8 September 2025

Key Insights: Jobs Shock, Crypto Resets

Jobs Shock Bounce

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

Last week, markets rebounded as the U.S. August job reports came in considerably below expectations (22k vs 75k expected), with June revised negative, and thus the first negative job print since 2020. Bitcoin (+3.4%) and the Nasdaq (1%) jumped while Gold hit all time highs (3.2%) and the Dollar Index (-0.1%) shed all its weekly gains as expectations for more aggressive rate cuts increased. A 25 bps September rate cut is all but locked in, while odds for 3 rate cuts in 2025 spiked from 18% to 38% on the news.

As expected with a poor jobs report in the wake of Powell signaling labor market weakness as a key consideration for a cut, the yield curve steepened. Short-end yields dropped 7–8 bps as markets priced in greater odds of Fed easing, while the 2Y held flat and the long end slipped 6 bps. This reinforces how markets are embracing a ‘bull steepening’ narrative, driven more by rate-cut anticipation than by renewed confidence in the economic outlook.

Volatility was muted throughout the week. Bitcoin IV slipped from 41.1 to 40.1 (-2.4%), while Ethereum’s IV slightly edged higher from 73.28 to 74 (+1%). Crypto vols remain contained, with option markets showing little urgency despite next week’s August CPI.

Our Take: A September cut was long anticipated, but markets are now leaning toward a more aggressive easing path that the Fed has yet to justify with the data. Bitcoin and equities have already priced in the near-term cut, leaving momentum muted, while gold’s breakout signals a defensive bid. Still, with cuts already priced and CPI risk ahead next week, chasing upside may offer less reward than positioning defensively into September.

Selective Altcoin Gainers

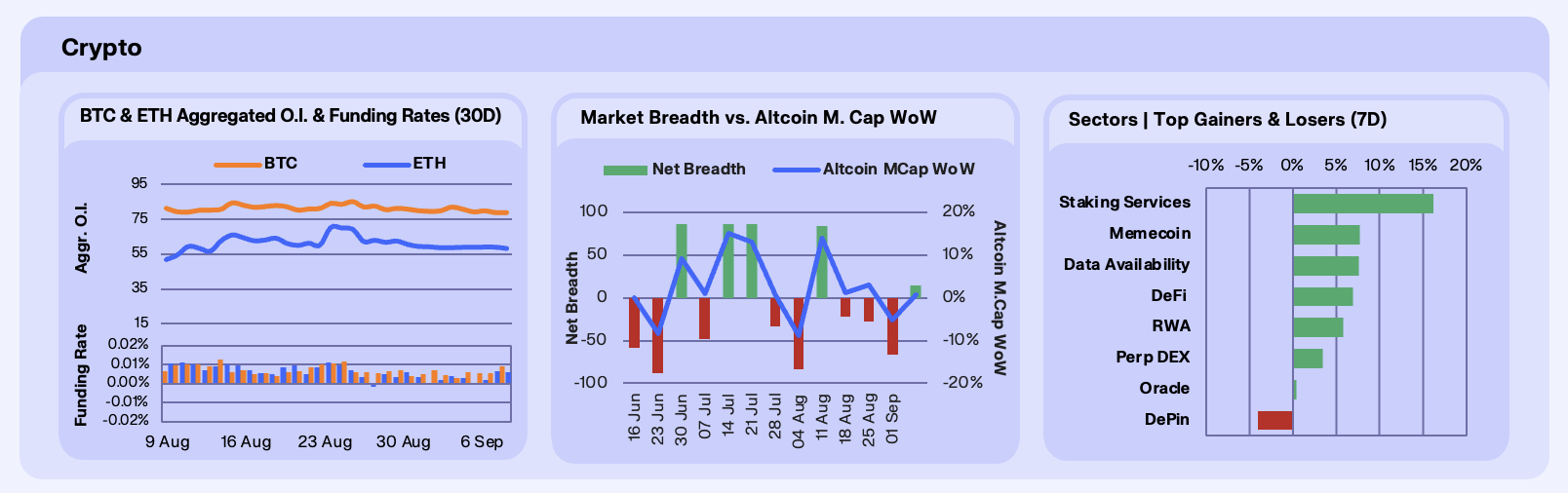

After three consecutive weeks of negative breadth, altcoins finally posted a modest rebound. Altcoin market cap rose 0.6% last week, with 57 of our 100 tracked tokens finishing higher (versus 43 lower) for a net breadth of +14. The recovery follows recent sell-offs that has kept traders cautious and selective in their altcoin exposure. In the short term, sustained momentum across altcoins remains shaky and is likely to hinge on macroeconomic catalysts that can shift sentiment quickly.

Just as with altcoins, sector performance was also disjointed. Performance was led by RWAs (5.8%), Perp DEXes (+3.4%), and staking services(+16.2%), with SYRUP a notable outperformer as Maple Finance marked its all-time high monthly revenue in August ($1.4m) and is on pace to post its highest quarterly revenue ever (>$4m). Overall, sector moves were less about broad risk appetite and more about token-specific catalysts, leaving performance scattered and not directional. This dynamic reinforces the idea that the current market is being driven by narratives and isolated themes rather than synchronized sector trends.

Bitcoin and Ethereum open interest continues to stay elevated despite a shaky market. BTC OI eased slightly to $79.2b from $81.9b, while ETH held firm around $58–59b. Funding stayed in positive territory, indicating a steady long bias, though positioning appears contained rather than overheated. This suggests positioning has shifted from aggressive buildup toward sustained leverage, leaving the market balanced but still sensitive to shifts in spot direction.

Our Take: Since early August, most altcoins have failed to make new local highs, fueling concerns the market may have already topped. Although in the near term performance will likely hinge on macro catalysts, sector narrative momentum and still-elevated open interest in Bitcoin and Ethereum point to altcoins consolidating within a range rather than breaking down, which creates a constructive risk-reward setup into Q4.

Cautious Onchain Capital

Onchain rates took a hit across the board this week with the general story being one of supply inflows outpacing leverage demand following $150m BTC long liquidations. USDC APY fell 11.3% WoW amid Aave deposits rising 23.1%, a dynamic in which demand failed to keep up with supply. USDT saw similar dynamics, dropping 12.4% WoW as supply rose 3.4%, pointing to an even further drop in demand for USDT. WETH rates fell 6.5% WoW in line with supply contracting 16.1%, highlighting soft borrow demand despite ETH’s ETF-driven price action.

Ethereum led inflows yet again, with ~$600m of capital flowing into the largest DeFi ecosystem by TVL. Bitcoin also saw inflows, though far more muted at ~$40m, supported by DAT expansion. Base was the largest loser, with ~$300m in outflows, reflecting rotation back to the L1 and a lack of organic, non-incentive driven demand to transact on the Coinbase chain. Arbitrum also faced outflows of ~$200m, with ecosystem trading volume down from ~$410m in August to ~$175m in early September, signalling the lack of demand to trade on L2s doesn’t sit with Base alone.

It was a good week for RWAs, with the total AUM rising 1.42% WoW, extending its 30-day growth to 7.21%. Maple grew ~2% this week, with growth from syrupUSDC as the asset expanded to Arbitrum. Paxos was up 2.8% in AUM, with PAXG benefitting from gold nearing $3,470/oz, with inflows pushing AUM near $1b. Centrifuge saw a slight pullback after Augusts’ 252% surge and $1b+ CLO fund allocation, signalling the sustainability of these flows given the shallowness of this pullback.

Our Take: Stablecoin yields remain compressed as capital continues to flood into lending venues, reflecting safety-seeking after last week’s liquidation flush. Onchain users are reflecting the current uncertainty in the market, with a resistance to push down the risk continuum, highlighting the fragility of market sentiment at this phase of the cycle.

Prop AMMs Dominate

This week we’re highlighting Solana’s onchain SOL-stablecoin DEX volume composition by DEX type, categorised across traditional AMMs such as Orca and Raydium, orderbooks, such as Phoenix, and prop AMMs such as SolFi, HumidFi and Lifinity. At a high-level, traditional AMMs are constant pool products, leveraging the famed ‘xy=k’ formula to passively provide liquidity with fixed formulas. Orderbooks merely refer to central limit order book style models, while prop AMMs dynamically adjust spreads using inventory-skew models to offer more efficient execution.

Since November 24’, prop AMMs have been rapidly gaining market share, jumping from ~35% in October 24’ to ~60% today. Traditional AMMs are the venues that have taken a hit as a result, falling from a dominant ~70% to ~40%, with orderbooks all but dormant on Solana today. The rise in prop AMMs demonstrates market participants’ preference for execution quality over legacy AMM models, with prop AMMs inventory-skew models allowing for tighter spreads. Solana is now effectively pioneering the next generation of liquidity infrastructure, with its execution environment favouring automated liquidity vs. central-limit models.

Our Take: Prop AMMs are now the default model for trading on Solana. If current trajectory holds, we see them exceeding 75% dominance as we head into 2026 across core SOL-Stables pairs. This would represent a reshaping of liquidity on Solana, with the potential to spark a new wave of incentive wars as prop AMMs jostle for position.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.