23 February 2026

Key Insights: Higher Bar for Cuts

Dollar Up, Bitcoin Drifts

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

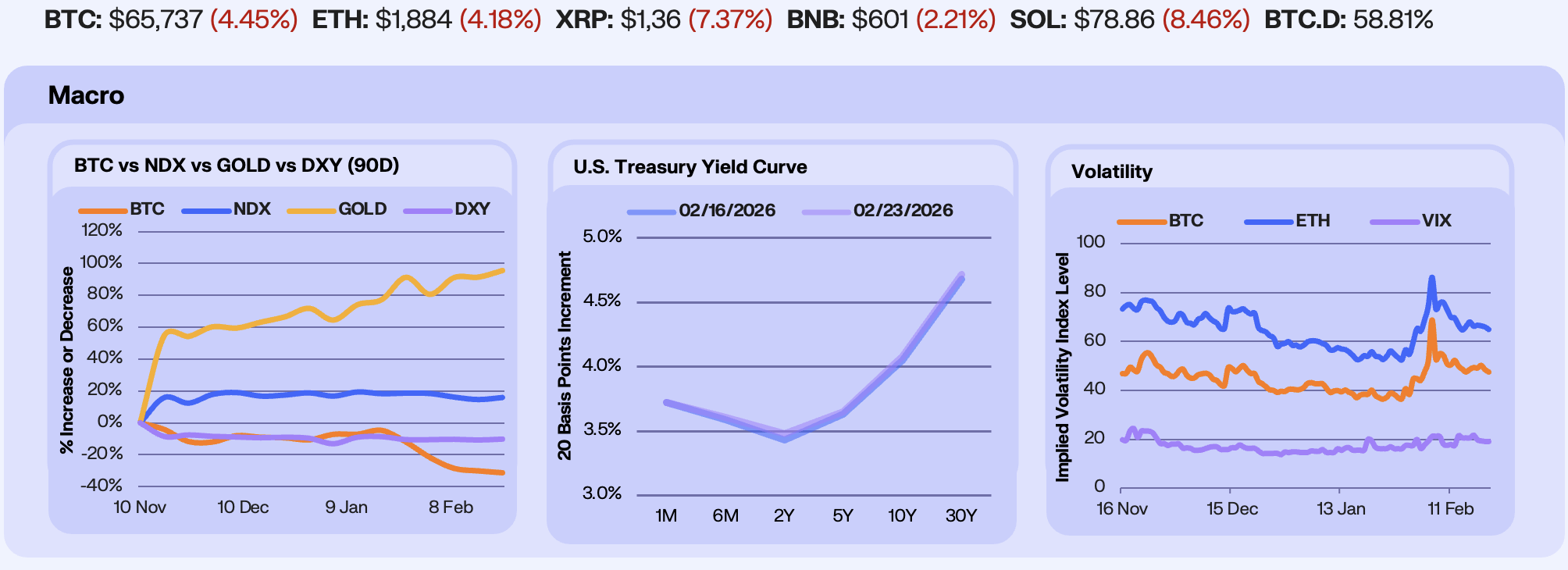

Markets consolidated this week, weighed by geopolitical tensions in the Middle East and mixed corporate earnings, while incoming macro data reinforced a resilient labour market. As a result, Fed minutes struck a hawkish tone with several participants warning that rates may need to move higher in coming months, bolstering the case for policy to remain restrictive for longer. The combination supported the dollar and kept rate cut expectations contained. BTC fell -1.7% on the week, gold edged higher +2.2% after surging above $5,000/oz on escalating US-Iran tensions, the NDX rose +1.13%, and the DXY gained +0.7%.

Rates markets reflected the firmer policy stance. Treasury yields moved modestly higher across the curve as traders absorbed signals from the latest Fed minutes that policymakers remain unwilling to rush into cuts despite softer data, anchoring yields near recent levels. The 10-year has held close to the psychologically important 4% mark, suggesting markets are balancing resilient growth data against downside risks to activity. Strong demand for long bonds at auction and safe-haven flows amid Middle East tensions have also contributed to keeping yields firm even as inflation expectations moderate, signaling that policy may stay restrictive for longer rather than swiftly pivoting to easing.

Volatility remained relatively contained despite the macro crosscurrents. BTC 30-day ATM implied volatility was unchanged WoW at 47, while ETH IV edged lower -1.9% to 65, and the VIX declined -7.3% to 19. Equity markets remain cautious but orderly. Options positioning across BTC and ETH shows a defensive bias.

Our Take: The next key catalyst is NVIDIA’s earnings on February 25. Given the equity market’s sensitivity to AI-driven growth expectations, guidance will likely have an outsized impact on tech, which Bitcoin has been tracking close to, and broader risk sentiment. A strong print could reinforce resilience and give confidence to equity investors, while disappointment risks reigniting volatility across high-beta assets, including Bitcoin.

Defensive Positioning Persists

Crypto markets drifted lower as the absence of a clear catalyst kept positioning cautious. BTC consolidated between $65K and $70K, while derivatives positioning rebuilt modestly. BTC open interest rose +4% WoW to $43.5b, and ETH OI climbed +3.5% to $24.2b. Funding rates largely traded sideways, though ETH perps spent much of the week below zero, signaling persistent downside bias among short-term traders. The extreme bearishness priced into futures markets over the weekend is now keeping investors defensive.

Institutional flows turned defensive again. Digital asset investment products saw approximately -$580m in net outflows this week, reversing last week’s modest accumulation. The average U.S. Bitcoin ETF holder is now sitting on roughly a 20% unrealized loss, with an estimated cost basis near $84K versus spot around $67K. Despite this, total ETF holdings remain within ~5% of all-time highs in BTC terms, indicating that while sentiment has deteriorated, structural allocation has not meaningfully unwound. The posture is defensive and the margin for error simply remains thin at current levels.

Crypto sectors broadly repriced lower this week as risk appetite faded and macro uncertainty lingered. Defensive areas like Utilities outperformed on a relative basis (-4.9%), while other segments bore the brunt of the move. Social (-15.7%) and Perp DEXs (-11.6%) led declines, reflecting reduced speculative activity and softer derivatives volumes amid choppy price action. AI (-10.1%) also retraced after recent strength, as investors trimmed exposure to narrative-driven themes. Overall, the rotation signals continued defensiveness, with capital stepping back from momentum trades rather than reallocating aggressively within crypto.

Our Take: The CLARITY Act is emerging as crypto’s most important near-term catalyst. Polymarket traders are pricing an 80% chance of passage this year. If signed, the bill would finally delineate SEC vs CFTC jurisdiction, giving tokenholders and projects the regulatory certainty they’ve lacked for years. Reduced enforcement risk and clearer listing pathways could unlock institutional capital that’s been sidelined by compliance ambiguity. With sentiment at rock bottom and infrastructure quietly building, clarity on the rules of the game may matter more than price action right now.

Onchain Growth Slows

Onchain rates reflected soft leverage demand. Stablecoin supply yields remained compressed, with Aave USDC at 2.35% and USDT at 1.79%, while Compound offered 2.52% and 2.41%, respectively. USDT yields drifted lower WoW, consistent with declining utilization and muted borrow appetite rather than fresh dollar-leverage buildup. In contrast, WETH supply APY moved modestly higher, with Aave WETH at 2.95%, suggesting more selective ETH-denominated positioning. Keyrock continues to stand out with structurally higher yields across USDC, USDT, and WETH, reflecting differentiated capital efficiency.

Cross-chain flows showed repositioning. Ethereum led with +$149M in net inflows, followed by Hyperliquid at +$93M, reinforcing capital concentration in core leverage venues. However, Arbitrum saw a substantial −$294M outflow. While part of that likely reflects users bridging out of Hyperliquid, the net differential implies capital is still exiting onchain perp venues in aggregate. Optimism and BNB Chain also posted declines, suggesting the dominant theme is contraction and venue consolidation rather than fresh speculative inflows.

RWAs softened at the aggregate level, with total AUM down −0.7% WoW. Dispersion widened meaningfully beneath the surface. Securitize rose +13.5%, benefiting from distribution strength and secondary liquidity advantages, while credit-heavy protocols underperformed. Maple fell −4.1% and Centrifuge slipped −0.49%, consistent with allocators trimming duration and balance-sheet risk amid macro uncertainty. Across 2026, institutional interest in real-world asset tokenization has accelerated, with demand emerging for tokenized treasuries, fixed-income instruments, and other traditional assets finding onchain homes, a trend driven by broader financial integration and regulatory clarity that is lowering structural barriers to participation.

Our Take: Onchain conditions remain defensive. Stablecoin utilization remains subdued, leverage demand is selective across tokenized products but is growing, and flows are consolidating into execution-efficient venues while growth is concentrating in distribution-led platforms. A sustained rise in stablecoin utilization alongside RWA expansion would signal genuine balance-sheet growth. Until then, the market remains in consolidation rather than early-cycle reacceleration.

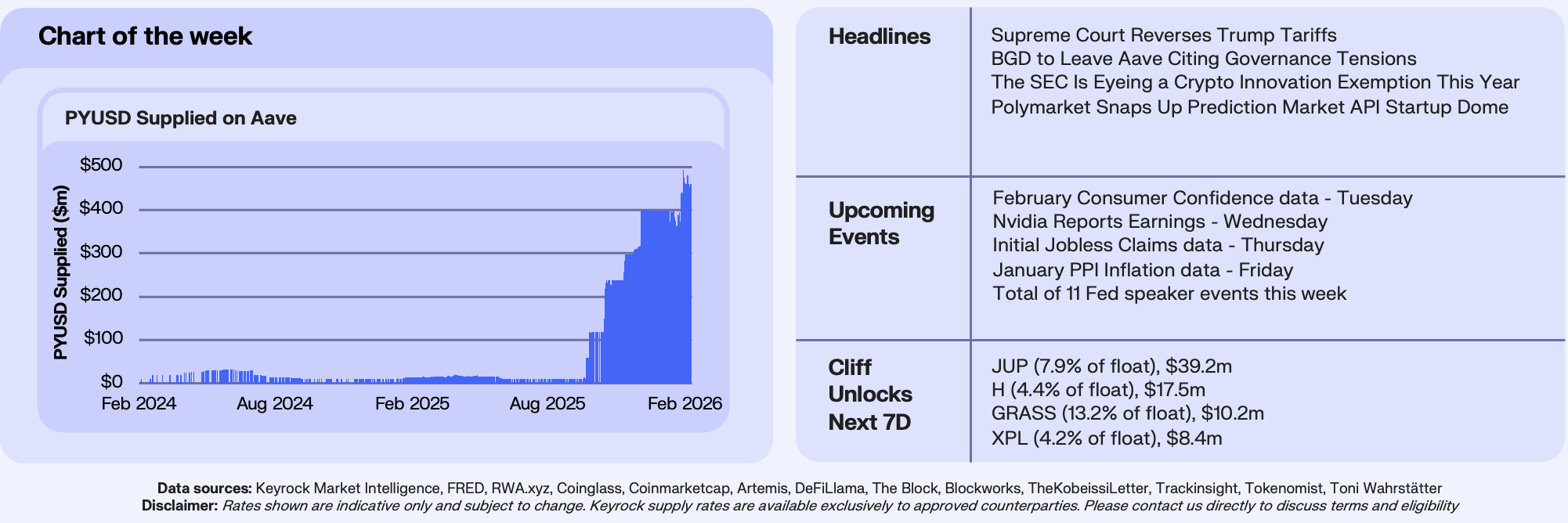

PYUSD Scales on Aave

PYUSD deposits on Aave V3 have quietly surged this quarter. PayPal’s stablecoin now sits at $463M supplied on Aave’s Ethereum market, just short of its all-time high deposits on Aave and approaching the 500M supply cap that was raised from 400M just two weeks ago after reaching full utilization. The growth has not been speculative.

PayPal, through its partner Trident Digital, is directly incentivizing Aave deposits with up to 4% APR in PYUSD on top of the protocol’s base yield, distributed monthly via a Merkle contract administered by the ACI team. The campaign also seeded an $8M PYUSD/GHO liquidity pool on Balancer, with maintenance costs split between PayPal and Aave DAO. Alongside this, PayPal launched a separate PYUSD Savings Vault on Spark offering 4.25% APY, with a stated goal of reaching $1B in deposits. The broader PYUSD supply has expanded from roughly $500M to $4B in the span of a year, and a meaningful share of that growth is flowing into DeFi lending markets through these incentive programs.

Aave’s PYUSD supply cap hit 100% utilization on Feb 4, prompting a Chaos Labs risk steward proposal to lift the cap from 400M to 500M. That new ceiling is already ~92% filled. At the current pace, another cap increase proposal looks likely within weeks. In effect, Aave governance is being mechanically pulled forward by PayPal’s distribution budget.

Our Take: This is one of the clearest examples of a TradFi firms direct intregation into DeFi working. The incentivization playbook is simple and clear, but what remains to be seen is the durability of it. Borrow utilization has remained consistently above 50%, suggesting PYUSD is finding use in savings, leverage, carry, or arbitrage strategies. However, its clear the additional incentives are doing significant work. Whether borrow demand can sustain current deposit levels without subsidies will determine if this marks a lasting liquidity migration, or simply a well-executed yield offering.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.