13 July 2026

Key Insights: Geopolitics Rewrites Relief

Geopolitics Rewrites Relief

Every Monday, we deliver a concise yet comprehensive briefing to help you navigate the week ahead.

Our weekly market dashboard brings together key insights across Macro, Crypto, and Onchain activity, distilled into a clear, actionable format. Whether you’re managing risk or spotting opportunity, start the week informed and aligned.

Join our Telegram Channel to get it delivered directly to your phone.

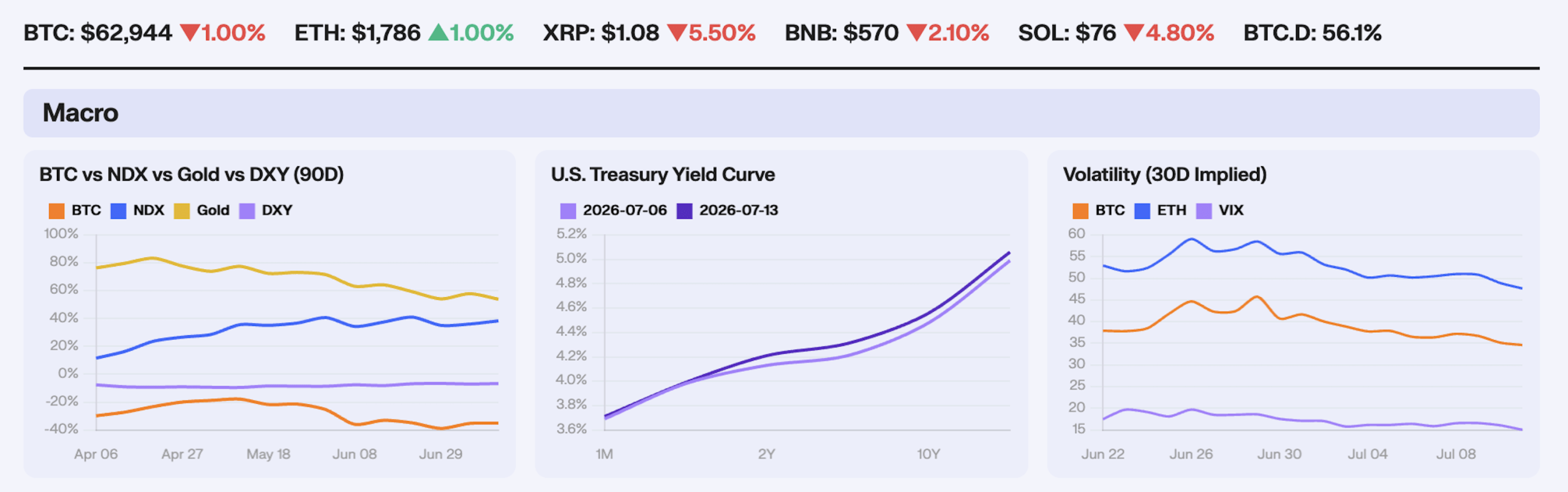

Risk assets gave back the prior week’s macro relief as Middle East tensions resurfaced and the Fed minutes reminded markets the inflation fight is not over. BTC slipped -1% to $62,944 and gold fell -2.5% to $4,057 after both had bounced hard into the July 4 jobs miss, while the Nasdaq still added +1.7% to 29,825 as chip names recovered from the prior week’s positioning unwind. The dollar firmed +0.34% to $101.08, a modest move but enough to show the post-payrolls soft-dollar bid had run its course once geopolitical risk returned to the tape.

Yields moved higher as markets repriced inflation risk back into the rate path. The move was led by the long end, with the 10-year rising +8bp to 4.56% and the 30-year reaching 5.06%, while shorter maturities barely moved. The catalyst was Wednesday’s dual hit of June FOMC minutes flagging upside inflation risks from Middle East energy, tariffs, and AI-related cost pressures, alongside President Trump’s declaration at the NATO summit in Ankara that the Iran ceasefire is “over” after US strikes on Hormuz shipping. CME FedWatch still prices roughly a 49-53% chance of a September hike, little changed from last week’s post-NFP fade near 55%, with July hold odds above 70%. Higher long-end yields are keeping financial conditions tight and limiting how far risk assets can run on a single soft data point.

Volatility compressed further even as macro risk repriced. BTC 30-day implied vol fell -5.2% to 34.6, ETH IV dropped -5.0% to 47.7, and the VIX slid -8.4% to 15.0 through July 11, extending the post-selloff compression from prior weeks. The surface is still low for the size of the macro overhang, with the September hike again priced as a live outcome rather than a fading tail risk. On Deribit, BTC options open interest sits at 370,863 contracts at a 0.55 put-call ratio, with August $60,000 puts marking near 39 vol against 36 vol on $65,000 calls, so downside skew remains rich even as the at-the-money surface only nudged higher. For investors who think this geopolitical spike will fade without breaking the range, selling call options remains a way to harvest the vol that returned to the surface.

Our Take: Last week’s relief trade met two walls this week, a Fed that still sees inflation risks to the upside and a Middle East conflict the market had filed under “de-escalating.” Bitcoin and gold gave back the NFP bounce while equities held up on tech, the classic split when rates and oil are moving against duration-sensitive hedges but AI beta still has a bid. The 10-year back at 4.56% and the long end within a few basis points of 5% tell us the September hike is still very much live. The line we watch into next week is whether Hormuz stays hot through the July 28 FOMC, since energy-led inflation scares are what keep hike odds near coin-flip and cap any sustained BTC recovery.

Ethereum Takes the Bid

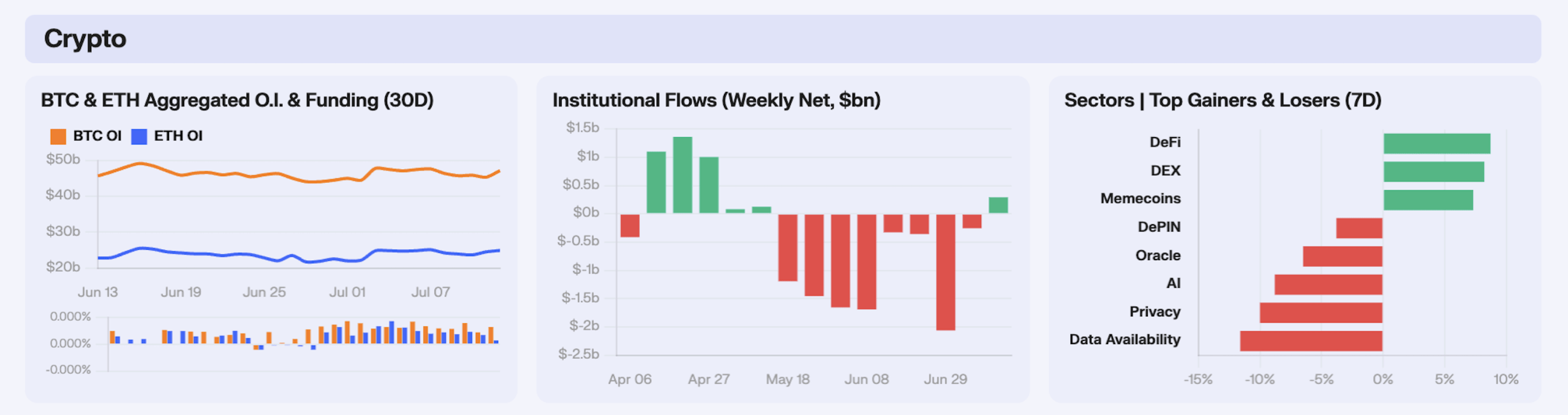

Bitcoin open interest described a full round-trip over the week, opening Monday near $47.5B, printing a weekly high of $47.65B on 7 July before flushing -4% to $45.75B by 9 July and then rebuilding into Sunday to close at $47.2B. This represents a net -0.6% WoW that flatters how much positioning actually changed hands underneath. Ethereum traced the same arc with more amplitude, peaking at $25.1B on 7 July, shedding -5.8% to a $23.65B trough on 10 July, then recovering the entire move to finish the week at its high of $24.9B, a cleaner rebuild than Bitcoin managed and the first indication that the marginal bid was skewing toward ETH. What matters more than the levels is that funding never once flipped negative on either asset yet stayed muted. The configuration reads as a positioning cleanse rather than a leverage build, because open interest was rebuilt to the week’s highs at the very moment funding reset from its lows, which tells us the longs that returned did so cheaply and without paying up, the healthiest setup available after a mid-week flush that lined up precisely with the two ETF outflow days.

The more consequential development was Bitcoin and Ethereum spot ETF products snapping eight-week outflow streaks in the same week, the first synchronised turn since the drawdown began. Bitcoin funds absorbed +$197.4M net to lift AUM to ~$77.42B and cumulative inflows since launch to ~$51.33B, with BlackRock again the marginal allocator behind the reversal, though the weekly figure disguises how narrowly it was won, since 6 July alone delivered +$265.7M and was very nearly handed back through outflows of -$84.9M and -$95.3M on the 8th and 9th before a +$90.4M Friday close salvaged the print. Ethereum funds took in +$84.4M to reach ~$9.59B in AUM and ~$11.00B cumulative. The proportional comparison is where the signal lives, because ETH’s +$84.4M against a $9.59B base is roughly 0.9% of AUM versus just 0.25% for Bitcoin, so on a size-adjusted basis Ethereum drew more than three times the relative demand, and it did so while spot funding stayed muted, which means the bid was cash driven rather than levered.

Beneath the index, sector dispersion told a coherent rotation story, in which DeFi led at roughly +8.7% WoW on the back of Uniswap (UNI) +15.8% and Aave (AAVE) +12.0%, with the closely related DEX complex just behind at +8.2% as Jupiter (JUP) +16.0% and Uniswap did the heavy lifting. The fact that the two leading sectors are the most direct expressions of Ethereum beta is no coincidence given the flow picture above. Memecoins ranked third near +7.3%, but the internal split is the more instructive detail, with the Solana-native pair of Bonk (BONK) +16.9% and dogwifhat (WIF) +14.2% running hard while Dogecoin (DOGE) +4.3% and Shiba Inu (SHIB) +0.9% were left behind, a sign that speculative retail appetite is concentrated in the Solana complex. The AI laggard is the point worth holding onto, because capital rotated out of last cycle’s marquee narrative and into ETH-beta DeFi, which is exactly what the early innings of a Ethereum-led leg would look like.

Our Take: The eight-week streak break will get the airtime, but it is a thinner result than the headline suggests, because stripping out the single 6 July print of +$265.7M leaves Bitcoin ETFs flat-to-negative across the other four sessions and rests the entire reversal on one Monday rebalance rather than any durable shift in demand. The signal we would actually emphasise sits with Ethereum, and this week three unrelated instruments point the same way, in that ETH ETFs outdrew Bitcoin more than threefold on a size-adjusted basis, the ETH open-interest recovery was visibly cleaner, and the sectors that led were the purest ETH-beta expressions in DeFi at +8.7% and DEX. Confirmation comes down to two prints next week, a second consecutive positive week for ETH ETFs and the ETH/BTC ratio holding its gain, and if the Monday flow disappoints then the streak-break was a one day rebalance rather than a regime change.

Spot Accumulation Confirmed

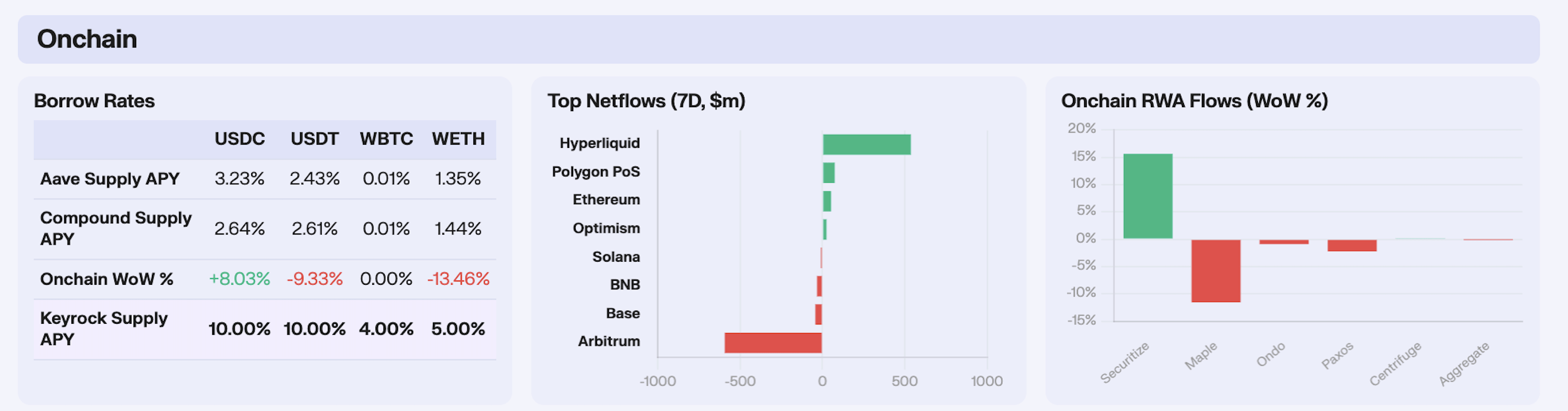

The onchain lending picture was defined by a pronounced reshuffle of deposits rather than any move in the headline rates, and the standout was WETH, where Aave deposits surged +62.67% WoW while the supply APY fell -13.46%. A wall of fresh WETH supply against a collapsing rate is the cleanest signal you get that ETH holders are choosing to park spot and earn yield, and it lines up with the cash-driven ETH bid we flagged in crypto. The stablecoin side told a rotation story of its own. USDC deposits drained -26.42% as its APY backed up +8.03%, while USDT ran the mirror image, deposits swelling +28.17% and the rate compressing -9.33%.

Chain-level flows were dominated by a near one-for-one rotation between two venues. Arbitrum bled -$593.5M on the week while Hyperliquid pulled in +$535.9M, the two moves so closely matched that most of the half-billion-plus leaving Arbitrum looks to have crossed straight into Hyperliquid’s chain. That migration is the onchain expression of the perp-DEX consolidation we’ve tracked for months, with liquidity and traders concentrating on Hyperliquid. The more telling smaller number was Ethereum mainnet, which took in a net +$51.5M to sit third on the inflow table, a print that squares with the spot-driven ETH bid running through both the ETF and Aave data this week. Polygon PoS led the remainder with +$73.4M and Optimism added +$23.7M, while the outflow side beyond Arbitrum was comparatively modest, with Base down -$43.6M, BNB -$33.4M and Solana off just -$9.9M. That last one is worth flagging, because Solana’s memecoins were among the week’s strongest performers yet the chain still saw a small net outflow, a sign the activity was speculative churn rather than fresh capital arriving.

Aggregate RWA AUM finished the week essentially unchanged at -0.02% WoW, but the flat headline masked sharp dispersion between the two ends of the tokenisation spectrum. Securitize led with a +15.61% weekly gain in assets as the tokenised-fund and treasury venue kept pulling institutional capital, while Maple sat at the opposite extreme with a -11.57% contraction as redemptions or maturities rolled out of its lending pools. The Maple move is worth pausing on, because its SYRUP token was at the same time the best-performing RWA name on price at +16.7% over the week, and a token rallying while the protocol’s own asset base shrinks is the kind of gap between speculative positioning and onchain fundamentals that rarely lasts, with the fundamentals usually the side that wins. The rest of the majors were quiet, with Ondo off a marginal -0.90%, Paxos -2.24%, Centrifuge flat at +0.11% and the residual other cohort -0.20%, leaving Securitize as effectively the only source of net growth in the sector this week.

Our Take: The onchain tape is the strongest corroboration of this week’s ETH story, and it comes from an entirely different dataset than the ETF flows. WETH deposits on Aave jumped +62.67%, and Ethereum mainnet drew a net +$51.5M while the major L2s bled capital, so holders are accumulating spot ETH and putting it to work, the same behaviour the muted funding implied. The USDC to USDT shuffle and the flat RWA aggregate are second- order by comparison.

Memes Before Equities

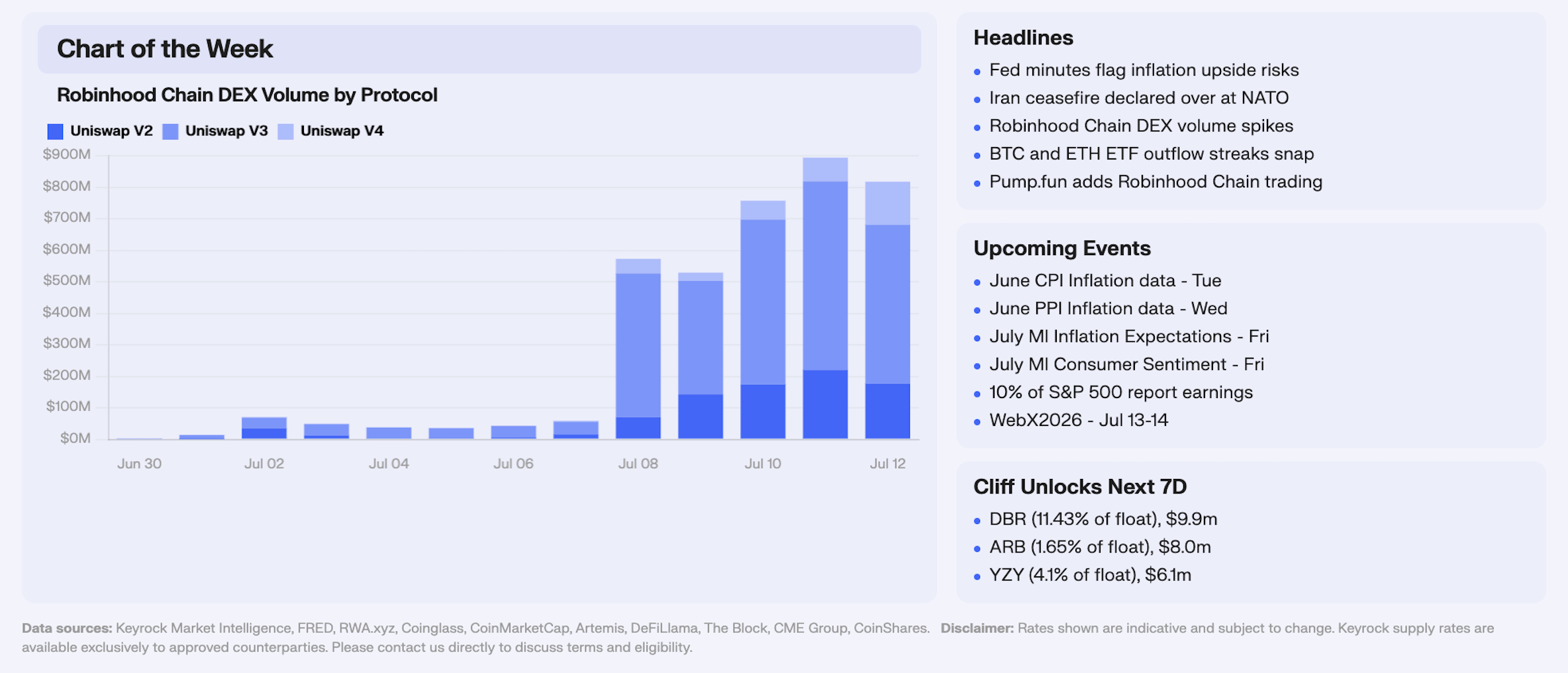

Robinhood Chain went public on July 1 as an Arbitrum-based L2 pitched for tokenized stocks and real-world assets with Uniswap, Morpho, and Chainlink on day one. However, it was the meme narrative that drove the primary traction on the chain. A memecoin rush led by CASHCAT (built around Robinhood’s old “Cash Cat” mascot), Pump.fun adding Robinhood Chain tokens on July 8 with SOL-denominated trading and no bridging, and CEO Vlad Tenev endorsing the trade on X (“it works great for memes too”) converged the same day. That is a sharp reversal from his July 2 CNBC line that memecoins without utility were a dead end. The chain was built for RWAs; retail speculation set the tone in week one.

Volume was negligible through late June, then $14.7M on July 1 at mainnet launch, $58.8M on July 7, and $572.8M on July 8, roughly 10x the prior day and 39x launch-day flow. Uniswap V3 took $456.3M of the July 8 total (80%), with V2 at $70.4M and V4 at $46.0M. The frenzy did not fade the next day as July 9–12 held $529M to $894M daily, peaking on July 11 at $893.8M as V3 took $597.8M, V2 $220.6M, and V4 $75.4M. Secondary Dune dashboards put ~193,000 daily active addresses on July 8, ~140,000 first-time wallets, and ~16,600 new tokens minted in 24 hours, with CASHCAT alone drawing ~8,700 unique traders and crossing ~$200M market cap. Tokenized RWAs on the chain remained a sliver, Entropy Advisors’ dashboard puts total tokenized asset value near $12.8M, a fraction of one day’s meme volume.

The spike is due to launchpad economics ported onto a chain with a built-in retail brand. Pump.fun routing Robinhood tokens into SOL removes the friction that usually caps early-L2 speculation, and Tenev’s public embrace gave the trade legitimacy from the top. Uniswap founder Hayden Adams noted the July 8 print ranked behind only Ethereum mainnet in single-day DEX volume, remarkable for a network eight days old, but concentrated in WETH pairs and meme flows. Ethena’s ~$50M USDG deposit into Morpho drove the headline TVL jump, while memes drove transactions, addresses, and DEX prints.

Our Take: Robinhood Chain’s record week is a distribution story more than an RWA story. The infrastructure for tokenized equities is live, but the volume that mattered was memecoins, CASHCAT first, then a flood of Robinhood-themed launches once Pump.fun opened the SOL on-ramp. That is not necessarily bearish for the chain long term; it is how new L2s have historically bootstrapped liquidity and user counts before the “serious” use case catches up. The test over the next few weeks is whether any of those wallets stick once CASHCAT mean-reverts, and whether DEX volume on stock-token pairs builds a second leg.

Join our Telegram Channel to get it delivered directly to your phone.

Stay up to date

Get the latest industry insights, in-house research and Keyrock updates.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.