2nd June 2025

Key Insights, Ethereum Yield Streams

Fragile Optimism

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

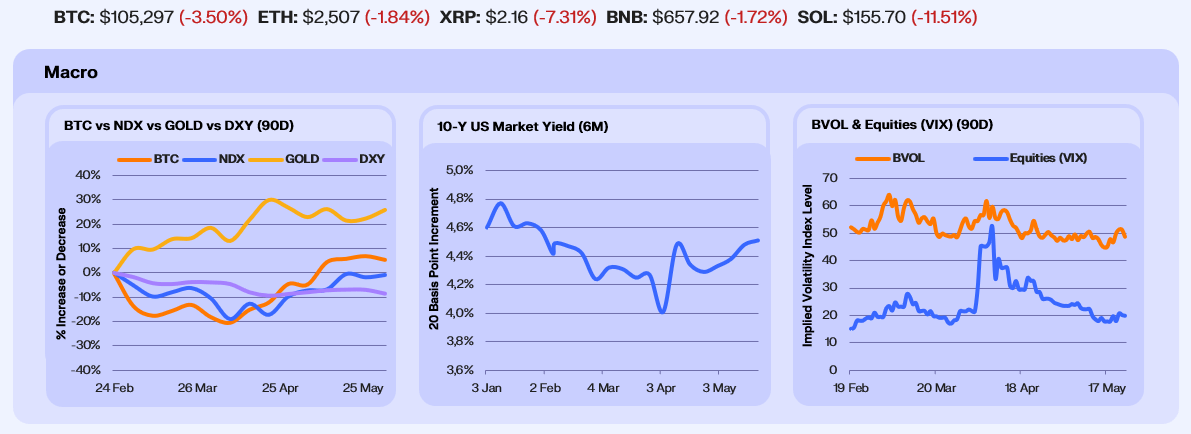

Risk assets bounced this week as markets digested a whirlwind of political and policy headlines. These headlines, including conflicting signals of tariff reversals and new export restrictions on chips and engines, injected volatility but ultimately tilted sentiment risk-on as markets clung to hopes of a near-term U.S./China trade resolution. The Nasdaq climbed ~2%, while safe-havens Gold and Bitcoin pulled back –1.2% and –3.8% respectively. Meanwhile, the Dollar Index rose slightly, and the 10Y Treasury yield dipped 9bps for the week to 4.42%. This reflects a shift in market expectations, particularly the path of interest rates, with Kalshi now pricing fewer than two cuts in 25’, down from four in April.

President Trump’s “Liberation Day” tariffs were blocked, then swiftly reinstated by an appeals court, while new export restrictions on chips and jet engines to China fueled fears of an accelerating tech war. These abrupt shifts drove sharp intraday moves in yields and equity futures, reinforcing the market’s hair-trigger sensitivity to policy headlines. Volatility metrics, however, suggest surface-level calm. BVOL fell from a high of 51.7 mid-week to 47.9 by Sunday, while the VIX dropped from 22.3 to 19.6 over the same period. Despite sharp policy-induced reactions, implied volatility continues to compress, masking the underlying fragility.

Yet, beneath the week’s risk-on tone, consumer sentiment painted a more fragile picture. A record 67% of Americans now expect higher unemployment, the most since 2008, while housing affordability continues to deteriorate, with median payments hitting $2,882/month. Overseas, Japan lost its title as the world’s top creditor for the first time in 34 years, just as its largest insurers posted a record $60b in unrealized bond losses, highlighting deepening strain in global sovereign debt markets. Markets may have rallied on near-term positioning and headline relief, but longer-term economic fragilities remain firmly in view.

Our Take: Markets aren’t calming down, they’re holding their breath. With inflation stickiness, global debt strain, and political uncertainty all unresolved, fragility continues to define the macro backdrop.

Majors Hold, Alts Fade

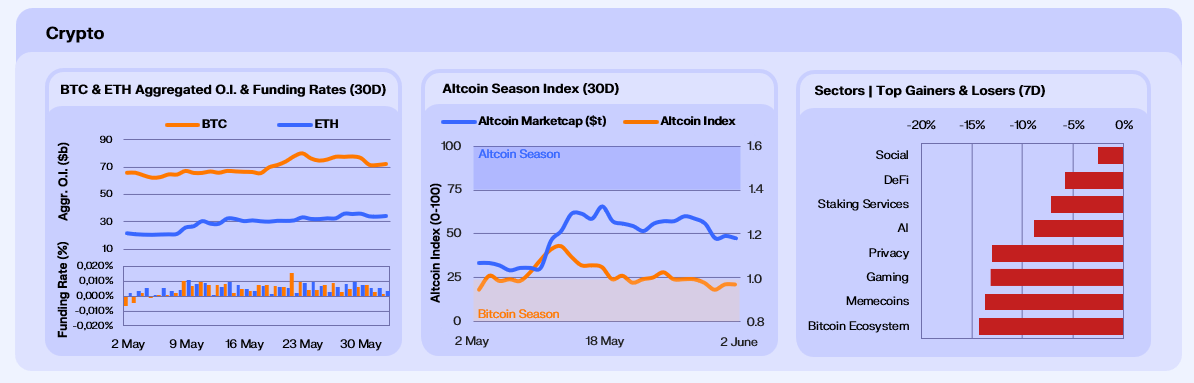

Crypto pulled back this week, with total market cap down 4.27%, led by a 3.8% drop in Bitcoin. Ether outperformed, falling by only 2.3%, with broader risk appetite clearly softening. Despite the price action, positioning in majors remained constructive. Bitcoin open interest held firm at $72.4b, while Ether open interest surged 5.2% to a new record high of $32.3b, having touched a new record high of $35.7b during the week, suggesting growing speculative interest in ETH exposure. Funding rates across both remained stable and moderate, indicating healthy leverage levels. ETH sentiment was further supported by regulatory clarity, as the SEC confirmed that staking would not be treated as a securities issue for spot Ethereum ETFs, removing a major hurdle to their approval.

The Altseason Index dropped from 28 to 21, and the total altcoin market cap declined by roughly $30b from recent highs. While capital remains sticky in majors, the retreat in altcoins points to waning momentum and selective risk-taking. Doubling clicking at the sector level, we can see where altcoins were hit the hardest. Memecoins (-13.7%), Bitcoin ecosystem tokens (-14.3%), and gaming (-31.1%) led declines. The sector-wide drop reinforces the view that last month’s rally was driven more by rotation and hype than broad-based conviction.

Meanwhile, crypto treasury companies are entering a new phase. MicroStrategy, down –3.16% on the week, continues to lead the Bitcoin treasury narrative, but a new wave of holding companies is emerging across ETH and SOL, with growing talk of similar structures for smaller cap assets. While the financial engineering behind these structures is generating short-term alpha, market participants are beginning to question their sustainability, particularly as future differentiation may rely on increased leverage.

Our Take: Ether’s open interest surge reflects growing trader interest in high-beta majors, and BTC positioning remains stable. But the broader market lacks leadership, and altcoins appear stuck in a reset phase. With treasury companies likely to proliferate across the long tail of tokens, investors should watch for signs of initial buy pressure, but longer term for unsustainable leverage and retail froth as this trend matures.

Yield-Driven Rotation

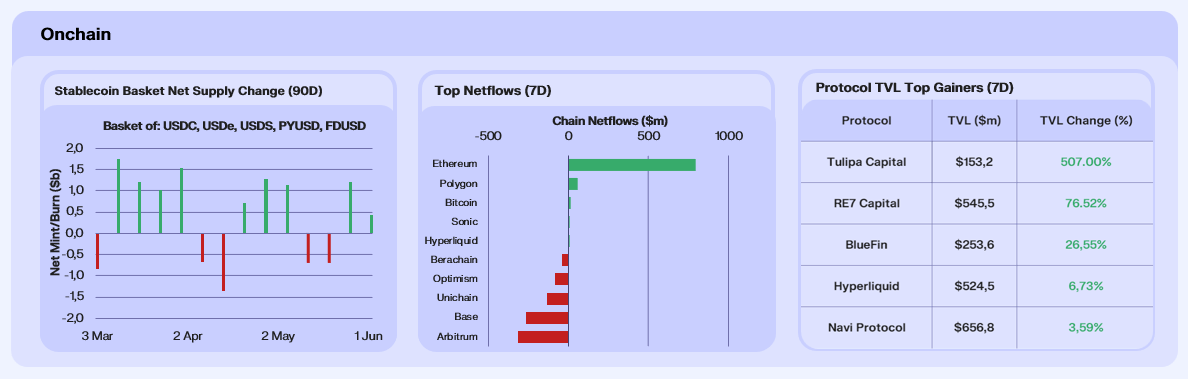

Stablecoin supply was mixed this week, with one notable standout; USDS jumped 10.36%, ~$712m, driven by new DeFi integrations with Pendle and Spark that unlocked high-yield opportunities and borrowing incentives. In contrast, USDC dipped slightly, likely due to capital rotation into higher-yield alternatives. USDe added 3.66%, while ecosystem-tied stablecoins like FDUSD and PYUSD remained flat, reflecting localised redemptions and weaker demand outside of DeFi-native use cases.

At the chain level, Ethereum led net inflows, as investor interest rotated back into L1 ecosystems with deep liquidity and DeFi infrastructure. Bitcoin also saw net inflows, albeit more modest, amid heightened BTCFi interest, which we’ve highlighted over the past month. Arbitrum was the major outlier, posting the sharpest outflows of the week. While onchain chatter continued to highlight inflows related to Hyperliquid’s growth, our data shows large withdrawals from Arbitrum itself, likely linked to the unwind of major Hyperliquid trades by trader James Wynn, as funds exited Hyperliquid and subsequently bridged out of Arbitrum. Hyperliquid itself posted continued net inflows, reinforcing its role as a destination for derivatives capital, while Arbitrum acted more as a throughput layer.

On the protocol side, TVL gains are concentrated around yield strategies. We’ve highlighted specific yield strategy providers; Tulipa Capital and RE7 Labs, who grew materially this week, the majority. We also saw growth in the Sui ecosystem, with BlueFin up +25.55%, spurred by boosted LP rewards of up to 580% APR and integrations with protocols like Kai Finance. Hyperliquid rose a further ~7% as perp trading and EVM ecosystem growth fueled persistent capital inflows.

Our Take: Flows are increasingly shaped by tactical yield-seeking and ecosystem-specific catalysts. With the altseason index still subdued, the near-term outlook for altcoins remains tepid. Until sentiment turns, we expect capital to keep moving fast , chasing narrative and yield over conviction.

Stablecoin Revenue Paradox

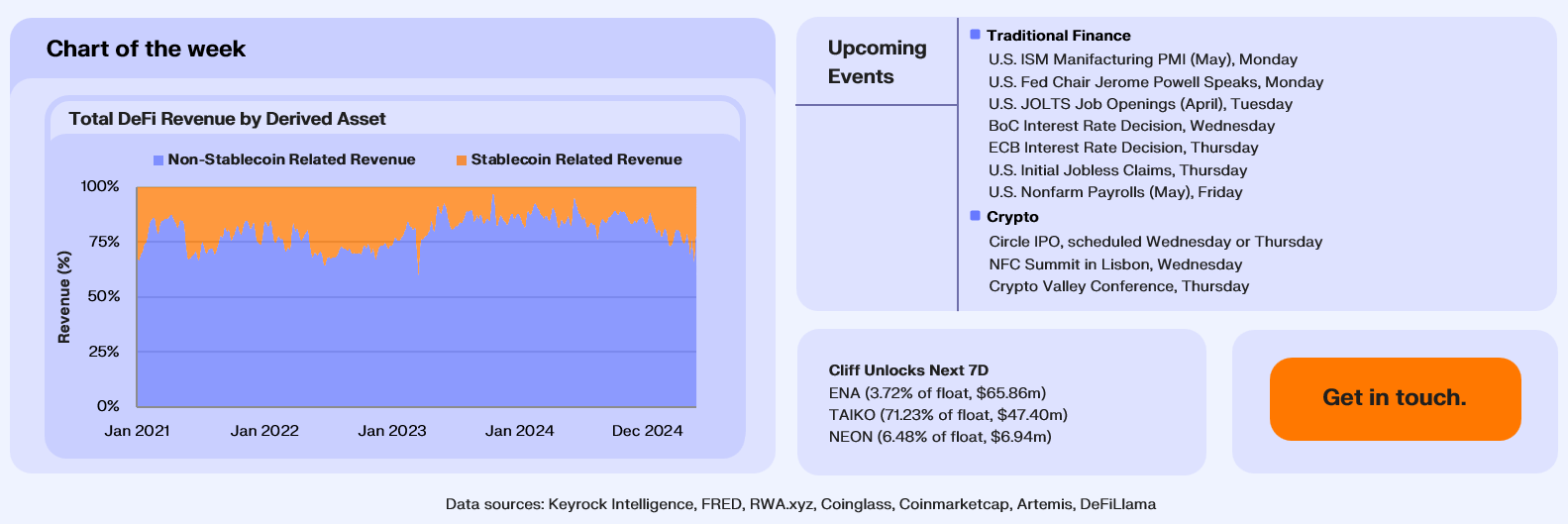

Our analysts have been diving deep into onchain DeFi protocol and stablecoin data, specifically exploring the percentage of protocol revenue that’s derived from stablecoin activity, and how this trends over time.

The latest shift in the percentage of DeFi protocol revenue, split across DEXes and lending, that stablecoins generate has been particularly noticeable. After compressing to just ~4.7% in June 2024, stablecoin-linked revenue has rebounded sharply, reaching a year-to-date high of ~30.8%. That’s a more than 7x increase in just a few months, a sign that stablecoins are once again central to how value circulates onchain.

What’s driving the resurgence? A combination of factors: rising onchain stablecoin supply, elevated yield opportunities in protocols like Pendle and Morpho, and declining altcoin conviction. In this environment, capital isn’t fleeing into safety — it’s tactically deploying through stables to extract yield while remaining nimble. Stablecoins are enabling users to loop leverage, farm incentives, and trade volatility with minimal directional exposure. We will be releasing a report touching on our analysis of stablecoin contribution to protocol revenue this coming week.

Our Take: The rebound in stablecoin linked revenue is a signal of how capital is adapting. With altcoin momentum faltering and risk appetite fragmenting, investors are rotating through stablecoins rather than exiting the ecosystem altogether. This points to a DeFi landscape defined not by fear, but by strategy: users staying active, looping capital, and targeting yield with precision. If this behavior persists, stablecoins won’t just be a liquidity layer, they’ll be the engine driving the next phase of DeFi growth.

Join our Telegram Channel to get it delivered directly to your phone.

Follow our Telegram Channel

Get the edge before markets move. Join our Telegram channel to receive our market update straight in your inbox.