26 January 2026

Key Insights: Greenland on Ice

All Eyes on the Fed

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

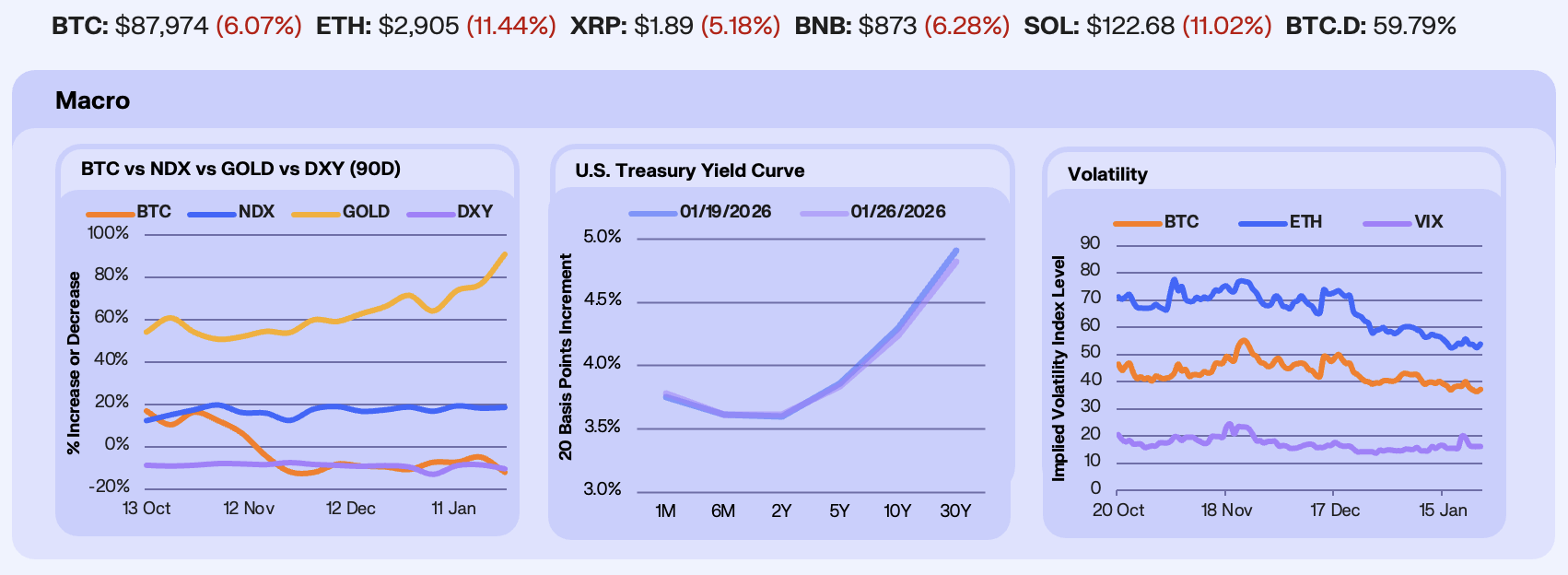

Last week unfolded amid easing geopolitical tension and stronger-than-expected growth data, allowing markets to stabilize after prior uncertainty. The US and EU moved toward a framework agreement on Greenland, with President Trump signaling US involvement in future mineral development and stepping back from tariffs on Europe. BTC fell -7.5%, continuing to trade as a higher-beta expression of Nasdaq weakness, while gold surged +7.9% to break above $5,000 per ounce for the first time. NDX finished effectively flat at +0.3%, and the DXY weakened -2.0% on yen intervention talk. Separately, US GDP growth surprised to the upside at +4.4% in Q3 2025, the fastest pace in two years, reinforcing the resilient growth narrative.

Rates markets reflected a modest repricing of policy expectations. Treasury yields edged slightly higher at the front end, with 1M tenor up +3 bps and 2Y up +1 bp, while the long end moved lower, flattening the curve. Following November PCE data that pointed to lingering inflation stickiness, investors have trimmed expected easing to roughly 40 bps of rate cuts by year-end, down from around 50 previously. The adjustment highlights a growing view that growth remains firm enough to limit near-term policy urgency, even as inflation continues to cool only gradually. Adding to near-term uncertainty, prediction markets are now pricing roughly a 78% probability of a US government shutdown by January 31.

Volatility spiked briefly midweek before settling. The VIX rose sharply amid uncertainty around US-Europe relations, then retraced once the Greenland framework was announced. Crypto volatility followed a similar pattern. BTC and ETH IV rose as Bitcoin slipped below $90,000 and ETH dipped under $3,000, before easing back toward multi-month lows by week’s end. BTC IV finished down −3.2% WoW to 37, ETH IV down −0.5% to 54, while the VIX ended higher by +4% to 16.1. Despite subdued spot volatility, options markets are signaling caution, with skew implying roughly 42% odds of BTC trading below $85,000 in January.

Our Take: Markets enter the coming week with conviction still fragile and focus squarely on policy signals. The Federal Reserve meeting looms as the primary catalyst, with no change in rates expected but close attention on messaging around inflation persistence, labor dynamics, and growth risks. A patient tone would likely support equities and pressure the dollar, while a more cautious or inflation-sensitive stance could reintroduce volatility across risk assets.

Flows Set the Tone

Derivatives positioning softened over the week as funding rates compressed toward neutral, with BTC funding briefly flipping negative during the selloff. Open interest declined modestly, with BTC OI down -3.3% WoW and ETH OI down -6.5%. Notably, despite the weekly pullback, both BTC and ETH open interest remain roughly +10% higher year-to-date, suggesting speculative participation has stabilized even as markets digest persistent headline risk. Overall, positioning is cautious as we head into a data packed week.

Institutional flows turned decisively negative, with roughly $1.9b in net outflows over the week, including $1.3b from Bitcoin products alone. This marked the largest weekly redemption since November and mirrors prior episodes where heavy ETF outflows coincided with local price troughs. In November, a similar four-day withdrawal of approximately $1.22b preceded BTC finding a low near $80,000 before rebounding above $90,000. While not a timing signal on its own, the magnitude of redemptions is historically consistent with late-stage selling pressure.

Altcoins remain broadly disconnected from the rest of the market. Despite retail participation of capital markets sitting near COVID-era highs, that activity has largely failed to translate into sustained demand for most alt tokens, with capital instead concentrating in equities. Sector performance continues to skew negative, underscoring a lack of conviction beyond a narrow set of themes. This disconnect has prompted growing industry introspection around token value capture, governance, and the legal and economic rights afforded to tokenholders, as participants reassess which assets can justify long-term allocation in a more mature market environment.

Our Take: With BTC struggling to regain upside momentum, demand for leveraged long exposure has remained muted, raising questions around the durability of the $90,000 support zone. A sustained move back toward $100,000 appears increasingly dependent on a reversal in institutional flows. While recent ETF outflows have weighed on sentiment, the combination of lighter leverage, neutral funding, and historically large redemptions suggests downside pressure may be maturing. Institutional flow dynamics remain the key variable to watch in the near term.

Sustained Onchain Defensiveness

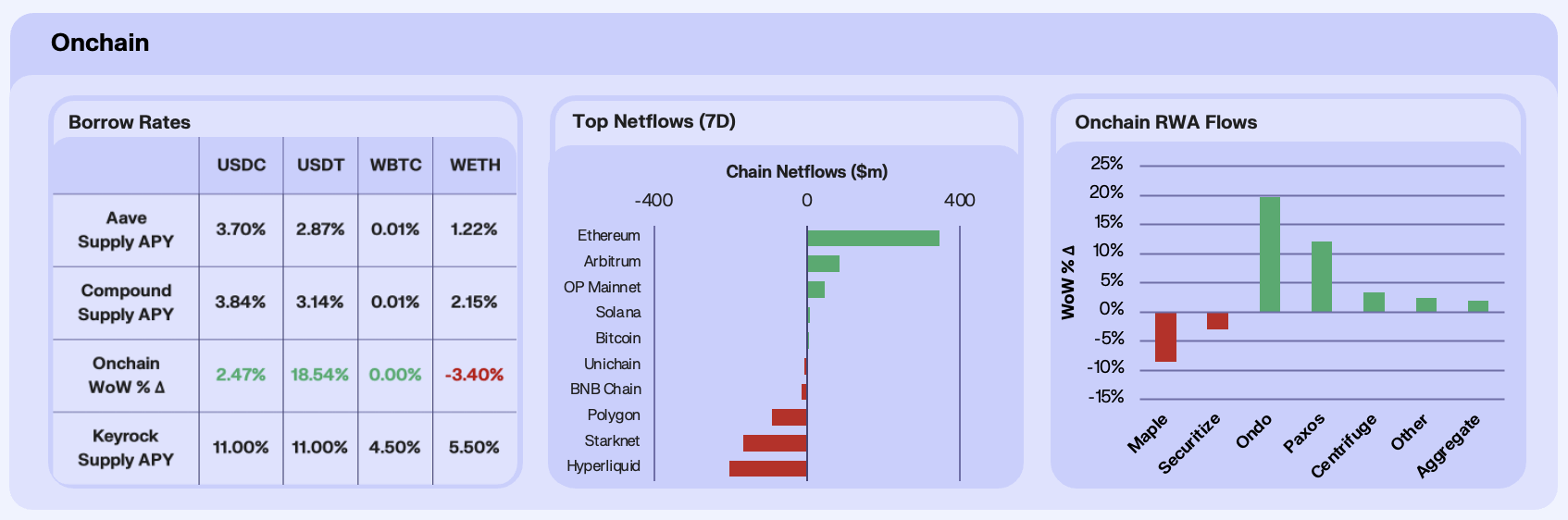

Onchain borrow rates were mixed this week, with stables gaining while volatile, beta-assets, compressed. USDC rates on Aave rose 2.5% WoW, but the primary gainer for the week was USDT, up 18.5% WoW. As we have seen for the whole of January, this move was primarily supply-driven. USDC supply fell 33.5% WoW, and USDT was down 5%. The proportional impact of unit change in supply to unit change in rate for USDT expanding, which points towards demand surges for the stable asset, indicating heightened looping strategies in line with growing onchain speculation. The opposite can be said for USDC, which printed lower than expected rate growth despite a dramatic contraction in supply.

Cross-chain flows reinforced a more defensive re-allocation, where we saw Ethereum lead inflows (+$244m) alongside Arbitrum (+$60m). Here we see capital flowing back to safety in deeper liquidity layers, following a more speculative start to January. Hyperliquid (-$184m) and StarkNet (-$179m) saw meaningful outflows, consistent with traders de-risking from speculative execution venues as volatility picked up and positioning reset. Net-net, we see this week as a clear risk-off rotation of capital.

RWAs continued to grow at the headline level, which aggregated AUM up 1.9% WoW, its fourth consecutive green weekly print. This is relatively unsurprising given the performance of commodities, and the risk off nature of crypto markets pushing allocators into onchain safety, in tokenised gold and treasuries. However, dispersion between the largest protocols this week was extreme. Ondo (+19.8%) and Paxos (+12.1%) did most of the work, while Maple (-8.6%) and Securitize (-3.1%) retraced. The pattern suggests a rotation within RWAs toward more liquid, benchmark-like exposures, which are, as mentioned, treasury and gold-adjacent. We’re seeing that parts of private credit and structured products tend to see more month-end churn when risk appetite wobbles.

Our Take: USDT’s rate jump on only a modest supply drop looks like looping demand coming back, with leverage reappearing, but it’s being expressed through USDT only, not beta nor USDC. Flows rotation reads as a preference for depth and optionality, so any next risk-on leg likely starts on the core rails or with a large migration towards Hyperliquid. RWAs echo that risk-off posture, with bids concentrating in treasuries and gold. We’re looking to capital broadening back into credit or risk on venues to see the start of risk-on onchain rotations.

Solana’s Stablecoin Moment

Solana just printed a new daily ATH in stablecoin swap volume, hitting $1.664b on Jan 21st according to Blockworks Data, up from $78m at the start of the year. This surge in stablecoin volumes is showing up alongside a broader pickup in Solana DEX activity and a materially larger stablecoin base sitting on the chain. The key nuance is where the volume is happening, we’re seeing a growing share being intermediated by proprietary AMMs, notably AlphaQ, and onchain orderbooks, notably Manifest. These venues are typically utilised by professional traders and institutions as opposed to the traditional retail-facing Solana AMM stack.

We see this spike as market-structure evolution in which stablecoin liquidity on Solana is now deep enough that sophisticated players can run tight-spread, high-throughput strategies onchain, such as arbitrage, routing, basis and looping, and MEV-adjacent execution. It also suggests USDC remains the primary quote rail for Solana DeFi, with USDT the key secondary leg, while the venue mix is fragmenting. As mentioned, traditional AMMs still matter for the long tail, but the marginal dollar of stable volume is increasingly price-sensitive and will route to the tightest execution.

Our Take: The stablecoin swap ATH is a signal that Solana is becoming a dollar-stablecoin execution venue, as opposed to what it’s typically known for, as a speculative memecoin chain. This is significant in that the chan now competes on microstructure, such as spreads, fees and routing quality, beyond UX, which it has typically relied on. If volume holds, we believe we’ll see a flywheel of deeper stable liquidity leading to a further tightening of execution, this more flow migrating to Solana and stronger unit economics for the venues controlling routing. The risk to this thesis is that a meaningful portion of this is synthetic churn, i.e. MEV-based, as opposed to organic new end-user payments.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.