26th May 2025

Key Insights, Bond Appetit

Bonds Catch Yield Fever

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

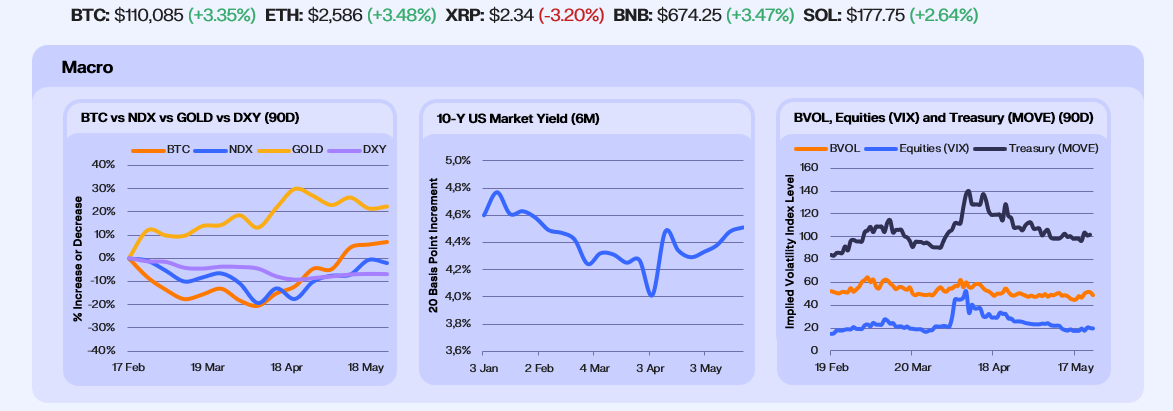

Last week, demand jumped for safe-haven assets like Bitcoin (+2.4%) and Gold (+4.1%) as bond markets priced in stronger growth, rising inflation, and a “higher for longer” rate outlook. Bitcoin hit all-time highs of $112,000, driven by $2.75b ETF inflows.

This shift in sentiment coincided with a synchronized uptick in volatility across markets after weeks of subdued activity. Bitcoin and S&P implied vols jumped midweek, while Treasury volatility remained elevated, underscoring persistent macro uncertainty and rate sensitivity.

The volatility was particularly evident in bond markets, where the 10-year Treasury yield climbed 0.6% after a weak 20-year auction, while the U.S. 5Y–30Y bond spread steepened to 1.00%, its widest since October 2021—when CPI inflation was 6.2%. Adding to global rate concerns, Japan saw 30-year yields hit record highs, a seismic shift for a country known for ultra-low rates, raising the risk of another yen carry trade unwind.

Despite these headwinds, the Nasdaq (-1.1%) and Dollar Index (-2.1%) posted declines as higher borrowing costs weighed on sentiment. More notably, equity retail demand remains resilient, with individual investors registering net selling in just six sessions since March.

Our Take: We expect the bullish long-term outlook for safe-haven assets like Bitcoin and Gold to hold, while maintaining a cautious stance on equities as markets adjust to interest rate expectations and elevated borrowing costs. Although recession risks have decreased, inflation remains a key concern. With U.S. tariffs reaching levels not seen since the 1930s and high global treasury bond yields signaling ongoing inflation worries, there’s mounting concern about U.S. debt sustainability as the government’s interest costs rise.

Majors Take the Stage

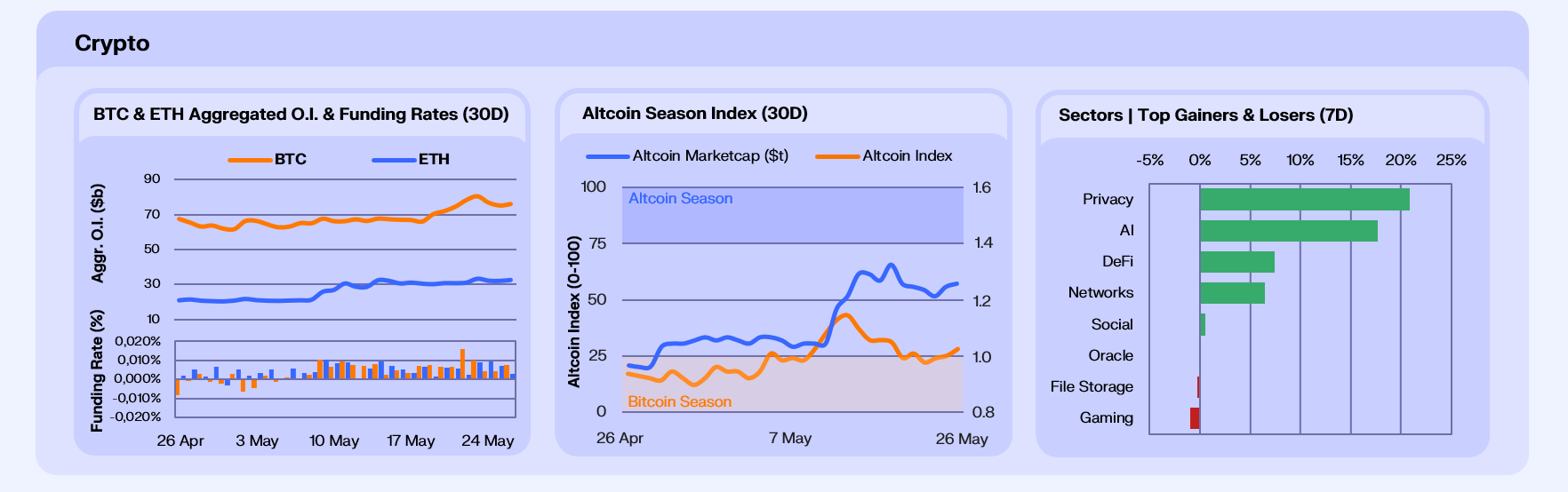

Bitcoin’s rally to new all-time highs pushed its open interest to a record $80b, while Ether’s open interest reached a new all-time high of $33b. Though funding rates rose between both assets, they remain at healthy levels, signaling modest leverage use. This bullish positioning was further confirmed in the options markets, where global open interest reached $56.5 billion, the highest since December 2024, with Bitcoin commanding 83.95% of total volume.

The rally broadened beyond Bitcoin, as Ether (+2.2%) and Altcoins (+1%) sustained their rally, both nearing three-month highs. However, the strength appears unevenly distributed: while Bitcoin attracted massive institutional flows, Ether’s advance remains retail-driven, with its ETFs posting weak $248m inflows even as Bitcoin broke out.

At the sector level, Privacy and AI assets led this week’s gains. Monero maintained its position as the top performer in crypto’s top 100 YTD (+110%), benefiting from growing demand for financial privacy tools as governments push CBDCs and stricter KYC/AML rules. Meanwhile, Worldcoin led the AI sector after the project team announced a $135m investment from a16z and Bain Capital through direct token purchases.

Our Take: We expect Ether’s momentum to continue in Q2, supported by its dominance in crypto’s fastest-expanding sectors: stablecoins (55% market share) and tokenization (59.5%). This fundamental strength is reinforced by technical factors: hedge funds have been covering short positions in CME futures since February, reducing exposure from -$1.55b to -$1.25b and setting up potential for a short squeeze.

While altcoins posted modest gains this week, we remain cautious about broader market direction. The current rally appears fragmented, with gains driven by individual token narratives rather than sector-wide momentum. We expect this narrow market breadth to persist throughout the quarter.

Breadth Before Breakout

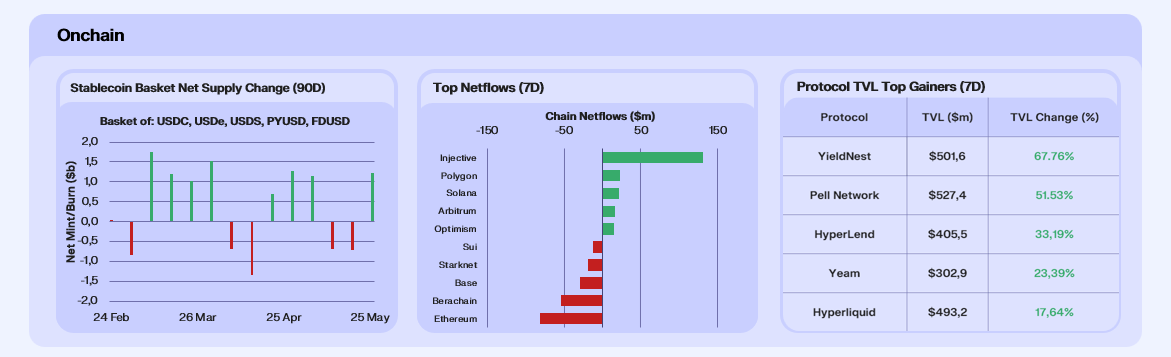

Stablecoin supply expanded this week, having contracted for two consecutive weeks prior. We saw net mints of ~$1.2b, equivalent to a 1.67% lift, reflecting renewed capital inflows into the ecosystem. USDC drove in absolute terms, with $112.9m of fresh USDC finding its way to Aave on Ethereum, despite a slight APR contraction on the week. FDUSD surged 8.53%, likely supported by Binance ecosystem demand, while USDS was the only stablecoin to contract, underscoring capital rotating to chase market moves as opposed to farming yield.

Chain netflows were mixed this week, driven primarily by shifts in underlying fundamentals across chains. Injective led inflows with $131m, propelled by the launch of Upshift, a new institutional-grade yield platform offering structured products and yield vaults on Injective. Arbitrum added $16.1m, boosted by its ‘Timeboost’ upgrade, which improves transaction ordering and MEV capture while channeling revenue to the Arbitrum DAO. Meanwhile Ethereum posted $81.2m in outflows, a rare shift, possibly reflecting rotation into faster, cheaper chains. The main event of the week centered around the Sui hack, with the ecosystem seeing $12.4m in outflows following a ~$250m exploit on Cetus, its largest DEX, which drained key liquidity pools and triggered a sharp, but partially contained, market reaction.

At the protocol levels, capital remains concentrated in high-yield ecosystems. YieldNext and Pell Network led this week, likely driven by rotation into liquid staking and yield-optimised strategies. HyperLend posted another strong week, securing a top-five spot for the third time running, and Hyperliquid saw continued strong growth, as users continue to engage with the HyperEVM ecosystem. Yearn rounded out the leaderboard, benefitting from renewed interest in blue-chip DeFi. While the BTCFi narrative remains present, capital appears more broadly distributed across protocols offering clear utility and compelling yield.

Our Take: The breadth of DeFi activity is beginning to pick up in line with the market. We’re increasingly seeing positive capital flows into new use cases and speculative ecosystems. Coupled with a recent uptick in the altseason index out of the Bitcoin zone, conviction that we’re seeing the early flickerings of life prior to a DeFi and altcoin led rally strengthens.

The Calm Before the Storm

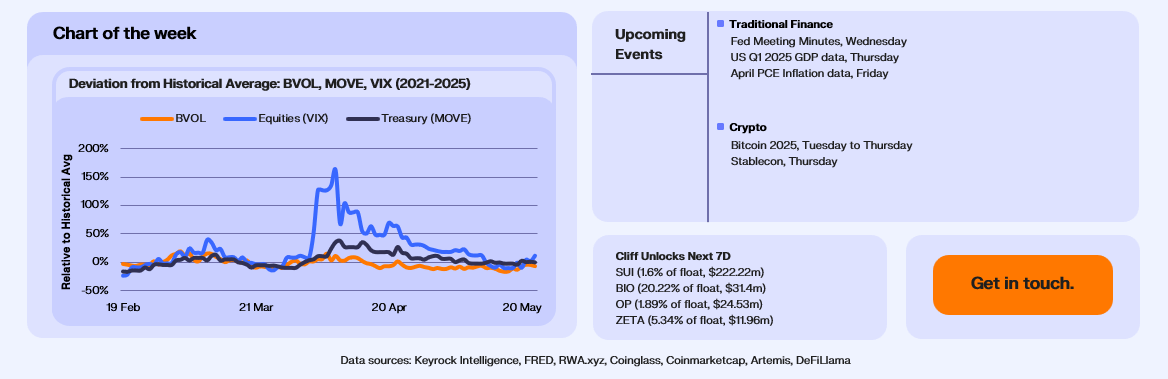

Looking at volatility data in recent months, recent readings reveal a remarkable story of market complacency across all asset classes. All three volatility indices — BVOL, VIX, and MOVE — are now trading near or below their historical averages, with Bitcoin showing the deepest discount. This compressed volatility is particularly striking given that just seven weeks ago, markets experienced one of the most dramatic shocks in recent history when the VIX exploded to over 150% above its historical average on Liberation Day (April 2nd).

The complete inversion during that event, where traditional markets panicked while Bitcoin remained relatively stable, has now given way to an eerie calm across all markets. This week’s low volatility readings raise important questions about whether markets have become dangerously complacent. The rapid transition from extreme fear to today’s relative calm suggests either that April’s concerns have been fully resolved, or more likely, that markets may be underpricing risk in an environment where such dramatic shocks have proven they can emerge with little warning.

Our Take: The current below-average volatility readings across all three indexes appear unsustainable given the evolving macro backdrop. With elevated global bond yields signaling rising inflation and elevated rates, we expect volatility to return above historical averages this year as uncertainty lingers. The compressed volatility in Bitcoin particularly stands out as a potential opportunity. Historically, such deep discounts to average volatility have preceded significant moves. As markets grapple with the implications of tariffs and rates on valuations, the current calm feels more like the eye of the storm than a return to the pre-Liberation Day stability.

Join our Telegram Channel to get it delivered directly to your phone.

Follow our Telegram Channel

Get the edge before markets move. Join our Telegram channel to receive our market update straight in your inbox.