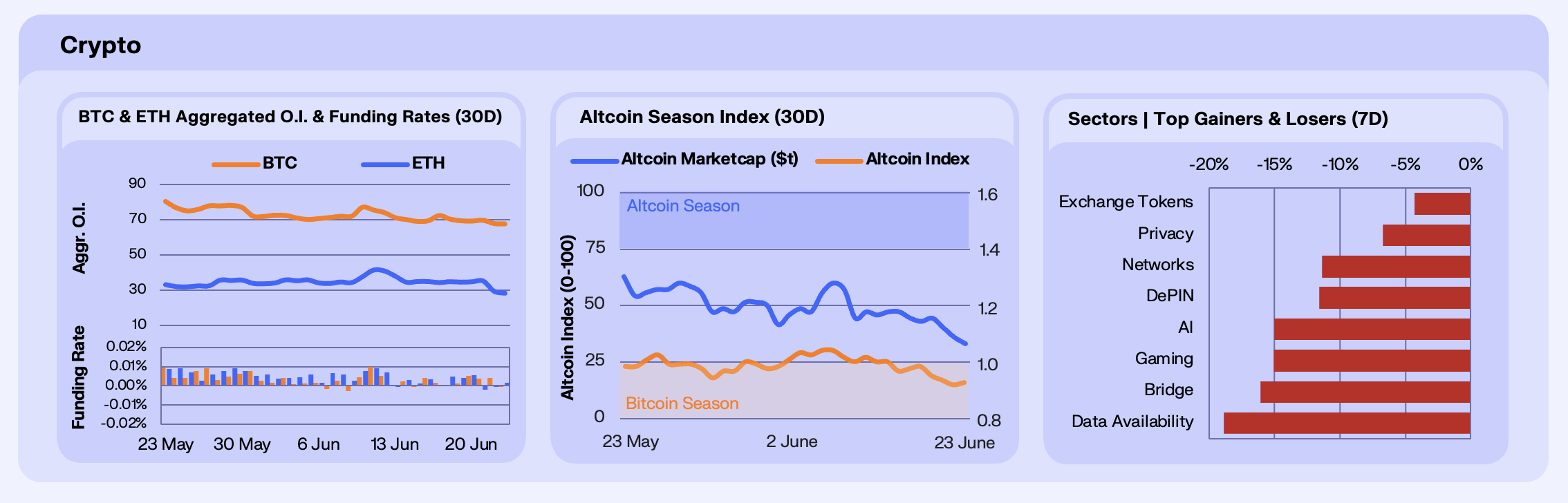

Geopolitical uncertainty drove crypto markets down -8.4% this week, reflecting continued weak appetite for risk assets. All sectors saw losses as Bitcoin dominance hit a yearly high of 66%. While short-term downside wicks in Bitcoin dominance reflect brief strength in altcoins, the broader BTCDOM trend remains firmly upward. Notably, a divergence emerged between altcoins and crypto equities, which have historically traded in tandem, as COIN (24.5%) and CRCL (62.9%) surged following the U.S. Senate’s passage of the GENIUS Act.

This underlying weakness is evident in derivatives markets as open interest retreated across both Bitcoin and Ethereum, reflecting position trimming. BTC OI has dropped 15.6% from its late-May peak of $80.16b to $67.6b, while Ethereum OI fell 32% from $41.4b to $28.2b over the past two weeks. The simultaneous decline in both assets’ open interest and shift into negative funding suggests a cooling of bullish positioning, a tilt toward downside hedging, and a market that is turning more defensive.

Our Take: With a sharp price decline across altcoins, the drop in Ether funding rates, and hedge funds holding record short positions on CME Ether futures (-$1.55b), the market continues to hedge against downside risk in crypto assets outside of Bitcoin. Given current sentiment, we see merit in expressing short-term downside protection on Ether and altcoins until macro conditions improve and risk appetite returns.

Flight to Quality

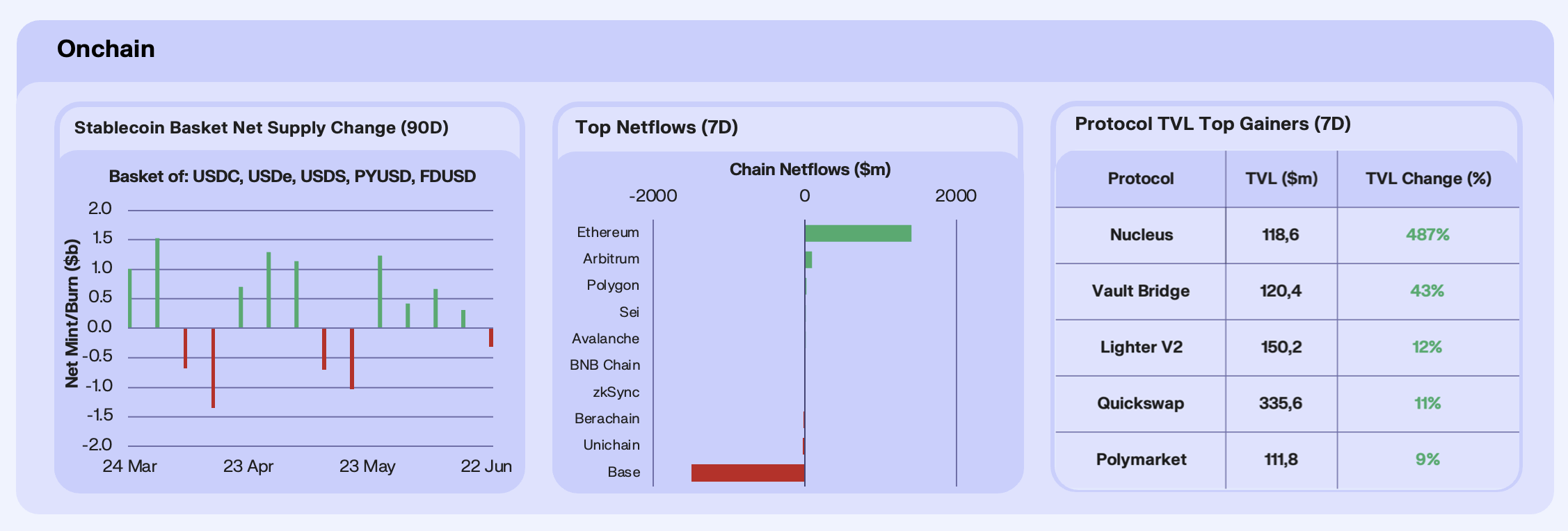

Stablecoin issuance saw its first net weekly burn in five weeks, with net redemptions totalling $307m. The decline was driven by burns in USDC (-$324m) and USDe (-$295m), as investors reacted to the passage of the GENIUS Act, a landmark U.S. bill introducing strict 1:1 reserve and AML requirements. While the bill boosted long-term confidence, evidenced by Circle’s +63% stock surge on the week, it also introduced short-term uncertainty, prompting redemptions as institutions reassessed positioning.

The most significant onchain moves this week came from a ~$1.4b net inflow into Ethereum and a ~$1.5b net outflow from Base, flows that were directly connected. This reflects a wider trend of capital consolidating back to Ethereum’s L1 as both institutional and retail users de-risked. Base, a hotspot for memecoins and high-yield DeFi activity, lost momentum as speculative interest cooled and market volatility rose following geopolitical tensions. Investors bridged capital back to Ethereum to protect capital and secure profits, gaining exposure to more stable, institutionally anchored platforms like Pendle, Ethena, and Spark; all of which saw a spike in TVL in ETH-terms.

Protocol flows showed a clear appetite for directional bets and tactical positioning. Polymarket saw a +9% TVL rise, driven by users speculating on geopolitical tension outcomes amid heightened macro uncertainty. Polymarket is increasingly becoming the go-to venue for placing targeted directional bets to either speculate on, or hedge specific events. Quickswap gained +11%, as traders repositioned around event risk to hedge or unwind exposure.

Our Take: The key theme this week onchain has been a flight to both quality and stability amid geopolitical uncertainty. Historically, these mass event-driven exodus’ have been short lived, with market participants typically overreacting to initial news. We suspect the same will be true onchain, with fundamentals improving short-term for risk-on protocols.

Maple Finds Product-Market Fit

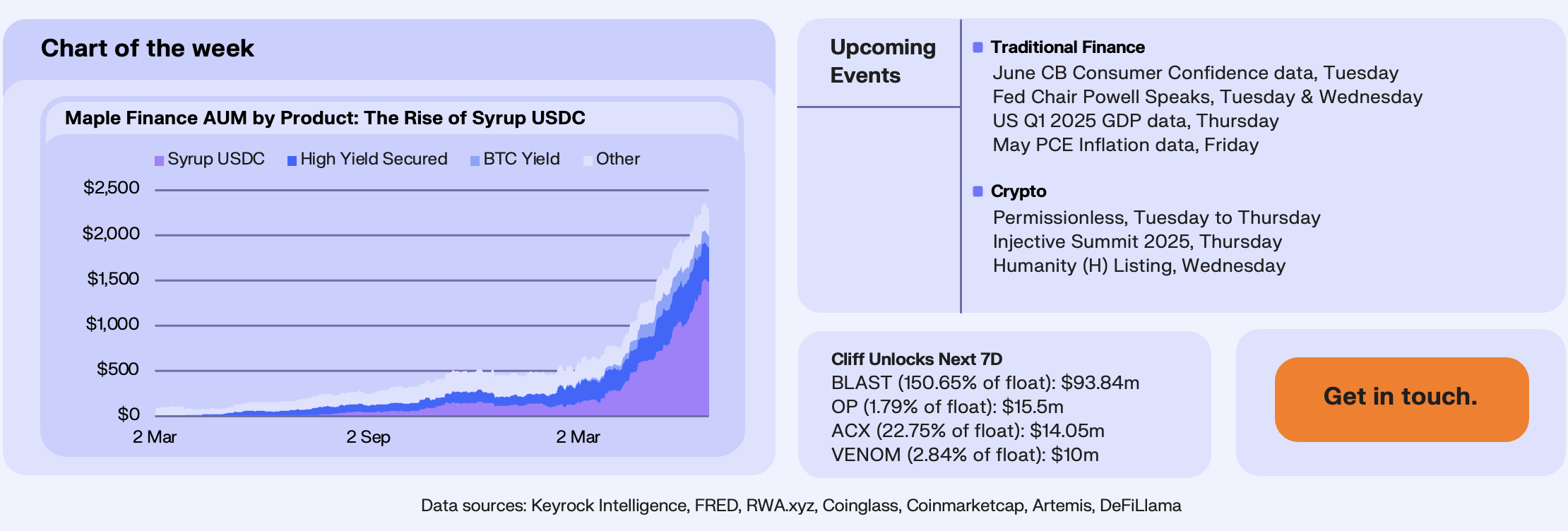

One of the more interesting charts we’re tracking in DeFi today is that of Maple Finance’s AUM, which has exploded in recent months, crossing the $2b mark at the start of the month and subsequently pushing to ~$2.36b on the 19th June. The standout contributor to this AUM gain has been Syrup USDC, a retail-friendly lending product that’s rapidly become the protocol’s growth engine. Syrup USDC now ranks as the third-largest yield-bearing stablecoin behind Ethena’s sUSDe and Sky’s sUSDS, yielding at 6.4% at the time of writing.

However, Maple’s material growth in AUM reflects only a drop in the ocean relative to the onchain Private Credit market in general, falling short of the leaders from a market share perspective at only 5.5% relative to Figure and Tradable at 75.0% and 14.5% respectively. The former focuses on Home Equity Lines of Credit, and the latter on tokenised strategies.

Our Take: Maple’s recent growth demonstrates product-market fit for institutional grade DeFi products in a yield hungry market. As the credibility of onchain yield providers strengthens, we forecast this is an area that will see material growth, particularly with improving regulatory clarity. To stay competitive, Maple will need to continue strengthening its distribution channels and underwriting transparency or risk being outpaced by more reputable or capital-efficient allocators.

Join our Telegram Channel to get it delivered directly to your phone.

Follow our Telegram Channel

Get the edge before markets move. Join our Telegram channel to receive our market update straight in your inbox.