19th May 2025

Key Insights, Retail Rally, Institutional Caution

Soft Prints, Hard Truths

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

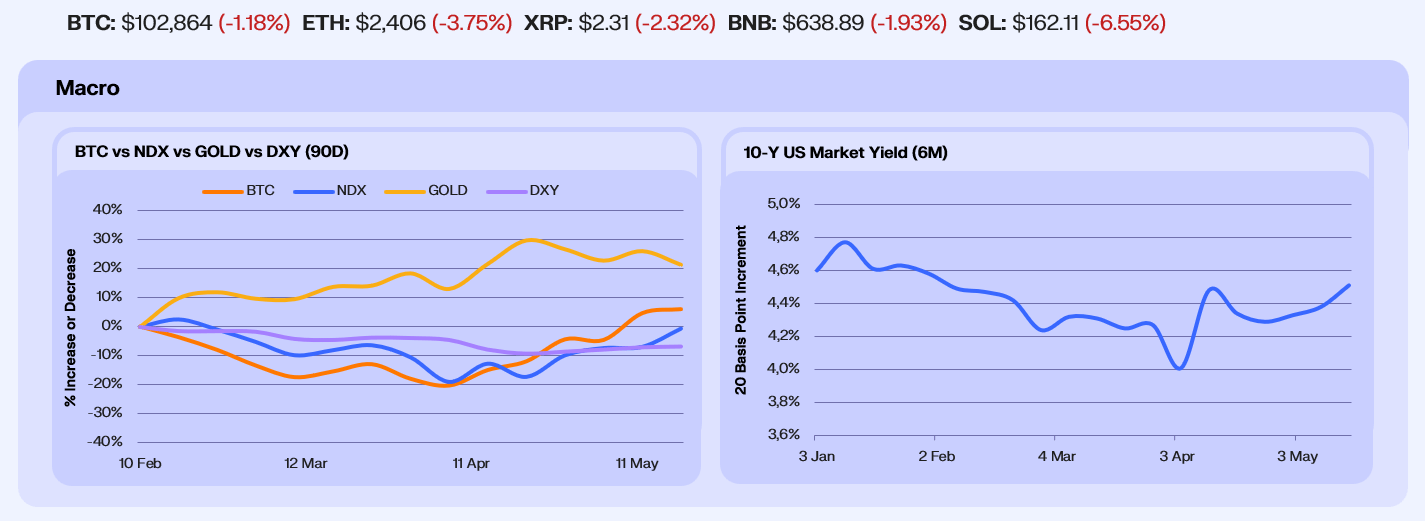

Risk assets rallied across the board this week as easing inflation and tariff relief reignited appetite for risk. The Nasdaq 100 led with a ~3.0% gain, while Bitcoin was up 2.6%, marking its sixth consecutive positive week. In contrast, traditional safe havens sold off, Gold fell 3.7%, its worst week since November 24’. The US 10Y yield spiked to 4.5%, reflecting continued upward pressure despite dovish inflation data. Meanwhile, the DXY rose ~0.3%, its fourth consecutive weekly gain, reflecting moderate dollar strength.

There were several bullish macro headlines this week; April CPI came in at 2.3% YoY, the lowest since March 21’, while PPI recorded its steepest monthly decline since May 20’ at –0.5%. Temporary tariff relief between the US and China drove risk-on sentiment, while retail sales slowed, and jobless claims remained stable. Together, these prints eased near-term inflation fears and revived appetite for equities and duration. That said, yields remain stubbornly high as markets contend with a Fed unwilling to cut, a bond market no longer responding to positive catalysts, and the 30Y Treasury yield breaking 5% into the weekend.

Stress fractures are emerging beneath the rally, however. For the first time in history, Moody’s downgraded US credit, citing unsustainable fiscal paths, with debt-to-GDP projected to breach 130% by 2035. Stock futures fell nearly 1% following the credit outlook downgrade. The last time S&P conducted a similar downgrade in 2011, the SPX lost 8% in two months, while 10Y Yield fell ~35% over the same timeframe. In Japan, the 40Y bond yield surged to multi-decade highs, with Prime Minister Ishiba warning the fiscal situation is “worse than Greece,” as GDP contracts once again. At the same time, retail investors now account for a record 36% of market volume, a surge not matched by institutional flows, which points towards a fragile market structure that will be highly reflexive should retail flows subside.

Our Take: Markets are rallying on soft inflation and tariff relief, but the underlying structure is flashing red. Retail is driving this leg higher while institutions stay cautious. With macro cracks showing, and the market yet to react to the Moody’s downgrade, we expect red across the board on Monday open.

BTC Holds the Line

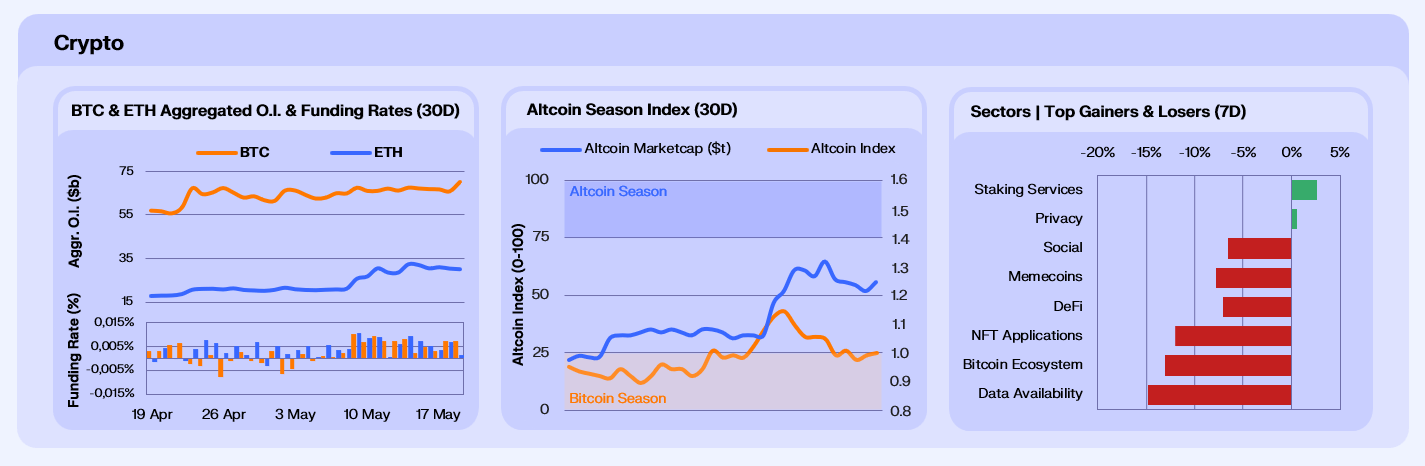

Crypto markets ended the week on firmer footing having consolidated mid-week. Bitcoin OI rose ~4.5% to $70b in the week the orange coin hit its highest ever weekly close, while Ethereum OI rose 5.1% to $30b, as traders added risk following the US credit downgrade and renewed macro volatility. Funding rates remain modestly positive across both assets, indicating balanced positioning rather than excessive leverage.

Ethereum’s recent performance cooled. Analysis suggests last weeks rally to have been driven not by new inflows, but by a cascade of short liquidations. Between May 8th – 10th over $500m in ETH shorts were wiped out, including the largest daily liquidation of the year, while ETH ETF netflows have amounted to a measly $35.6m in the past two weeks. Given these short liquidations have subsided, it’s no surprise ETH performance has slowed this past week, with ETH/BTC down 2.8%.

Altcoins were hit hard this week, with more speculative sectors lagging, such as memecoins, NFTs and BTCFi, reflecting a clear rotation away from high-beta narratives and into more structurally supported protocols. Data Availability led losses post-Pectra, with improved native Ethereum DA capabilities reducing immediate demand and narrative support for alternative DA solutions such as Celestia. Staking and privacy were the only green spots, up 2.6% and 0.6% respectively.

Our Take: Crypto is shifting from momentum-driven gains to macro-sensitive repricing. Capital is still rotating, but increasingly away from high-beta assets and into crypto-native safe havens. With OI climbing and macro volatility re-entering, the next move will likely hinge on how BTC absorbs external stress. This looks to be a reset, not a retreat.

Risk Rotates Onchain

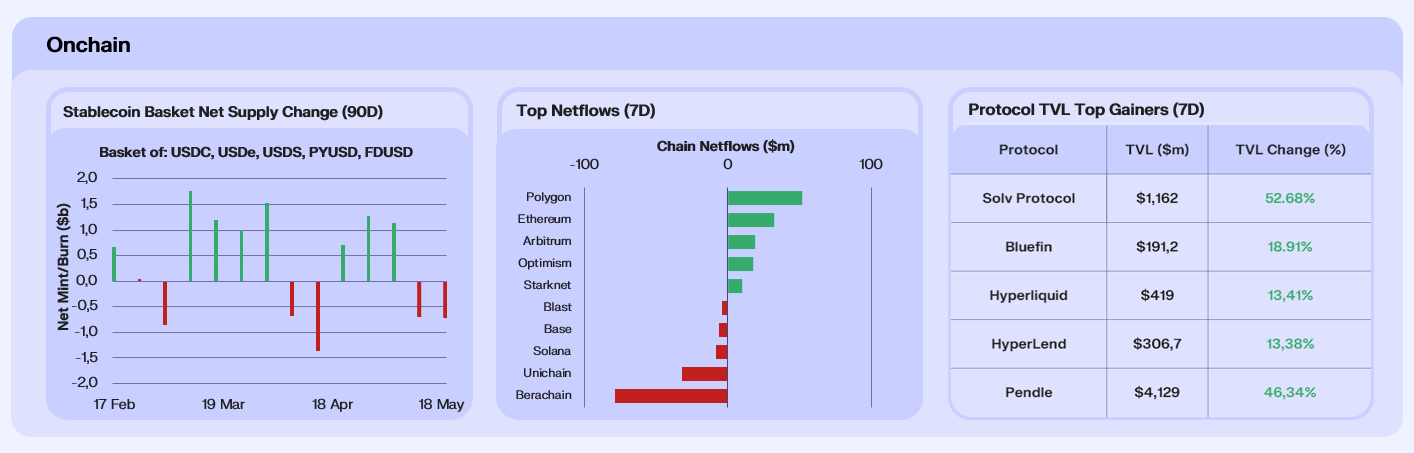

Onchain stablecoin supply contracted by ~1% this week, led by a ~1% decline in USDC. This marks the second consecutive week of net stablecoin outflows and aligns with the ongoing rotation into volatile assets. USDe expanded by ~6.92%, fuelled by integrations with platforms like LayerZero and Blast, and sustained borrowing demand on Aave. In contrast, USDS fell ~5.52%, reflecting a pullback from recent incentive-driven growth as yields decline and users rotate into higher-beta opportunities.

Chain netflows paint a more mixed picture. Polygon and Ethereum led inflows, buoyed by stablecoin inflows and a continuation of activity post-Pectra. However, Base and Solana saw moderate outflows for the week.

At the protocol level, a clear theme is emerging; BTCFi infrastructure is gaining traction. We’re witnessing the early formation of a Bitcoin-native capital stack, with Solv leading the pack this week, and other stack verticals having led in recent weeks. Meanwhile Bluefin continues to rise, benefitting from its position in Sui’s growing ecosystem, and HyperEVM protocols gained, reinforcing the demand for onchain speculation this week.

Our Take: Onchain flows clearly depict sustained risk-on sentiment, but what’s interesting this cycle is the expansion in, and adoption of BTCFi protocols. Previously, a few select protocols have dominated this vertical, primarily from a narrative perspective. We’re now seeing capital to back this up. If these flows sustain, this could be a theme that emerges mainstream this year.

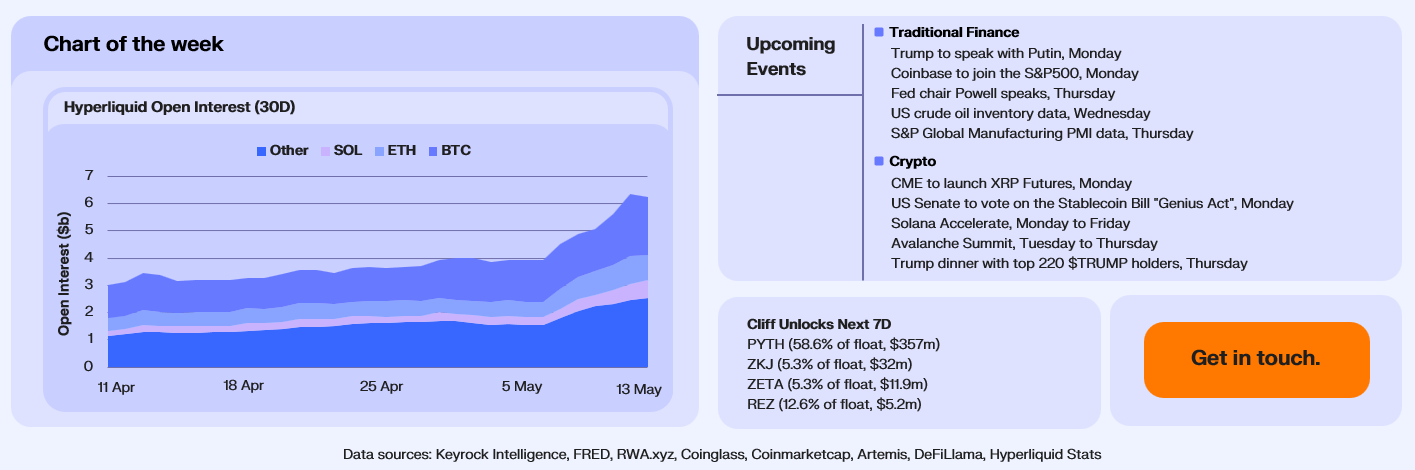

Hyperliquid Hits Escape Velocity

Hyperliquid OI reached a new all-time high of ~$6.34b on May 12th, continuing multi-week momentum. As has been the case since December last year, BTC led with ~$2.28b in OI, but the biggest shift can be seen in ‘Other’ OI, which surged to ~$2.48b, now accounting for ~39% of total Hyperliquid OI. A breakdown of this category highlights a surge in speculative flows into alts and meme-driven assets despite price pullbacks, with HYPE, FARTCOIN, kPEPE and XRP driving the majority of OI.

This surge in OI can be attributed to Hyperliquid’s HLP hitting ATHs in TVL at ~$2.98b, reflecting the growing depth of the protocol’s liquidity infrastructure, and thus capacity to facilitate OI. The bigger picture, however, underscores a structural shift in how users are opting to trade. Hyperliquid itself now commands ~78% of onchain perp volume, another ATH for the protocol. This structural shift extends offchain too, as Hyperliquid nears its highest-ever perps market share relative to Binance, now trading at ~8.5% of Binance’s perp volume.

The implications are twofold. First, we’re in a clear speculation-heavy environment, with traders placing trades in speculative assets in alts and memes. Second, Hyperliquid is the protocol capturing that flow, and not just through liquidity, but through product breadth too, with Hyperliquid offering a broader range than any DEX or CEX competitor. As majors consolidate and new retail capital returns, protocols that can scale volume without friction and respond quickly to token demand will lead the next phase of growth.

Our Take: Hyperliquid’s breakout is more than a function of alts-driven speculative, it’s a structural rerating. We expect Hyperliquid to catalyse perp volumes flowing onchain throughout 2025.

Join our Telegram Channel to get it delivered directly to your phone.

Follow our Telegram Channel

Get the edge before markets move. Join our Telegram channel to receive our market update straight in your inbox.