4 August 2025

Key Insights, Holding the Line

A Turn in the Tide

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

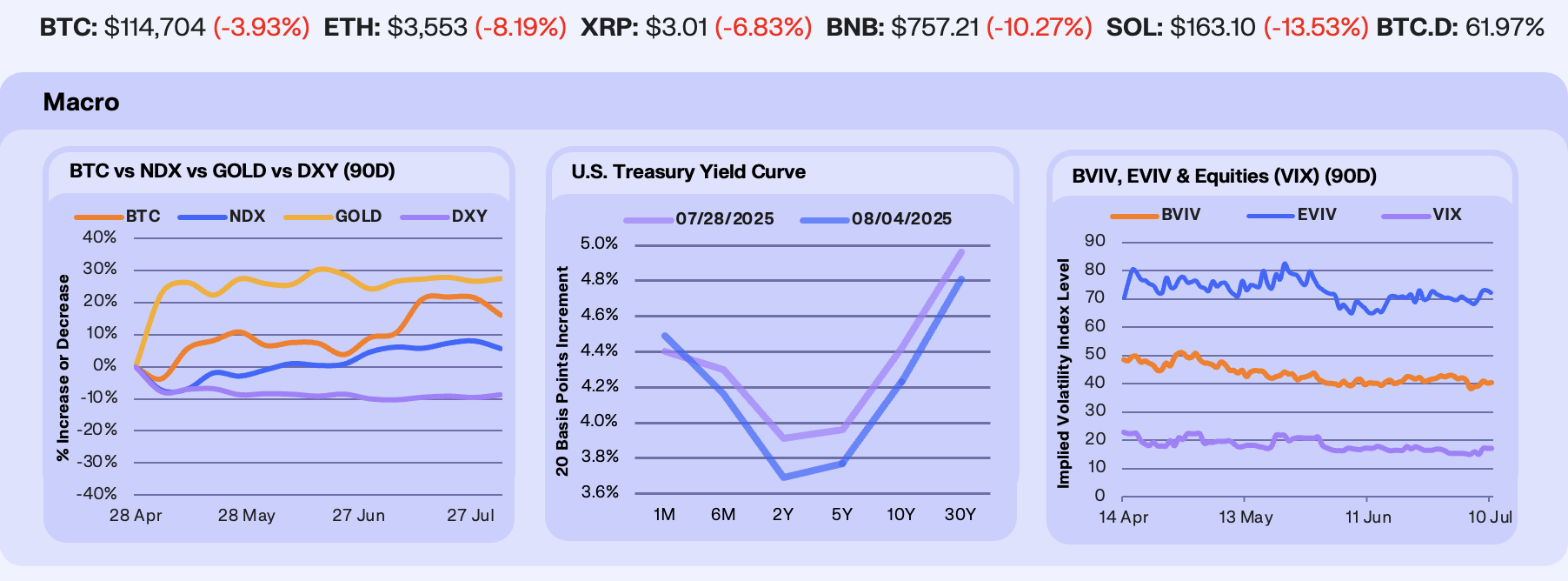

Last week was one of the busiest of the year, with large-cap earnings, the Fed’s rate decision, and tariff announcements driving markets. The Dollar (+1%) and Gold (+0.7%) both posted weekly gains, while tariff headlines and the July jobs report weighed on risk appetite, leading Bitcoin (-4.4%) and the Nasdaq (-2.2%) lower.

The narrative shifted sharply on Friday after the July jobs report came in well below expectations, with May and June payrolls also revised down. This triggered a Treasury rally, driving yields lower across the curve and sending Polymarket odds for a 25 bps September rate cut surging from 38% to 72%. The Treasury curve bull flattened, with the 30Y yield falling to 4.81% and the 2Y dropping -22 bps on the week. While front-end yields had been pinned higher earlier by strong GDP data, the weak jobs data overpowered that as markets priced in a faster pivot from the Fed.

Bitcoin’s implied volatility continued to ease, falling from 41.2 to 40.4 (-1.9%), while Ethereum’s was little changed and remains elevated at 72.1. Our options desk observed BTC and ETH realized volatility compress recently. However, ETH and the broader altcoin market realized volatiltiy are huge compared to those of BTC. The market seems reluctant to lower the vols further in ETH. Equity volatility moved in the opposite direction. The VIX rose from 15.2 to 17.4 (+12.5%) as earnings results and tariff concerns weighed on market sentiment.

Our Take: With macro uncertainty running high, traders turned defensive across risk assets. BTC stalled near $118K–$120K and ETH pulled back from $3,800, driving a wave of short-term hedging into early August. The protection points to nerves over near-term volatility rather than a shift in longer-term conviction. The bigger risk is the market’s reliance on institutional inflows. Without them, sentiment suggests ETH could have easily slipped below $3,500. Overall, positioning looks defensive, but not outright bearish.

Majors Reset

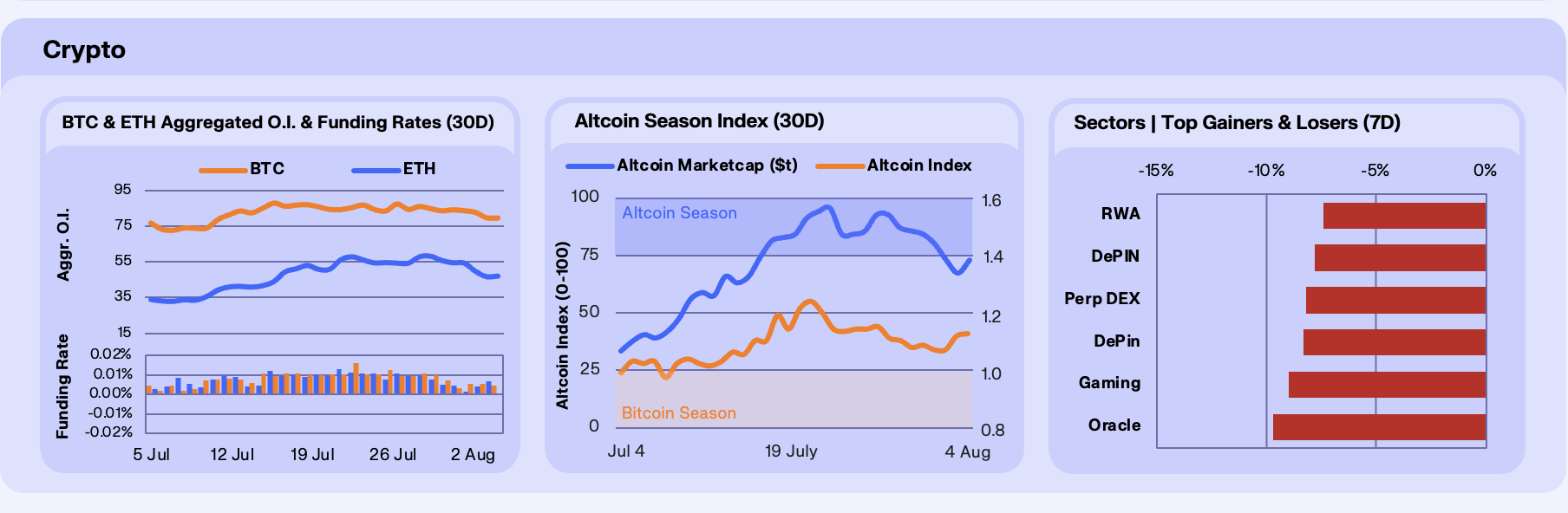

It was a week of pullback for majors following BTC’s push to ATHs last week. BTC and ETH dipped –4.2% and –9.6% respectively. SOL underperformed, falling –16.3% as profit-taking hit after a strong July. Headlines were dominated by the SEC, which approved in-kind redemptions for BTC and ETH ETFs, bringing improved arbitrage mechanisms and potentially tighter spreads. The regulator also launched Project Crypto, a regulatory overhaul that could fast-track ETF approvals for other assets like Solana and XRP. Meanwhile, institutional allocation continued. MicroStrategy upsized its STRC offering due to strong demand, from $500m to $2.52b, announcing a $4.2b ATM STRC program alongside the IPO. This will fuel further BTC buys. Mill City joined the Digital Asset Treasury (DAT) adoption wave with a $450m SUI purchase, the first major DAT for SUI.

Funding markets softened across the board. ETH open interest dropped sharply (-45% WoW), unwinding post-DAT euphoria and flushing out long leverage. BTC OI remained marginally more stable, down just –6.7%, as traders held onto high-conviction positions. Perps funding remains stabilised near neutral on both majors. Overall, the market looks reset, but not yet re-leveraged.

The Altseason Index fell –6.54% WoW, to touch its lowest reading since June. Broader altcoin market cap slipped from $1.57t to $1.43t, led by rotation out of high-beta names and waning momentum in the long tail. Despite positive ETF regulatory signals, most of the capital remains concentrated in majors, with signs that traders are de-risking into strength rather than rotating down the risk curve.

It was a red week across all major sectors, with DeFi (-10.7%) and Data Availability (-12.8%), led by assets such as Sky and Celestia, posting the steepest losses. Even defensive narratives like RWA (-7.4%) and Perp DEXs (-8.2%), which have retained strong fundamentals, couldn’t hold up as risk appetite faded. The weakness reflects broad de-risking and reduced speculative rotation, with few catalysts to support sector-specific outperformance.

Our Take: Majors conviction remains strong, especially with the SEC outlining perhaps one of the most bullish regulatory paths forward crypto has ever seen, but the market needs time to digest. Deleveraging is a healthy reset. If BTC and ETH can find support above key levels of $111k and $3,375 respectively, we expect alts to regain steam in late August. For now, this feels like a breather, not a breakdown.

Yield Rises, Flows Stall

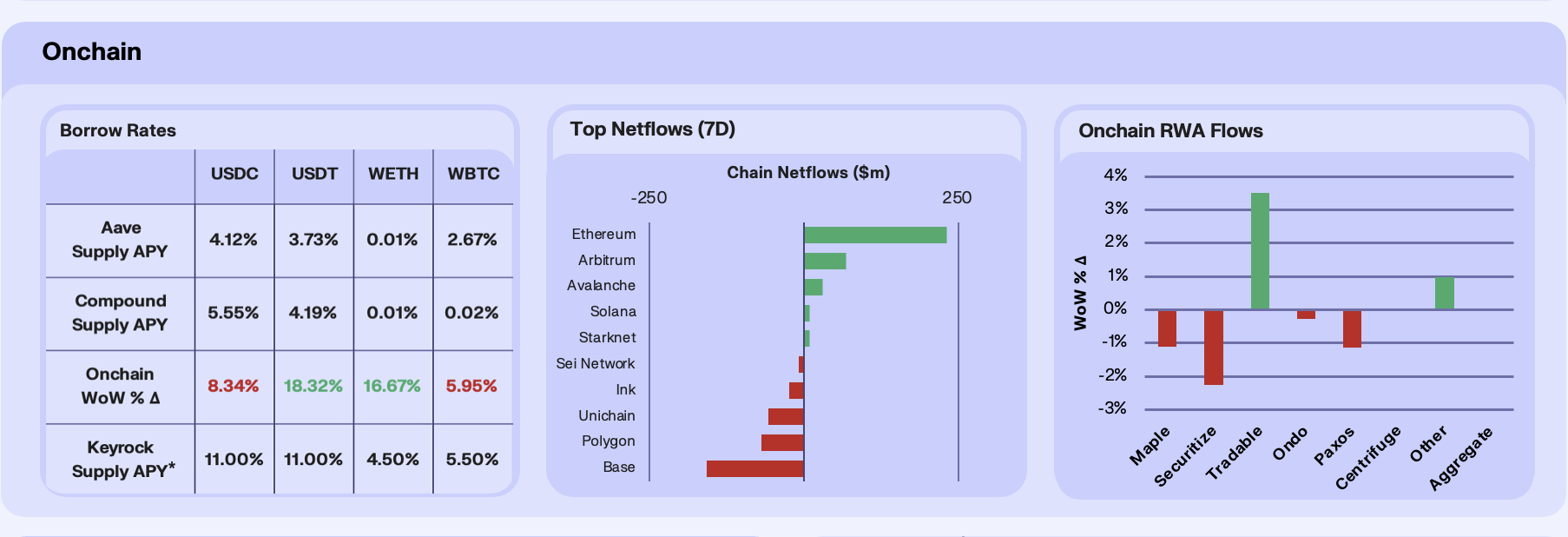

Rates moved higher across all major assets this week, driven by a rebound in borrowing demand and reduced supply in key lending pools. USDC and USDT supply rates climbed to 4.12% and 3.72% on Aave, weekly gains of +8.3% and +18.3%, respectively. The move likely reflects increased delta-neutral borrowing and less aggressive yield farming supply inflows. WETH supply APYs stabilised around 2.55% after last week’s stETH unwind, while WBTC remained stuck near 0.01%, reflecting continued low demand for BTC leverage in DeFi.

Netflows reversed sharply. Ethereum was the only chain with meaningful inflows, while Base posted its second consecutive week of major outflows. Polygon and Unichain followed with notable losses, while Avalanche and Arbitrum showed small gains. Breadth of net-negative flows suggests capital is rotating cautiously rather than exiting the ecosystem entirely.

Given the growth rate of the RWA sub-sector, starting this week we’re including a data section on RWA flows, shown at the protocol level. RWAs posted on aggregate a relatively flat week this week, at –0.02% onchain AUM, following the strongest weekly gain since February last week. Permissionless, onchain providers, including Maple and Paxos, were the largest losers, suggesting short-term rebalancing rather than structural outflows.

Our Take: Lending rates are rising, not because of explosive demand, but because supply has temporarily dried up. Meanwhile, RWA flows may plateau in the near term, but the sector’s structural trajectory remains firmly up and to the right. The dynamics we’re seeing onchain are in line with the general sentiment drawback, though we expect this to reverse sharply upon a sentiment reversal.

Ethena’s Institutional Play

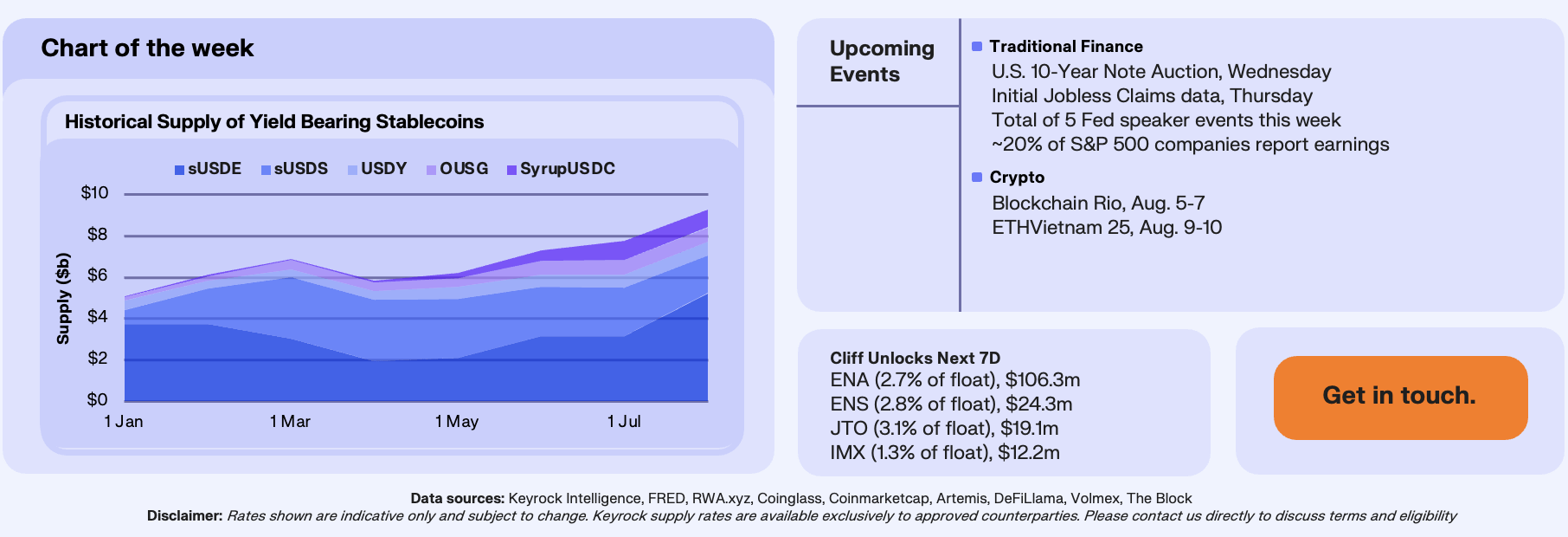

sUSDe supply has surged 59.5% since July 17 to $5.2b and has distributed over $324M to holders, nearly half of the $730m cumulative yield paid out by all yield-bearing stablecoins. Overall, Yield-bearing stablecoins have marked an all-time high of $9.3b in TVL, underscoring how quickly crypto-native yield products are absorbing liquidity.

The immediate driver is Ethena Liquid Leverage on Aave and rising funding rates. Users are looping 50/50 USDe/sUSDe positions by borrowing USDC, USDT, or USDS, amplifying exposure to sUSDe yields. At the same time, Ethena is exploiting divergences in funding rates across exchanges.

This fits neatly into Ethena’s Convergence roadmap, which moves from DeFi-native traction to CeFi distribution and eventually into TradFi portfolios. sUSDe is structurally distinct because its returns are negatively correlated with real rates. When rates fall, yield potential rises. With U.S. rates near 4.5% and expected to decline, institutions facing portfolio compression have a logical alternative. With CeFi distribution through CEXs, integrations like PayPal, and the development of a TradFi-oriented liquidity hub, the groundwork for institutional adoption is in motion.

Our Take: sUSDe’s surge is more than opportunistic yield-chasing, it builds on Maker’s template for bringing institutional capital into DeFi yields. Ethena provides the infrastructure while TerminalFi bridges to TradFi. If adoption follows the roadmap, the upside isn’t just billions in stablecoin supply, but the recognition of sUSDe as a legitimate asset class for institutions.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.