18 August 2025

Key Insights: CPI Lift, PPI Drag

Inflation Crosscurrents

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

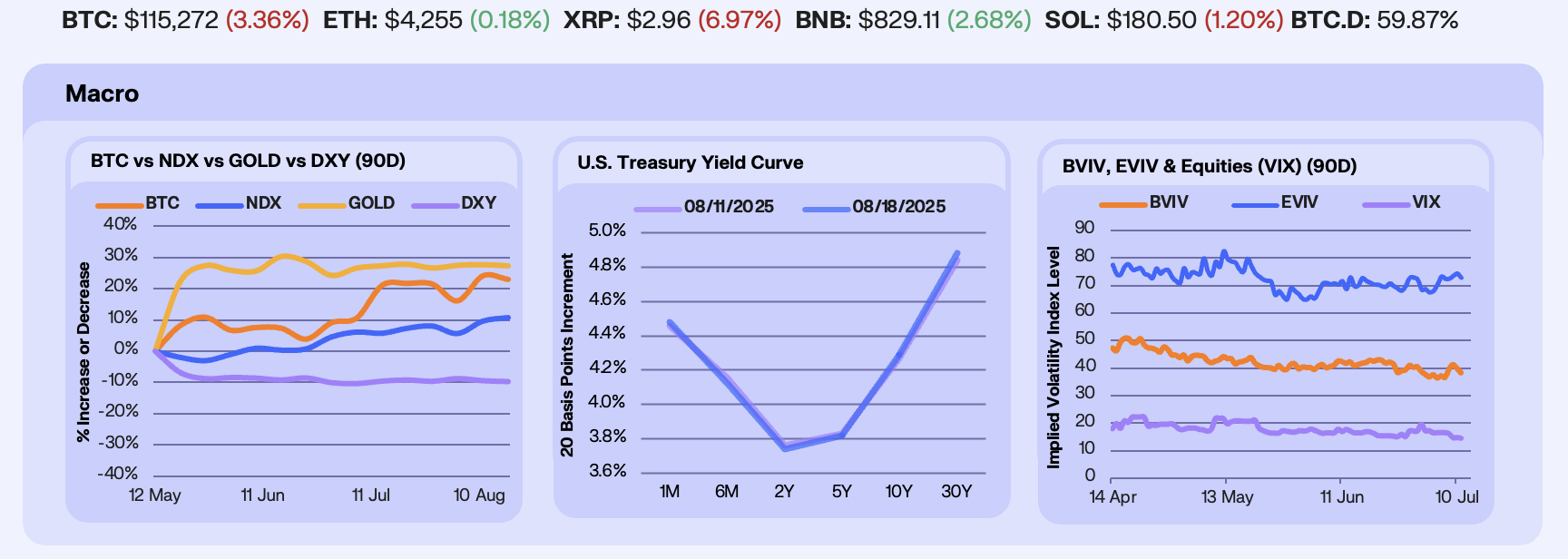

Markets swung on inflation data last week, with a soft CPI print lifting sentiment before the hottest PPI reading since March 2022 reversed gains. Bitcoin (-5.4%) and the Nasdaq (+0.4%) hit fresh all-time highs before retreating, while Gold (-0.4%) and the Dollar (-0.2%) held in a three-month range as traders await the next wave of central bank easing. Despite the Nasdaq’s new peak, breadth remains narrow, with only half of NDX constituents trading above their 50-day moving average.

Treasury yields fell after a soft CPI print but retraced higher on a hotter PPI reading. Markets now price a 72% chance of a 25 bps cut in September, with odds of a 50 bps move collapsing more than 50% to just 3.3%. While a weaker labor market gives the Fed room to ease, the PPI surprise tempers the case for aggressive cuts. A 25 bps move allows policymakers to acknowledge inflation and softer growth without risking a perception of overreacting to near-term data, especially with core inflation not yet decisively anchored.

Implied volatility was mixed over the week. Bitcoin’s IV fell from 38.9 to 37.7 (-3.1%), while Ethereum’s edged higher from 72.1 to 74.3 (+3.1%). The VIX extended its slide from 15.81 to 14.43 (-8.7%), reaching one of the lowest levels in the past five years. The subdued backdrop supports the view of a patient market awaiting the next catalyst, with attention on upcoming macro events and mindful that surprise headlines could quickly shift sentiment.

Our Take: Heavy institutional flows and the likelihood of a September rate cut point to the start of central bank easing, a backdrop that has historically fueled Bitcoin’s strongest rallies. Liquidity tailwinds, coupled with risk on sentiment creeping back into equities, create fertile ground for another leg higher. Within this context, Bitcoin’s $140,000 strike has emerged as a clear upside target, carrying the largest notional value across all expirations and anchored by heavy September call positioning. With calls roughly twice the size of puts, traders remain firmly positioned for upside despite the recent pullback.

Majors Diverge

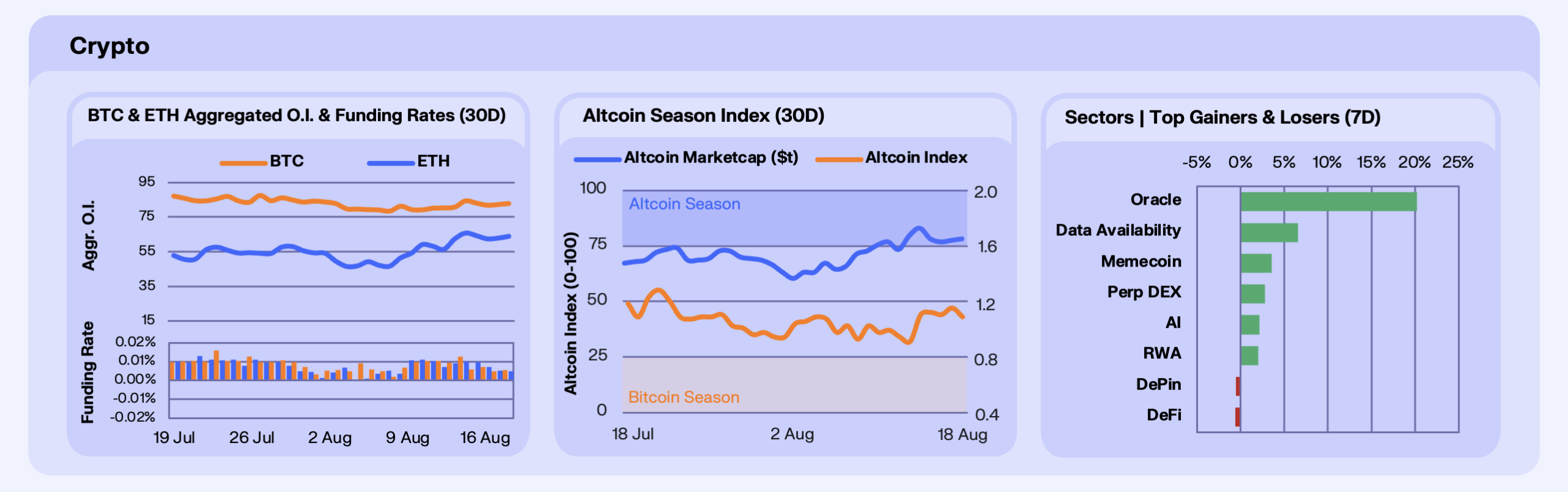

Majors posted another volatile week, with ETH seizing the spotlight as it surged to near ATHs of ~$4.8k, buoyed by $1.7b in August spot ETF inflows and the ETH/BTC pair breaking multi-year resistance. It has since retraced to end the week marginally down. BTC fell 5.4% WoW, having hit a fresh ATH of ~$124.5k mid-week before retracing to ~$115.5k as hotter US PPI data tempered rate-cut optimism. SOL held up well amid market conditions, only falling by 2% WoW on sustained ecosystem momentum in DeFi, NFTs, and DePIN. Across majors, despite price action, sentiment remained bullish, with DAT, ETF flows and network-specific tailwinds mitigating against macro jitters from inflation prints.

Derivatives positioning reflected this optimism. BTC OI rose 3.17% WoW, peaking alongside its ATH, before cooling as funding rates eased. ETH OI jumped 13.18%, its sharpest weekly rise in months, with funding holding firm as long positioning stayed bid. The divergence, BTC’s funding cooling while ETH’s remained elevated, underscores the rotation trade, with traders chasing ETH upside while BTC consolidates.

The Altseason Index climbed as Alts MCap rose 4.43% WoW, led by MNT (19.7%) and ARB (12.4%). ETH’s temporary breakout catalysed flows into mid-caps and L2 ecosystems, with BTC dominance sliding back below 60%. While the index remains well below the 75 ‘full altseason’ threshold, rotation dynamics are in motion. Capital is moving from BTC, down the risk curve to ETH and selective alts, with perp liquidity and stablecoin velocity supporting the shift.

Out Take: ETH’s breakout, albeit temporary, has cracked open the door to a sustained rotation, with BTC consolidating and alts beginning to stir. If DAT and ETF inflows persist and ETH/BTC holds its breakout, we expect capital rotation down the risk continuum with a particular focus on market breadth to accelerate into September, led by high-liquidity assets and DeFi majors, while BTC grinds higher on a slower trajectory.

Stable Squeeze

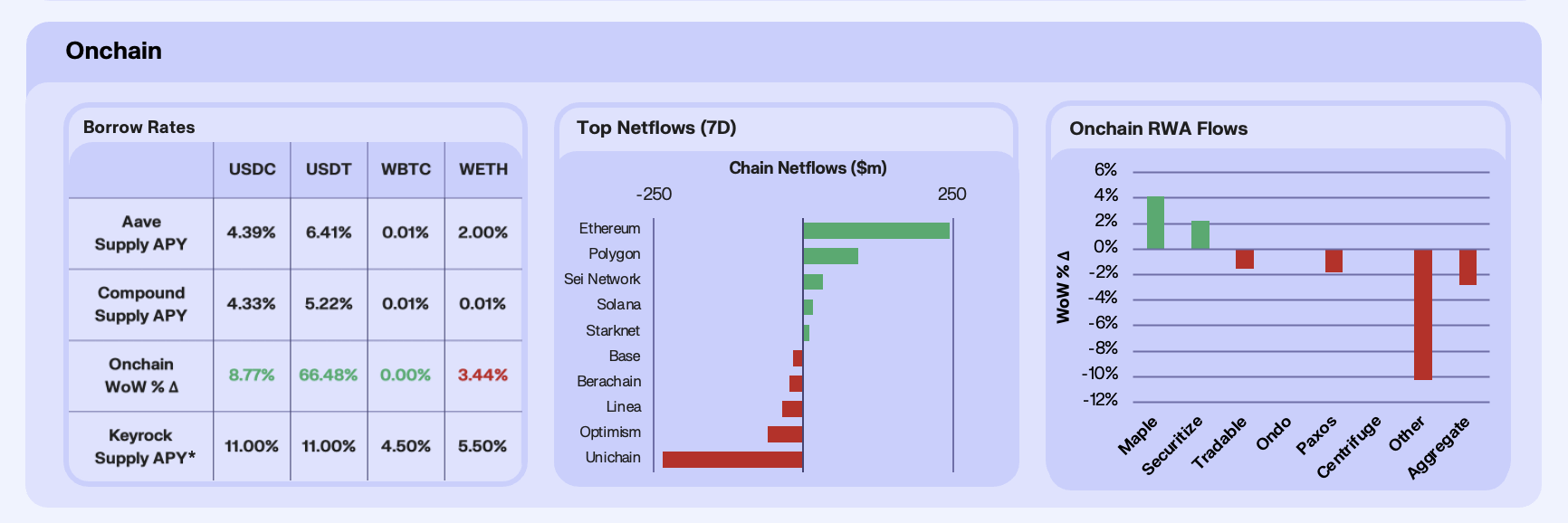

Onchain stablecoin lending rates climbed this week despite mixed supply shifts, reflecting resilient leverage demand as ETH rallied. USDC APY on Aave rose to 4.39% WoW even as supply jumped 10.1%, with borrow demand outpacing inflows amid stablecoin looping strategies. USDT saw the sharpest move, with APY spiking 66.5% WoW, as supply halved to $313m, driving utilisation higher. Marc Zeller of Aave noted that the “recent rate volatility in Aave’s USDT implementation on Ethereum Mainnet has been driven by large, recurring withdrawals from Justin Sun, which temporarily distort utilisation and rates. We’re working to mitigate these supply shocks, having adjusted the interest rate curve to enable smoother growth, while continuing efforts to scale diversified liquidity depth.” WBTC rates stayed flat at 0.01% despite a 15.6% supply increase, underscoring muted BTC leverage appetite, while WETH dipped 3.44% WoW. Overall, stable rates remain below 10%, suggesting healthy leverage conditions, but persistent supply tightness in USDT could pressure rates higher.

RWA TVL fell 2.79% WoW, sustaining above the $26b mark. Maple led with 4.16% AUM growth on strong inflows to private credit pools, while Securitize added 2.21% on steady institutional adoption. Paxos (-1.84%) and Ondo (-0.02%) saw mild pullbacks, likely tied to profit-taking and alt rotation. The growth skewed toward permissionless credit and tokenised securities, with actively managed RWA strategies seeing outsized momentum as onchain yields remain attractive relative to T-bills.

Ethereum led WoW inflows again, continuing a sustained run of capital accumulation, while Polygon and Sei also posted gains. On the other side, Unichain lost ~$180m, likely a rotation into more established L1s like ETH and SOL, while OP Mainnet bled ~$100m following Retro Funding 7 and fee switch delays. Base, -$40m, and Berachain, -$50m, also slipped, underscoring a broader L2 shakeout as capital concentrated in higher-liquidity chains.

Our Take: Lending markets are tilting toward stables, with USDT’s supply crunch a key pressure point that could trigger rate spikes if leverage demand persists. On RWAs, momentum is hitting key support, which if holds, we could see a breakout quarter. Private credit and tokenised equity strategies are gaining institutional traction, and the $26b TVL support zone suggests the next leg up could be sector-defining. If current inflow trends hold, September could bring fresh ATHs for onchain RWA liquidity.

Stablecoin Supply Projections

Last week, Circle and Stripe unveiled plans for new payments blockchains, signaling a move to capture the full stablecoin value chain, from issuance to end-user services. That push comes as stablecoins hit another all-time high in supply at $277b, underscoring their growing role in payments. Our newest report, ‘Stablecoin Payments: The Next Trillion Dollar Opportunity,’ explores this value chain in depth and the rise of stablecoins as global payment rails. Stablecoins have grown from just 0.04% of the U.S. M2 in 2020 to over 1% today. If current trajectories hold, they could comprise 10% of the U.S. money supply and handle up to 12% of all cross-border payment flows by 2030. At a $2 trillion supply, stablecoins could hold 25% of the U.S. Treasury bill market, a shift that would fundamentally reshape monetary policy.

That growth is being driven by institutional adoption across business-to-business (B2B), peer-to-peer (P2P) and card payment rails, sectors already showing rapid uptake. B2B and card-based stablecoin usage has pushed total monthly payments from under $2 billion to over $6.3 billion by February 2025, with card transactions alone surging 375% over the same period, from $231 million to nearly $1.1 billion per month. While P2P payments made up the majority of transaction volume in early 2023, they have since declined, with B2B now taking the lead.

Our Take: Stablecoins are on track to unlock $1 trillion in annual cross-border volume by 2030, but reaching that scale will require progress on four enablers: regulatory clarity, interoperability, liquidity and programmability. Regulatory clarity is shifting from barrier to tailwind, with the CLARITY and GENIUS Acts providing long-awaited certainty. Interoperability is the last mile, bridging fiat and onchain ecosystems for use. Liquidity will determine whether stablecoins stay niche or become true settlement assets, demanding depth to handle large flows without slippage. Programmability turns them into dynamic infrastructure. The faster these pillars mature, both individually and together, the sooner stablecoins will evolve from promising innovation to core global payment infrastructure.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.